Cheese Analogue Market Size

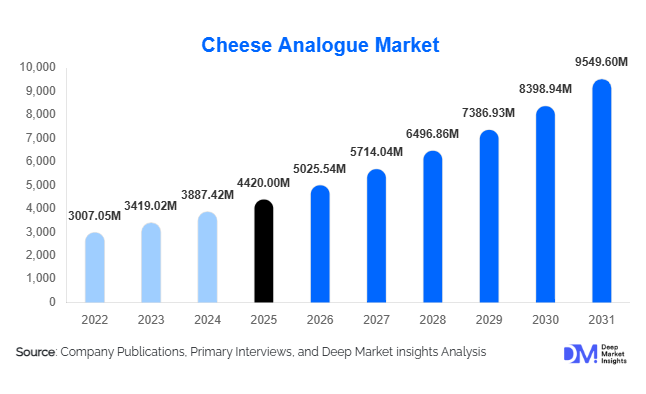

According to Deep Market Insights, the global cheese analogue market size was valued at USD 4,420 million in 2025 and is projected to grow from USD 5,025.54 million in 2026 to reach USD 9,549.60 million by 2031, expanding at a CAGR of 13.7% during the forecast period (2026–2031). Market growth is primarily driven by the rapid adoption of plant-based diets, rising lactose intolerance awareness, and increasing demand for sustainable dairy alternatives across foodservice and packaged food industries. Cheese analogues, formulated using plant proteins and vegetable fats, are increasingly being integrated into pizzas, ready meals, bakery products, and quick-service restaurant menus as cost-efficient and environmentally sustainable substitutes for conventional dairy cheese.

Key Market Insights

- Plant-based consumption trends are accelerating globally, positioning cheese analogues as a mainstream dairy alternative rather than a niche vegan product.

- Foodservice applications dominate demand, particularly pizza chains and QSR operators requiring meltable cheese substitutes.

- North America leads global consumption, supported by strong retail penetration and innovation ecosystems.

- Asia-Pacific is the fastest-growing region, driven by lactose intolerance prevalence and urban dietary shifts.

- Technological advancements in fermentation and plant protein structuring are improving taste, texture, and melting performance.

- Private-label expansion by supermarkets is reducing prices and increasing consumer accessibility worldwide.

What are the latest trends in the cheese analogue market?

Clean-Label and Functional Ingredient Innovation

Consumers increasingly demand plant-based foods with recognizable ingredients and improved nutritional profiles. Manufacturers are reformulating cheese analogues using natural emulsifiers, fortified proteins, and allergen-free bases such as oat and pea protein. Clean-label positioning has become a major competitive differentiator, particularly in Europe and North America, where consumers prioritize transparency and minimal processing. Fortification with calcium, vitamin B12, and protein enrichment is helping cheese analogues compete nutritionally with dairy cheese while expanding appeal beyond vegan consumers toward flexitarian households.

Foodservice-Led Product Customization

Cheese analogue producers are collaborating closely with quick-service restaurants and frozen food manufacturers to create application-specific formulations optimized for melt stretch, browning behavior, and shelf stability. Customized mozzarella-style analogues designed for pizza applications now represent the largest revenue segment globally. Foodservice demand has encouraged bulk packaging innovations, cost optimization strategies, and scalable production models. This trend is accelerating industrial adoption, transforming cheese analogues into functional ingredients rather than standalone retail products.

What are the key drivers in the cheese analogue market?

Growing Flexitarian Consumer Base

The expansion of flexitarian diets is a primary growth driver, as consumers increasingly reduce dairy intake without fully eliminating animal products. Health concerns, ethical consumption patterns, and environmental awareness are encouraging trial and repeat purchases of plant-based cheese. Retailers have expanded shelf space dedicated to dairy alternatives, significantly improving product visibility and accessibility.

Sustainability and Carbon Reduction Goals

Food manufacturers and restaurant chains are adopting plant-based ingredients to meet sustainability targets and reduce carbon footprints. Cheese analogue production typically requires fewer natural resources compared to dairy cheese, aligning with corporate ESG commitments. Governments and institutional buyers are also encouraging alternative proteins within public food programs, strengthening long-term demand.

What are the restraints for the global market?

Taste and Texture Perception Challenges

Despite technological improvements, some consumers still perceive cheese analogues as inferior to dairy cheese in flavor depth and mouthfeel. Premium culinary applications remain sensitive to sensory differences, limiting adoption in traditional cuisine markets.

Regulatory and Labeling Variability

Different regulatory frameworks governing dairy alternative labeling create compliance challenges for global manufacturers. Restrictions on terminology such as “cheese” in certain regions require rebranding efforts and additional marketing investment, slowing market expansion.

What are the key opportunities in the cheese analogue industry?

Precision Fermentation and Hybrid Cheese Development

Advancements in fermentation technology are enabling the production of dairy-identical proteins without animal agriculture. Hybrid formulations combining plant fats with fermentation-derived proteins are closing sensory gaps with traditional cheese. Companies investing in biotechnology integration are expected to capture premium market segments and expand into gourmet categories.

Emerging Market Manufacturing Expansion

Regions with high dairy import dependency, including Southeast Asia and the Middle East, present strong opportunities for localized production. Cheese analogues offer longer shelf life and price stability compared to imported dairy products, encouraging government support for domestic alternative protein facilities. Strategic investments in regional manufacturing hubs are expected to reduce logistics costs and improve supply reliability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4420 Million |

| Market Size in 2026 | USD 5025.54 Million |

| Market Size in 2031 | USD 9549.60 Million |

| CAGR | 13.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global cheese analogue market demonstrates strong product diversification; however, mozzarella analogue continues to dominate the competitive landscape, accounting for nearly 34% of total revenue share in 2025. The segment’s leadership is primarily supported by its critical functional properties, including superior meltability, stretchability, and browning performance, which closely replicate conventional dairy mozzarella. These characteristics make it highly suitable for large-scale industrial applications, particularly within pizza manufacturing, quick-service restaurant (QSR) chains, and frozen food production. The rapid expansion of global pizza consumption, coupled with the need for cost-efficient and standardized ingredients, has reinforced sustained demand for mozzarella analogue products. In addition, manufacturers increasingly prefer mozzarella analogues due to improved shelf stability, predictable pricing compared to dairy cheese, and compatibility with plant-based formulations.Cheddar-style and processed slice analogues represent the next major product categories, benefiting from their extensive usage in burgers, sandwiches, and convenience foods. The growth of fast-casual dining formats and ready-to-eat packaged meals has increased reliance on sliceable and easily portioned cheese alternatives that deliver consistent texture and flavor across large production volumes. Processed analogue formats also allow manufacturers to customize fat content, sodium levels, and nutritional profiles, aligning with evolving health-conscious consumer preferences.Cream cheese and spreadable analogue varieties are gaining strong traction in retail-driven consumption environments as breakfast occasions, snacking culture, and home cooking trends expand globally. These products appeal to flexitarian consumers seeking dairy-free alternatives without compromising taste or usability. Meanwhile, specialty and artisanal plant-based cheeses are emerging within premium market tiers, supported by advancements in precision fermentation, nut-based culturing techniques, and gourmet vegan culinary innovation. As foodservice operators increasingly emphasize differentiated menu experiences, premium analogue cheeses are expected to expand their share within high-value segments.

Application Insights

By application, melting applications remain the dominant category, contributing approximately 41% of global demand, driven by widespread utilization in frozen pizzas, baked foods, casseroles, and ready meals. The leading position of this segment is largely attributed to the functional versatility of cheese analogues, which enable manufacturers to achieve consistent melting behavior while maintaining cost efficiency and extended product shelf life. Rising global consumption of convenience foods and increasing reliance on frozen meal solutions among urban consumers continue to reinforce demand for melt-focused formulations.Processed food manufacturing represents another critical application area, as producers integrate cheese analogues into snacks, prepared meals, and packaged foods to optimize ingredient costs and enable vegan or lactose-free labeling claims. Manufacturers benefit from formulation flexibility, allowing them to adjust flavor intensity, texture, and nutritional composition according to regional consumer preferences. This adaptability has encouraged widespread adoption among multinational food processors seeking scalable plant-based product portfolios.Cold consumption applications, including sandwiches, wraps, salads, and deli products, are expanding steadily due to rising on-the-go eating habits and growing demand for plant-based lunch solutions. At the same time, cooking ingredients and sauce applications are emerging as fast-growing niches, supported by experimentation in plant-based culinary formats and the increasing popularity of dairy-free pasta sauces, dips, and home-cooking kits. As consumers increasingly replicate restaurant-style meals at home, ingredient-based analogue cheese usage is expected to accelerate further.

Distribution Channel Insights

Retail supermarkets and hypermarkets collectively account for nearly 38% of global sales, maintaining their leadership position due to extensive product visibility, expanding private-label portfolios, and rising consumer familiarity with plant-based dairy alternatives. Large retail chains continue to allocate greater shelf space to vegan and lactose-free categories, supported by aggressive promotional strategies and improved cold-chain logistics. The expansion of affordable store-brand offerings has also broadened accessibility beyond niche vegan consumers to mainstream households.Foodservice distribution represents the fastest-growing channel, fueled by rapid menu innovation across global restaurant chains and institutional catering providers. Quick-service restaurants, casual dining establishments, and cloud kitchens increasingly adopt cheese analogues to meet rising consumer demand for plant-based menu options while maintaining operational cost stability. The scalability and consistency offered by analogue cheese products make them particularly attractive for high-volume foodservice operations.Online retail and direct-to-consumer platforms are gaining notable momentum, especially among younger demographics and urban consumers seeking specialty vegan products. Subscription-based grocery services, digital-first plant-based brands, and e-commerce grocery marketplaces are enhancing product discovery and enabling niche premium offerings to reach wider audiences. Improved cold delivery infrastructure and digital marketing strategies are expected to further accelerate online channel growth over the forecast period.

End-Use Industry Insights

The foodservice sector leads overall end-use demand, accounting for approximately 36% market share, supported by the rapid global expansion of QSR chains and increasing diversification of vegan and flexitarian menu offerings. Restaurants benefit from the predictable pricing and functional reliability of cheese analogues, allowing them to manage food costs while responding to changing dietary preferences. The growing popularity of plant-based pizzas, burgers, and baked dishes continues to reinforce foodservice adoption.Packaged food manufacturers represent a major growth engine within the market, integrating cheese analogues into frozen meals, savory snacks, ready-to-cook kits, and plant-based prepared foods. The segment’s growth is primarily driven by the need for scalable, stable, and customizable ingredients that align with clean-label and dairy-free product positioning. As convenience food consumption rises globally, analogue cheese inclusion across processed food categories is expected to deepen.Household consumption is steadily increasing as product affordability improves and taste parity with dairy cheese advances through formulation innovation. Retail availability, expanding recipe awareness, and growing adoption of flexitarian diets are encouraging repeat purchases among consumers. Emerging applications are also appearing in bakery fillings, plant-based sauces, and protein-enriched ready-to-eat meals, reflecting broader integration of cheese analogues into everyday culinary usage patterns.

Explore more data points, trends and opportunities Download Free Sample Report

Cheese Analogue Market Segmentations

By Product Type

- Mozzarella Cheese Analogues

- Cheddar Cheese Analogues

- Processed Slice Cheese Analogues

- Cream Cheese Spreadable Analogues

- Specialty Artisan Plant-Based Cheese Analogues

By Application

- Pizza Bakery Products

- Processed Packaged Foods

- Sauces, Dressings Culinary Ingredients

- Ready-to-Eat Frozen Meals

- Household Consumption

By Distribution Channel

- Supermarkets Hypermarkets

- Foodservice HoReCa Distribution

- Online Retail E-commerce

- Direct-to-Consumer Sales

By End-Use Industry

- Foodservice Industry

- Packaged Food Manufacturers

- Household Retail Consumers

- Industrial Food Processing

Regional Insights

North America

North America holds approximately 32% of global market share, led by the United States, which accounts for nearly 27% of global consumption. Regional growth is strongly supported by high consumer awareness of plant-based nutrition, widespread vegan and flexitarian adoption, and continuous innovation from food technology startups and established food manufacturers. Advanced retail infrastructure enables rapid commercialization of new analogue products, while strong investment in alternative protein research accelerates product development. Additionally, rising lactose intolerance awareness, sustainability-focused purchasing behavior, and aggressive expansion of plant-based offerings across QSR chains are further strengthening market penetration. Canada is witnessing increasing private-label adoption and institutional procurement of plant-based foods across schools and healthcare facilities, contributing to stable regional expansion.

Europe

Europe accounts for nearly 29% market share, with Germany, the United Kingdom, and the Netherlands emerging as leading adoption hubs. Regional growth is driven by strong environmental consciousness, carbon reduction initiatives, and supportive regulatory frameworks promoting sustainable food systems. European consumers demonstrate a pronounced preference for clean-label, organic, and ethically sourced products, encouraging manufacturers to develop premium-quality cheese analogues with natural ingredients. Government-backed sustainability campaigns, expanding vegan product labeling standards, and increased availability of plant-based options in retail and foodservice channels continue to stimulate demand. The region also benefits from strong innovation in fermentation-based dairy alternatives and culinary acceptance of plant-forward diets.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at an estimated CAGR of nearly 16%. Growth is primarily fueled by rapid urbanization, expanding middle-class populations, and high lactose intolerance prevalence across several countries. China, India, Japan, and Australia serve as key demand centers, where Western-style fast food consumption and frozen food adoption are increasing significantly. The proliferation of international pizza and burger chains across metropolitan areas has created strong demand for meltable cheese alternatives. In addition, rising health awareness, growing vegetarian populations, and government initiatives promoting food innovation are accelerating regional acceptance of plant-based dairy substitutes. Local manufacturers are increasingly investing in regionally tailored flavors and price-competitive formulations to capture mass-market adoption.

Latin America

Latin America, led by Brazil and Mexico, is emerging as a promising growth region as processed food manufacturers increasingly incorporate cheese analogues to stabilize raw material costs amid dairy price volatility. Urbanization and expanding retail modernization are improving product accessibility, while growing consumer exposure to plant-based diets through social media and international food trends is supporting gradual demand expansion. Regional food processors are adopting analogue cheese solutions to enhance product affordability and extend shelf life, particularly within frozen and packaged food categories. As economic conditions encourage cost optimization across food production, adoption of cheese analogues is expected to strengthen further.

Middle East & Africa

The Middle East & Africa region is witnessing steady adoption, with the UAE and Saudi Arabia representing key markets driven by import-dependent food systems and strong hospitality sector activity. Limited domestic dairy production and fluctuating dairy supply costs encourage foodservice operators to explore alternative cheese solutions that offer pricing stability and longer storage life. Tourism-driven hospitality expansion, international restaurant franchises, and rising demand for halal-certified plant-based products are accelerating regional growth. Increasing expatriate populations and evolving dietary preferences toward healthier and sustainable foods are also contributing to market expansion, while modern retail development continues to enhance consumer exposure to plant-based dairy alternatives.

Key Players in the Cheese Analogue Market

- Daiya Foods Inc.

- Violife Foods

- Follow Your Heart

- Miyoko’s Creamery

- Upfield Holdings B.V.

- Kite Hill

- Tofutti Brands Inc.

- Good Planet Foods

- Parmela Creamery

- Green Vie Foods

- Nush Foods

- Bute Island Foods

- Willicroft

- Nurishh (Bel Group)

- Dr. Mannah’s