Coconut Milk and Cream Stabilizer Market Size

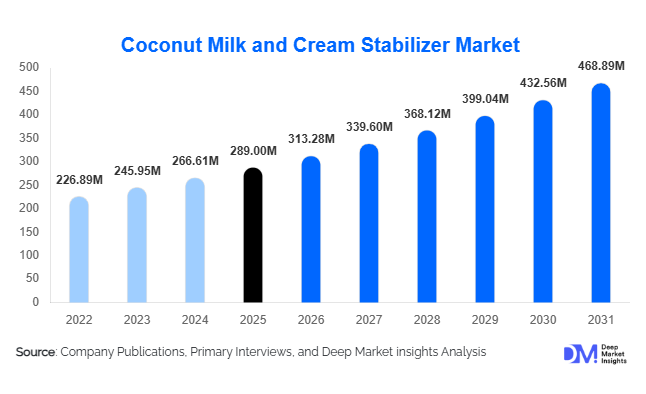

According to Deep Market Insights, the global coconut milk and cream stabilizer market size was valued at USD 289 million in 2025 and is projected to grow from USD 313.28 million in 2026 to reach USD 468.89 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). Market growth is primarily driven by the rapid expansion of plant-based dairy alternatives, increasing exports of shelf-stable coconut milk from Southeast Asia, and rising demand for clean-label hydrocolloid and emulsifier systems that enhance texture, prevent phase separation, and extend shelf life in coconut-based beverages and desserts.

Key Market Insights

- Hydrocolloids dominate product demand, accounting for over 40% of global stabilizer consumption due to their superior thickening and water-binding functionality.

- Asia-Pacific leads production, supported by strong coconut processing industries in Thailand, Indonesia, and the Philippines.

- North America is the fastest-growing consumption region, driven by rising demand for dairy alternatives and clean-label beverages.

- Powdered stabilizers account for more than 70% of market share, owing to longer shelf life and ease of industrial blending.

- Direct B2B contracts dominate distribution, as food processors secure long-term ingredient supply agreements.

- Clean-label reformulation and non-GMO ingredient sourcing are reshaping product development strategies globally.

What are the latest trends in the coconut milk and cream stabilizer market?

Clean-Label and Natural Hydrocolloid Blends

Manufacturers are increasingly shifting toward plant-derived stabilizers such as guar gum, locust bean gum, and xanthan gum to meet clean-label demands. Synthetic emulsifiers are gradually being replaced or reduced in favor of multifunctional natural blends. Food processors are seeking stabilizer systems that deliver viscosity, emulsion stability, and improved mouthfeel with minimal ingredient declaration complexity. Organic-certified and non-GMO stabilizer solutions are gaining traction, particularly in North America and Europe, where consumer awareness of ingredient sourcing is high.

Customized Stabilizer Systems for Barista and RTD Applications

The growth of barista-style coconut milk and ready-to-drink (RTD) beverages is driving demand for tailored stabilizer systems that enhance frothing, heat stability, and suspension performance. Ingredient companies are investing in precision blending technologies and application labs to co-develop solutions with beverage brands. These customized blends command premium margins and support long-term B2B supply partnerships.

What are the key drivers in the coconut milk and cream stabilizer market?

Expansion of Plant-Based Dairy Alternatives

The global dairy alternatives industry continues to expand at high single-digit to double-digit growth rates. Coconut milk remains one of the leading non-dairy bases for beverages, desserts, curries, and yogurt alternatives. Stabilizers are essential in preventing oil-water separation, improving creaminess, and ensuring product consistency during storage and transportation. As private label brands and multinational food companies expand plant-based portfolios, stabilizer demand rises proportionally.

Export Growth from Southeast Asia

Thailand, Indonesia, and the Philippines are major exporters of packaged coconut milk products. Shelf-stable exports to the U.S., Germany, the UAE, and Japan require advanced stabilizer systems that ensure 12–18 months of product stability. Export-oriented manufacturing growth directly stimulates upstream demand for hydrocolloids, emulsifiers, and blended stabilizer systems.

What are the restraints for the global market?

Raw Material Price Volatility

Hydrocolloid raw materials such as guar gum and locust bean gum are agriculturally dependent and subject to weather variability and trade restrictions. Price fluctuations directly impact stabilizer production costs and profit margins, particularly for small and mid-sized manufacturers.

Regulatory Scrutiny on Additives

Certain emulsifiers and carrageenan variants face regulatory reviews and consumer perception challenges in Western markets. Reformulation efforts increase R&D costs and can temporarily disrupt supply chains.

What are the key opportunities in the coconut milk and cream stabilizer industry?

Premium and Organic Coconut Product Expansion

The premiumization of coconut-based beverages and desserts presents a major opportunity. Organic-certified and minimally processed stabilizer blends are in demand among high-end retail and specialty brands. Manufacturers offering customized, clean-label systems can secure long-term supply agreements and higher margins.

Emerging Applications in Coconut Yogurt and Vegan Cream

Coconut yogurt and plant-based whipping cream segments are growing at over 10% annually. These applications require advanced stabilization to mimic dairy textures, opening opportunities for innovation in protein-starch-hydrocolloid blends.

Product Type Insights

Hydrocolloids represent the leading product category in the global coconut milk stabilizer market, accounting for approximately 42% of total market share in 2025. Their dominance is primarily driven by their superior water-binding capacity, emulsion stabilization efficiency, and cost-effectiveness in large-scale processing environments. Guar gum and xanthan gum blends are particularly preferred due to their ability to maintain fat dispersion in high-lipid coconut formulations, prevent phase separation, and enhance viscosity without altering taste profiles. These functional advantages make hydrocolloids the preferred choice among industrial coconut milk processors seeking extended shelf life and improved texture consistency.

Emulsifiers and blended stabilizer systems follow closely, especially in beverage-grade coconut milk applications where smooth mouthfeel and homogenization stability are critical. Customized stabilizer blends are increasingly being developed to meet specific processing conditions such as ultra-high temperature (UHT) treatment and aseptic packaging. Meanwhile, protein-based stabilizers represent a niche but rapidly expanding segment, fueled by clean-label reformulation initiatives and consumer demand for recognizable, plant-derived ingredients. The growth of this segment is supported by innovation in pea and rice protein stabilizing systems that offer both functional and nutritional value.

Application Insights

Shelf-stable coconut milk holds the largest application share, accounting for nearly 46% of the global market in 2025. The leading driver for this segment is the strong global retail and export demand for long-life packaged coconut milk products, particularly in regions where refrigeration infrastructure is limited. Stabilizers play a critical role in maintaining product integrity during extended storage and international shipping, thereby supporting consistent quality across export markets.

Coconut cream represents a substantial portion of demand, particularly in culinary applications and HoReCa channels where thick texture and stable fat emulsification are essential. RTD beverages and coconut-based desserts are emerging as the fastest-growing applications, driven by rising plant-based consumption trends in developed markets. Increasing demand for dairy alternatives, smoothie bases, and vegan desserts in North America and Europe continues to accelerate stabilizer integration into new product development pipelines.

End-Use Industry Insights

The food processing industry dominates overall end-use consumption, accounting for approximately 58% of global demand. The primary growth driver in this segment is the need for large-scale packaged coconut milk manufacturers to maintain consistent viscosity, prevent creaming, and ensure uniformity across high-volume production batches. Stabilizers are essential for meeting international export standards and shelf-life requirements, particularly for UHT-treated and canned products.

Beverage manufacturers represent the fastest-growing end-use segment, supported by expanding portfolios of barista-style coconut beverages, plant-based coffee creamers, and ready-to-drink formulations. The surge in plant-based beverage launches across global markets has intensified the need for advanced stabilizing systems capable of delivering smooth mouthfeel and thermal stability. Export-driven demand further influences purchasing volumes, with multinational processors securing bulk ingredient contracts to support cross-border shipments and private-label production.

Distribution Channel Insights

Direct B2B contracts account for approximately 61% of total market distribution, reflecting the prevalence of long-term supply agreements between stabilizer manufacturers and coconut milk processors. The dominance of this channel is driven by the need for customized formulations, price stability, and assured raw material supply in high-volume production environments. Strategic procurement partnerships allow manufacturers to maintain consistent product specifications while optimizing input costs.

Ingredient distributors continue to serve small and mid-sized manufacturers that require lower order volumes and technical formulation support. In parallel, online B2B platforms are gradually expanding their presence, particularly in emerging markets where digital procurement systems are improving ingredient accessibility and supplier transparency.

| By Product Type | By Application | By End-Use Industry | By Distribution Channel | By Form | By Source |

|---|---|---|---|---|---|

|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 38% of the global market share in 2025, making it the leading regional market. Regional growth is primarily driven by strong coconut production capacity, expanding processing infrastructure, and export-oriented manufacturing hubs. Thailand alone contributes nearly 14% of global demand due to its dominant coconut milk export industry, supported by well-established processing facilities and international trade networks. Indonesia and the Philippines also play critical roles in stabilizer consumption, as both countries continue to expand coconut processing capacity to meet rising global demand.

Government-backed agro-processing investments, export incentives, and infrastructure modernization programs further strengthen regional competitiveness. Increasing private-sector investment in automated processing lines and quality certification standards is accelerating the adoption of advanced stabilizer systems to meet international regulatory requirements.

North America

North America holds approximately 27% of the global market share, with the United States accounting for nearly 22%. The primary growth driver in this region is the rapid expansion of dairy-alternative consumption, particularly among health-conscious and vegan consumers. Clean-label reformulation initiatives are pushing manufacturers to adopt optimized stabilizer blends that balance functionality with ingredient transparency.The United States remains one of the fastest-growing markets, expanding at an estimated CAGR of around 9%, supported by innovation in plant-based beverages, private-label product launches, and strong retail distribution networks. Increased demand for barista-style coconut milk in foodservice chains and specialty coffee outlets further contributes to stabilizer adoption.

Europe

Europe represents approximately 21% of global demand, led by Germany, France, and the United Kingdom. Growth in this region is driven by rising plant-based dietary preferences, strong import volumes of coconut milk products, and stringent food quality standards. Germany stands out as one of the largest importers of coconut milk products, indirectly stimulating stabilizer demand across the value chain.Regulatory compliance requirements under European food safety frameworks encourage continuous product innovation, prompting manufacturers to develop high-performance stabilizer systems that meet labeling and additive regulations. Sustainability initiatives and demand for organic-certified ingredients also influence formulation strategies.

Middle East & Africa

The United Arab Emirates and Saudi Arabia are key import-driven markets within the Middle East & Africa region. Growth is supported by strong consumption of packaged coconut milk in foodservice, hospitality, and expatriate-driven retail segments. Expanding modern retail infrastructure and rising awareness of plant-based nutrition contribute to steady demand growth.In Africa, increasing urbanization and improving distribution networks are gradually enhancing product availability, supporting moderate but consistent market expansion.

Latin America

Brazil and Mexico are emerging markets where plant-based beverage trends are gaining traction. Although the region currently accounts for a smaller share of global demand, rising health awareness, expanding middle-class populations, and increasing retail penetration are expected to drive long-term growth. Local beverage manufacturers are gradually incorporating coconut-based formulations into their portfolios, creating new opportunities for stabilizer suppliers over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Coconut Milk and Cream Stabilizer Market

- Cargill Incorporated

- Kerry Group plc

- Ingredion Incorporated

- Tate & Lyle PLC

- Ashland Inc.

- CP Kelco

- DuPont Nutrition & Biosciences

- DSM-Firmenich

- BASF SE

- Nexira

- Palsgaard A/S

- Givaudan

- AAK AB

- Corbion NV

- International Flavors & Fragrances (IFF)