Cherry Acerola Powder Market Size

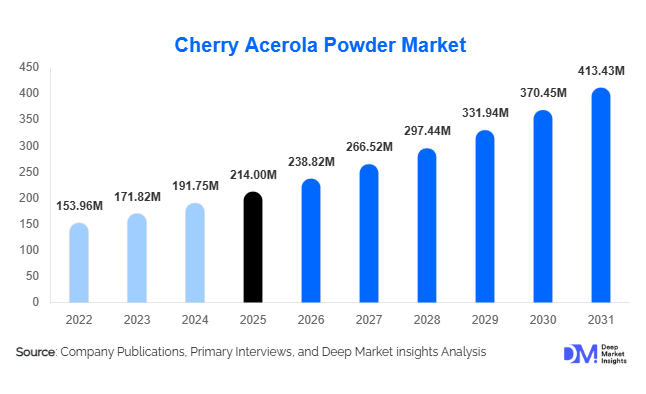

According to Deep Market Insights,the global cherry acerola powder market size was valued at USD 214 million in 2025 and is projected to grow from USD 238.82 million in 2026 to reach USD 413.43 million by 2031, expanding at a CAGR of 11.6% during the forecast period (2026–2031). Market growth is primarily driven by rising demand for natural vitamin C ingredients, increasing adoption of clean-label food formulations, and expanding applications across nutraceuticals, functional beverages, and natural cosmetics. The transition toward preventive healthcare and plant-based nutrition is accelerating the adoption of acerola-derived ingredients as manufacturers increasingly replace synthetic ascorbic acid with botanical alternatives.

Key Market Insights

- Natural vitamin C demand is accelerating globally, as consumers increasingly prefer plant-derived immunity-support ingredients over synthetic additives.

- Nutraceutical applications dominate demand, supported by strong growth in dietary supplements, gummies, and powdered wellness formulations.

- North America leads global consumption, driven by mature supplement markets and clean-label product innovation.

- Asia-Pacific is the fastest-growing region, supported by expanding supplement manufacturing in India and China.

- Organic-certified acerola powder is gaining premium positioning, enabling higher margins for suppliers and processors.

- Advanced drying technologies, including freeze-drying and microencapsulation, are improving nutrient stability and product functionality.

What are the latest trends in the cherry acerola powder market?

Shift Toward Clean-Label Functional Ingredients

Food and beverage manufacturers are increasingly reformulating products using natural ingredients to meet clean-label standards. Cherry acerola powder is widely used as a natural antioxidant and vitamin C fortification ingredient, allowing brands to eliminate synthetic preservatives while maintaining product shelf life. Clean-label positioning has become particularly important in beverages, dairy alternatives, and fortified snacks, where ingredient transparency directly influences purchasing decisions. Regulatory alignment favoring botanical additives in Europe and North America is further accelerating this transition, encouraging long-term adoption across large-scale food manufacturing operations.

Expansion of Functional Beverage Applications

Functional beverages represent one of the fastest-growing applications for acerola powder. Immunity shots, plant-based smoothies, hydration drinks, and sports nutrition beverages increasingly incorporate acerola as both a nutritional enhancer and natural stabilizer. Beverage startups and premium wellness brands are leveraging acerola powder’s high antioxidant profile to differentiate products in crowded markets. Technological improvements in solubility and flavor masking are enabling broader use across ready-to-drink formulations, while consumer demand for convenient health solutions continues to drive innovation in this category.

What are the key drivers in the cherry acerola powder market?

Rising Preventive Healthcare Awareness

Consumers worldwide are prioritizing immune health and preventive nutrition, significantly increasing demand for natural vitamin C sources. Cherry acerola powder is perceived as a whole-food nutrient, offering antioxidants beyond isolated ascorbic acid. This perception supports strong growth in capsules, powders, and functional foods targeted at immunity and wellness. Subscription-based supplement models and personalized nutrition platforms are further reinforcing consistent demand.

Growth of the Global Nutraceutical Industry

The rapid expansion of nutraceutical manufacturing across North America, Europe, and Asia is driving ingredient consumption. Supplement brands increasingly rely on standardized botanical extracts to support premium positioning and product differentiation. Acerola powder aligns well with vegan, plant-based, and organic product claims, making it a preferred ingredient among health-focused brands launching new formulations.

What are the restraints for the global market?

Raw Material Supply Volatility

Acerola cherries are highly sensitive to climate conditions and must be processed quickly after harvesting. Weather variability in producing regions such as Brazil and the Caribbean can affect supply volumes, creating price instability and procurement challenges for manufacturers relying on consistent ingredient sourcing.

High Processing and Production Costs

Premium processing methods such as freeze-drying preserve nutrient integrity but significantly increase production expenses. This cost difference compared to synthetic vitamin C limits adoption in price-sensitive food categories, particularly in emerging markets where cost efficiency remains a priority.

What are the key opportunities in the cherry acerola powder industry?

Natural Replacement for Synthetic Additives

Manufacturers are increasingly replacing artificial antioxidants and preservatives with plant-based alternatives. Acerola powder enables “natural vitamin C” labeling while maintaining functional performance, creating major opportunities in packaged foods, beverages, and confectionery products seeking clean-label reformulation.

Vertical Integration in Producing Regions

Processing investments in Latin America are enabling suppliers to move beyond raw fruit exports toward high-value standardized powders. Companies adopting contract farming, traceability systems, and organic certification are securing long-term competitive advantages while improving supply chain stability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 214 Million |

| Market Size in 2026 | USD 238.82 Million |

| Market Size in 2031 | USD 413.43 Million |

| CAGR | 11.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The organic cherry acerola powder segment accounts for the largest share of the global market, primarily driven by accelerating consumer preference for clean-label, traceable, and naturally sourced nutritional ingredients. Rising awareness regarding pesticide-free cultivation, environmental sustainability, and product transparency has strengthened demand for certified organic ingredients across nutraceutical, functional food, and premium beverage applications. Organic certification enables manufacturers to position products within high-value health and wellness categories while achieving premium pricing advantages, particularly across mature markets in North America and Europe where regulatory scrutiny and label transparency strongly influence purchasing decisions. Additionally, growing retailer requirements for organic sourcing and increasing investment in sustainable agricultural practices are encouraging supply chain transformation toward certified organic production. Conventional cherry acerola powder continues to maintain relevance in large-scale food processing and cost-sensitive applications, where manufacturers prioritize production efficiency and stable supply volumes. However, ongoing shifts toward natural fortification and sustainable ingredient sourcing are steadily reinforcing long-term expansion of the organic segment as the leading product category.

Application Insights

Dietary supplements represent the leading application segment, supported by rising global demand for immunity enhancement, preventive healthcare, and plant-based micronutrient supplementation. The naturally high vitamin C concentration in acerola powder positions it as a preferred alternative to synthetic ascorbic acid, enabling supplement manufacturers to develop natural-positioned capsules, powders, gummies, and effervescent formulations. Increasing consumer focus on immune resilience, daily wellness routines, and holistic nutrition continues to accelerate adoption within this segment. Functional foods and beverages are emerging as the fastest-growing application area as manufacturers increasingly fortify everyday consumables such as juices, snack bars, dairy alternatives, and sports nutrition products with natural antioxidants. Growth is further supported by evolving consumer lifestyles that favor convenient nutrition delivery formats. Cosmetics and personal care applications are expanding steadily as acerola-derived vitamin C gains recognition for antioxidant protection, skin brightening, and anti-aging benefits within clean beauty formulations. Pharmaceutical applications remain comparatively niche but are witnessing gradual expansion, particularly in pediatric nutrition, effervescent vitamin products, and natural therapeutic formulations where bioavailable vitamin sources are gaining clinical interest.

Distribution Channel Insights

Direct manufacturer contracts dominate the distribution landscape, as large nutraceutical and food manufacturers increasingly establish long-term sourcing agreements to ensure consistent ingredient quality, supply reliability, and price stability amid fluctuating raw material availability. Strategic supplier partnerships also allow manufacturers to meet regulatory compliance and traceability requirements, which are becoming critical in global ingredient trade. B2B ingredient suppliers and specialty distributors continue to play an essential role in regional market penetration by offering technical expertise, formulation support, and localized logistics capabilities. At the same time, online ingredient procurement platforms are rapidly emerging as transformative distribution channels, enabling small and mid-sized brands to access international suppliers with improved transparency and reduced sourcing barriers. Digital procurement ecosystems are enhancing price discovery, shortening procurement cycles, and facilitating cross-border ingredient trade, thereby reshaping traditional distribution models across the global acerola powder market.

End-Use Industry Insights

Nutraceutical manufacturers constitute the largest end-use industry segment, driven by sustained global expansion of dietary supplement consumption and increasing demand for naturally derived vitamins and antioxidants. Acerola powder’s positioning as a whole-food vitamin C source aligns strongly with consumer preferences for minimally processed nutrition solutions, encouraging widespread adoption in immune health, energy support, and wellness-focused formulations. The food and beverage industry represents a rapidly growing end-use segment as companies accelerate clean-label reformulation strategies and replace synthetic additives with plant-based alternatives to meet evolving regulatory and consumer expectations. Cosmetic and personal care brands are increasingly incorporating acerola extracts into natural skincare and beauty formulations, leveraging antioxidant properties to support product claims related to skin rejuvenation and environmental protection. Meanwhile, animal nutrition is emerging as a niche yet promising application area, particularly within premium pet food and specialty livestock nutrition, where natural antioxidant supplementation is gaining importance for enhancing immunity and overall animal health.

Explore more data points, trends and opportunities Download Free Sample Report

Cherry Acerola Powder Market Segmentations

By Product Type

- Organic Cherry Acerola Powder

- Conventional Cherry Acerola Powder

- Freeze-Dried Acerola Powder

- Spray-Dried Acerola Powder

- Microencapsulated Acerola Powder

By Application

- Dietary Supplements & Nutraceuticals

- Functional Food & Beverages

- Pharmaceutical Preparations

- Cosmetics & Personal Care Products

- Animal Nutrition & Pet Supplements

By Distribution Channel

- Direct B2B Ingredient Supply

- Specialty Ingredient Distributors

- Online Ingredient Marketplaces

- Contract Manufacturing Supply Agreements

- Retail & Private Label Supply Chains

By End-Use Industry

- Nutraceutical Manufacturers

- Food & Beverage Manufacturers

- Pharmaceutical Companies

- Cosmetics & Personal Care Brands

- Animal Nutrition Producers

By Nature

- Organic Certified

- Non-Organic / Conventional

Regional Insights

North America

North America holds the largest share of the global cherry acerola powder market, supported by high dietary supplement penetration, advanced consumer awareness regarding preventive healthcare, and strong adoption of clean-label ingredients. The United States leads regional demand due to elevated consumer spending on wellness products, a mature nutraceutical industry, and extensive e-commerce infrastructure that facilitates rapid product accessibility. Regional growth is further driven by increasing demand for plant-based vitamins, expansion of functional beverage innovation, and regulatory encouragement toward natural ingredient substitution in food formulations. Strong presence of leading supplement brands, rising personalized nutrition trends, and continued investment in premium health products are reinforcing sustained market expansion across the region.

Europe

Europe represents a major consumption hub characterized by stringent food safety regulations and strong consumer preference for natural and organic ingredients. Regulatory limitations on synthetic additives and growing transparency requirements are encouraging manufacturers to adopt acerola powder as a natural vitamin C alternative. Countries such as Germany, France, Italy, and the United Kingdom demonstrate particularly strong demand, where organic certification significantly influences purchasing behavior and retail positioning. Regional growth is driven by expanding organic food markets, increasing vegan and plant-based product adoption, and rising consumer focus on sustainability and ethical sourcing. Additionally, innovation in functional foods and clean beauty products continues to accelerate ingredient adoption across European markets.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, fueled by rapid expansion of nutraceutical manufacturing capabilities and increasing health awareness among a growing middle-class population. China and India are emerging as key demand centers due to rising supplement consumption, urbanization, and expanding domestic health product industries. Japan and South Korea contribute stable demand supported by advanced functional beverage innovation and strong consumer acceptance of fortified nutrition products. Regional growth is further supported by increasing disposable incomes, expanding e-commerce penetration, government initiatives promoting preventive healthcare, and growing interest in natural immunity-enhancing ingredients following heightened public health awareness across the region.

Latin America

Latin America plays a dual role as both a major production base and an expanding consumption market for cherry acerola powder, with Brazil dominating global acerola cultivation and raw material supply. Favorable climatic conditions, agricultural expertise, and increasing investment in processing infrastructure are enabling regional producers to move up the value chain through standardized powder production and export-oriented manufacturing. Growth drivers include rising international demand for traceable natural ingredients, improvements in post-harvest processing technologies, and expanding partnerships between regional producers and global nutraceutical companies. Increasing domestic awareness of functional nutrition is also gradually strengthening local consumption across key Latin American markets.

Middle East & Africa

The Middle East & Africa market is experiencing gradual but steady expansion, supported by rising health awareness, growing supplement imports, and increasing availability of premium wellness products. The United Arab Emirates and South Africa serve as primary regional demand centers due to expanding modern retail infrastructure and growing consumer interest in preventive healthcare solutions. Market growth is further driven by increasing expatriate populations, rising disposable incomes in urban centers, and expanding distribution networks for imported nutraceutical products. Additionally, the development of organized wellness retail channels and increasing adoption of functional foods are contributing to long-term regional market development.

Key Players in the Cherry Acerola Powder Market

- Naturex (Givaudan)

- Diana Food (Symrise)

- Nexira

- Duas Rodas Industrial

- Martin Bauer Group

- BGG World

- AIDP Inc.

- Sabinsa Corporation

- Nutra Green Biotechnology Co., Ltd.

- Xi’an Lyphar Biotech Co., Ltd.

- Foodchem International Corporation

- The Green Labs LLC

- Herbal Creative

- Acerola do Nordeste

- Ingredia Nutritional