China Pizza Vending Machine Market Size

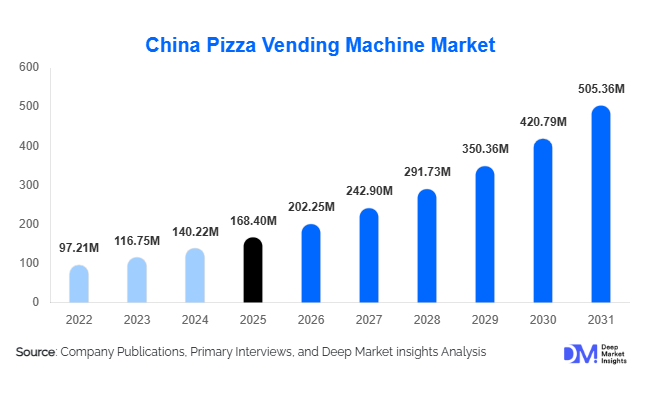

According to Deep Market Insights, the global China pizza vending machine market size was valued at USD 168.4 million in 2025 and is projected to grow from USD 202.25 million in 2026 to reach USD 505.36 million by 2031, expanding at a CAGR of 20.1% during the forecast period (2026–2031). Market growth is primarily driven by rising adoption of unattended retail solutions, increasing labor costs in the foodservice industry, and growing consumer demand for convenient, contactless, and 24/7 food access. Rapid urbanization, strong penetration of digital payment ecosystems, and advancements in robotic cooking technologies are further accelerating deployment across transportation hubs, commercial complexes, and institutional environments globally.

Key Market Insights

- Automation in foodservice is reshaping quick-service dining, with pizza vending machines emerging as scalable micro-restaurant solutions.

- China leads global manufacturing and deployment due to strong robotics ecosystems and widespread mobile payment adoption.

- Transportation hubs represent the largest installation segment, benefiting from high passenger footfall and round-the-clock demand.

- AI-enabled vending machines are gaining traction, improving predictive maintenance, inventory management, and customer personalization.

- Asia-Pacific dominates global demand, while Europe and North America are rapidly adopting automated food retail concepts.

- Franchise and revenue-sharing deployment models are accelerating international expansion with reduced operator CapEx.

What are the latest trends in the China pizza vending machine market?

Rise of AI-Powered Smart Vending Ecosystems

Pizza vending machines are evolving into intelligent automated kitchens powered by artificial intelligence and cloud analytics. Operators increasingly deploy machines capable of monitoring ingredient freshness, predicting peak demand periods, and optimizing cooking performance remotely. AI-driven recommendation systems personalize menu offerings based on purchasing behavior, improving conversion rates and repeat usage. Cloud connectivity allows centralized fleet management across cities, enabling operators to scale operations efficiently while minimizing downtime. Integration with mobile apps also allows customers to pre-order pizzas, further blending vending technology with digital foodservice platforms.

Shift Toward Freshly Prepared Automated Food

Consumer preferences are shifting away from traditional snack vending toward freshly prepared meals. Modern pizza vending machines now incorporate robotic dough preparation, automated topping systems, and high-speed ovens capable of delivering restaurant-quality pizzas within minutes. This shift enhances perceived food quality and supports premium pricing models. Fresh preparation technology also enables menu customization, dietary personalization, and regional flavor adaptation, increasing appeal among urban consumers seeking convenience without compromising food experience.

What are the key drivers in the China pizza vending machine market?

Rising Labor Costs and Workforce Constraints

Global foodservice operators face rising wage pressures and staffing shortages, making automation an attractive alternative. Pizza vending machines significantly reduce operational labor requirements while enabling 24-hour service availability. This improves profit margins and operational scalability, especially in high-rent urban environments where traditional restaurant formats face cost pressures.

Expansion of Digital Payment Infrastructure

The widespread adoption of QR-based and contactless payment systems has transformed vending machine usability. Seamless payment integration through mobile wallets increases transaction speed and impulse purchases while improving customer convenience. Regions with strong digital payment ecosystems demonstrate faster adoption rates due to reduced friction in automated retail transactions.

What are the restraints for the global market?

High Initial Equipment Investment

Advanced pizza vending machines require substantial upfront investment, typically ranging between USD 25,000 and USD 60,000 per unit. Smaller operators often face financing challenges, slowing early-stage adoption in developing markets. Profitability depends heavily on installation location and consistent daily sales volumes.

Operational Maintenance and Supply Chain Complexity

Maintaining consistent food quality requires efficient ingredient supply chains and regular machine servicing. Fresh ingredient logistics, refrigeration systems, and technical maintenance add operational complexity compared to conventional vending machines. Equipment downtime or inconsistent maintenance can negatively affect consumer trust and brand perception.

What are the key opportunities in the China pizza vending machine industry?

Expansion Across Smart Cities and Transportation Infrastructure

Urban infrastructure modernization provides significant deployment opportunities. Governments investing in smart city ecosystems increasingly support automated retail solutions that reduce staffing requirements while improving public service accessibility. Metro stations, airports, and high-speed rail networks offer consistent demand environments where automated food solutions can operate efficiently with minimal operational overhead.

Integration with Franchise and SaaS Business Models

The shift toward franchise-based deployment and software-enabled revenue models presents strong growth potential. Vendors are transitioning from hardware-only sales toward subscription-based services that include analytics platforms, maintenance contracts, and ingredient supply partnerships. This recurring revenue structure enhances profitability while lowering barriers for new entrants seeking scalable business models.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 168.40 Million |

| Market Size in 2026 | USD 202.25 Million |

| Market Size in 2031 | USD 505.36 Million |

| CAGR | 20.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Machine Type Insights

The global pizza vending machine market is primarily led by fully automated pizza vending machines, which account for nearly 58% of total deployments worldwide. The dominance of this segment is largely attributed to its strong operational efficiency, reduced dependency on labor, and ability to deliver standardized product quality across diverse locations. Fully automated systems integrate robotic dough handling, ingredient dispensing, baking, and final delivery processes within a compact enclosed unit, enabling operators to maintain consistent output while minimizing operational complexity. The growing shortage of skilled foodservice labor and rising wage pressures across developed and emerging economies have significantly accelerated the transition toward fully autonomous solutions. Additionally, advancements in robotics, sensor-based cooking precision, and real-time monitoring technologies have improved reliability, making fully automated machines increasingly attractive for large-scale deployments.Semi-automated pizza vending machines continue to maintain relevance among mid-sized operators and regional franchise owners seeking a balance between automation and investment cost. These systems typically combine automated baking functions with partially manual ingredient preparation, allowing flexibility in menu customization while lowering capital expenditure requirements. Meanwhile, frozen pizza dispensing machines remain operationally viable in low-footfall environments such as industrial zones, rural transit stops, and secondary commercial areas where demand variability requires simplified and cost-efficient machine formats. However, the broader market trend is shifting toward freshly prepared offerings as consumer expectations increasingly favor hot, restaurant-quality meals delivered instantly, reinforcing the long-term growth trajectory of fully automated machine types.

Technology Insights

Hybrid smart cooking systems represent the fastest-growing technological category within the market, capturing approximately 34% market share as operators seek an optimal balance between food freshness and operational efficiency. These systems utilize partially prepared ingredients combined with automated cooking technologies, enabling faster preparation cycles while maintaining product consistency and taste quality comparable to quick-service restaurants. The leading growth driver for this segment is the rising consumer demand for freshly cooked meals without extended wait times, alongside operator requirements for scalable and repeatable production models.Technological innovation is increasingly centered on artificial intelligence and connected device ecosystems. AI-enabled diagnostics allow machines to perform predictive maintenance, identify component wear, and reduce downtime through automated alerts. Cloud-connected platforms provide centralized dashboards where operators can track performance metrics, monitor ingredient consumption, adjust pricing dynamically, and analyze purchasing behavior across multiple locations. The integration of cashless payment technologies, mobile app ordering, and loyalty program synchronization further enhances customer engagement while supporting data-driven decision-making. As smart retail infrastructure expands globally, technology providers are prioritizing modular software architectures that enable remote upgrades, menu personalization, and operational optimization, transforming pizza vending machines into intelligent autonomous foodservice units rather than traditional vending equipment.

Installation Location Insights

Transportation hubs remain the leading installation locations, accounting for roughly 26% of global deployments due to their ability to generate continuous and predictable customer traffic throughout the day. Airports, railway stations, metro terminals, and intercity transit centers provide ideal operating environments where travelers seek convenient, quick meal options during waiting periods. The primary driver behind this segment’s leadership is the combination of high passenger volumes and limited access to affordable freshly prepared food during non-peak restaurant hours, enabling vending machines to operate as complementary foodservice solutions.Commercial complexes and shopping malls follow closely as major deployment environments, supported by impulse purchasing behavior and extended visitor dwell times associated with entertainment and retail activities. Pizza vending machines enhance food court capacity without requiring additional staffing or kitchen space, allowing property owners to diversify food offerings efficiently. Educational institutions and corporate campuses are emerging as some of the fastest-growing installation segments, primarily driven by demand for late-night food accessibility, flexible dining options, and extended operational availability beyond cafeteria schedules. Universities, technology parks, and large office environments increasingly view automated foodservice solutions as cost-effective methods to provide round-the-clock meal access while reducing operational overhead.

End-Use Insights

Smart retail and unattended commerce collectively account for approximately 31% of global market demand, representing the leading end-use segment. The expansion of cashier-less retail models and autonomous convenience formats has accelerated adoption, as operators seek scalable solutions capable of operating continuously without on-site staff. Pizza vending machines align strongly with this transition by enabling foodservice integration within automated retail ecosystems, creating new revenue channels while reducing operational complexity. The primary growth driver for this segment is the rapid global shift toward frictionless consumer experiences supported by digital payments, remote monitoring, and data-driven retail management.Quick-service retail operators are increasingly leveraging pizza vending machines as low-risk expansion tools to test new geographic markets without investing in full restaurant infrastructure. This approach enables brand visibility in high-traffic locations while maintaining controlled operational costs. Institutional environments-including hospitals, universities, and public facilities-are witnessing accelerated adoption due to the growing need for 24/7 food availability for staff, students, and visitors. Additionally, export-oriented deployments are expanding rapidly as Chinese manufacturers scale international distribution networks, supplying machines across Europe, the Middle East, and Southeast Asia. This trend reflects the broader globalization of robotic foodservice technologies and increasing acceptance of automated dining experiences among diverse consumer groups.

Explore more data points, trends and opportunities Download Free Sample Report

China Pizza Vending Machine Market Segmentations

By Machine Type

- Fully Automated Pizza Vending Machines

- Semi-Automated Pizza Vending Machines

- Frozen Pizza Dispensing Machines

- Hybrid Smart Cooking Pizza Machines

By Technology

- AI-Enabled Smart Vending Systems

- Cloud-Connected Remote Monitoring Machines

- Robotic Cooking & Baking Systems

- Touchless & Digital Payment Integrated Machines

By Installation Location

- Transportation Hubs

- Shopping Malls & Commercial Complexes

- Corporate Offices & Business Parks

- Educational Institutions & Universities

- Hospitals & Healthcare Facilities

- Entertainment & Leisure Venues

By End Use

- Smart Retail & Unattended Commerce Operators

- Quick Service Restaurant (QSR) Extensions

- Institutional Foodservice

- Franchise & Independent Operators

By Distribution Model

- Direct Sales

- Leasing & Revenue Sharing Model

- Franchise Deployment

- Operator Managed Networks

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global pizza vending machine market, accounting for approximately 52% of total market share in 2025, supported by strong adoption across China, Japan, and South Korea. China alone contributes nearly 38% of global demand, driven by a deeply established vending culture, widespread adoption of mobile payment ecosystems, and strong government support for smart retail and automated commerce initiatives. Rapid urbanization across major metropolitan regions has increased demand for compact foodservice solutions capable of operating in dense urban environments where traditional restaurant expansion faces spatial and labor constraints. Japan and South Korea contribute significantly through advanced consumer acceptance of robotics and automation technologies, alongside high expectations for convenience-driven dining formats.Regional growth is further supported by expanding digital infrastructure, increasing penetration of AI-enabled retail technologies, and strong manufacturing capabilities that reduce production costs. Southeast Asia is emerging as the fastest-growing subregion due to rising middle-class consumption, modernization of retail ecosystems, and increasing investment in smart city development across countries such as Singapore, Thailand, and Indonesia. The combination of technological readiness, urban density, and evolving consumer lifestyles positions Asia-Pacific as both the largest production hub and the most dynamic demand center for pizza vending machines.

Europe

Europe holds approximately 22% market share, supported by widespread adoption across Italy, France, Germany, and the United Kingdom. One of the primary regional growth drivers is persistently high labor costs within the foodservice sector, which encourage operators to adopt automated solutions that maintain service availability while reducing staffing expenses. European consumers demonstrate strong acceptance of premium automated food concepts, particularly those emphasizing freshness, authenticity, and gourmet customization.The region is witnessing growing deployment of high-end pizza vending machines offering artisanal ingredients, customizable toppings, and restaurant-quality preparation processes. Urbanization trends and increasing demand for late-night dining options further support installations in metropolitan areas, transportation corridors, and tourism-heavy destinations. Sustainability initiatives also influence regional adoption, as newer machines incorporate energy-efficient ovens and waste reduction technologies aligned with European environmental regulations.

North America

North America accounts for approximately 15% of global market share, with the United States leading installations across universities, office complexes, retail centers, and mixed-use developments. Regional growth is primarily driven by ongoing automation trends within the quick-service restaurant industry, where operators seek solutions that improve operational efficiency while addressing rising labor shortages and wage inflation. Pizza vending machines provide an attractive extension strategy for food brands seeking scalable distribution without traditional restaurant investments.Consumer familiarity with self-service kiosks, mobile ordering platforms, and cashless payments further accelerates adoption. Additionally, growing demand for convenience-oriented meal solutions among urban professionals and students supports increased deployment in nontraditional foodservice locations. Technological partnerships between vending manufacturers and digital payment providers are enhancing user experience, contributing to steady market expansion across the region.

Latin America

Latin America represents approximately 5% of global demand, led by Brazil and Mexico, where adoption is gradually increasing alongside modernization of urban retail infrastructure. Regional growth is supported by expanding shopping mall developments, increasing smartphone penetration, and growing exposure to automated retail concepts. Rising urban population density and evolving consumer lifestyles are creating opportunities for compact, cost-efficient foodservice models capable of operating in high-traffic public environments.Although adoption remains at an early stage compared to developed regions, improving digital payment ecosystems and growing entrepreneurial interest in unattended retail formats are expected to accelerate deployments. Local operators are increasingly viewing pizza vending machines as affordable entry points into the foodservice industry, particularly in metropolitan areas where traditional restaurant setup costs remain high.

Middle East & Africa

The Middle East and Africa collectively account for nearly 6% of global market share, with the United Arab Emirates and Saudi Arabia emerging as key high-growth markets. Regional expansion is strongly driven by large-scale smart infrastructure investments, smart city initiatives, and tourism-focused economic diversification strategies. High footfall in airports, shopping destinations, and entertainment districts creates favorable conditions for automated dining solutions capable of operating continuously in premium locations.In Gulf Cooperation Council countries, strong consumer purchasing power and openness toward innovative technologies support rapid adoption of robotic foodservice concepts. Meanwhile, selected African urban centers are beginning to adopt vending-based food solutions as retail modernization progresses. Increasing investment in digital payments, hospitality infrastructure, and urban mobility networks is expected to gradually strengthen regional demand, positioning the Middle East and Africa as an emerging opportunity market over the long term.

Key Players in the China Pizza Vending Machine Market

- Paline (Let's Pizza)

- PizzaForno

- Basil Street

- API Tech

- Vending Robotics

- Smart Pizza France

- A1 Concepts

- Piestro

- Wonder Pizza

- VendCafe

- RoboPizza

- XY Vending Technology

- TCN Vending Machine Co.

- Fuhan Intelligent Equipment

- Guangzhou Micron Smart Technology