Cheese Ingredients Market Size

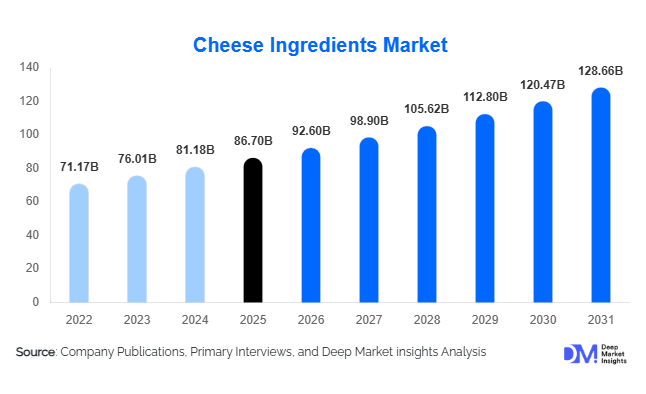

According to Deep Market Insights, the global cheese ingredients market size was valued at USD 86.7 billion in 2025 and is projected to grow from USD 92.60 billion in 2026 to reach USD 128.66 billion by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). Market growth is primarily driven by increasing global cheese consumption, expansion of processed and convenience food industries, and rising adoption of advanced fermentation-based dairy technologies. Cheese ingredients such as cultures, enzymes, milk proteins, emulsifiers, and stabilizers play a critical role in ensuring consistent texture, flavor, yield efficiency, and shelf-life performance across industrial cheese production.

Key Market Insights

- Milk proteins and milk powders dominate ingredient demand, accounting for over one-third of total market revenue due to their essential role in cheese yield optimization.

- Processed cheese production continues expanding globally, driven by fast-food chains, frozen meals, and packaged snacks.

- North America leads global demand supported by large-scale industrial cheese manufacturing and high per-capita consumption.

- Asia-Pacific is the fastest-growing region, fueled by westernized diets and rapid expansion of foodservice sectors in China and India.

- Precision fermentation and microbial cultures are reshaping production, enabling consistent quality and sustainable ingredient sourcing.

- Clean-label and specialty cheese innovation is encouraging development of natural cultures and enzyme-based flavor solutions.

What are the latest trends in the cheese ingredients market?

Rise of Precision Fermentation and Microbial Innovation

Fermentation-based technologies are transforming cheese ingredient production by enabling scalable manufacturing of enzymes and cultures without reliance on animal-derived sources. Fermentation-produced chymosin and specialized microbial cultures are increasingly used to improve coagulation efficiency, flavor development, and consistency across industrial cheese plants. These technologies reduce variability in production while supporting sustainability goals. Manufacturers are investing heavily in microbial strain development, allowing tailored solutions for regional cheese varieties and automated processing environments. Precision fermentation also improves cost stability by reducing dependency on fluctuating livestock supply chains, positioning biotechnology as a long-term growth pillar for the industry.

Growth of Clean-Label and Premium Cheese Formulations

Consumers increasingly prefer natural and minimally processed foods, prompting cheese manufacturers to reformulate products using clean-label ingredients. Natural starter cultures, enzyme-driven flavor enhancement, and reduced additive formulations are gaining traction across retail and foodservice applications. Premium and artisanal cheese categories are expanding globally, encouraging ingredient suppliers to develop culture blends that replicate traditional aging processes while maintaining industrial efficiency. Regulatory pressure for transparent labeling in Europe and North America further accelerates adoption of natural ingredients, driving innovation in preservation techniques and flavor optimization.

What are the key drivers in the cheese ingredients market?

Expansion of Processed and Convenience Foods

The rapid growth of ready-to-eat meals, frozen snacks, and quick-service restaurant menus has significantly increased demand for standardized cheese production. Processed cheese requires precise emulsification, texture stability, and meltability characteristics, all of which depend heavily on specialized ingredient systems. Urban lifestyles and rising dual-income households worldwide continue to support convenience food consumption, strengthening long-term ingredient demand across industrial manufacturing facilities.

Technological Advancements in Dairy Processing

Modern cheese production relies on automated manufacturing systems that require consistent ingredient performance. Advanced enzyme systems and starter cultures enable manufacturers to control moisture content, coagulation time, and flavor outcomes with high precision. Ingredient suppliers are evolving into formulation partners, offering customized blends designed for specific cheese applications, improving operational efficiency and reducing production waste.

What are the restraints for the global market?

Volatility in Dairy Raw Material Prices

Milk price fluctuations significantly impact production costs for cheese ingredients, particularly milk powders and whey proteins. Climate variability, feed price changes, and supply chain disruptions create pricing uncertainty, affecting margins for ingredient manufacturers and cheese processors alike.

Regulatory Complexity Across Regions

Different regulatory frameworks governing microbial cultures, additives, and labeling standards across regions create compliance challenges. Approval timelines and varying food safety requirements increase operational costs and may delay new ingredient commercialization, especially for innovative fermentation-derived products.

What are the key opportunities in the cheese ingredients industry?

Emerging Market Foodservice Expansion

Rapid expansion of pizza chains, burger outlets, and casual dining formats across Asia-Pacific, the Middle East, and Latin America is creating strong demand for processed cheese formulations. Ingredient suppliers capable of delivering performance-focused blends tailored to high-volume foodservice applications are expected to benefit from long-term supply contracts and recurring demand.

Clean-Label and Functional Ingredient Innovation

Opportunities are emerging for ingredient manufacturers to develop natural preservation systems, sodium-reduction solutions, and protein-enhanced formulations aligned with evolving consumer health preferences. Functional cultures and enzyme blends that improve flavor naturally while maintaining shelf life are gaining strong commercial traction, especially in premium retail cheese segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 86.70 Billion |

| Market Size in 2026 | USD 92.60 Billion |

| Market Size in 2031 | USD 128.66 Billion |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ingredient Type Insights

The global cheese ingredients market is strongly led by milk proteins and milk powders, which collectively account for approximately 34% of total market share. Their dominance is primarily attributed to their functional versatility in cheese manufacturing, where they play a central role in improving yield efficiency, moisture retention, protein standardization, and texture optimization. As global cheese production scales to meet rising consumer demand, manufacturers increasingly rely on milk-derived ingredients to ensure consistency across batches while maintaining cost efficiency. The growth of industrial cheese processing, particularly in processed and recombined cheese formats, continues to reinforce demand for milk powders and protein concentrates, as these ingredients allow producers to stabilize supply despite fluctuations in raw milk availability. Additionally, increasing adoption of high-protein dairy formulations aligned with evolving consumer nutrition preferences further strengthens this segment’s leadership position.Starter cultures and enzymes represent another critical component of market development, supported by growing emphasis on flavor customization, fermentation control, and product differentiation. Advanced microbial cultures enable manufacturers to achieve precise texture profiles, aroma development, and maturation consistency, which are increasingly important in both premium and mass-market cheese categories. The expansion of specialty and artisanal cheeses globally has accelerated demand for tailored culture solutions capable of delivering region-specific taste characteristics. Technological advancements in enzyme engineering are also enhancing coagulation efficiency and reducing processing time, contributing to improved operational productivity for large-scale producers.Emulsifiers and stabilizers remain indispensable, particularly within processed cheese applications where uniform meltability, sliceability, and extended shelf stability are essential product attributes. As convenience foods and ready-to-eat meal categories expand worldwide, manufacturers depend heavily on stabilizing systems to maintain product integrity during transportation, reheating, and long storage cycles. Meanwhile, flavoring ingredients and colorants are gaining increasing prominence as companies diversify portfolios toward premium, flavored, and culturally adapted cheese products. Consumer demand for innovative taste experiences, including smoked, spiced, and regionally inspired varieties, continues to expand the functional importance of flavor systems within ingredient formulations.

Application Insights

Processed cheese applications dominate global demand, contributing nearly 29% of the market and serving as the leading application segment due to their scalability, affordability, and compatibility with modern foodservice and packaged food industries. The primary driver behind this segment’s leadership is the growing global reliance on standardized cheese formats used in burgers, sandwiches, sauces, frozen meals, and snack products. Processed cheese enables manufacturers to achieve consistent melting behavior, longer shelf life, and stable flavor profiles, making it highly suitable for large-scale industrial and quick-service restaurant operations. Increasing urbanization and rising consumption of convenience foods further reinforce sustained demand for ingredient systems tailored to processed cheese manufacturing.Natural and hard cheese categories continue to experience steady expansion as premiumization trends reshape consumer preferences across developed markets. Growing appreciation for authentic dairy products, combined with rising disposable income levels, has encouraged demand for aged and specialty varieties requiring high-quality cultures, enzymes, and functional additives. The resurgence of artisanal production and protected-origin cheeses in several regions is also stimulating innovation in ingredient development to support traditional processing methods while maintaining commercial scalability.Fresh and soft cheeses are witnessing accelerating adoption in emerging economies where exposure to western cuisine and modern retail formats is increasing rapidly. Expanding middle-class populations and evolving dietary habits are encouraging consumption of mozzarella, cream cheese, and spreadable formats, thereby driving ingredient usage across new production facilities. Specialty cheese applications represent one of the fastest-growing areas, fueled by gourmet retail expansion, culinary experimentation, and consumer willingness to explore diverse flavor profiles. Food manufacturers are increasingly integrating specialty cheeses into premium ready meals and fusion cuisines, further strengthening ingredient demand.

Form Insights

Powdered cheese ingredients account for approximately 57% of total market demand, making them the dominant form segment due to their logistical, operational, and economic advantages. The leading driver behind powdered format adoption lies in its extended shelf life, reduced refrigeration requirements, and lower transportation costs, which collectively enhance supply chain efficiency. Powdered ingredients also enable precise dosing and formulation consistency in industrial production environments, allowing manufacturers to optimize production yields while minimizing waste. As global cheese trade expands and cross-border ingredient sourcing increases, powders provide superior stability compared to liquid alternatives, reinforcing their widespread adoption.Liquid formulations are primarily utilized in large-scale automated processing facilities that require continuous production flows and rapid ingredient integration. These systems support high-volume cheese manufacturing where speed and process uniformity are critical performance metrics. Paste and concentrate formats, although smaller in share, serve specialized roles in customized formulations and premium cheese production, where texture manipulation and flavor concentration are essential. The coexistence of multiple ingredient forms reflects the industry’s need to balance efficiency, flexibility, and product differentiation across diverse manufacturing models.

End-Use Industry Insights

Industrial cheese manufacturers represent the largest end-use segment, accounting for nearly 62% of global consumption and serving as the primary driver of ingredient demand worldwide. The segment’s dominance is largely supported by mass-scale production aimed at supplying retail chains, foodservice operators, and packaged food manufacturers. Increasing automation within dairy processing facilities has heightened the need for standardized ingredient solutions that ensure consistent texture, taste, and shelf stability across high production volumes. As global cheese consumption continues to expand, industrial producers increasingly depend on functional ingredient systems to maintain efficiency while controlling costs.Food processing companies constitute the fastest-growing end-use segment, propelled by rising demand for cheese-based snacks, sauces, frozen foods, and ready-to-eat meals. The integration of cheese ingredients into convenience food categories has expanded significantly as busy lifestyles and urban consumption patterns reshape global eating habits. Ingredient suppliers are therefore developing multifunctional solutions capable of delivering flavor intensity, melting performance, and storage stability suitable for processed food applications.Foodservice operators, particularly quick-service restaurant chains, continue to increase ingredient consumption through standardized menu offerings that rely heavily on consistent cheese performance. Global expansion of fast-food brands and cloud kitchen models further amplifies demand for reliable ingredient formulations. Additionally, export-oriented cheese producers contribute significantly to market growth, as international distribution requires stable compositions capable of maintaining quality throughout extended logistics cycles and varying climatic conditions.

Explore more data points, trends and opportunities Download Free Sample Report

Cheese Ingredients Market Segmentations

By Ingredient Type

- Milk Proteins & Milk Powders

- Starter Cultures

- Enzymes

- Emulsifiers & Stabilizers

- Flavoring Agents & Colorants

By Application

- Processed Cheese

- Natural Cheese

- Fresh Cheese

- Specialty & Artisanal Cheese

By Form

- Powder

- Liquid

- Paste

- Concentrates

By End-Use Industry

- Industrial Cheese Manufacturers

- Food Processing Companies

- Foodservice Industry

- Retail & Private Label Producers

By Distribution Channel

- Direct B2B Supply Contracts

- Ingredient Distributors

- Online B2B Procurement Platforms

- Regional Dairy Ingredient Suppliers

Regional Insights

North America

North America holds approximately 32% of global market share, led primarily by the United States, where large-scale industrial cheese production and high per-capita cheese consumption sustain strong ingredient demand. Regional growth is driven by advanced dairy processing infrastructure, widespread adoption of automation technologies, and continuous innovation in processed cheese applications tailored for foodservice and packaged food sectors. The rapid expansion of convenience foods, frozen meals, and cheese-based snacks further reinforces ingredient utilization. Additionally, strong research and development investments by dairy ingredient companies support formulation innovation focused on clean-label solutions, functional proteins, and improved melt performance. Canada contributes to regional growth through premium and specialty cheese production, supported by evolving consumer preference for high-quality dairy products and value-added formulations.

Europe

Europe accounts for nearly 29% of the global market, supported by deep-rooted cheese-making traditions across Germany, France, Italy, and the Netherlands. Regional growth is primarily driven by strong demand for specialty cultures and enzymes required for traditional and protected-origin cheeses. Stringent food quality regulations and increasing consumer focus on natural ingredients encourage adoption of clean-label and minimally processed cheese ingredient solutions. The continued expansion of artisanal and farm-based cheese production across European countries sustains demand for advanced fermentation technologies. Furthermore, export-oriented European cheese manufacturers rely heavily on ingredient innovation to maintain consistent quality standards across international markets, strengthening long-term market stability.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 8%, driven by rapid dietary transformation and modernization of dairy industries. China leads regional growth as western-style food consumption expands through fast-food chains, bakery applications, and ready meals incorporating cheese ingredients. India’s organized dairy sector modernization, investment in cold-chain infrastructure, and rising urban middle-class population are accelerating domestic cheese production and ingredient adoption. Japan and South Korea contribute through premium processed cheese consumption and innovation-led retail markets that emphasize convenience and product diversification. Increasing exposure to global cuisines, rising disposable incomes, and expanding retail penetration collectively position Asia-Pacific as a major future growth engine for cheese ingredients.

Latin America

Latin America is emerging as a promising growth region led by Brazil and Mexico, where expanding domestic dairy processing capabilities and growing fast-food penetration are increasing demand for standardized cheese ingredients. Urbanization and rising middle-class purchasing power are encouraging higher consumption of packaged dairy products and convenience foods incorporating cheese. Regional manufacturers are investing in production modernization to reduce reliance on imports, thereby creating opportunities for localized ingredient supply chains. Additionally, the popularity of processed and fresh cheese varieties across household consumption continues to support steady ingredient market expansion.

Middle East & Africa

The Middle East demonstrates strong demand for processed cheese products, particularly in Saudi Arabia and the United Arab Emirates, where limited domestic milk production results in significant reliance on imported ingredients and recombined cheese manufacturing. Growth in the regional foodservice industry, expanding retail infrastructure, and high consumption of packaged dairy products drive sustained ingredient demand. Increasing tourism and hospitality sector expansion further contribute to cheese usage across commercial kitchens. In Africa, gradual market expansion is supported by improving dairy infrastructure, investments in local milk processing, and rising urban populations adopting packaged and convenience food products. As cold-chain logistics improve and modern retail channels expand, cheese ingredient adoption is expected to accelerate steadily across the region.

Key Players in the Cheese Ingredients Market

- Chr. Hansen Holding A/S

- DSM-Firmenich

- IFF (DuPont Nutrition & Biosciences)

- Kerry Group plc

- Fonterra Co-operative Group Ltd.

- Arla Foods Ingredients Group

- Glanbia plc

- FrieslandCampina Ingredients

- Lactalis Ingredients

- Novonesis

- Ingredion Incorporated

- Corbion N.V.

- ADM (Archer Daniels Midland Company)

- Stern-Wywiol Gruppe

- Saputo Inc.