Cocoa Liquor Market Size

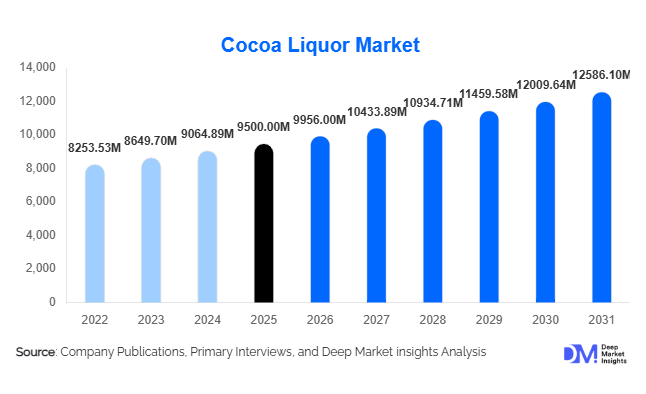

According to Deep Market Insights, the global cocoa liquor market size was valued at USD 9,500 million in 2025 and is projected to grow from USD 9,956 million in 2026 to reach USD 12,586.10 million by 2031, expanding at a CAGR of 4.8% during the forecast period (2026–2031). The cocoa liquor market growth is primarily driven by rising global chocolate consumption, increasing demand for premium and dark chocolate formulations, expansion of functional food applications, and growing adoption of sustainable cocoa sourcing practices across major processing economies.

Cocoa liquor, a key intermediate derived from roasted and ground cocoa beans, serves as the foundational ingredient for chocolate manufacturing and is increasingly being utilized in bakery, confectionery, dairy, nutraceutical, and cosmetic applications. Europe continues to dominate global consumption due to its strong chocolate manufacturing base, while Asia-Pacific is emerging as the fastest-growing region, led by increasing disposable income and Western dietary influence in countries such as India and China. Meanwhile, Africa and Latin America remain critical supply-side regions, investing heavily in cocoa processing infrastructure to capture more value addition domestically.

Key Market Insights

- Chocolate manufacturing dominates demand, accounting for the largest share of cocoa liquor consumption globally due to its essential role in chocolate production.

- Alkalized cocoa liquor leads processing preference due to improved flavor consistency and better usability in large-scale confectionery manufacturing.

- Europe remains the largest consumption region, supported by strong chocolate brands and high per capita chocolate consumption.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and expanding bakery and confectionery industries.

- Food & beverage industry dominates end-use demand, while nutraceuticals and cosmetics are emerging as high-growth segments.

- Sustainability and traceability are reshaping sourcing models, with increasing adoption of certified cocoa supply chains.

What are the latest trends in the cocoa liquor market?

Premiumization and Dark Chocolate Expansion

Global demand is shifting toward high-cocoa-content dark chocolate, directly increasing cocoa liquor consumption. Consumers are increasingly prioritizing health-oriented indulgence, pushing manufacturers to adopt higher cocoa concentrations. This trend is particularly strong in developed markets such as Europe and North America, where premium confectionery consumption continues to rise steadily. Artisanal and craft chocolate brands are further accelerating demand for high-quality cocoa liquor with consistent flavor profiles.

Sustainability and Traceable Cocoa Supply Chains

Companies are increasingly investing in blockchain-enabled traceability systems and certified sourcing models such as Fair Trade and Rainforest Alliance. Regulatory pressure from deforestation laws in Europe is pushing manufacturers to adopt transparent sourcing strategies. This is transforming cocoa liquor procurement into a sustainability-driven value chain, where compliance and ESG alignment are becoming critical competitive differentiators.

What are the key drivers in the cocoa liquor market?

Rising Chocolate and Confectionery Consumption

The steady rise in global chocolate consumption remains the most significant driver of cocoa liquor demand. Expanding urban populations and increasing disposable incomes in emerging markets such as India and China are driving higher confectionery consumption. Seasonal demand spikes during festivals and increased availability of premium chocolate products are further strengthening market growth.

Expansion of Functional Foods and Nutraceuticals

Cocoa liquor contains antioxidants and flavonoids, making it increasingly attractive for functional food applications. It is widely used in energy bars, protein snacks, and fortified beverages. The global shift toward preventive healthcare and wellness-based nutrition is significantly boosting demand from nutraceutical manufacturers.

Growth in Value-Added Cocoa Processing

Cocoa-producing regions in West Africa are increasingly investing in local processing facilities, shifting from raw bean exports to value-added cocoa liquor production. This is improving global supply stability while also increasing availability for industrial buyers across Europe and North America.

What are the restraints for the global market?

Volatility in Cocoa Bean Prices

The cocoa liquor market is highly sensitive to fluctuations in raw cocoa bean prices, which are influenced by climate change, supply chain disruptions, and geopolitical instability in key producing regions such as Côte d’Ivoire and Ghana. This creates pricing uncertainty for manufacturers and impacts profit margins across the value chain.

Stringent Sustainability and Compliance Regulations

Increasing regulatory requirements related to deforestation-free sourcing, child labor prevention, and ESG reporting are raising compliance costs. While necessary for sustainability, these regulations add operational complexity and limit sourcing flexibility for manufacturers who fail to meet certification standards.

What are the key opportunities in the cocoa liquor industry?

Expansion into Cosmetics and Personal Care Applications

Cocoa liquor-derived ingredients are increasingly used in skincare, anti-aging, and moisturizing formulations due to their natural antioxidant properties. The shift toward clean-label and plant-based cosmetics in markets like United States and Germany is creating strong demand opportunities for cocoa-based inputs.

Growth in Premium and Organic Cocoa Segments

Organic and single-origin cocoa liquor is gaining traction among premium chocolate manufacturers. Consumers are willing to pay higher prices for ethically sourced and high-quality cocoa products, creating significant margin expansion opportunities for producers.

Technological Advancements in Cocoa Processing

Automation in roasting, grinding, and fermentation control is improving yield efficiency and flavor consistency. AI-based quality monitoring systems and blockchain traceability are enhancing production transparency and operational efficiency across global supply chains.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9500 Million |

| Market Size in 2026 | USD 9956 Million |

| Market Size in 2031 | USD 12586.10 Million |

| CAGR | 4.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global cocoa liquor market is predominantly led by alkalized cocoa liquor, which accounts for approximately 38% share of the total market. Its dominance is primarily driven by its superior flavor consistency, reduced acidity, and enhanced solubility, which make it highly suitable for large-scale industrial chocolate production. The leading growth driver for this segment is the expanding demand for standardized taste profiles in mass-market confectionery, where manufacturers prioritize product uniformity across global markets. Additionally, alkalized cocoa liquor offers improved color intensity and functional versatility, making it highly preferred in processed food applications such as flavored coatings, ready-to-eat desserts, and beverage mixes. The segment continues to benefit from advancements in alkalization technologies that allow manufacturers to fine-tune pH levels without compromising cocoa flavor integrity.High-fat cocoa liquor continues to maintain strong demand in premium confectionery and luxury chocolate applications. The primary growth driver for this segment is its ability to enhance mouthfeel, texture richness, and overall sensory experience in finished chocolate products. Premium chocolate manufacturers in Europe and North America particularly rely on high-fat variants to differentiate their products in high-margin segments. Additionally, innovation in fat content optimization is enabling manufacturers to balance cost efficiency with premium product positioning.

Application Insights

Chocolate manufacturing remains the dominant application segment, accounting for approximately 42% share of total cocoa liquor consumption. The leading growth driver for this segment is the sustained global expansion of the chocolate industry, particularly in emerging markets where Western dietary patterns are increasingly adopted. Large-scale confectionery manufacturers depend heavily on cocoa liquor as a foundational ingredient for producing milk chocolate, dark chocolate, and compound coatings. Product innovation in flavored chocolates, sugar-reduced variants, and functional chocolate formulations further strengthens demand in this segment.Bakery and confectionery applications represent another significant consumption area, supported by rising demand for indulgent baked goods, pastries, and desserts. The key driver for this segment is the premiumization of bakery products, where cocoa-based ingredients are used to enhance flavor complexity and consumer appeal. Artisanal bakeries and industrial bakery chains alike are incorporating cocoa liquor into cakes, cookies, and filled pastries to meet evolving consumer preferences for rich and authentic chocolate flavors.Nutraceutical and cosmetic applications are emerging as the fastest-growing segments within the cocoa liquor market. The primary driver for this growth is the increasing recognition of cocoa’s antioxidant, anti-inflammatory, and skin-nourishing properties. In nutraceuticals, cocoa liquor is being incorporated into functional foods and dietary supplements aimed at improving cardiovascular health and overall wellness. In cosmetics, it is being used in skincare formulations, particularly in moisturizers and anti-aging products, due to its natural emollient characteristics and rich bioactive profile.

Distribution Channel Insights

Direct B2B sales continue to dominate the cocoa liquor distribution landscape, as large-scale chocolate manufacturers prefer direct procurement relationships with processors to ensure consistent quality, price stability, and supply reliability. The leading driver for this channel is the need for supply chain control and cost optimization in a highly competitive confectionery industry. Long-term contracts between cocoa processors and food manufacturers further reinforce this distribution structure, enabling predictable sourcing and reduced exposure to raw material price volatility.Ingredient distributors play a vital role in serving mid-sized food manufacturers and regional producers who lack direct procurement capabilities. The growth driver for this segment is the increasing fragmentation of the food manufacturing industry, where small and medium enterprises require flexible sourcing options and smaller order volumes. Distributors also provide value-added services such as blending, storage, and logistics management, making them essential intermediaries in the supply chain.Digital procurement platforms are emerging as a transformative channel in the cocoa liquor market. The leading driver for this segment is the digitalization of global commodity trading, which enables transparent pricing, improved supplier discovery, and faster procurement cycles. These platforms are particularly beneficial for smaller manufacturers seeking competitive pricing and diversified supplier access. As supply chain digitization accelerates, this channel is expected to gain further traction across both developed and emerging markets.

End-Use Industry Insights

The food and beverage industry remains the largest end-use segment, accounting for over 60% of total cocoa liquor consumption. The leading growth driver is the continuous expansion of chocolate, bakery, and dairy product categories, supported by rising global demand for indulgent food experiences. The industry’s strong reliance on cocoa liquor as a base ingredient ensures sustained long-term demand, particularly in premium and value-added product categories.The nutraceutical industry is expanding rapidly as consumers increasingly prioritize health-oriented food choices. The key driver for this segment is the growing awareness of cocoa’s functional benefits, including its antioxidant properties and potential cardiovascular health advantages. This has led to the incorporation of cocoa liquor into energy bars, health supplements, and functional beverages.The pharmaceutical sector remains relatively niche but is gradually expanding due to ongoing research into cocoa-derived bioactive compounds. The primary driver for this segment is the exploration of cocoa’s potential therapeutic benefits, particularly in cardiovascular and metabolic health applications. While still in early stages, pharmaceutical interest in cocoa-based ingredients is expected to grow steadily over the long term.

Explore more data points, trends and opportunities Download Free Sample Report

Cocoa Liquor Market Segmentations

By Source of Cocoa Beans

- Forastero Cocoa Beans

- Criollo Cocoa Beans

- Trinitario Cocoa Beans

By Processing Type

- Natural Cocoa Liquor

- Alkalized Cocoa Liquor

- Organic Cocoa Liquor

- Fair Trade Certified Cocoa Liquor

Fat Content Level

- High-Fat Cocoa Liquor

- Standard Fat Cocoa Liquor

- Reduced Fat Cocoa Liquor

By Application

- Chocolate Manufacturing

- Confectionery Products

- Bakery & Pastry Products

- Dairy & Ice Cream Products

- Beverages

- Cosmetics & Personal Care

By End-Use Industry

- Food & Beverage Industry

- Nutraceuticals & Functional Foods

- Cosmetics & Personal Care

- Pharmaceutical Applications

By Distribution Channel

- Direct B2B Sales

- Food Ingredient Distributors

- Online Industrial Procurement Platforms

- Specialty Ingredient Suppliers

Regional Insights

Europe

Europe holds approximately 34% share of the global cocoa liquor market, driven by its well-established chocolate manufacturing industry and strong consumer preference for premium confectionery products. The leading growth driver in this region is the high demand for dark and artisanal chocolate, particularly in countries such as Switzerland, Belgium, and Germany. Strict quality standards and strong regulatory frameworks also encourage the use of high-quality cocoa liquor inputs. Additionally, sustainability initiatives and ethical sourcing requirements are shaping procurement strategies across European manufacturers, further strengthening demand for certified cocoa products.

North America

North America accounts for around 25% market share, with the United States and Canada being major consumption hubs. The primary growth driver is the increasing consumer shift toward premium, organic, and functional chocolate products. Rising health awareness has also contributed to the growing popularity of dark chocolate, which requires higher cocoa liquor content. Furthermore, innovation in confectionery products, including reduced-sugar and protein-enriched chocolates, continues to support market expansion in the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, and changing dietary preferences. The leading growth driver is the increasing adoption of Western-style confectionery products among younger consumers in countries such as India, China, and Japan. Expanding retail infrastructure and the growth of organized food distribution networks are further accelerating market penetration. Additionally, multinational chocolate brands are investing heavily in regional expansion, which significantly boosts cocoa liquor demand.

Latin America

Latin America plays a dual role as both a production base and an emerging consumption market. The leading growth driver in this region is the expansion of domestic chocolate manufacturing industries in Brazil and Ecuador, supported by abundant raw cocoa availability. Increasing investments in value-added cocoa processing are also strengthening regional supply chains. Furthermore, rising local consumption of chocolate-based products is contributing to steady market growth.

Middle East & Africa

Africa remains the primary global supplier of cocoa beans, while the Middle East is emerging as a high-growth consumption region. The leading growth driver in this region is the rising demand for premium confectionery products among affluent consumers, particularly in countries such as the UAE and Saudi Arabia. Growth in retail tourism, luxury hospitality, and gifting culture further supports demand. In Africa, increasing investments in local processing capabilities are gradually enhancing value addition within the region, strengthening its role in the global cocoa liquor value chain.