Cocktail Market Size

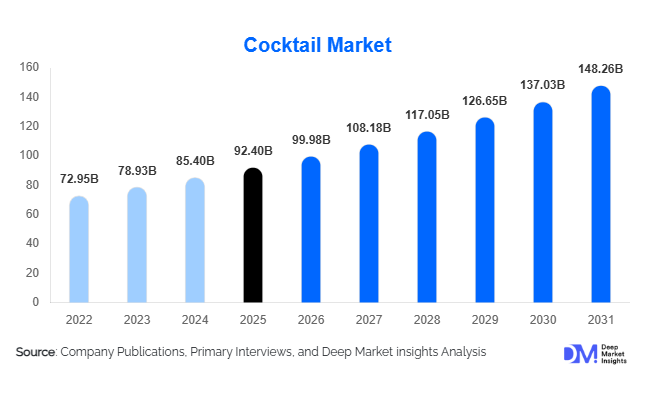

According to Deep Market Insights, the global cocktail market size was valued at USD 92.4 billion in 2025 and is projected to grow from USD 99.98 billion in 2026 to reach USD 148.26 billion by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). Market expansion is supported by rising premium alcohol consumption, increasing popularity of ready-to-drink (RTD) cocktails, growing urban nightlife culture, and consumer preference for experiential beverage consumption. The cocktail industry has transitioned from traditional bar-centric consumption toward diversified channels including retail, e-commerce, and home mixology.

Globally, consumer drinking behavior is shifting toward curated flavor experiences, craft ingredients, and premium spirits-based beverages. Millennials and Gen Z consumers are driving experimentation with botanical flavors, low-alcohol cocktails, and visually appealing drinks influenced by social media culture. The emergence of RTD cocktails has significantly expanded accessibility by eliminating preparation complexity while maintaining bar-quality taste profiles. Additionally, innovation in packaging formats such as cans, kegs, and eco-friendly bottles is enabling broader retail penetration.

Hospitality recovery, expansion of tourism, and rapid growth of organized nightlife ecosystems across emerging economies continue to support demand growth. Premiumization trends are also reshaping pricing structures, with consumers willing to pay higher prices for artisanal ingredients, craft spirits, and branded cocktail experiences. Meanwhile, digital ordering platforms and direct-to-consumer alcohol models are improving distribution efficiency. As global beverage companies invest heavily in innovation and brand diversification, the cocktail market is evolving into a hybrid ecosystem combining hospitality, retail beverages, and lifestyle consumption.

Key Market Insights

- Ready-to-drink cocktails represent the fastest-growing product category, driven by convenience and retail expansion.

- Premium and craft cocktails dominate value share due to higher pricing and experiential consumption trends.

- North America leads global demand supported by strong cocktail culture and premium spirit consumption.

- Asia-Pacific is the fastest-growing region, fueled by urbanization and expanding middle-class spending.

- Digital ordering and home mixology trends are reshaping consumption beyond bars and restaurants.

- Flavor innovation and low-alcohol options are attracting health-conscious consumers.

What are the latest trends in the cocktail market?

Premiumization and Craft Cocktail Culture

The cocktail industry is increasingly defined by premiumization, where consumers prefer high-quality spirits, natural ingredients, and artisanal preparation techniques. Craft cocktail bars are expanding globally, emphasizing mixology expertise, unique garnishes, and locally sourced ingredients. Premium cocktails command higher margins, encouraging beverage companies to introduce upscale variants and limited-edition flavors. This trend has strengthened brand differentiation and enhanced profitability across hospitality and retail channels.

Rise of Ready-to-Drink (RTD) Cocktails

RTD cocktails are transforming the industry by bridging the gap between convenience beverages and traditional bar experiences. Canned cocktails, bottled mixes, and pre-mixed premium beverages are witnessing strong adoption among younger consumers and home entertainers. Retail chains and online alcohol delivery platforms are increasingly allocating shelf space to RTD formats, expanding distribution reach globally.

What are the key drivers in the cocktail market?

Expansion of Urban Nightlife and Hospitality

Growth in bars, lounges, restaurants, and tourism-driven hospitality venues is driving cocktail consumption worldwide. Emerging cities across Asia-Pacific and the Middle East are witnessing rapid development of nightlife infrastructure, increasing demand for premium beverages and signature cocktails.

Changing Consumer Preferences Toward Experiences

Consumers increasingly associate cocktails with lifestyle experiences rather than simple alcohol consumption. The visual appeal of cocktails, storytelling around ingredients, and experiential dining concepts are enhancing demand. Social media influence has further accelerated adoption by promoting visually distinctive beverages.

Innovation in Flavors and Low-Alcohol Alternatives

Health-conscious consumers are encouraging innovation in low-ABV, alcohol-free, and botanical cocktails. Brands are investing in functional ingredients, natural sweeteners, and organic mixers to attract wellness-focused demographics while maintaining flavor complexity.

What are the restraints for the global market?

Regulatory and Taxation Challenges

Alcohol regulations vary significantly across countries, affecting distribution, marketing, and pricing. High excise duties and advertising restrictions limit expansion opportunities in several emerging markets.

Volatility in Raw Material Prices

Fluctuating prices of spirits, fruits, sugar, and packaging materials directly impact production costs and margins. Supply chain disruptions and agricultural variability remain persistent challenges for manufacturers.

What are the key opportunities in the cocktail industry?

Growth of E-commerce Alcohol Sales

Online alcohol retail platforms are creating new growth opportunities by enabling direct consumer engagement and subscription-based cocktail delivery models. Personalized recommendations and digital marketing campaigns are improving customer retention and expanding premium product penetration.

Emerging Market Consumption Expansion

Rising disposable income in countries such as India, Vietnam, Brazil, and Indonesia is accelerating cocktail adoption beyond metropolitan regions. Localization of flavors and culturally adapted recipes present strong growth opportunities for global brands.

Technology Integration in Beverage Innovation

AI-driven flavor development, automated dispensing systems, and smart bar technologies are improving operational efficiency while enabling customization. These innovations are particularly valuable for large hospitality chains seeking standardized quality across locations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 92.40 Billion |

| Market Size in 2026 | USD 99.98 Billion |

| Market Size in 2031 | USD 148.26 Billion |

| CAGR | 8.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global cocktail market demonstrates strong product diversification, with spirit-based cocktails continuing to dominate overall consumption patterns. Spirit-based cocktails accounted for approximately 48% of global revenue in 2025, primarily driven by sustained consumer preference for classic and premium alcoholic beverages made using vodka, rum, tequila, gin, and whiskey. The segment’s leadership is supported by premiumization trends, growing craft mixology culture, and increasing consumer willingness to experiment with high-quality spirits in both on-trade and at-home environments. Rising investments by international spirit brands in flavored variants, artisanal blends, and premium positioning further reinforce the segment’s leading position.Ready-to-drink (RTD) cocktails represent the fastest-growing product category, holding nearly 26% market share. Growth in this segment is largely driven by convenience-oriented consumption behavior, expanding retail shelf space, and the growing popularity of portable beverage formats among younger consumers. Increasing urbanization, busy lifestyles, and demand for consistent taste experiences without preparation complexity have accelerated RTD adoption globally. Innovation in packaging formats, low-calorie formulations, and premium canned cocktails continues to attract new consumer demographics.Wine-based cocktails account for around 14% of the market, supported by rising demand in social dining, brunch occasions, and casual hospitality settings. Products such as spritzers and sangria-style beverages benefit from lower alcohol content preferences and strong seasonal consumption trends, particularly across Europe and North America. Meanwhile, non-alcoholic cocktails hold approximately 12% share and are expanding steadily as wellness-conscious and sober-curious consumers seek sophisticated beverage alternatives. The segment is increasingly supported by alcohol-free spirits innovation, health-focused branding, and expanding availability across restaurants and retail channels.

Application Insights

Bars and pubs remain the leading application segment, accounting for approximately 41% market share in 2025, as experiential consumption continues to drive global cocktail demand. The leading position of this segment is supported by consumers prioritizing social experiences, live entertainment, and premium beverage presentation, which cannot be easily replicated in home environments. The expansion of themed bars, rooftop lounges, and craft cocktail establishments has further strengthened on-premise consumption patterns.Restaurants contribute nearly 27% of total market demand, supported by the integration of curated cocktail menus within premium and casual dining experiences. Food and beverage pairing strategies, chef-driven dining concepts, and higher-margin beverage offerings are encouraging restaurants to expand cocktail portfolios, enhancing revenue per customer.Household consumption has grown significantly to around 22% market share, driven by the rise of home mixology trends, increased availability of RTD cocktails, and digital content influencing consumer experimentation with cocktail preparation. Growth in retail accessibility and e-commerce alcohol platforms has accelerated at-home consumption habits established during recent shifts in social behavior.Events and catering account for approximately 10% of market demand, supported by rising spending on weddings, corporate gatherings, music festivals, and private celebrations. Premium beverage packages and customized cocktail experiences are increasingly being adopted to enhance guest engagement and event differentiation.

Distribution Channel Insights

On-trade distribution channels lead the global cocktail market with nearly 52% share, driven by bars, hotels, nightclubs, and lounges offering professionally crafted cocktails and premium experiences. The dominance of this channel is supported by higher profit margins on mixed beverages, strong tourism activity, and expanding nightlife infrastructure across major urban centers.Off-trade retail channels account for approximately 38% of the market, supported by supermarkets, liquor stores, and specialty beverage retailers expanding their RTD cocktail assortments. Retail-driven growth is fueled by convenience purchasing behavior, promotional pricing strategies, and increasing consumer preference for ready-made premium beverages for home consumption.Online distribution channels currently represent around 10% of total sales but are emerging as the fastest-growing segment. Growth is driven by digital alcohol delivery platforms, subscription-based cocktail kits, and direct-to-consumer brand strategies. Improved logistics networks, mobile commerce adoption, and personalized recommendation algorithms are accelerating online purchasing behavior globally.

End-Use Analysis

The hospitality industry remains the largest end-use sector in the global cocktail market, supported by the recovery of international tourism, expansion of luxury hotels, and increasing investments in nightlife and entertainment venues. Hotels and resorts increasingly position cocktails as premium experiential offerings that enhance guest satisfaction and brand differentiation.The global foodservice industry, valued above USD 3.5 trillion, continues to integrate cocktails as high-margin menu components, enabling operators to improve profitability while enhancing dining experiences. Cocktail innovation and seasonal menus are becoming key revenue drivers for restaurants worldwide.Retail beverage consumption is expanding at a faster pace, particularly through RTD formats that enable convenient at-home consumption. Growth in modern retail infrastructure and expanding consumer access to premium beverage brands are accelerating household penetration rates.The event management and entertainment industries are emerging as significant demand contributors, as premium beverage packages and customized cocktail services increase average spending per attendee. Additionally, export-driven demand is rising as international spirit manufacturers expand distribution networks into emerging markets across Asia-Pacific and Latin America, increasing cross-border beverage trade volumes and brand visibility.

Explore more data points, trends and opportunities Download Free Sample Report

Cocktail Market Segmentations

By Product Type

- Ready-to-Drink (RTD) Cocktails

- Pre-Mixed Bottled Cocktails

- Craft & Freshly Prepared Cocktails

- Low & No-Alcohol Cocktails

- Frozen & Specialty Cocktails

By Base Spirit Type

- Vodka-Based Cocktails

- Rum-Based Cocktails

- Whiskey-Based Cocktails

- Tequila-Based Cocktails

- Gin-Based Cocktails

- Wine & Aperitif-Based Cocktails

By Distribution Channel

- On-Trade

- Off-Trade Retail

- E-commerce & Direct-to-Consumer

- Travel Retail & Duty-Free

By Consumer Demographics

- Millennials

- Gen Z Consumers

- Gen X Consumers

- Premium & Luxury Consumers

By Price Category

- Economy Cocktails

- Mid-Range Cocktails

- Premium Cocktails

- Super-Premium & Craft Cocktails

Regional Insights

North America

North America held approximately 34% of global cocktail market share in 2025, led primarily by the United States, where strong bar culture, high disposable income levels, and widespread premium alcohol adoption support sustained demand. Regional growth is further driven by rapid innovation in ready-to-drink cocktails, expansion of craft distilleries, and increasing consumer preference for premium and artisanal beverages. The rise of experiential nightlife, cocktail festivals, and mixology-focused hospitality concepts continues to strengthen on-trade consumption, while advanced e-commerce alcohol delivery infrastructure supports off-trade expansion. Canada contributes steady growth through increasing adoption of craft cocktails, premium RTD beverages, and evolving urban dining culture.

Europe

Europe accounted for nearly 28% market share, supported by long-established cocktail traditions and a mature hospitality ecosystem. Demand across the U.K., Germany, France, Italy, and Spain is driven by strong tourism flows, outdoor dining culture, and widespread popularity of aperitif-based and gin-based cocktails. Regional growth is supported by rising premiumization trends, sustainability-focused beverage innovation, and increasing consumer preference for lower-alcohol and wine-based cocktails. The expansion of boutique bars, mixology education, and regional spirit heritage further enhances market stability and innovation.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 10% CAGR. Growth is driven by rapid urbanization, rising middle-class income levels, and evolving social consumption habits across China, India, Japan, South Korea, and Australia. India’s expanding urban nightlife ecosystem, increasing acceptance of premium alcohol brands, and growth of organized hospitality chains are accelerating cocktail adoption. Japan contributes through advanced mixology craftsmanship and premium cocktail innovation, while China’s expanding retail and digital commerce infrastructure supports RTD cocktail penetration. Increasing Western cultural influence and tourism recovery further strengthen regional demand.

Middle East & Africa

The Middle East and Africa region is witnessing gradual expansion, led by the UAE and South Africa through tourism-driven hospitality growth and luxury lifestyle development. Regional growth is supported by expanding premium hotel infrastructure, international events, and rising demand for high-end dining experiences. While regulatory environments vary significantly across countries, hotel bars and licensed venues continue to broaden cocktail offerings to attract international travelers and affluent consumers. Growth in non-alcoholic cocktails is particularly strong due to cultural preferences and wellness trends.

Latin America

Latin America demonstrates steady market expansion, with Brazil and Mexico dominating regional demand due to deeply rooted cocktail traditions centered around tequila, rum, and regional spirits. Growth is supported by expanding tourism activity, increasing urban nightlife development, and rising popularity of premium beverage experiences among younger consumers. Cultural festivals, beach tourism, and hospitality investments continue to stimulate on-trade consumption, while improving retail distribution networks are enabling broader availability of ready-to-drink cocktails across the region.

Key Players in the Cocktail Market

- Diageo plc

- Pernod Ricard SA

- Bacardi Limited

- Brown-Forman Corporation

- Beam Suntory Inc.

- Campari Group

- Rémy Cointreau

- Constellation Brands Inc.

- Molson Coors Beverage Company

- Anheuser-Busch InBev

- Asahi Group Holdings

- Kirin Holdings Company

- Davide Campari-Milano N.V.

- Heineken N.V.

- William Grant & Sons