Chocolate-Coated Inclusions Market Size

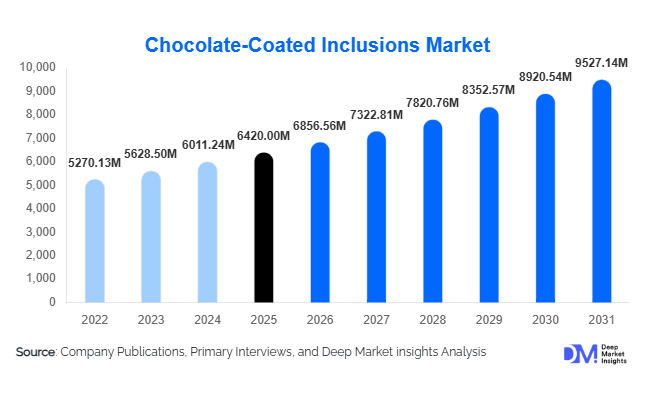

According to Deep Market Insights, the global chocolate-coated inclusions market size was valued at USD 6,420 million in 2025 and is projected to grow from USD 6,856.56 million in 2026 to reach USD 9,527.14 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The chocolate-coated inclusions market growth is primarily driven by rising demand for premium snacking, increasing applications in protein and energy bars, and expanding use in bakery, dairy, and confectionery formulations. Manufacturers are innovating with dark chocolate, reduced-sugar coatings, and functional inclusions to meet evolving consumer preferences for indulgence combined with nutrition.

Key Market Insights

- Chocolate-coated nuts dominate the product landscape, accounting for nearly 32% of the 2025 market share due to strong retail penetration and premium positioning.

- B2B industrial demand represents approximately 60% of total revenue, driven by bakery, confectionery, and snack bar manufacturers.

- Europe holds the largest regional share at around 30%, supported by strong confectionery exports and advanced chocolate processing capabilities.

- Asia-Pacific is the fastest-growing region, expanding at over 8% CAGR due to rising disposable income and westernized snacking habits.

- Dark chocolate and reduced-sugar variants are gaining traction, reflecting growing health-conscious consumption trends.

- Technological advancements in enrobing and high-melt coatings are enabling expansion into tropical and emerging markets.

What are the latest trends in the chocolate-coated inclusions market?

Functional and Protein-Enriched Inclusions

One of the most prominent trends in the chocolate-coated inclusions market is the integration of functional ingredients such as plant proteins, fiber, probiotics, and adaptogens. With the global protein snack segment expanding steadily, coated protein crispies and energy bites are increasingly incorporated into bars, breakfast cereals, and meal-replacement products. Consumers are seeking indulgent formats that also deliver nutritional benefits, encouraging manufacturers to develop hybrid offerings that balance taste and functionality. High-protein, keto-friendly, and low-glycemic coatings are gaining visibility in North America and Europe, particularly among fitness-focused demographics.

Premiumization and Clean-Label Formulations

Premium chocolate-coated inclusions featuring single-origin cocoa, organic certifications, and ethically sourced ingredients are expanding rapidly. Clean-label formulations with reduced artificial additives and transparent sourcing are influencing purchasing decisions, especially in developed markets. Sustainability certifications such as Fairtrade and Rainforest Alliance are becoming important differentiators. Additionally, manufacturers are experimenting with exotic fruit centers, flavored dark chocolate coatings, and artisan-style inclusions to capture premium retail segments.

What are the key drivers in the chocolate-coated inclusions market?

Growth of the Global Confectionery and Snack Bar Industry

The global confectionery industry, valued at over USD 220 billion, continues to grow steadily, providing strong demand for chocolate-coated inclusions as a core ingredient. Snack and energy bars, growing at approximately 7–8% CAGR globally, are major consumption drivers. These sectors rely heavily on coated nuts, crispies, and fruit inclusions for texture, taste differentiation, and value addition.

Rising Consumer Preference for Premium Snacking

Consumers are shifting from traditional sugar confectionery toward premium, texture-rich snacks that combine indulgence with perceived health benefits. Chocolate-coated almonds, cranberries, and seeds align with this trend by offering antioxidant appeal and protein content. The demand for dark chocolate variants, perceived as healthier, is accelerating growth in premium product segments.

What are the restraints for the global market?

Cocoa Price Volatility

Fluctuations in cocoa prices, particularly due to supply disruptions in West Africa, significantly affect production costs and profit margins. Raw material price instability can compress manufacturer margins and lead to periodic price adjustments across the supply chain.

Temperature Sensitivity and Shelf-Life Constraints

Chocolate coatings are susceptible to bloom and melting in high-temperature environments, limiting distribution flexibility in tropical markets without adequate cold-chain infrastructure. This raises logistical costs and can affect product quality.

What are the key opportunities in the chocolate-coated inclusions industry?

Emerging Market Expansion

Rapid urbanization and organized retail expansion in India, China, Brazil, and Southeast Asia present strong growth opportunities. Localized flavor innovation and affordable premium positioning can help manufacturers tap into rising middle-class consumption. Asia-Pacific is projected to grow at over 8% CAGR, offering significant incremental revenue potential.

Customized B2B Ingredient Solutions

Food manufacturers increasingly demand customized inclusions with specific size, coating thickness, and heat resistance. Suppliers investing in advanced enrobing technologies and co-development partnerships with bakery and dairy brands can secure long-term industrial contracts and stable revenue streams.

Product Type Insights

Chocolate-coated nuts lead the global market, contributing approximately 32% of total revenue in 2025. The dominance of this segment is primarily driven by strong consumer preference for premium snacking options that combine indulgence with perceived nutritional benefits. Almond-coated variants hold the largest share within this category, supported by their premium positioning, high protein content, and strong retail demand across supermarkets and specialty gourmet outlets. Increasing adoption of dark chocolate coatings and flavored variants such as sea salt and caramel further enhances product differentiation and repeat purchases.

Chocolate-coated dried fruits represent a steadily expanding segment, fueled by growing consumer inclination toward antioxidant-rich and better-for-you indulgent snacks. The combination of fruits such as raisins, cranberries, and blueberries with dark chocolate appeals to health-conscious consumers seeking balance between taste and nutrition. Rising awareness regarding functional ingredients and clean-label positioning is accelerating growth in this segment across developed markets.

Cereal and biscuit inclusions are widely utilized in snack bars, breakfast cereals, and hybrid confectionery products, benefiting from demand for texture-enhancing ingredients in value-added food formulations. However, chocolate-coated protein and functional inclusions are emerging as the fastest-growing sub-segment, supported by expanding fitness trends, increasing sports nutrition consumption, and the mainstreaming of high-protein diets. The integration of whey protein crisps, plant-based protein clusters, and fortified inclusions into chocolates and snack bars is significantly contributing to segment expansion.

Application Insights

Confectionery and candy applications account for nearly 35% of total market share, maintaining leadership due to the integral role of coated inclusions in chocolate dragees, specialty sweets, and premium boxed assortments. Continuous innovation in flavor combinations, layered textures, and seasonal offerings supports segment growth. Rising consumer spending on premium and artisanal confectionery further reinforces demand in this category.

Bakery products represent a substantial share of the market, driven by increasing incorporation of chocolate-coated nuts, fruits, and cereals into cookies, muffins, brownies, and premium pastries. The leading growth driver in this segment is the rising demand for premiumization in baked goods, as manufacturers seek to differentiate offerings through enhanced texture and flavor complexity. In-store bakeries and café chains are increasingly utilizing coated inclusions to elevate product appeal and pricing power.

Dairy and frozen desserts are witnessing increasing usage of coated inclusions, particularly in premium ice cream toppings, mix-ins, and yogurt parfaits. The growth of indulgent dessert formats and limited-edition flavors is stimulating demand from dairy processors. Snack and energy bars form one of the fastest-growing application areas, benefiting from rising protein consumption trends, on-the-go lifestyles, and expanding availability of fortified snack formats across retail and online platforms.

Distribution Channel Insights

B2B sales dominate the market with approximately 60% revenue share, primarily driven by long-term supply agreements with global bakery, dairy, and confectionery manufacturers. Large-scale food processors rely on consistent quality, customized formulations, and bulk supply capabilities, which strengthens supplier relationships and stabilizes revenue streams. Growing private-label production by major retailers further supports B2B demand.

Retail distribution through supermarkets and hypermarkets forms the primary B2C channel, supported by strong shelf visibility, promotional strategies, and impulse purchasing behavior. Online retail is expanding steadily due to the rapid growth of direct-to-consumer snack brands and subscription-based premium confectionery models. Specialty gourmet stores are increasingly featuring premium coated nut and fruit products, capitalizing on consumer interest in artisanal, organic, and imported offerings.

Nature Insights

Conventional chocolate-coated inclusions account for nearly 78% of total market revenue, owing to cost efficiency, wide availability of raw materials, and established manufacturing infrastructure. These products remain highly accessible across both mass-market and premium categories.

However, organic and vegan variants are expanding at a notable pace, particularly in Europe and North America, where consumers increasingly prioritize sustainability, clean-label ingredients, and plant-based diets. The leading growth driver for this segment is rising demand for ethically sourced cocoa, non-dairy chocolate alternatives, and certified organic nuts and fruits. Manufacturers are investing in transparent supply chains and sustainability certifications to capture environmentally conscious consumers.

| By Product Type | By Chocolate Type | By Application | By Distribution Channel | By Nature |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 28% of the global market share in 2025, led by the United States, which accounts for nearly three-quarters of regional demand. Growth in the region is primarily driven by strong snack bar consumption, high per capita chocolate intake, and continuous innovation in protein-enriched and functional confectionery products. The expanding sports nutrition industry and demand for clean-label snacks further stimulate product development. Canada contributes steadily through rising demand for organic, premium, and ethically sourced variants, supported by growing health awareness and specialty retail expansion.

Europe

Europe dominates the global market with around 30% share in 2025, supported by its well-established chocolate manufacturing heritage and advanced processing capabilities. Germany, Belgium, Switzerland, and the UK serve as major production and export hubs, with Germany accounting for roughly 20% of European demand. Regional growth is driven by strong consumer preference for premium chocolate products, increasing demand for organic and fair-trade certifications, and extensive export networks supplying global confectionery markets. Innovation in artisanal and high-cocoa-content products further strengthens Europe’s leadership position.

Asia-Pacific

Asia-Pacific represents the fastest-growing region, projected to expand at over 8% CAGR during the forecast period. China, India, Japan, and South Korea are major demand centers, supported by rapid urbanization, rising disposable incomes, and expanding modern retail infrastructure. Increasing westernization of dietary habits and growing popularity of chocolate-based snacks are key growth drivers. India is emerging as one of the fastest-growing national markets due to its expanding middle-class population, strengthening food processing infrastructure, and rising demand for premium and protein-fortified snacks. Regional manufacturers are also investing in capacity expansion to meet domestic and export demand.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico. Expansion of domestic confectionery manufacturing, increasing premium snack consumption among urban populations, and rising supermarket penetration are key growth drivers. Growing youth demographics and strong cultural preference for chocolate-based sweets further contribute to sustained regional demand.

Middle East & Africa

The Middle East & Africa region demonstrates gradual expansion, with the UAE and Saudi Arabia acting as key import-driven markets supported by strong demand for premium confectionery and gifting products. High per capita income levels and expanding modern retail channels contribute to market growth in the Gulf Cooperation Council countries. South Africa remains a major regional production hub, benefiting from established food processing infrastructure and growing domestic consumption. Increasing urbanization and rising exposure to international brands are further supporting market development across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Chocolate-Coated Inclusions Market

- Barry Callebaut AG

- Cargill Incorporated

- Olam Food Ingredients

- Puratos Group

- Fuji Oil Holdings Inc.

- Blommer Chocolate Company

- Clasen Quality Chocolate

- Guittard Chocolate Company

- Irca Group

- AAK AB

- Dawn Foods

- Mantrose-Haeuser Co. Inc.

- Kanegrade Ltd.

- Orchard Valley Foods

- Pecan Deluxe Candy Company