Children’s Sunscreen Market Size

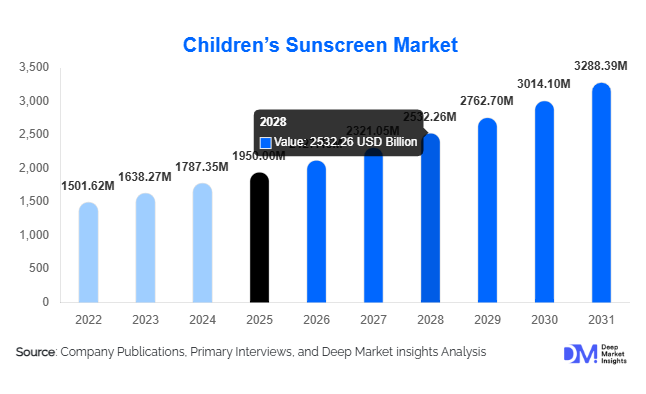

According to Deep Market Insights, the global children’s sunscreen market size was valued at USD 1,950 million in 2025 and is projected to grow from USD 2,127.45 million in 2026 to reach USD 3,288.39 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The market growth is primarily driven by rising awareness regarding pediatric skin protection, increasing incidence of UV-related skin conditions, and growing parental preference for safe, dermatologically tested sun care products.

Key Market Insights

- Mineral-based sunscreens are gaining strong traction due to increasing concerns over chemical ingredients and regulatory restrictions.

- Offline retail channels, particularly pharmacies and specialty baby stores, dominate the market due to higher consumer trust.

- North America leads the global market, supported by strong awareness and regulatory frameworks promoting sun safety.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and expanding pediatric skincare awareness.

- SPF 30–50 products account for the largest share, offering optimal protection and affordability for daily use.

- E-commerce platforms are rapidly expanding, improving accessibility and boosting sales in emerging markets.

What are the latest trends in the children’s sunscreen market?

Shift Toward Clean Label and Organic Formulations

Parents are increasingly opting for sunscreens that are free from harmful chemicals such as oxybenzone and parabens. This has accelerated demand for mineral-based and organic products that are perceived as safer for children’s sensitive skin. Brands are investing in reef-safe, biodegradable, and hypoallergenic formulations, aligning with global sustainability trends. Certifications such as dermatologically tested and pediatrician-approved labels are becoming key differentiators in product positioning.

Innovation in Product Formats and Application Methods

Manufacturers are introducing innovative formats such as spray sunscreens, sticks, and roll-ons to improve ease of application for children. Water-resistant and sweat-proof formulations are gaining popularity, especially for outdoor activities and sports. Smart packaging innovations, including travel-friendly sizes and UV-sensitive indicators, are enhancing consumer convenience and engagement. These advancements are particularly appealing to busy parents seeking quick and effective application solutions.

What are the key drivers in the children’s sunscreen market?

Increasing Awareness of UV Protection in Early Childhood

Growing awareness regarding the harmful effects of UV radiation on children’s skin is a major driver. Healthcare professionals and dermatologists are increasingly recommending early adoption of sun protection habits, leading to higher demand for specialized children’s sunscreens. Public health campaigns in developed regions have further reinforced the importance of daily sun protection.

Growth in the Pediatric Skincare Industry

The expanding pediatric skincare market is positively influencing sunscreen demand. Parents are increasingly investing in specialized skincare products tailored for children, including sunscreens formulated for sensitive and allergy-prone skin. This trend is supported by rising disposable incomes and a greater focus on child health and wellness.

What are the restraints for the global market?

High Cost of Premium Products

Mineral and organic sunscreens are relatively expensive compared to conventional products, limiting their adoption in price-sensitive markets. This pricing gap is particularly evident in developing economies, where affordability remains a key concern for consumers.

Seasonal Demand Fluctuations

The market experiences strong seasonality, with peak demand during the summer months and reduced consumption during the winter. This variability affects production planning and revenue stability for manufacturers, particularly in regions with temperate climates.

What are the key opportunities in the children’s sunscreen industry?

Expansion in Emerging Markets

Countries in the Asia-Pacific and Latin America present significant growth opportunities due to increasing awareness of skincare and rising disposable incomes. Markets such as India, China, and Brazil are witnessing growing demand for children’s sunscreen products, supported by urbanization and improved access to retail channels.

Development of Multifunctional Products

There is increasing demand for multifunctional sunscreens that offer additional benefits such as moisturizing, anti-pollution protection, and insect repellency. Companies investing in such innovations can capture a broader consumer base and enhance product value propositions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1950 Million |

| Market Size in 2026 | USD 2127.45 Million |

| Market Size in 2031 | USD 3288.39 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Mineral sunscreens dominate the children’s sunscreen market, accounting for approximately 52% of the global market share in 2025. This leadership is primarily driven by increasing parental preference for non-toxic, skin-safe formulations, especially for infants and children with sensitive or allergy-prone skin. Mineral ingredients such as zinc oxide and titanium dioxide provide broad-spectrum protection without penetrating the skin, making them highly recommended by dermatologists. Additionally, tightening global regulations restricting the use of certain chemical UV filters have accelerated the shift toward mineral-based products. Chemical sunscreens continue to hold a notable share due to their lower cost and lightweight texture, making them suitable for mass-market consumption. Meanwhile, hybrid formulations are gaining traction as they offer a balance between safety, affordability, and enhanced UV protection, appealing to consumers seeking performance without compromising on safety standards.

SPF Level Insights

SPF 30–50 products lead the market with around 46% share, as they provide an optimal balance between effective UV protection and affordability, making them the most commonly recommended range by healthcare professionals. This segment benefits from strong consumer trust and widespread availability across retail channels. Higher SPF categories (SPF 50 and above) are witnessing increasing demand, particularly in regions with intense UV radiation such as Australia, the U.S., and parts of Asia-Pacific, where prolonged outdoor exposure necessitates stronger protection. Conversely, lower SPF products (below SPF 30) are gradually declining in popularity due to growing awareness of inadequate protection levels, especially for children’s delicate skin. The trend indicates a clear shift toward higher efficacy and preventive healthcare-focused purchasing behavior.

Formulation Type Insights

Lotions account for approximately 38% of the market share, driven by their ease of application, uniform coverage, and widespread consumer familiarity. Their versatility across different skin types and climates makes them the preferred choice among parents. Cream-based formulations continue to perform well, particularly for children with dry or sensitive skin, as they offer added moisturizing benefits. Meanwhile, sprays and sticks are emerging as high-growth segments due to their convenience, portability, and suitability for active lifestyles, including outdoor sports and travel. These formats are increasingly favored for quick reapplication, especially in school and recreational settings, supporting their rising adoption globally.

Distribution Channel Insights

Offline retail dominates the market with nearly 63% market share, particularly through pharmacies, drugstores, and specialty baby care outlets. This dominance is driven by consumer preference for trusted purchase points where professional recommendations and product authenticity are assured. Pharmacist and pediatrician endorsements play a crucial role in influencing purchasing decisions. However, online retail channels are expanding rapidly, supported by increasing digital penetration, convenience, and availability of a wider product range. E-commerce platforms are also enabling access to premium and international brands in emerging markets, contributing to faster growth in this segment. Subscription-based models and direct-to-consumer (D2C) strategies are further strengthening online channel expansion.

Age Group Insights

Children aged 6–12 years represent the largest segment, contributing approximately 41% of the market share, primarily due to higher outdoor activity levels, including school, sports, and recreational exposure. This age group requires frequent sunscreen application, driving consistent product usage. Additionally, increasing awareness among parents and schools regarding sun safety practices is supporting demand. The infant segment (0–2 years) is also witnessing notable growth, fueled by heightened safety concerns and increasing availability of ultra-gentle, pediatrician-approved formulations specifically designed for delicate skin. This trend reflects a broader shift toward preventive skincare from an early age.

End-Use Insights

Household consumption accounts for over 85% of total demand, as parents remain the primary purchasers and decision-makers in the children’s sunscreen market. Increasing awareness of long-term skin health and preventive care is driving regular usage across households. Institutional demand is gradually rising, particularly from schools, daycare centers, summer camps, and recreational facilities, especially in developed regions where sun safety regulations are being implemented. The global childcare industry, valued at over USD 250 billion and growing steadily, is indirectly supporting sunscreen demand. Additionally, export-driven demand is increasing, with major production hubs in Europe and Asia supplying high-quality products to North America and other developed markets, further strengthening global trade dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

Children’s Sunscreen Market Segmentations

By Product Type

- Mineral (Physical) Sunscreens

- Chemical Sunscreens

- Hybrid Sunscreens

By SPF Level

- SPF 15–30

- SPF 30–50

- SPF 50–70

- SPF 70+

By Formulation Type

- Creams

- Lotions

- Sprays

- Sticks/Roll-ons

- Gels

By Age Group

- Infants

- Toddlers

- Children

By Distribution Channel

- Offline Retail

- Online Retail

Regional Insights

North America

North America holds approximately 34% of the global market share, with the United States being the dominant contributor. Market growth in this region is driven by high awareness regarding skin cancer prevention, strong recommendations from dermatological associations, and well-established regulatory frameworks ensuring product safety. The presence of leading global brands and continuous product innovation further supports market expansion. Additionally, high disposable income and widespread adoption of premium pediatric skincare products contribute to sustained demand. Increasing participation in outdoor recreational activities among children also drives consistent sunscreen usage.

Europe

Europe accounts for around 27% of the market share, with key markets including Germany, France, and the UK. Growth in this region is strongly influenced by stringent regulations on chemical sunscreen ingredients, which are encouraging a shift toward mineral and organic formulations. Consumer preference for eco-friendly and sustainable products is particularly high, supporting demand for reef-safe and biodegradable sunscreens. Government-led awareness campaigns on UV protection and strong healthcare systems promoting preventive care further drive market growth. Additionally, the region’s well-developed retail infrastructure ensures wide product accessibility.

Asia-Pacific

Asia-Pacific is the fastest-growing region, registering a CAGR of approximately 11%. Rapid urbanization, rising disposable incomes, and increasing awareness of skincare and child health are key growth drivers. China and India are leading markets due to their large population base and expanding middle class, while Japan and South Korea contribute through innovation in advanced formulations and premium product offerings. The growing influence of social media and beauty trends is also accelerating product adoption. Furthermore, increasing penetration of e-commerce platforms is significantly improving accessibility in both urban and semi-urban areas.

Latin America

Latin America accounts for nearly 6% of the global market, with Brazil and Mexico as major contributors. The region’s tropical climate and high UV exposure levels create a natural demand for sun protection products. Growing consumer awareness regarding skin health, coupled with rising middle-class income levels, is supporting market growth. Government initiatives promoting healthcare awareness and increasing the availability of affordable sunscreen products are further driving adoption. Additionally, the expansion of retail networks and international brand presence is strengthening market penetration.

Middle East & Africa

The Middle East & Africa region holds around 5% of the market share, driven primarily by extreme climatic conditions and high UV radiation levels. Countries such as the UAE and South Africa are key markets, supported by increasing consumer awareness and growing demand for premium skincare products. Rising expatriate populations and higher disposable incomes in Gulf countries are also contributing to market growth. In Africa, improving access to healthcare products and increasing urbanization are gradually expanding demand. However, affordability challenges remain a constraint in certain parts of the region, limiting widespread adoption.

Key Players in the Children’s Sunscreen Market

- Johnson & Johnson

- Beiersdorf AG

- L’Oréal Group

- Procter & Gamble

- Unilever

- Edgewell Personal Care

- Pierre Fabre Group

- Mustela (Laboratoires Expanscience)

- California Baby

- Thinkbaby

- Babyganics

- Himalaya Wellness

- Chicco

- Sebapharma

- Sun Bum