Cider Market Size

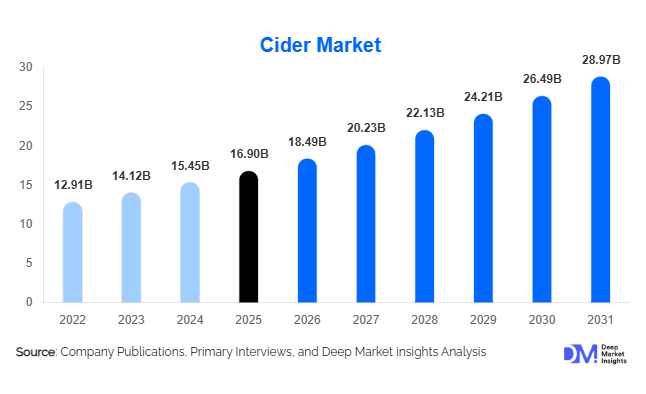

According to Deep Market Insights, the global cider market size was valued at USD 16.9 billion in 2025 and is projected to grow from USD 18.49 billion in 2026 to reach USD 28.97 billion by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). The cider market growth is primarily driven by rising consumer preference for flavored alcoholic beverages, increasing demand for premium craft drinks, and growing adoption of gluten-free and low-alcohol beverage alternatives among younger demographics.

Key Market Insights

- Premium and craft cider categories are witnessing strong global demand, driven by consumers seeking artisanal beverages with authentic ingredients and differentiated flavor profiles.

- Fruit-flavored and botanical-infused cider variants are reshaping product innovation, particularly among millennials and Gen Z consumers looking for experimental drinking experiences.

- Europe dominates the global cider market, supported by established cider-drinking cultures across the United Kingdom, Ireland, France, and Spain.

- Asia-Pacific is the fastest-growing regional market, fueled by rising disposable income, westernized drinking habits, and expanding urban retail infrastructure.

- Low-alcohol and alcohol-free cider products are gaining traction, as health-conscious consumers moderate alcohol consumption while maintaining social drinking preferences.

- Sustainable packaging and can-based cider formats are expanding rapidly, supported by portability, lower logistics costs, and increasing environmental awareness among consumers.

Cider Market Latest Trends

Premium Craft Cider Expansion

The global cider industry is increasingly shifting toward premium and craft beverage offerings. Consumers are showing greater willingness to spend on artisanal cider products made with locally sourced apples, organic ingredients, and small-batch fermentation methods. Craft cider makers are introducing seasonal flavors, barrel-aged variants, and farmhouse-style cider to create differentiated experiences. Premiumization trends are especially strong across North America and Europe, where consumers associate craft beverages with authenticity, sustainability, and superior taste profiles. Manufacturers are also investing heavily in premium glass packaging, sustainable sourcing, and limited-edition product launches to strengthen brand loyalty and improve margins.

Rapid Growth of Low-Alcohol and Alcohol-Free Cider

Health-conscious consumers are driving strong demand for low-alcohol and alcohol-free cider products globally. Younger consumers are increasingly moderating alcohol intake while still participating in social drinking occasions. Beverage companies are responding with innovative alcohol-free cider variants featuring natural sweeteners, fruit infusions, and functional ingredients. Supermarkets, cafes, and online retail platforms are expanding shelf space for alcohol-free alternatives, particularly across Europe and North America. This trend is expected to create a significant secondary growth channel for cider manufacturers over the forecast period.

Cider Market Drivers

Growing Demand for Flavored Alcoholic Beverages

Consumers worldwide are increasingly shifting toward fruit-flavored alcoholic beverages that offer refreshing taste profiles and lighter drinking experiences compared to traditional beer and spirits. Berry, citrus, tropical fruit, and mixed-fruit cider variants are experiencing strong demand across bars, restaurants, and retail channels. Younger demographics are particularly attracted to innovative flavor combinations and premium packaging formats. This trend has encouraged manufacturers to continuously diversify flavor portfolios, expand limited-edition launches, and strengthen seasonal product offerings to maintain consumer engagement.

Rising Premiumization Across Alcoholic Beverage Industry

The growing global preference for premium alcoholic beverages is significantly supporting cider market growth. Consumers are increasingly prioritizing quality ingredients, artisanal production methods, and authentic brand storytelling. Premium and craft cider categories are recording faster growth compared to mass-market products, particularly in developed economies. Barrel-aged cider, farmhouse cider, and organic variants are enabling companies to improve pricing power and profit margins. Premium packaging innovation, including aluminum cans and sustainable glass bottles, is also improving shelf visibility and consumer perception.

Global Market Restraints

Regulatory and Taxation Challenges

The cider industry faces strict alcohol regulations and taxation policies across multiple countries. Governments continue to impose excise duties, advertising restrictions, labeling requirements, and alcohol sales limitations that directly impact profitability and market expansion. Regulatory frameworks related to sugar content disclosures and sustainability compliance are becoming increasingly stringent, especially across Europe and North America. Such regulations can increase operating costs for cider manufacturers and create barriers for smaller producers entering the market.

Intense Competition from Alternative Alcoholic Beverages

The cider market faces rising competition from hard seltzers, flavored beers, ready-to-drink cocktails, and premium spirits. Consumers frequently shift preferences based on pricing, health trends, and evolving lifestyle choices. Hard seltzers and low-calorie alcoholic beverages, in particular, have intensified competition among younger consumers. This creates constant pressure on cider producers to innovate rapidly, launch differentiated products, and maintain competitive pricing structures while preserving brand relevance.

Cider Industry Key Opportunities

Expansion in Asia-Pacific Markets

Asia-Pacific presents substantial untapped growth opportunities for global cider manufacturers. Rising urbanization, western dining trends, and increasing disposable income are driving alcoholic beverage demand in countries such as China, India, Vietnam, and South Korea. International beverage companies are increasingly partnering with local distributors and e-commerce platforms to improve regional penetration. In many Asian markets, cider is positioned as a lighter and more approachable alternative to beer and spirits, particularly among younger urban consumers and female demographics. Investments in localized flavors and digital engagement strategies are expected to strengthen long-term growth across the region.

Growth of Sustainable and Organic Cider

Sustainability-driven consumer behavior is creating new opportunities for organic and environmentally responsible cider production. Consumers are increasingly prioritizing beverages produced using organic apples, recyclable packaging, and carbon-neutral manufacturing processes. Manufacturers adopting sustainable farming partnerships, renewable energy integration, and eco-friendly packaging are gaining competitive advantages among environmentally conscious buyers. Organic cider categories are also generating higher profit margins due to premium pricing and strong consumer perception regarding health and quality.

Product Type Insights

Alcoholic cider continues to dominate the global cider market, accounting for nearly 82% of total market revenue in 2025. The strong position of alcoholic cider is primarily driven by rising global consumption of flavored alcoholic beverages, expanding craft alcohol culture, and increasing consumer preference for gluten-free alternatives to beer. Traditional apple cider maintains the largest market share due to long-standing consumer familiarity, established production infrastructure, and extensive availability across Europe and North America. Leading manufacturers are increasingly introducing premium apple cider variants with natural ingredients, lower sugar content, and artisanal production techniques to strengthen brand differentiation and premium positioning.Premium and craft cider categories are rapidly expanding worldwide, supported by rising disposable income, premiumization trends within the alcoholic beverage industry, and growing consumer interest in artisanal and locally produced beverages. Additionally, non-alcoholic cider is emerging as a high-growth segment as health-conscious consumers increasingly adopt alcohol moderation lifestyles without compromising social drinking experiences. The expansion of low-alcohol and alcohol-free beverage portfolios by major beverage companies is expected to further support long-term market growth.

Flavor Profile Insights

Apple-based cider remains the dominant flavor segment within the global cider market, accounting for nearly 58% of global consumption in 2025. The leadership of this segment is driven by strong traditional consumer preference, abundant apple cultivation across major producing countries, and the widespread availability of classic apple cider products in both retail and hospitality channels. Apple cider continues to benefit from its broad flavor acceptance among mainstream consumers and its strong association with authentic cider heritage, particularly across the United Kingdom, France, and the United States.Pear cider and mixed-fruit variants are steadily gaining market traction as consumers increasingly seek diverse taste experiences and premium beverage alternatives. Berry-based, tropical, and exotic fruit-flavored cider products are recording particularly strong growth among millennials and Gen Z consumers due to rising experimentation with flavored alcoholic beverages and growing influence from social media beverage trends. Manufacturers are also leveraging seasonal flavors and limited-edition launches to improve brand engagement and increase repeat purchases.Botanical and herbal-infused cider products are emerging as niche premium offerings within urban markets, supported by rising consumer interest in wellness-oriented beverages, natural ingredients, and craft beverage innovation. The increasing popularity of low-sugar, organic, and naturally flavored cider formulations is expected to further diversify flavor innovation across global markets during the forecast period.

Packaging Insights

Glass bottles continue to dominate global cider packaging, accounting for approximately 49% of total market share in 2025. The dominance of glass packaging is largely driven by its premium brand perception, superior product preservation capabilities, and extensive usage across bars, pubs, restaurants, and premium hospitality venues. Glass bottles remain strongly associated with traditional and craft cider consumption, particularly in mature European markets where premium presentation and authenticity play a significant role in consumer purchasing behavior.However, aluminum cans are witnessing the fastest growth rates globally owing to increasing demand for portable, lightweight, and sustainable beverage packaging solutions. The rapid expansion of outdoor entertainment activities, music festivals, sports events, and convenience-based consumption is significantly increasing the popularity of canned cider formats. In addition, cans offer lower transportation costs, improved storage efficiency, and higher recyclability, making them increasingly attractive for manufacturers seeking operational efficiency and sustainability compliance.Manufacturers are also investing heavily in eco-friendly and recyclable packaging materials to align with evolving environmental regulations and growing consumer awareness regarding sustainable packaging. Innovations in lightweight bottles, biodegradable labels, and reduced-carbon packaging solutions are expected to further influence future packaging trends within the global cider market.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel within the global cider market, accounting for nearly 37% of total sales revenue in 2025. The dominance of this segment is driven by extensive product visibility, strong consumer accessibility, competitive pricing strategies, and the availability of a wide range of domestic and imported cider brands under a single retail environment. Large retail chains also support higher product penetration through promotional campaigns, seasonal product placements, and expanding premium beverage sections.Specialty liquor stores continue to maintain strong market performance, particularly within premium, imported, and craft cider categories. Consumers seeking artisanal products, exclusive flavor offerings, and premium international brands frequently prefer specialty alcohol retailers due to their broader product expertise and curated selections.Online retail and direct-to-consumer distribution channels are experiencing rapid expansion due to rising alcohol e-commerce penetration, increasing smartphone usage, and growing adoption of digital marketing strategies by beverage companies. Subscription-based beverage delivery services, app-based alcohol delivery platforms, and quick-commerce models are further accelerating cider accessibility in urban markets. The growing preference for home delivery convenience and personalized purchasing experiences is expected to continue strengthening online cider sales globally.

Price Category Insights

Mid-range cider products account for the largest share of the global cider market, representing nearly 44% of total revenue in 2025. The leadership of this segment is primarily driven by strong demand from mainstream consumers seeking a balance between affordability, product quality, and flavor diversity. Mid-priced cider offerings benefit from wide retail availability, attractive promotional pricing, and growing consumer willingness to explore flavored alcoholic beverages without entering ultra-premium price categories.Premium and super-premium cider categories are witnessing significantly faster growth due to increasing disposable income levels, rising demand for craft alcoholic beverages, and expanding consumer preference for artisanal and imported beverage products. Consumers are increasingly associating premium cider with higher-quality ingredients, authentic production methods, unique flavor profiles, and sophisticated packaging formats. Craft cider producers are particularly benefiting from premiumization trends across developed economies.Economy cider products continue to maintain steady demand in price-sensitive markets, particularly across developing regions where affordability remains a key purchasing factor. However, ongoing premiumization trends and rising urban consumer spending are gradually shifting global consumption patterns toward higher-value cider offerings.

End-Use Insights

Household consumption remains the dominant end-use segment within the global cider market, accounting for nearly 52% of total demand in 2025. The leadership of this segment is driven by increasing at-home socialization trends, growing popularity of home entertainment, and the rapid expansion of alcohol delivery services worldwide. Retail-oriented consumption strengthened considerably as consumers increasingly preferred convenient and affordable at-home beverage experiences supported by expanding e-commerce and quick-commerce alcohol platforms.The HoReCa sector represents one of the fastest-growing end-use segments, supported by the continued expansion of premium pubs, restaurants, hotels, and tourism-driven hospitality industries. Rising consumer interest in craft beverages, premium dining experiences, and experiential consumption is further increasing cider penetration across hospitality venues globally.Event venues, sports arenas, concerts, and entertainment festivals are also contributing significantly to market growth, particularly for canned cider products due to their portability and convenience. Additionally, travel retail and duty-free channels continue to support premium imported cider sales across major international airport hubs as global tourism and international travel activity continue to recover and expand.

| By Product Type | By Flavor Profile | By Packaging Type | By Distribution Channel | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for nearly 29% of global cider market revenue in 2025, with the United States representing the largest country-level market within the region. Regional growth is being driven by the strong expansion of craft beverage culture, increasing consumer preference for gluten-free alcohol alternatives, rising demand for low-calorie alcoholic beverages, and continuous flavor innovation by both multinational and craft beverage producers. The growing popularity of fruit-flavored, low-sugar, and premium cider products among millennials and Gen Z consumers is further supporting market expansion.The United States continues to witness strong demand for craft and artisanal cider products due to increasing consumer experimentation and the rapid expansion of local cider breweries. Canada is experiencing rising demand for premium organic cider variants supported by health-conscious consumer behavior and growing sustainability awareness. Meanwhile, Mexico is gradually emerging as a promising opportunity market due to rapid urbanization, expanding middle-class populations, evolving alcohol consumption patterns, and increasing penetration of modern retail infrastructure.

Europe

Europe dominates the global cider market with approximately 41% share of total revenue in 2025. The region’s leadership is primarily supported by deeply established cider-drinking traditions, strong domestic apple production, advanced cider manufacturing infrastructure, and high per capita alcohol consumption across several European countries. Europe also benefits from a highly developed craft beverage ecosystem and strong consumer preference for premium alcoholic products.The United Kingdom remains the largest cider-consuming country globally due to its longstanding cider heritage, extensive local production capacity, and strong pub culture. France maintains substantial demand through premium apple and pear cider production concentrated in regions such as Normandy and Brittany, where traditional cider-making practices continue to support premium product positioning. Ireland and Spain are also witnessing stable market expansion supported by tourism growth, hospitality consumption, and increasing availability of flavored and craft cider products.Europe additionally leads global innovation in organic cider production, sustainable packaging technologies, premium craft cider development, and low-alcohol beverage innovation. Strong regulatory support for sustainable manufacturing and growing consumer demand for natural and locally sourced beverages are expected to continue supporting regional market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing regional cider market and is projected to record a CAGR exceeding 12% during the forecast period. Regional growth is being driven by rapid urbanization, rising disposable income, expanding middle-class populations, westernization of food and beverage consumption patterns, and increasing adoption of flavored alcoholic beverages among younger consumers. The growing influence of international beverage brands and expanding digital alcohol delivery platforms are also accelerating cider penetration across major urban centers.Australia remains the leading cider-producing and consuming country within the region due to high alcohol consumption levels, strong local manufacturing capabilities, and established consumer familiarity with cider products. China and India are emerging as major high-growth markets supported by increasing youth populations, premiumization trends, rising social drinking culture, and expanding organized retail infrastructure. Japan and South Korea are witnessing growing demand for premium imported cider, fruit-based alcoholic beverages, and low-alcohol drink alternatives driven by evolving consumer lifestyle preferences.The expansion of supermarkets, convenience retail chains, e-commerce alcohol platforms, and app-based delivery services is significantly improving product accessibility throughout the region. Increasing investments by international beverage companies in regional manufacturing and distribution partnerships are expected to further strengthen Asia-Pacific market growth.

Latin America

Latin America is experiencing gradual cider market development led by Brazil, Argentina, and Chile. Regional growth is supported by rising urbanization, expanding middle-class income levels, increasing exposure to international beverage trends, and growing demand for premium alcoholic beverages among younger consumers. The rising popularity of flavored alcoholic drinks and social consumption culture is further encouraging market expansion across urban centers.Imported European cider brands are gaining popularity within premium retail channels, hotels, restaurants, and hospitality sectors due to increasing consumer interest in international beverage experiences. Craft cider categories are also gradually expanding as local producers introduce fruit-based and regionally inspired flavor variants tailored to evolving consumer preferences. Improvements in retail distribution networks and expanding modern trade infrastructure are expected to support future market growth across the region.

Middle East & Africa

The Middle East & Africa currently represents a smaller share of the global cider market; however, the region is witnessing steady expansion supported by tourism growth, premium hospitality development, and rising expatriate populations in key economies. Market growth is particularly concentrated in tourism-driven countries such as the UAE and South Africa, where international consumer exposure and premium dining culture continue to strengthen demand for imported cider products.South Africa benefits from favorable apple cultivation conditions, expanding local craft beverage production, and increasing consumer interest in premium flavored alcoholic drinks. The UAE continues to support imported premium cider sales through luxury hotels, restaurants, entertainment venues, and international tourism activity. Increasing investments in hospitality infrastructure, modern retail expansion, and premium beverage distribution networks are expected to further support regional cider market growth over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Cider Market

- Heineken N.V.

- Carlsberg Group

- C&C Group plc

- Molson Coors Beverage Company

- Asahi Group Holdings

- Thatchers Cider

- Aston Manor Cider

- The Boston Beer Company

- Kopparbergs Bryggeri

- Westons Cider