Cereal and Snack Inclusions Market Size

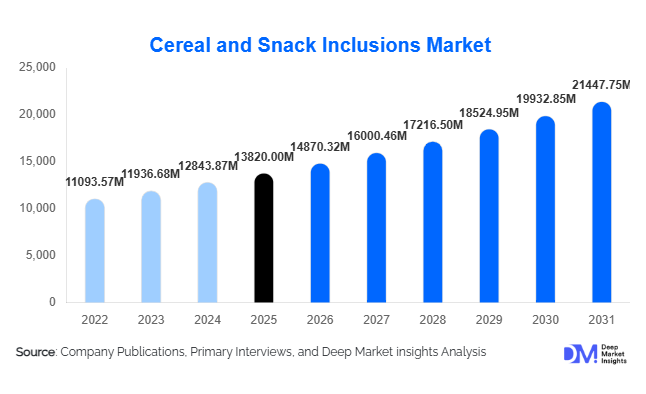

According to Deep Market Insights,the global cereal and snack inclusions market size was valued at USD 13,820 million in 2025 and is projected to grow from USD 14,870.32 million in 2026 to reach USD 21,447.75 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). Market growth is primarily driven by the rising global demand for texture-rich and functional snacking products, increasing premiumization across bakery and dairy applications, and the expanding popularity of protein-fortified cereals and snack bars.

Key Market Insights

- Chocolate inclusions dominate globally, accounting for nearly 28% of total market share, driven by strong demand in cereals, bakery, and frozen desserts.

- Snack bars represent the leading application segment (24% share), supported by rising protein and energy bar consumption worldwide.

- North America holds the largest regional share (34%), with the U.S. being the primary consumption hub for premium snack inclusions.

- Asia-Pacific is the fastest-growing region, expanding at approximately 9% CAGR due to urbanization and Westernized dietary patterns.

- Solid-form inclusions account for over 50% of demand, preferred for texture enhancement and processing convenience.

- Functional and clean-label inclusions are emerging as high-growth niches, particularly protein crispies, fiber-enriched bits, and freeze-dried fruit pieces.

What are the latest trends in the cereal and snack inclusions market?

Functional and High-Protein Inclusions Gaining Momentum

One of the most prominent trends shaping the cereal and snack inclusions market is the rapid growth of protein-fortified and functional inclusions. Consumers increasingly seek snacks that offer satiety, muscle recovery, and digestive benefits. Protein crispies, collagen-infused bits, vitamin-fortified clusters, and fiber-enriched grains are being widely integrated into snack bars and breakfast cereals. Food manufacturers are leveraging extrusion technologies to develop high-protein, low-sugar inclusions that maintain texture stability during processing. This shift toward health-driven indulgence is enabling brands to command premium pricing while meeting clean-label expectations.

Premiumization and Texture Innovation

Texture has become a major differentiator in competitive snack categories. Brands are incorporating multi-textural inclusions such as caramel-filled chocolate chunks, coated nut clusters, and freeze-dried fruit bits to enhance sensory appeal. In dairy and frozen desserts, inclusions are used to create layered experiences that justify premium positioning. Technological advancements in coating and encapsulation are helping prevent moisture migration, thereby preserving crunch and extending shelf life. The growing demand for artisanal bakery and gourmet cereals is further accelerating innovation in customized inclusion formats.

What are the key drivers in the cereal and snack inclusions market?

Expansion of Global Snacking Culture

Urban lifestyles and on-the-go consumption habits have fueled sustained growth in snack bars, ready-to-eat cereals, and convenience bakery products. With the global snack bar industry exceeding USD 6 billion and growing steadily, demand for chocolate chips, nut clusters, and protein crispies continues to expand. This behavioral shift toward frequent small meals is a structural driver for inclusion manufacturers.

Growth of Premium Bakery and Dairy Segments

Premium ice creams, yogurts, and artisanal baked goods increasingly rely on inclusions to enhance product differentiation. Coated chocolate pieces, freeze-dried fruit, and caramel bits elevate both flavor and visual appeal. As global bakery markets surpass USD 500 billion in value, even incremental inclusion adoption translates into significant revenue growth for ingredient suppliers.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuating prices of cocoa, nuts, dairy solids, and specialty grains significantly impact inclusion production costs. Climate-related disruptions in cocoa-producing regions and supply chain uncertainties can compress margins, particularly for chocolate-based inclusions.

Technical Challenges in Shelf Stability

Moisture migration between inclusions and host products such as cereals can affect texture quality. Advanced encapsulation and fat-based barriers are required to maintain crunch, increasing R&D and production costs for manufacturers.

What are the key opportunities in the cereal and snack inclusions industry?

Emerging Market Expansion

Asia-Pacific and Latin America present strong growth opportunities due to rising disposable incomes and expanding processed food consumption. Countries such as India, China, Brazil, and Mexico are witnessing rapid growth in breakfast cereal and packaged snack demand, creating long-term revenue potential for inclusion manufacturers.

Clean-Label and Sustainable Ingredient Development

Consumers are increasingly prioritizing non-GMO, organic, and sustainably sourced ingredients. Companies investing in traceable cocoa sourcing, upcycled fruit inclusions, and reduced-sugar chocolate chips are well-positioned to capture premium segments. Sustainability-focused CapEx is also strengthening brand equity among global food manufacturers.

Ingredient Type Insights

Chocolate inclusions lead the global market with approximately 28% revenue share in 2025, primarily driven by their extensive application across cereals, snack bars, frozen desserts, bakery products, and confectionery. The dominance of chocolate inclusions is supported by strong consumer preference for indulgent flavors, premiumization trends, and the rising demand for high-protein and energy-based snacks where chocolate enhances taste appeal and value perception. Continuous innovation in dark, sugar-reduced, and functional chocolate variants further strengthens this segment’s leadership.

Fruit inclusions, particularly freeze-dried and dehydrated variants, are witnessing accelerated adoption due to their ability to retain nutritional value, natural color, and authentic flavor profiles. Growing consumer demand for clean-label, plant-based, and naturally sourced ingredients is significantly boosting fruit inclusion penetration across cereals, yogurts, and snack bars. Nut and seed inclusions maintain steady growth momentum, supported by increasing demand for protein-rich, fiber-dense, and healthy snacking formats. Almonds, peanuts, chia seeds, and flax seeds are widely incorporated into energy bars and breakfast applications to enhance nutritional positioning. Cereal and grain crispies continue to see strong adoption, particularly in cost-sensitive, high-volume energy bar and cereal production, where texture enhancement and structural stability are key purchasing drivers. Functional inclusions represent the fastest-growing sub-segment, driven by rising consumer interest in fortified foods featuring probiotics, added protein, adaptogens, and immunity-supporting ingredients.

Form Insights

Solid-form inclusions account for nearly 52% of total demand, supported by their structural integrity, visual appeal, and superior texture performance in baked goods, bars, and confectionery applications. Solid inclusions provide defined shape retention during processing, making them ideal for extrusion, baking, and mixing operations. Their dominance is further strengthened by ease of handling, longer shelf life, and compatibility with automated manufacturing systems.

Coated and encapsulated inclusions are expanding rapidly, particularly in high-moisture and temperature-sensitive applications such as yogurt, ice cream, and frozen desserts. The primary growth driver for this segment is the need for moisture protection, flavor stability, and controlled release functionality. Encapsulation technologies help prevent ingredient migration, preserve crunchiness, and extend product shelf life, making them increasingly important in premium dairy and dessert innovations.

Application Insights

Snack bars dominate the application landscape with approximately 24% market share, driven by the rapid expansion of protein bars, meal-replacement bars, and functional snack products across North America and Europe. The leading driver for this segment is rising consumer preference for convenient, on-the-go nutrition combined with high-protein and fortified formulations. Inclusions enhance both texture differentiation and nutritional claims, making them essential components in bar innovation.

Breakfast cereals remain a high-volume application segment, supported by widespread household consumption and continuous flavor innovation. Dairy and frozen desserts are emerging as premium, high-margin application areas, fueled by demand for indulgent textures, layered sensory experiences, and premium positioning in developed markets. Confectionery and ready-to-eat snacks also represent significant consumption channels, benefiting from ongoing product diversification, seasonal launches, and clean-label reformulations.

Distribution Channel Insights

Direct B2B sales to large food manufacturers account for approximately 63% of total revenue, reflecting long-term supply agreements, stringent quality assurance requirements, and the need for customized ingredient solutions. Large multinational food companies prefer direct procurement to ensure formulation consistency, pricing stability, and supply chain reliability.Ingredient distributors play a critical role in serving regional, mid-sized, and emerging manufacturers that require flexible order volumes and technical support. The growing number of small and medium-scale snack and bakery brands, particularly in emerging economies, continues to strengthen the importance of distributor networks in market expansion.

| By Ingredient Type | By Form | By Application | By Nature | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global market share, led predominantly by the United States, which accounts for over 80% of regional revenue. Regional growth is primarily driven by high consumption of protein bars, breakfast cereals, premium ice creams, and functional snacks. Strong health and wellness awareness, demand for fortified food products, and rapid product innovation cycles further stimulate inclusion demand. Additionally, well-established food processing infrastructure, advanced cold chain systems, and the presence of leading snack manufacturers contribute significantly to sustained regional dominance.

Europe

Europe represents nearly 29% of the global market share, with Germany, the U.K., France, and Belgium serving as key markets. Growth in the region is supported by strong bakery traditions, premium chocolate expertise, and high demand for artisanal and clean-label products. Increasing consumer preference for organic, sustainably sourced, and low-sugar formulations further drives inclusion innovation. The region’s well-developed retail network and private label expansion also contribute to stable demand growth across cereals, confectionery, and dairy applications.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at approximately 9% CAGR. China, India, and Japan lead regional demand growth, supported by rapid urbanization, rising disposable incomes, and increasing adoption of Western-style snacking habits. Expanding modern retail infrastructure, growth in e-commerce grocery platforms, and a young consumer demographic significantly boost snack and cereal consumption. Additionally, multinational food brands are increasing manufacturing investments in the region, further accelerating inclusion demand.

Latin America

Brazil and Mexico dominate regional demand, driven by the expansion of packaged snack industries and growing middle-class consumption. Increasing penetration of modern retail chains, rising demand for indulgent confectionery products, and improving economic stability in key countries contribute to steady growth. Local manufacturers are also incorporating value-added inclusions to differentiate products in competitive retail environments.

Middle East & Africa

The UAE and South Africa represent major markets within the region, supported by rapid retail expansion, premium food imports, and growing expatriate populations. Regional growth is fueled by increasing adoption of Western breakfast formats, rising demand for convenience foods, and expansion of international foodservice chains. Investments in food processing infrastructure and government initiatives supporting domestic food manufacturing are further strengthening long-term market potential.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Cereal and Snack Inclusions Market

- Barry Callebaut AG

- Cargill Incorporated

- ADM

- Kerry Group plc

- Tate & Lyle PLC

- Puratos Group

- AGRANA Beteiligungs-AG

- Sensient Technologies

- Döhler Group

- Ingredion Incorporated

- Bunge Limited

- Olam Group

- Taura Natural Ingredients

- Buhler Group

- Blommer Chocolate Company