Coconut Water Drinks Market Size

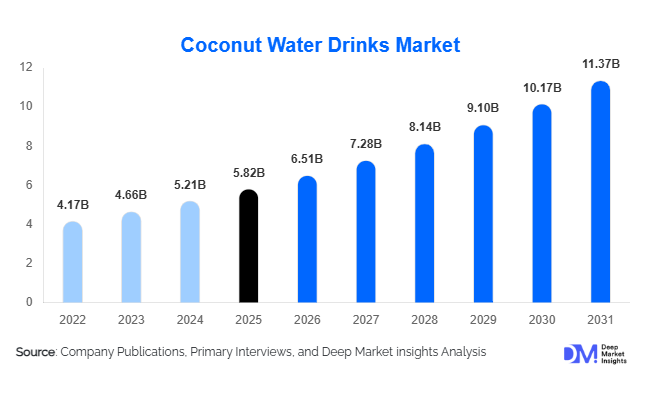

According to Deep Market Insights, the global coconut water drinks market size was valued at USD 5.82 billion in 2025 and is projected to grow from USD 6.51 billion in 2026 to reach USD 11.37 billion by 2031, expanding at a CAGR of 11.8% during the forecast period (2026–2031). The coconut water drinks market growth is primarily driven by increasing consumer preference for natural hydration beverages, rising awareness regarding plant-based nutrition, and growing demand for clean-label functional drinks with electrolyte-rich formulations.

Key Market Insights

- Consumers are increasingly replacing carbonated soft drinks with natural hydration beverages, accelerating global demand for coconut water drinks.

- Functional coconut water formulations enriched with vitamins, probiotics, and electrolytes are rapidly expanding, particularly across premium wellness beverage categories.

- Asia-Pacific dominates the global market, supported by strong coconut cultivation, expanding domestic beverage industries, and rising health-conscious consumption.

- North America remains one of the largest premium consumption markets, led by strong adoption among fitness-focused and vegan consumers.

- Europe is emerging as the fastest-growing regional market, driven by demand for organic, low-calorie, and sustainable beverage alternatives.

- Sustainable packaging innovation, including recyclable tetra packs and aluminum cans, is reshaping product positioning and consumer purchasing behavior.

What are the latest trends in the coconut water drinks market?

Functional and Fortified Coconut Water Beverages Gaining Momentum

Manufacturers are increasingly launching functional coconut water beverages that provide benefits beyond basic hydration. Coconut water drinks fortified with probiotics, collagen, vitamins, adaptogens, protein, and botanical extracts are gaining strong traction among fitness enthusiasts and health-conscious consumers. The trend is particularly prominent in North America, Europe, Japan, and South Korea, where premium wellness beverages are witnessing significant demand growth. Beverage brands are positioning coconut water as a natural sports recovery solution and a healthier alternative to synthetic energy drinks. Functional formulations are also enabling companies to command premium pricing and differentiate themselves within an increasingly competitive beverage landscape.

Sustainable Packaging and Clean-Label Innovation

Sustainability is becoming a central focus across the coconut water drinks industry. Beverage manufacturers are adopting recyclable tetra packaging, lightweight aluminum cans, and bio-based plastic alternatives to align with environmentally conscious consumer preferences. Simultaneously, clean-label beverage demand is encouraging companies to reduce preservatives, artificial sweeteners, and additives in coconut water formulations. Consumers increasingly favor minimally processed beverages with transparent ingredient labeling and ethical sourcing certifications. Sustainable sourcing partnerships with coconut farmers in Southeast Asia and Latin America are also strengthening brand value while supporting long-term supply chain resilience.

What are the key drivers in the coconut water drinks market?

Growing Demand for Natural Hydration Beverages

One of the primary drivers supporting the coconut water drinks market is the global shift toward healthier beverage alternatives. Consumers are increasingly avoiding sugary carbonated drinks and synthetic sports beverages due to growing concerns related to obesity, diabetes, and lifestyle-related diseases. Coconut water is perceived as a natural electrolyte-rich beverage containing potassium, magnesium, and hydration benefits with comparatively lower calorie content. This transition toward plant-based hydration solutions is significantly expanding the consumer base across developed and emerging economies.

Expansion of Fitness and Sports Nutrition Culture

The rapid expansion of fitness culture, gym memberships, and sports nutrition consumption is accelerating demand for coconut water drinks globally. Athletes and active consumers increasingly prefer coconut water as a natural post-workout hydration beverage due to its electrolyte composition and clean-label positioning. Sports hydration applications are growing particularly strongly in the United States, Canada, Australia, Germany, and urban Asia-Pacific markets. Beverage manufacturers are capitalizing on this trend through sports-focused marketing campaigns and product innovations tailored to fitness-conscious consumers.

Rising Popularity of Plant-Based and Vegan Diets

The increasing adoption of vegan and plant-based lifestyles is also contributing substantially to market expansion. Coconut water aligns strongly with consumer demand for dairy-free, naturally sourced, and minimally processed beverages. Millennials and Gen Z consumers increasingly prioritize plant-based nutrition and sustainable beverage consumption, encouraging retailers and beverage companies to expand coconut water product portfolios globally.

What are the restraints for the global market?

Raw Material Price Volatility and Supply Chain Risks

The coconut water drinks market remains highly dependent on coconut-producing tropical economies such as the Philippines, Indonesia, Thailand, Vietnam, Brazil, and India. Climatic disruptions, typhoons, crop diseases, and seasonal agricultural fluctuations can significantly impact coconut supply and increase raw material prices. These supply-side uncertainties create operational challenges for beverage manufacturers and may negatively impact production margins during periods of reduced coconut availability.

Premium Product Pricing Limiting Mass Adoption

Coconut water beverages are often priced significantly higher than conventional soft drinks, flavored beverages, and bottled water products. Premium organic formulations, cold-pressed variants, and imported products particularly face pricing pressure in price-sensitive economies. Packaging costs, cold-chain logistics, and export transportation expenses further increase retail pricing, limiting broader mass-market penetration despite rising consumer awareness regarding health benefits.

What are the key opportunities in the coconut water drinks industry?

Premium Functional Beverage Expansion

The growing global functional beverage industry presents significant opportunities for coconut water manufacturers. Beverage companies are increasingly integrating coconut water into immunity drinks, digestive wellness beverages, protein-enhanced hydration solutions, and botanical wellness formulations. Premium functional hydration beverages are expected to witness strong growth among affluent urban consumers, athletes, and wellness-focused millennials. Companies that successfully integrate science-backed functional ingredients with clean-label positioning are likely to gain substantial competitive advantages.

Emerging Market Consumption Growth

Emerging economies across Asia-Pacific, the Middle East, and Africa represent major untapped opportunities for coconut water beverage manufacturers. Urbanization, rising disposable incomes, expanding organized retail infrastructure, and westernized consumption habits are accelerating packaged beverage demand in countries such as India, Indonesia, Vietnam, Saudi Arabia, and the UAE. Governments across coconut-producing economies are also supporting agro-processing infrastructure development and beverage exports, creating favorable investment opportunities for both domestic and international beverage companies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.82 Billion |

| Market Size in 2026 | USD 6.51 Billion |

| Market Size in 2031 | USD 11.37 Billion |

| CAGR | 11.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global coconut water drinks market is witnessing substantial expansion as consumers increasingly shift toward natural hydration beverages, clean-label formulations, and plant-based wellness products. Among all product categories, pure coconut water continues to dominate the global market, accounting for nearly 48% of total market revenue in 2025. The dominance of this segment is primarily driven by growing consumer preference for minimally processed beverages that are free from artificial preservatives, synthetic sweeteners, and chemical additives. Consumers across developed economies are increasingly prioritizing authenticity, nutritional transparency, and naturally sourced hydration solutions, which has significantly strengthened the market position of pure coconut water products. The segment is also benefiting from rising awareness regarding the electrolyte-rich composition of coconut water, particularly potassium, magnesium, and natural minerals that support hydration and recovery.Sparkling coconut water products are also gaining considerable traction as consumers seek healthier alternatives to traditional carbonated beverages and sugary sodas. The segment is benefiting from growing demand for low-calorie sparkling drinks that offer natural ingredients and refreshing taste profiles. Beverage brands are increasingly targeting urban consumers who desire premium lifestyle beverages with functional benefits and reduced sugar content. Organic coconut water beverages continue to witness robust growth due to increasing awareness regarding sustainable agriculture, pesticide-free cultivation, and environmentally responsible sourcing practices. Organic certification has become an important purchasing factor among premium consumers, particularly across Europe and North America where demand for ethical and sustainable food and beverage products remains exceptionally strong.

Packaging Type Insights

Packaging innovation plays a critical role in shaping product distribution, shelf stability, consumer convenience, and brand positioning within the global coconut water drinks market. Tetra pack packaging remains the dominant packaging segment, accounting for nearly 53% of global market revenue in 2025. The leading position of this segment is primarily supported by its superior shelf-life extension capabilities, portability, lightweight structure, and suitability for international transportation and export distribution. Beverage manufacturers increasingly prefer aseptic tetra packaging because it helps preserve nutrients, flavor quality, and freshness while reducing refrigeration dependency during logistics and retail storage. The ability of tetra packaging to support large-scale global trade operations has become particularly important as international demand for coconut water beverages continues expanding across developed economies.Flexible pouch packaging is also emerging rapidly within travel-oriented beverage applications, children's beverage categories, and sports nutrition markets. Flexible pouches offer lightweight transportation advantages, reduced packaging material usage, and enhanced convenience for mobile consumers. The growing expansion of single-serve beverage formats and compact packaging solutions is expected to create additional growth opportunities for flexible packaging manufacturers over the coming years. As beverage consumption patterns continue evolving toward convenience-focused lifestyles, packaging innovation will remain a major competitive factor within the global coconut water drinks industry.

Distribution Channel Insights

Distribution channel expansion continues to play a central role in accelerating the global penetration of coconut water beverages across diverse consumer demographics and geographic regions. Supermarkets and hypermarkets remain the dominant distribution channel, accounting for nearly 42% of global sales in 2025. The leadership of this segment is primarily driven by extensive product visibility, large retail shelf space availability, strong promotional activities, and high-volume consumer traffic. Organized retail channels allow beverage companies to showcase multiple product variants, packaging formats, and premium offerings simultaneously, thereby encouraging impulse purchases and enhancing overall brand exposure.Health food stores and specialty beverage retailers continue to play an important role in premium product positioning and consumer education. These channels are especially influential for organic coconut water beverages, functional wellness drinks, and clean-label product categories targeting health-conscious consumers. Specialty retailers often provide detailed product information, nutritional guidance, and premium brand exposure that support higher-value purchasing decisions. Growing consumer trust in specialty wellness retailers is further strengthening the market presence of premium coconut water formulations.Foodservice channels including cafes, hotels, gyms, airlines, restaurants, and corporate wellness programs are also emerging as significant demand generators for branded coconut water beverages. The increasing incorporation of natural hydration drinks into wellness-oriented menus and hospitality offerings is enhancing product accessibility across both leisure and professional consumption environments. Fitness centers and sports facilities are particularly important distribution points due to rising demand for post-workout hydration beverages and natural electrolyte replenishment solutions. As consumer lifestyles continue prioritizing convenience, wellness, and premium beverage experiences, distribution channel diversification will remain essential for long-term market growth.

Consumer Group Insights

The global coconut water drinks market serves a highly diversified consumer base driven by evolving health preferences, active lifestyles, and growing awareness regarding natural hydration benefits. Fitness and sports consumers represent one of the largest demand segments within the market due to increasing preference for natural electrolyte beverages that support hydration, endurance, and muscle recovery. Coconut water has gained strong popularity among athletes and physically active consumers because of its naturally occurring potassium and mineral content, which provides an effective alternative to synthetic sports drinks. The increasing participation in gym memberships, fitness programs, endurance sports, and recreational physical activities is significantly accelerating demand across this consumer segment.Vegan and plant-based consumers are also contributing substantially to market growth as coconut water becomes increasingly recognized as a dairy-free and naturally sourced hydration solution. The broader expansion of plant-based diets, vegan lifestyles, and environmentally conscious food consumption patterns is supporting higher demand for naturally derived beverages. Coconut water products align well with sustainability-oriented consumer values and ethical purchasing preferences, particularly in developed markets where plant-based food adoption continues expanding rapidly.Pediatric and family-oriented demand is gradually increasing as parents seek healthier beverage alternatives for children compared to traditional sugar-rich soft drinks and artificially flavored juices. Coconut water products with lower sugar content, natural ingredients, and added nutritional benefits are increasingly being incorporated into family consumption habits. Manufacturers are responding by introducing child-friendly flavors, smaller packaging formats, and fortified beverage variants that appeal to family-oriented consumers seeking balanced nutritional options.

End-Use Insights

Direct beverage consumption remains the dominant end-use segment within the global coconut water drinks market, accounting for more than 58% of global demand in 2025. The leading position of this segment is primarily supported by rising consumer preference for ready-to-drink natural hydration beverages that can be consumed conveniently throughout the day. Increasing urbanization, busy lifestyles, and on-the-go consumption habits are encouraging consumers to choose packaged coconut water products as convenient hydration solutions. The growing shift away from sugary carbonated beverages toward healthier ready-to-drink alternatives continues to strengthen demand within this segment globally.The hospitality and foodservice sector is increasingly integrating premium coconut water beverages into wellness-oriented menus across hotels, cafes, luxury resorts, restaurants, and travel hospitality environments. Premium hospitality brands are leveraging consumer demand for healthier beverage experiences by incorporating coconut water into breakfast offerings, spa menus, detox programs, and tropical beverage selections. Airlines and premium travel operators are also increasingly offering coconut water beverages as part of enhanced wellness-focused passenger experiences.Functional beverage manufacturers are utilizing coconut water as a base ingredient in immunity drinks, wellness tonics, nutritional beverages, and fortified hydration products. The increasing popularity of multifunctional beverages that combine hydration with immunity support, digestive health, and energy enhancement is creating new commercial opportunities for coconut water integration across broader beverage formulations. Additionally, smoothie blending applications, meal replacement beverages, and nutraceutical drink formulations are expanding the commercial utilization of coconut water across both developed and emerging markets.

Explore more data points, trends and opportunities Download Free Sample Report

Coconut Water Drinks Market Segmentations

By Product Type

- Pure Coconut Water

- Flavored Coconut Water

- Functional Coconut Water Drinks

- Sparkling Coconut Water

- Coconut Water Juice Blends

- Organic Coconut Water Drinks

- Low-Calorie

By Nature

- Organic

- Conventional

By Packaging Type

- Tetra Packs

- PET Bottles

- Glass Bottles

- Aluminum Cans

- Flexible Pouches

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health Stores

- Online Retail & E-commerce

- Foodservice Channels

- Direct-to-Consumer (DTC)

By Consumer Group

- Fitness & Sports Consumers

- Health-Conscious Adults

- Millennials & Gen Z

- Vegan & Plant-Based Consumers

- Pediatric/Natural Beverage Consumers

Regional Insights

North America

North America accounted for nearly 29% of the global coconut water drinks market in 2025, led primarily by the United States. The region continues to experience strong market expansion due to rising consumer demand for plant-based beverages, clean-label hydration products, and natural sports nutrition drinks. Increasing health consciousness among American consumers is significantly accelerating the replacement of sugary soft drinks with functional hydration alternatives such as coconut water. The growing prevalence of fitness culture, gym memberships, active lifestyle adoption, and preventive health awareness remains a major driver supporting long-term regional market growth.Canada is witnessing steady growth driven by expanding health-focused retail chains, growing e-commerce beverage sales, and increasing consumer awareness regarding natural hydration benefits. The rapid adoption of vegan lifestyles and environmentally responsible consumption patterns is further contributing to regional demand. Additionally, rising multicultural populations and growing exposure to tropical beverage consumption trends are enhancing coconut water market expansion throughout North America.

Europe

Europe accounted for approximately 22% of the global coconut water drinks market in 2025 and remains one of the fastest-growing regional markets globally. Germany, the United Kingdom, France, Spain, Italy, and the Netherlands represent major demand centers due to increasing consumer preference for organic, low-sugar, and environmentally sustainable beverage products. European consumers strongly prioritize clean-label nutrition, ethical sourcing, and sustainable packaging solutions, which significantly supports the adoption of premium coconut water beverages.The rapid growth of veganism and plant-based dietary trends across Europe is also strengthening market demand. Consumers increasingly seek dairy-free and naturally sourced hydration products that align with sustainable lifestyle values. European retailers are expanding shelf space for organic and wellness-oriented beverages, while beverage brands are investing heavily in recyclable packaging and carbon-neutral sourcing strategies. Furthermore, premiumization trends across Western Europe are encouraging consumers to purchase imported organic coconut water products with ethical and sustainable certifications.

Asia-Pacific

Asia-Pacific dominates the global coconut water drinks market with nearly 36% market share in 2025 and remains the most important production and consumption hub globally. Countries including India, Thailand, Indonesia, Vietnam, the Philippines, and Sri Lanka benefit from extensive coconut cultivation ecosystems, favorable climatic conditions, abundant agricultural resources, and rapidly expanding beverage manufacturing industries. The region’s strong raw material availability significantly supports large-scale production and export competitiveness.China and Japan are experiencing increasing imports of premium coconut water beverages driven by wellness trends, premium beverage consumption, and growing consumer interest in functional nutrition products. Rising health awareness among younger urban populations is encouraging higher demand for low-sugar and naturally sourced beverages. Southeast Asia remains critically important for both regional consumption and export-oriented beverage manufacturing due to strong coconut production infrastructure and lower processing costs. Government support for agro-processing industries and food exports across several Southeast Asian economies is further strengthening the region’s global market leadership.

Latin America

Latin America remains strategically important within the global coconut water drinks market due to Brazil’s dominant coconut production industry and rapidly expanding domestic beverage sector. Brazil serves as both a major producer and exporter of coconut water products while simultaneously witnessing strong growth in domestic consumption of natural hydration beverages. Rising consumer awareness regarding healthy lifestyles, sports nutrition, and low-calorie beverage alternatives is significantly supporting market expansion across urban populations.Mexico and Argentina are gradually emerging as important growth markets due to expanding organized retail networks, rising disposable incomes, and increasing health-conscious consumer populations. The expansion of supermarkets, convenience stores, and wellness retail chains is improving product accessibility and supporting greater market penetration. Additionally, regional tourism growth and hospitality sector expansion are contributing to increased demand for premium coconut-based beverages across Latin America.

Middle East & Africa

The Middle East & Africa region is witnessing accelerating demand for premium functional beverages, particularly across the UAE, Saudi Arabia, Qatar, Kuwait, and South Africa. Rising disposable incomes, expanding expatriate populations, luxury retail growth, and increasing wellness-focused consumption patterns are driving higher imports of coconut water beverages throughout the region. Consumers increasingly prefer premium hydration drinks that align with fitness-oriented lifestyles and modern health trends.South Africa represents one of the leading African markets due to rising urbanization, growing health awareness, and increasing adoption of premium wellness beverages among middle-income consumers. Additionally, several African tropical economies are investing heavily in coconut cultivation, agro-processing infrastructure, and export-oriented agricultural industries. Expanding agricultural investments and government support for food processing industries are expected to strengthen the region’s role within the global coconut water supply chain over the forecast period.

Key Players in the Coconut Water Drinks Market

- The Vita Coco Company

- PepsiCo

- The Coca-Cola Company

- Harmless Harvest

- Amy & Brian Naturals

- Taste Nirvana

- Maverick Brands

- C2O Pure Coconut Water

- FOCO

- Tradecons GmbH