Citric Acid Market Size

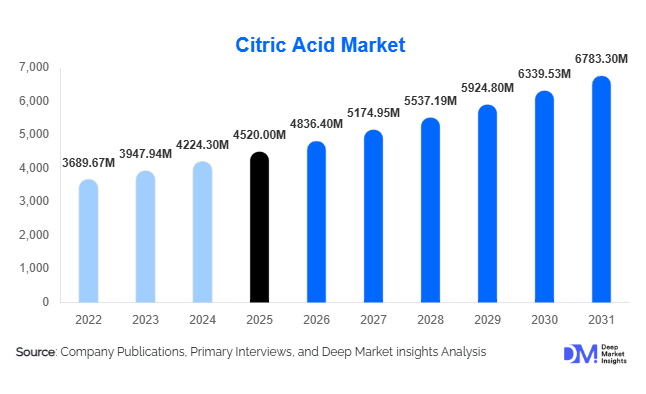

According to Deep Market Insights, the global citric acid market size was valued at USD 4,520 million in 2025 and is projected to grow from USD 4,836.40 million in 2026 to reach USD 6,783.30 million by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). Market growth is primarily driven by rising demand for processed foods and beverages, increasing adoption of bio-based ingredients, and expanding applications in pharmaceuticals, nutraceuticals, and eco-friendly cleaning solutions. Citric acid’s multifunctional properties as an acidulant, preservative, and chelating agent make it an essential ingredient across multiple industries, supporting steady long-term demand growth worldwide.

Key Market Insights

- Food and beverage applications dominate global demand, accounting for the majority of citric acid consumption due to its role in flavor enhancement and shelf-life stabilization.

- Fermentation-based production exceeds 95% of global supply, reflecting industry preference for sustainable and cost-efficient manufacturing methods.

- Asia-Pacific leads both production and consumption, supported by large-scale fermentation capacity and strong export networks.

- Pharmaceutical and nutraceutical applications are the fastest-growing segments, driven by effervescent formulations and preventive healthcare trends.

- Eco-friendly cleaning products are creating new demand streams, as citric acid replaces phosphates and harsh chemical agents.

- Long-term supply contracts and direct industrial distribution are becoming dominant procurement models among large buyers.

What are the latest trends in the citric acid market?

Shift Toward Clean-Label and Natural Ingredients

Food manufacturers are increasingly replacing synthetic additives with fermentation-derived ingredients that align with clean-label standards. Citric acid, naturally produced through microbial fermentation, is gaining preference among global food and beverage companies seeking transparent ingredient labeling. Rising consumer awareness regarding artificial preservatives has accelerated adoption in flavored beverages, ready-to-eat foods, confectionery, and plant-based products. Clean-label positioning has become a competitive differentiator, encouraging manufacturers to invest in traceable and non-GMO production processes.

Expansion of Green Cleaning Formulations

The transition toward environmentally sustainable cleaning products represents a major industry trend. Citric acid’s biodegradable nature and effective descaling capabilities make it a preferred ingredient in household and industrial cleaners. Regulatory pressure to reduce phosphate-based detergents across Europe and North America is accelerating adoption. Manufacturers are increasingly marketing plant-based cleaning solutions that utilize citric acid as a core active ingredient, supporting growth beyond traditional food applications.

What are the key drivers in the citric acid market?

Rising Processed Food and Beverage Consumption

Urbanization and changing lifestyles continue to increase consumption of packaged foods and ready-to-drink beverages globally. Citric acid plays a critical role in maintaining flavor balance, acidity regulation, and microbial stability, making it indispensable for beverage manufacturers. Growth in energy drinks, flavored water, and functional beverages has significantly strengthened demand.

Growing Adoption of Bio-Based Industrial Chemicals

Industries are transitioning toward renewable and environmentally safe chemicals to meet sustainability targets. Citric acid serves as an effective substitute for synthetic acids and chelating agents in detergents, water treatment, and industrial cleaning processes. Government regulations promoting biodegradable chemicals are further reinforcing this shift.

What are the restraints for the global market?

Raw Material Price Volatility

Citric acid production relies heavily on sugar substrates such as corn and molasses. Fluctuations in agricultural commodity prices can significantly impact manufacturing costs and profit margins. Supply disruptions or unfavorable harvest cycles may result in price instability across global markets.

Production Concentration and Supply Chain Risks

A large share of global citric acid production capacity is concentrated in Asia, particularly China. This geographic concentration creates risks related to trade policies, logistics disruptions, and energy cost fluctuations, potentially affecting global supply availability and pricing stability.

What are the key opportunities in the citric acid industry?

Growth in Pharmaceutical and Nutraceutical Applications

The expanding global nutraceutical industry presents strong opportunities for pharmaceutical-grade citric acid. Effervescent tablets, mineral supplements, and buffered formulations rely heavily on citric acid for stability and absorption enhancement. Aging populations and preventive healthcare adoption are expected to sustain long-term demand growth.

Emerging Demand from Sustainable Cleaning Products

The rapid growth of eco-certified cleaning brands offers new market entry opportunities. Companies developing biodegradable detergents and institutional cleaning solutions are increasingly incorporating citric acid as a natural alternative to harsh chemicals. This trend is particularly strong in Europe and North America, where environmental regulations are tightening.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4520 Million |

| Market Size in 2026 | USD 4836.40 Million |

| Market Size in 2031 | USD 6783.30 Million |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global citric acid market is structurally led by anhydrous citric acid, which accounts for approximately 52% of total market demand owing to its superior stability, extended shelf life, and compatibility with dry and powdered formulations. Its widespread use in instant beverage powders, confectionery coatings, seasoning blends, and processed food applications positions it as the preferred product form among large-scale food manufacturers seeking longer storage durability and efficient transportation logistics. The increasing global demand for convenience foods and ready-to-mix beverages continues to strengthen the adoption of anhydrous citric acid, particularly in export-oriented food production environments where moisture sensitivity remains a critical concern.Citric acid monohydrate maintains strong demand across liquid-based applications due to its excellent solubility characteristics and ease of formulation integration. Pharmaceutical manufacturers extensively utilize this form in syrups, effervescent tablets, and nutraceutical products where controlled dissolution and bioavailability are essential. Growth in health supplements and over-the-counter medicines has reinforced the relevance of monohydrate variants, especially in regions experiencing expanding healthcare access and aging populations.Liquid citric acid solutions are gaining increasing commercial traction in industrial processing and institutional cleaning applications. Their ability to enable precise dosing, reduce handling complexity, and improve operational efficiency makes them particularly attractive for large manufacturing facilities and automated production systems. Rising adoption of sustainable industrial cleaning agents and descaling solutions further contributes to the expansion of liquid formulations. Continuous advancements in microbial fermentation technology, strain optimization, and downstream purification processes have enhanced production efficiency, reduced environmental impact, and improved consistency across all product forms, supporting long-term market scalability.

Application Insights

Food and beverage applications remain the dominant revenue-generating segment, contributing nearly 60% of global citric acid consumption. The leading driver for this segment is the growing global preference for flavor enhancement, natural preservation, and acidity regulation in processed foods and beverages. Carbonated soft drinks, flavored waters, confectionery products, dairy alternatives, sauces, and ready-to-eat meals extensively rely on citric acid to maintain taste balance, microbial stability, and product shelf life. Increasing consumer demand for clean-label ingredients and naturally derived additives further strengthens citric acid’s position as a preferred acidulant compared to synthetic alternatives.Pharmaceutical applications are witnessing accelerated expansion as citric acid plays a critical role in effervescent drug formulations, mineral supplements, and pH buffering systems. The rapid growth of preventive healthcare, dietary supplementation, and functional medicines is driving higher utilization rates, particularly in emerging economies where healthcare infrastructure is improving. In addition, citric acid supports enhanced drug stability and palatability, making it essential for pediatric and geriatric formulations.The personal care and cosmetics sector continues to integrate citric acid for pH adjustment, antioxidant stabilization, and preservative enhancement in skincare, haircare, and hygiene products. Growing consumer awareness regarding product safety and mild formulation chemistry has encouraged manufacturers to incorporate multifunctional organic acids. Industrial cleaning applications are emerging as a strong growth avenue, supported by sustainability initiatives promoting biodegradable and phosphate-free cleaning agents. Meanwhile, animal feed applications maintain stable demand as citric acid improves mineral absorption, supports gut health, and enhances feed preservation efficiency, particularly in poultry and aquaculture industries.

Distribution Channel Insights

Direct industrial sales dominate the global distribution landscape, accounting for more than half of total transactions as large beverage producers, pharmaceutical companies, and detergent manufacturers secure long-term supply agreements to stabilize procurement costs and ensure uninterrupted raw material availability. The leading driver of this segment is the growing need for supply chain reliability amid fluctuating raw material prices and increasing global production volumes. Strategic partnerships between citric acid producers and multinational manufacturers enable predictable pricing structures and optimized logistics planning.Ingredient distributors continue to play a vital role in serving small and medium-sized manufacturers that require flexible purchasing volumes, technical formulation support, and localized inventory access. These distributors facilitate market penetration in developing regions where direct procurement infrastructure remains limited. The rapid digitalization of procurement systems is transforming distribution dynamics, with online sourcing platforms, automated inventory tracking, and contract-based digital marketplaces improving transparency, traceability, and operational efficiency across global supply chains. As cross-border trade expands, integrated logistics solutions and regional warehousing networks are expected to further enhance distribution efficiency.

End-Use Industry Insights

The food processing and beverage manufacturing industries remain the largest end-use sectors for citric acid, supported by expanding global consumption of packaged foods and beverages growing at an annual rate exceeding 6%. The leading driver for this segment is the continuous innovation in processed food formulations aimed at extending shelf life while maintaining flavor integrity and regulatory compliance with clean-label standards. Rapid urbanization, busy consumer lifestyles, and rising demand for convenience foods continue to reinforce long-term industry demand.Pharmaceutical manufacturing represents the fastest-growing end-use industry, fueled by increasing global healthcare expenditure, rising nutraceutical consumption, and expansion of generic drug production. Citric acid’s multifunctional properties as a buffering agent, stabilizer, and flavor enhancer make it indispensable across multiple dosage forms. Growth in preventive healthcare and wellness-oriented consumption patterns is expected to further accelerate demand.The detergent and cleaning industry is experiencing accelerated adoption of citric acid as manufacturers transition toward environmentally friendly and biodegradable product formulations. Increasing regulatory restrictions on harsh chemicals and phosphates are encouraging the replacement of traditional cleaning agents with organic acid-based alternatives. Additionally, emerging industrial applications such as biodegradable plastics processing, metal treatment, and water treatment chemicals are broadening the material’s industrial relevance and creating new avenues for market diversification.

Explore more data points, trends and opportunities Download Free Sample Report

Citric Acid Market Segmentations

By Product Type

- Anhydrous Citric Acid

- Citric Acid Monohydrate

- Liquid Citric Acid

By Application

- Food & Beverages

- Pharmaceuticals & Nutraceuticals

- Personal Care & Cosmetics

- Industrial Cleaning & Detergents

- Animal Feed Additives

By Distribution Channel

- Direct Industrial Sales

- Ingredient Distributors

- Online B2B Procurement Platforms

Regional Insights

North America

North America accounts for approximately 20% of global citric acid demand, with the United States serving as the primary consumption hub. Regional growth is driven by strong consumer preference for clean-label and naturally sourced food ingredients, which encourages manufacturers to replace synthetic additives with fermentation-derived acids. The expansion of premium beverage categories, including functional drinks and low-sugar formulations, continues to increase citric acid usage for flavor optimization and preservation. Additionally, stringent environmental regulations are accelerating the adoption of biodegradable cleaning formulations across institutional and household applications. The presence of advanced pharmaceutical manufacturing infrastructure and rising production of dietary supplements further supports sustained demand for pharmaceutical-grade citric acid across the region.

Europe

Europe holds nearly 23% of the global market share, led by Germany, France, and the Netherlands. Regional growth is strongly influenced by strict environmental and food safety regulations that promote sustainable ingredients and bio-based chemicals. The European Union’s emphasis on circular economy initiatives and reduced chemical toxicity is encouraging the adoption of citric acid in eco-friendly detergents and preservation systems. Increasing demand for organic foods, plant-based products, and minimally processed beverages is further driving consumption. In addition, strong research and development capabilities within European food and pharmaceutical industries support innovation in functional formulations, reinforcing long-term market expansion.

Asia-Pacific

Asia-Pacific dominates the global citric acid market with an estimated 46% share in 2025, supported by large-scale production capacity and rapidly expanding consumption markets. China remains the world’s largest producer and exporter due to cost-efficient fermentation infrastructure and integrated supply chains. Regional growth is primarily driven by rising disposable incomes, rapid urbanization, and increasing consumption of packaged foods and beverages across emerging economies such as India, Thailand, and Indonesia. Expanding pharmaceutical manufacturing, government support for domestic chemical production, and strong export-oriented food processing industries further strengthen demand. The growth of e-commerce food distribution and modern retail networks also contributes to higher processed food consumption, reinforcing regional market dominance.

Latin America

Latin America demonstrates steady growth led by Brazil and Mexico, where expanding beverage production and processed food exports are increasing citric acid utilization. Regional market expansion is supported by improving food processing infrastructure, rising urban middle-class populations, and growing investments in packaged food manufacturing. Increasing adoption of modern preservation techniques and the gradual shift toward value-added agricultural processing are enhancing demand across both domestic consumption and export markets. Industrial cleaning applications are also gaining traction as manufacturing modernization initiatives improve sanitation and operational efficiency standards.

Middle East & Africa

The Middle East and Africa region represents the fastest-growing citric acid market, driven by rapid urbanization, population growth, and increasing reliance on processed and imported food products. Expanding food processing industries in countries such as the UAE, Saudi Arabia, and South Africa are creating new demand for preservation and flavor-enhancing ingredients. Growth in hospitality, institutional cleaning, and water treatment sectors is accelerating adoption of citric acid-based cleaning solutions due to their biodegradability and safety profile. Additionally, government initiatives aimed at strengthening pharmaceutical manufacturing capabilities and diversifying industrial economies are contributing to rising regional consumption, positioning the region as a high-growth market over the forecast period.

Key Players in the Citric Acid Market

- Archer Daniels Midland Company (ADM)

- Cargill Incorporated

- Tate & Lyle PLC

- Jungbunzlauer Suisse AG

- COFCO Biochemical (Anhui) Co., Ltd.

- RZBC Group Co., Ltd.

- TTCA Co., Ltd.

- Huangshi Xinghua Biochemical Co., Ltd.

- Gadot Biochemical Industries Ltd.

- Weifang Ensign Industry Co., Ltd.

- S.A. Citrique Belge N.V.

- Foodchem International Corporation

- Thai Citric Acid Co., Ltd.

- Shandong Lemon Biochemical Co., Ltd.

- Laiwu Taihe Biochemistry Co., Ltd.