Citrus Beverage Cloud Market Size

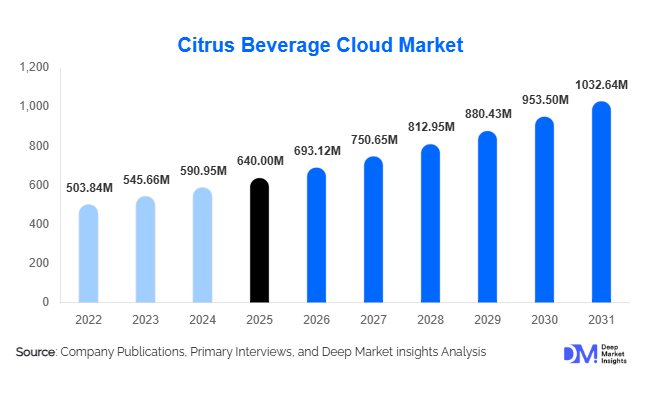

According to Deep Market Insights, the global citrus beverage cloud market size was valued at USD 640 million in 2025 and is projected to grow from USD 693.12 million in 2026 to reach USD 1,032.64 million by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The citrus beverage cloud market growth is primarily driven by rising global consumption of citrus-flavored beverages, increasing demand for clean-label and natural ingredient formulations, and expanding production of carbonated soft drinks (CSDs), ready-to-drink (RTD) juices, and alcoholic RTD beverages. Citrus beverage cloud plays a critical role in enhancing turbidity, visual appeal, and mouthfeel in beverages, reinforcing consumer perception of authenticity and fruit content. Rapid expansion of beverage manufacturing in Asia-Pacific and Latin America, combined with technological advancements in emulsion stability and shelf-life enhancement, is strengthening market fundamentals globally.

Key Market Insights

- Orange-based citrus cloud dominates globally, accounting for nearly 48% of total demand due to strong consumption of orange-flavored beverages.

- Liquid citrus cloud form leads the market, supported by ease of blending and compatibility with large-scale beverage manufacturing lines.

- Asia-Pacific is the fastest-growing region, driven by expanding RTD beverage markets in China and India.

- Conventional variants account for the majority share, although organic and clean-label segments are expanding at a faster pace.

- Carbonated soft drinks remain the largest application segment, supported by stable global production volumes.

- Technological innovation in emulsion stabilization is enhancing product performance in low-sugar and functional beverages.

What are the latest trends in the citrus beverage cloud market?

Clean-Label and Natural Emulsion Systems

Beverage manufacturers are increasingly reformulating citrus beverages to eliminate synthetic emulsifiers and artificial stabilizers. Natural cloud systems utilizing gum arabic, modified starch, and plant-derived stabilizers are gaining widespread adoption, particularly in North America and Europe. Consumers associate clean-label formulations with higher quality and safety, prompting beverage brands to invest in ingredient transparency. As regulatory scrutiny around food additives intensifies, suppliers are prioritizing research and development in natural emulsion systems that maintain turbidity stability while complying with international standards.

Growth of Functional and Alcoholic RTD Beverages

The expansion of vitamin-enriched beverages, botanical-infused drinks, and hard seltzers is broadening application scope for citrus beverage cloud. Alcoholic RTD formulations require stable cloud systems that perform consistently under varying alcohol concentrations, creating opportunities for customized formulations. Functional beverages fortified with vitamin C, electrolytes, and plant extracts rely on advanced cloud systems to preserve visual appeal and mouthfeel. This diversification of end-use applications is significantly contributing to market expansion.

What are the key drivers in the citrus beverage cloud market?

Rising Global Consumption of Citrus-Flavored Beverages

Citrus flavors consistently rank among the top beverage flavor categories worldwide. Strong demand for orange, lemon, and lime-based beverages across carbonated and non-carbonated segments is directly increasing demand for citrus cloud systems. Urbanization and higher disposable incomes in emerging markets are further accelerating consumption patterns.

Premiumization and Visual Authenticity in Beverages

Consumers increasingly equate turbidity with authenticity in fruit beverages. Beverage brands use citrus cloud formulations to enhance opacity and replicate freshly squeezed juice aesthetics. Premium beverage positioning and packaging innovation are reinforcing demand for high-performance cloud systems.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in citrus oil and gum arabic prices, largely influenced by climatic conditions in major producing countries such as Brazil and Mexico, impact production costs and profit margins. Price instability can limit long-term contract pricing stability for manufacturers.

Stringent Regulatory Compliance

Food safety regulations across Europe and North America require extensive testing, documentation, and labeling compliance. Reformulation costs and certification requirements create operational challenges for smaller manufacturers.

What are the key opportunities in the citrus beverage cloud industry?

Expansion in Emerging Markets

Rapid beverage market growth in Asia-Pacific and Latin America offers strong expansion potential. Establishing regional blending and technical centers can improve supply chain efficiency and capture growing demand from local beverage manufacturers.

Customized High-Performance Cloud Systems

Innovation in cloud stability for low-sugar, plant-based, and alcoholic beverages presents lucrative opportunities. Tailored formulations designed for specific beverage matrices can command premium pricing and enhance long-term supplier partnerships.

Product Type Insights

Single-strength citrus cloud holds the largest market share at approximately 42% in 2025, primarily due to its cost-effectiveness, formulation simplicity, and broad compatibility across mainstream beverage applications. Its ability to deliver stable turbidity, natural appearance, and consistent mouthfeel in high-volume production environments makes it the preferred choice for carbonated soft drinks and ready-to-drink (RTD) beverages. The leading segment driver for single-strength variants is the continued expansion of mass-market beverage production, particularly in emerging economies where pricing competitiveness and operational efficiency are critical.

Double-strength and customized functional cloud systems are gaining traction, particularly in premium beverage categories where enhanced opacity, suspension stability, and improved flavor retention are required. These advanced systems are increasingly utilized in fortified beverages, plant-based drinks, and alcoholic RTDs where formulation complexity is higher. Custom-formulated citrus clouds designed for fortified and alcoholic beverages are expected to witness higher growth rates during the forecast period, driven by innovation in functional beverages and premiumization trends across developed markets.

Source Fruit Insights

Orange-based citrus cloud leads the market with nearly 48% share in 2025, supported by dominant global demand for orange-flavored beverages across carbonated drinks, juices, and nectars. The leading driver for this segment is the sustained global consumption of orange-flavored carbonated soft drinks and juice-based RTDs, particularly in North America and Asia-Pacific. Orange variants offer balanced acidity, natural color appeal, and broad consumer acceptance, reinforcing their market leadership.

Lemon and lime-based variants collectively account for around 34% of total market share, driven by increasing demand in flavored waters, sparkling beverages, and low-calorie drink formulations. Their growth is supported by rising consumer preference for refreshing, citrus-forward taste profiles and reduced-sugar beverages. Grapefruit and blended citrus clouds represent niche yet expanding segments, particularly in functional beverages and alcoholic RTD categories, where differentiated flavor positioning and premium branding strategies are gaining momentum.

Form Insights

Liquid citrus cloud dominates the market, accounting for approximately 67% of total revenue in 2025. Its ease of incorporation into high-speed bottling lines, superior dispersion stability, and compatibility with automated blending systems make it the preferred format for large-scale beverage manufacturers. The leading segment driver is operational efficiency, as liquid formulations reduce processing time and ensure consistent turbidity in large production batches.Powdered citrus cloud is primarily utilized in beverage concentrates, dry mixes, and export-oriented premixes. While holding a smaller share, this format offers logistical and storage advantages, particularly in regions with extended supply chains or limited cold storage infrastructure. Its growing adoption in international trade and contract manufacturing supports steady demand growth.

Application Insights

Carbonated soft drinks represent the largest application segment, holding nearly 36% of the market in 2025. The leading driver for this segment is the sustained global production of citrus-flavored carbonated beverages, where citrus cloud plays a critical role in delivering visual opacity and authentic juice-like appearance. Despite evolving consumer trends, carbonated beverages remain a foundational category for citrus cloud demand.

RTD juices and nectars follow closely, supported by increasing consumption of packaged fruit beverages in urban markets. Functional beverages and alcoholic RTDs are emerging as high-growth applications, driven by product diversification, premiumization strategies, and innovation in botanical and citrus-infused alcohol blends. The expansion of beverage portfolios globally is reinforcing stable demand across multiple categories, ensuring balanced application growth.

Nature Insights

Conventional citrus cloud accounts for approximately 78% of market share in 2025, primarily driven by cost sensitivity in emerging markets and large-scale beverage manufacturing economics. The leading driver for this segment is price competitiveness combined with reliable performance in high-volume production.Organic and clean-label certified variants are expanding at a faster CAGR of nearly 10%, reflecting shifting consumer preferences in developed regions toward natural, minimally processed ingredients. Regulatory pressures, transparent labeling requirements, and sustainability initiatives are further accelerating demand for certified and traceable citrus cloud solutions.

| By Product Type | By Source Fruit | By Form | By Application | By Nature | By Distribution Model |

|---|---|---|---|---|---|

|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of global market share in 2025, led by strong beverage production in the United States. The United States remains the primary growth engine due to its advanced beverage processing infrastructure and high per capita consumption of carbonated and RTD beverages. Regional growth is driven by clean-label reformulations, premium beverage innovation, and increasing demand for functional and fortified drinks. Additionally, the presence of multinational beverage manufacturers and continuous product innovation supports sustained demand for advanced citrus cloud systems.

Europe

Europe holds nearly 24% of global share, with Germany, France, the U.K., Italy, and Spain driving demand. Growth in this region is strongly influenced by stringent regulatory compliance standards, sustainability initiatives, and reformulation strategies aimed at reducing artificial additives. The shift toward organic and clean-label beverages, along with premium alcoholic RTDs, is accelerating adoption of customized citrus cloud solutions. Environmental considerations and traceability requirements are further shaping product development and supplier selection.

Asia-Pacific

Asia-Pacific leads with around 31% share and is the fastest-growing region at approximately 9.5% CAGR. China and India are key contributors due to rapidly expanding RTD beverage industries, urbanization, and rising middle-class consumption. Increasing disposable income, growth of convenience retail formats, and expansion of domestic beverage brands are key regional growth drivers. Additionally, the diversification of flavor profiles and adoption of Western-style carbonated drinks are reinforcing long-term market expansion across Southeast Asia and Oceania.

Latin America

Latin America accounts for about 12% of the market, with Brazil and Mexico serving as both major producers and consumers of citrus-based ingredients. The region benefits from abundant citrus fruit cultivation, supporting localized production and supply chain advantages. Growth drivers include strong regional consumption of citrus-flavored carbonated beverages, increasing penetration of packaged juices, and expanding beverage exports to North America and Europe.

Middle East & Africa

The Middle East & Africa region represents nearly 5% share, supported by increasing urbanization and rising demand for flavored beverages in Saudi Arabia, the UAE, and South Africa. Expanding retail infrastructure, growing youth demographics, and higher consumption of non-alcoholic beverages are key regional growth drivers. Additionally, rising tourism and hospitality sector expansion in Gulf countries are contributing to increasing beverage innovation and diversified product offerings.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Citrus Beverage Cloud Market

- Givaudan SA

- Firmenich SA

- Symrise AG

- International Flavors & Fragrances Inc.

- Kerry Group plc

- Sensient Technologies Corporation

- Döhler Group

- ADM

- Tate & Lyle PLC

- Cargill Incorporated

- Takasago International Corporation

- Flavorchem Corporation

- Robertet Group

- Frutarom Industries Ltd

- BASF SE