Coconut Drink Market Size

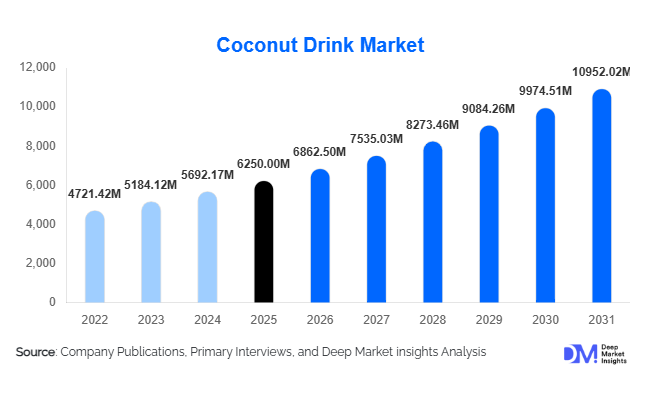

According to Deep Market Insights, the global coconut drink market size was valued at USD 6,250 million in 2025 and is projected to grow from USD 6,862.50 million in 2026 to reach USD 10,952.02 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The coconut drink market growth is primarily driven by the rising global shift toward plant-based beverages, increasing consumer preference for natural hydration products, and the expansion of functional drink formulations enriched with vitamins, electrolytes, and probiotics.

Key Market Insights

- Coconut water continues to dominate the product landscape, driven by its positioning as a natural sports drink with electrolyte-rich properties.

- Functional and fortified coconut beverages are gaining strong traction, particularly among fitness-conscious and health-driven consumers.

- Asia-Pacific dominates the global market, supported by abundant raw material availability and strong export-oriented production.

- North America remains a key consumption hub, with high demand for premium, organic, and flavored coconut drinks.

- E-commerce and direct-to-consumer channels are expanding rapidly, enhancing accessibility and brand engagement.

- Sustainability and ethical sourcing practices are becoming critical differentiators, influencing purchasing decisions in developed markets.

What are the latest trends in the coconut drink market?

Rise of Functional Coconut Beverages

The coconut drink market is witnessing a strong shift toward functional beverages that deliver added health benefits beyond hydration. Manufacturers are introducing coconut drinks fortified with probiotics, plant protein, collagen, and essential vitamins to cater to evolving consumer preferences. These products are increasingly positioned within the broader functional beverage segment, appealing to consumers seeking immunity support, digestive health, and sports recovery solutions. This trend is particularly prominent in North America and Europe, where consumers are willing to pay premium prices for value-added beverages. Additionally, brands are leveraging clean-label positioning, emphasizing natural ingredients and minimal processing to strengthen consumer trust and product differentiation.

Premiumization and Flavored Innovations

Flavor innovation and premiumization are reshaping the competitive landscape of the coconut drink market. Companies are launching a wide range of flavored coconut drinks, including tropical fruit blends, chocolate-infused variants, and low-sugar options, targeting younger demographics and urban consumers. Premium packaging formats such as glass bottles and sleek tetra packs are enhancing product appeal and positioning coconut drinks as lifestyle beverages. The introduction of organic-certified and cold-pressed variants is further supporting premium pricing strategies. These innovations are expanding the consumer base beyond traditional users and driving repeat purchases across developed and emerging markets.

What are the key drivers in the coconut drink market?

Growing Demand for Plant-Based Alternatives

The global shift toward plant-based diets is a major driver of coconut drink market growth. Increasing lactose intolerance and rising vegan populations are encouraging consumers to adopt coconut-based beverages as alternatives to dairy products. Coconut milk drinks are widely used in coffee, smoothies, and culinary applications, further boosting demand. The expansion of plant-based product portfolios by major beverage companies is accelerating market penetration and consumer awareness.

Rising Health and Wellness Awareness

Consumers are increasingly prioritizing health and wellness, driving demand for natural and low-calorie beverages. Coconut water, known for its natural electrolyte composition, is gaining popularity as a healthier alternative to sugary carbonated drinks and synthetic sports beverages. The growing influence of fitness culture, particularly among urban populations, is significantly contributing to increased consumption. Marketing campaigns emphasizing hydration, energy replenishment, and immunity support are further strengthening demand.

What are the restraints for the global market?

Raw Material Price Volatility

The coconut drink market is highly dependent on coconut-producing regions such as Southeast Asia, making it vulnerable to fluctuations in raw material prices. Weather conditions, climate change, and supply chain disruptions can significantly impact coconut availability and pricing. These fluctuations create challenges for manufacturers in maintaining stable profit margins and competitive pricing strategies.

Limited Shelf Life and Processing Challenges

Maintaining the freshness and nutritional integrity of coconut drinks, particularly coconut water, remains a key challenge. Natural coconut water has a relatively short shelf life, requiring advanced processing and packaging technologies such as aseptic filling. While these technologies extend shelf life, they increase production costs. Balancing product quality with cost efficiency continues to be a major restraint for market participants.

What are the key opportunities in the coconut drink industry?

Expansion into Emerging Markets

Emerging markets in the Middle East, Africa, and Latin America present significant growth opportunities for coconut drink manufacturers. Rapid urbanization, rising disposable incomes, and improving retail infrastructure are driving demand for health-oriented beverages in these regions. Governments are also encouraging imports and local bottling operations, creating favorable conditions for market entry and expansion.

Sustainable and Ethical Sourcing

Sustainability is becoming a key competitive advantage in the coconut drink market. Consumers are increasingly prioritizing products that are ethically sourced and environmentally friendly. Companies investing in fair trade practices, eco-friendly packaging, and transparent supply chains are gaining stronger brand loyalty. Certification programs and sustainability labels are further enhancing product credibility, particularly in developed markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6250.00 Million |

| Market Size in 2026 | USD 6862.50 Million |

| Market Size in 2031 | USD 10952.02 Million |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product type segmentation of the global coconut drink market reflects a strong consumer inclination toward natural, functional, and plant-based beverages, with coconut water firmly maintaining its leadership position. Coconut water dominates the global coconut drink market, accounting for approximately 42% of the total market share in 2025, owing to its inherent positioning as a natural isotonic beverage. Its rich electrolyte profile, including potassium, magnesium, and sodium, aligns closely with evolving consumer demand for hydration solutions that go beyond traditional sugary soft drinks. The growing global focus on fitness, sports nutrition, and wellness-centric lifestyles has further strengthened coconut water’s role as a preferred hydration alternative. This dominance is particularly reinforced by its clean-label appeal, absence of artificial additives, and compatibility with a wide range of dietary preferences including vegan, paleo, and gluten-free diets.Coconut milk beverages are also gaining significant traction, particularly as a dairy alternative in the expanding plant-based beverage segment. With rising incidences of lactose intolerance and growing adoption of vegan lifestyles globally, coconut milk-based drinks are witnessing increased demand in both developed and emerging markets. These beverages are widely used in coffee applications, smoothies, and culinary preparations, making them highly versatile. Meanwhile, flavored and functional coconut drinks represent one of the fastest-evolving categories within the market. Premiumization trends, combined with consumer interest in unique taste profiles and added health benefits, are driving the introduction of innovative products infused with fruits, herbs, and functional ingredients such as collagen or adaptogens. This dynamic innovation landscape is not only diversifying product offerings but also strengthening overall market growth.

Nature Insights

The nature-based segmentation of the coconut drink market highlights a clear distinction between affordability-driven consumption and premium health-conscious purchasing behavior. Conventional coconut drinks hold the largest share, contributing nearly 68% of the global market in 2025. This dominance is primarily attributed to their widespread availability, cost-effectiveness, and well-established supply chains, particularly in coconut-producing regions. Conventional products are more accessible to a broader consumer base, making them the default choice in price-sensitive markets across Asia-Pacific, Latin America, and parts of Africa. The leading driver for this segment is the consistent demand for affordable and widely available hydration beverages, especially in emerging economies where price sensitivity remains a critical purchasing factor.At the same time, organic coconut drinks are experiencing a notable surge in demand, albeit from a smaller base. The shift toward organic variants is being driven by increasing consumer awareness regarding pesticide-free farming, environmental sustainability, and clean-label consumption. Consumers in developed regions such as North America and Europe are particularly inclined toward organic certifications, perceiving them as indicators of superior quality and safety. Although premium pricing and limited availability currently restrict the organic segment to niche markets, advancements in organic farming practices and improvements in supply chain logistics are expected to gradually reduce these barriers. Over the long term, the organic segment is poised for robust expansion as sustainability becomes a central theme in global consumption patterns and as regulatory frameworks increasingly support organic agriculture.

Packaging Format Insights

Packaging plays a critical role in shaping consumer perception, product shelf life, and distribution efficiency within the coconut drink market. Tetra packs dominate the packaging segment, accounting for approximately 47% of the market share in 2025. Their aseptic packaging technology ensures extended shelf life without the need for preservatives, making them highly suitable for international trade and long-distance transportation. The leading driver for this segment is the growing demand for safe, durable, and long-lasting packaging solutions that maintain product freshness while enabling efficient logistics. Tetra packs also offer convenience in storage and handling, which further enhances their appeal among both manufacturers and consumers.In addition to tetra packs, PET bottles and aluminum cans are widely utilized, particularly for ready-to-drink formats targeting on-the-go consumption. These packaging formats cater to urban lifestyles characterized by convenience and mobility, making them popular among younger consumers and working professionals. Meanwhile, glass bottles are gaining traction in the premium segment, where brand positioning and sustainability considerations play a more prominent role. Glass packaging is often associated with higher quality and purity, and its recyclability aligns with the increasing emphasis on environmentally responsible consumption. As sustainability becomes a key differentiator in the beverage industry, manufacturers are exploring eco-friendly packaging innovations, including biodegradable materials and reduced plastic usage, to enhance their competitive positioning.

Distribution Channel Insights

The distribution landscape of the coconut drink market is evolving rapidly, driven by changes in consumer shopping behavior and advancements in retail infrastructure. Supermarkets and hypermarkets represent the largest distribution channel, holding around 38% of the market share in 2025. These retail formats provide extensive shelf space, strong brand visibility, and the ability to offer a wide variety of products under one roof. The leading driver for this segment is the high level of consumer trust and convenience associated with organized retail, which enables easy product comparison and immediate availability. In addition, promotional activities, in-store marketing, and strategic product placement further boost sales through these channels.Online retail is emerging as the fastest-growing distribution channel, fueled by increasing internet penetration, smartphone usage, and the adoption of e-commerce platforms. Consumers are increasingly turning to online channels for their convenience, access to a broader product range, and the ability to compare prices and reviews. Subscription-based models and direct-to-consumer strategies are also gaining popularity, allowing brands to build stronger relationships with their customers while ensuring consistent demand. Specialty health stores, on the other hand, play a crucial role in targeting niche segments of health-conscious consumers. These stores often emphasize premium, organic, and functional products, thereby contributing to the growth of higher-value segments within the market.

End-Use Insights

The end-use segmentation of the coconut drink market underscores the dominance of direct consumption while highlighting the growing importance of industrial applications. Direct consumption dominates the end-use segment, accounting for nearly 61% of the global market in 2025. This dominance is driven by the increasing preference for ready-to-drink beverages that combine convenience with health benefits. The leading driver for this segment is the rising demand for functional beverages that can be consumed anytime, anywhere, without preparation. Coconut drinks, particularly coconut water, align perfectly with this demand, offering hydration, nutrition, and portability in a single package.The foodservice sector is emerging as a significant growth avenue, particularly with the incorporation of coconut milk and coconut-based beverages into menus across cafes, restaurants, and quick-service outlets. The growing popularity of plant-based diets has encouraged foodservice providers to include coconut-based alternatives in beverages such as lattes, smoothies, and desserts. Additionally, the food processing and nutraceutical industries are increasingly utilizing coconut-based drinks as ingredients in a variety of products, ranging from functional foods to dietary supplements. This diversification of applications is enhancing the overall market potential and creating new revenue streams for manufacturers.

Explore more data points, trends and opportunities Download Free Sample Report

Coconut Drink Market Segmentations

By Product Type

- Coconut Water

- Coconut Milk Beverages

- Flavored Coconut Drinks

- Functional Coconut Beverages

- Coconut Smoothies & Blends

By Nature

- Conventional Coconut Drinks

- Organic Coconut Drinks

By Packaging Format

- Tetra Packs

- PET Bottles

- Glass Bottles

- Cans

- Pouches

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Health Stores

- Foodservice Channels

By End-Use

- Direct Consumption

- Foodservice Industry

- Food Processing Industry

- Nutraceutical & Functiona

- Beverage Industry

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the coconut drink market, accounting for approximately 36% of the global market in 2025, supported by its strong production base and deep-rooted cultural familiarity with coconut-based products. Countries such as Indonesia, Thailand, India, and the Philippines dominate global coconut production, ensuring a steady supply of raw materials and cost advantages for regional manufacturers. The primary drivers of growth in this region include abundant coconut resources, increasing urbanization, and rising disposable incomes, which are collectively boosting domestic consumption. Additionally, the growing influence of health and wellness trends, coupled with the expansion of modern retail formats, is enhancing product accessibility and awareness. Export-oriented production and government support for agricultural development further strengthen the region’s leadership position in the global market.

North America

North America accounts for around 28% of the market share, with the United States serving as the primary consumption hub. The region’s growth is largely driven by strong consumer demand for functional and plant-based beverages, reflecting a broader shift toward healthier lifestyles. High disposable incomes and a well-established retail infrastructure enable consumers to access a wide range of premium and imported coconut drink products. The key drivers in this region include the rising popularity of plant-based diets, increasing awareness of the health benefits associated with coconut water, and continuous product innovation by leading beverage companies. Furthermore, the expansion of e-commerce platforms and direct-to-consumer channels is facilitating market penetration and enhancing brand visibility.

Europe

Europe holds approximately 22% of the market, characterized by a strong emphasis on sustainability, ethical sourcing, and plant-based consumption. Countries such as Germany, the United Kingdom, and France are leading markets within the region, supported by high consumer awareness and well-developed distribution networks. The primary drivers of growth in Europe include the increasing demand for environmentally friendly and organic products, as well as stringent regulatory standards that promote quality and transparency. The region’s mature retail landscape, combined with the growing popularity of vegan and flexitarian diets, is further supporting the expansion of coconut-based beverages. Additionally, innovations in packaging and branding are playing a crucial role in attracting environmentally conscious consumers.

Latin America

Latin America is experiencing steady growth in the coconut drink market, with countries such as Brazil and Mexico leading regional demand. The region benefits from favorable climatic conditions for coconut cultivation, which enhances local production capabilities and reduces reliance on imports. Key growth drivers include increasing health awareness among consumers, expanding middle-class populations, and improvements in retail infrastructure. The growing presence of international brands, along with the expansion of modern trade channels, is also contributing to market development. As consumers become more health-conscious, the demand for natural and minimally processed beverages is expected to rise, further supporting the growth of coconut drinks in the region.

Middle East & Africa

The Middle East & Africa region is the fastest-growing market, with a CAGR exceeding 11%, driven by a combination of demographic and economic factors. Rising disposable incomes, rapid urbanization, and increasing exposure to global health trends are fueling demand for coconut-based beverages. Countries such as the United Arab Emirates and South Africa are emerging as key markets, supported by expanding retail infrastructure and a growing expatriate population familiar with coconut products. The primary drivers of growth in this region include increasing import penetration, the development of organized retail sectors, and a rising preference for premium and functional beverages. Additionally, the region’s hot climate creates a natural demand for hydrating drinks, positioning coconut water as an attractive alternative to traditional sugary beverages.

Key Players in the Coconut Drink Market

- Vita Coco Company

- PepsiCo Inc.

- Coca-Cola Company

- Danone S.A.

- Amy & Brian Naturals

- Taste Nirvana International

- Zico Beverages

- Goya Foods Inc.

- Celebes Coconut Corporation

- Edward & Sons Trading Co.

- GraceKennedy Group

- Thai Agri Foods

- Maverick Brands

- Chi Coconut Water

- Rebel Kitchen