CBD Supplements Market Size

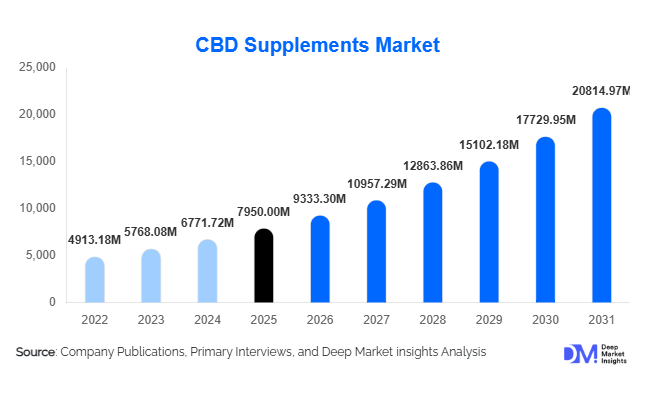

According to Deep Market Insights,the global CBD supplements market size was valued at USD 7,950 million in 2025 and is projected to grow from USD 9,333.30 million in 2026 to reach USD 20,814.97 million by 2031, expanding at a CAGR of 17.4% during the forecast period (2026–2031). The CBD supplements market growth is primarily driven by increasing legalization of hemp-derived products, growing consumer preference for natural wellness solutions, and technological innovations improving bioavailability and formulation consistency.

Key Market Insights

- Oils & Tinctures dominate product formats, offering high concentration, flexible dosing, and premium positioning, appealing to new and experienced users alike.

- Hemp-derived CBD leads the market globally due to broader legal acceptance, lower regulatory barriers, and suitability for international trade.

- Online retail is the leading distribution channel, fueled by direct-to-consumer subscription models, e-commerce platforms, and increasing digital marketing penetration.

- Sleep & Stress Management applications are expanding rapidly, supported by increasing prevalence of mental wellness concerns worldwide.

- Adults aged 18–40 years represent the largest end-user group, driven by urban lifestyles, digital purchasing habits, and high engagement with wellness supplements.

- Asia-Pacific is emerging as the fastest-growing regional market, driven by regulatory evolution, rising disposable income, and growing awareness of plant-based wellness

What are the latest trends in the CBD supplements market?

Clinical-Backed and Evidence-Based Formulations

Manufacturers are increasingly shifting toward scientifically validated CBD formulations to meet consumer demand for efficacy and safety. Products targeting specific health conditions such as sleep disorders, anxiety, and chronic pain are gaining traction. Clinical trials, third-party testing, and certification programs are becoming common, enhancing consumer trust and brand credibility. Proprietary delivery technologies like nano-emulsions and water-soluble formulations are improving bioavailability and consistency, enabling premium pricing and repeat purchases.

Expansion of E-Commerce and Direct-to-Consumer Channels

The growth of online retail has transformed the CBD supplements landscape. Consumers increasingly rely on D2C brand websites and e-commerce marketplaces for product selection, price comparison, and subscription-based models. Digital marketing campaigns, influencer promotions, and social media engagement are critical for reaching urban, younger demographics. Online channels also allow brands to offer personalized products, loyalty programs, and educational content, enhancing retention and increasing cross-sell opportunities.

What are the key drivers in the CBD supplements market?

Rising Health and Wellness Awareness

Consumers are seeking natural, non-addictive alternatives to traditional pharmaceuticals, particularly for anxiety, sleep disturbances, and pain management. This has significantly increased demand for plant-based wellness solutions like CBD supplements. Urbanized lifestyles and heightened awareness of preventive health measures are further supporting this trend, especially in North America and Europe.

Regulatory Progress and Legalization

The gradual legalization of hemp-derived CBD products in key global markets has reduced entry barriers, expanded supply chains, and increased consumer confidence. Clear labeling, dosage standards, and quality regulations are helping mainstream adoption, enabling manufacturers to scale operations and target international markets.

Technological Innovations in Formulations

Advanced delivery systems, such as nano-emulsions, encapsulated powders, and water-soluble CBD, are improving absorption and efficacy. These technologies are crucial for attracting health-conscious consumers seeking fast-acting, reliable supplements. Enhanced formulations also support premium product positioning and brand differentiation.

Market Restraints

Regulatory Inconsistencies Across Regions

Despite progress in legalization, CBD regulations remain inconsistent globally. Differences in THC thresholds, labeling requirements, and import/export rules limit cross-border market penetration. This creates challenges for international brands and can delay product launches.

Raw Material Price Volatility

CBD production relies heavily on hemp biomass, which is subject to yield fluctuations, climate impact, and cultivation costs. These supply-side pressures can increase production costs and affect profit margins for manufacturers, potentially slowing market growth.

What are the key opportunities in the CBD supplements market?

Regulatory Normalization and Standardization

Improved clarity in global regulations, including dosage standards, labeling requirements, and certification programs, presents a significant opportunity. Companies entering newly regulated markets can leverage compliance to build consumer trust and expand exports. Institutional investors are also more likely to fund established players in transparent regulatory environments.

Emerging Regional Markets in Asia-Pacific and Latin America

Countries like India, Japan, Brazil, and Mexico are witnessing increased interest in hemp-derived wellness products. Rising disposable income, urban stress lifestyles, and expanding e-commerce channels are creating a fertile market for new entrants. Local partnerships, targeted marketing campaigns, and culturally tailored formulations can help companies capture these growth opportunities.

Integration with Sports Nutrition and Women’s Health

CBD supplements are increasingly being incorporated into sports recovery and women’s health applications. Athletes and active lifestyle consumers are adopting CBD for inflammation reduction and performance enhancement, while women’s health products address PMS and hormonal balance. Targeted marketing and specialized formulations in these sub-segments offer high repeat purchase potential and brand differentiation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7950 Million |

| Market Size in 2026 | USD 9333.30 Million |

| Market Size in 2031 | USD 20814.97 Million |

| CAGR | 17.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product landscape of the CBD supplements market remains diversified, yet Oils & Tinctures continue to lead with approximately 34% of the global market share in 2025. Their dominance is primarily driven by superior bioavailability, flexible dosing control, faster onset of action, and higher concentration formulations that appeal to both therapeutic and preventive health users. The leading segment driver is consumer preference for customizable dosage formats that support personalized wellness regimens. As awareness of cannabinoid science expands, oils and tinctures benefit from clinical validation trends and their compatibility with both medical and lifestyle applications. Capsules & Softgels account for nearly 20% of the market, supported by convenience, discreet consumption, and standardized dosing advantages that attract first-time and compliance-focused consumers. Gummies & Chewables hold approximately 15%, driven by palatability, lifestyle branding, and growing demand among younger demographics seeking enjoyable supplement experiences. Powders, drink mixes, and topical formulations collectively represent the remaining 31%, benefiting from innovation in functional beverages, sports nutrition blends, and dermaceutical applications. Continuous innovation in nano-emulsion technology, water-soluble CBD, and premium full-spectrum extracts is expected to reinforce oils & tinctures leadership while expanding the addressable market for advanced delivery formats.

Application Insights

Sleep & Stress Management remains the leading application segment with approximately 29% global share, primarily driven by rising anxiety prevalence, demanding urban lifestyles, and increasing consumer focus on mental wellness. The leading segment driver is the growing global burden of stress-related disorders and insomnia, prompting consumers to adopt natural, non-addictive alternatives to traditional pharmaceuticals. Pain management follows closely with around 24% share, supported by the increasing incidence of chronic pain conditions, arthritis, and sports-related injuries, alongside a shift toward plant-based therapeutic options. General wellness applications are expanding steadily as preventive healthcare gains momentum worldwide. Sports recovery is witnessing accelerated uptake among fitness-focused consumers and professional athletes seeking inflammation management and muscle recovery solutions. Women’s health applications, including hormonal balance and menstrual support formulations, are emerging as high-growth niches fueled by targeted marketing and research-backed positioning. The market increasingly favors multifunctional formulations combining relaxation, immunity enhancement, cognitive support, and metabolic benefits, strengthening overall application diversification and consumer retention rates.

Distribution Channel Insights

Online retail leads distribution with 38% market share, propelled by direct-to-consumer platforms, subscription-based delivery models, cross-border e-commerce expansion, and data-driven digital marketing strategies. The leading segment driver is the rapid digitalization of consumer purchasing behavior combined with broader product accessibility and competitive pricing transparency. Pharmacies and drug stores are expanding their footprint as regulatory clarity improves and CBD gains credibility within mainstream healthcare frameworks. Specialty wellness stores contribute through curated product assortments, premium positioning, and experiential retail strategies that strengthen brand loyalty. Supermarkets and hypermarkets are gradually incorporating CBD offerings, enhancing product visibility and impulse purchasing opportunities. Social media engagement, influencer-driven campaigns, educational content marketing, and AI-powered recommendation systems are increasingly shaping purchase decisions, particularly among millennials and Gen Z consumers, thereby reinforcing omnichannel retail integration.

End-User Insights

Adults aged 18–40 represent the largest consumer group, accounting for approximately 41% of total demand. This dominance is driven by heightened health awareness, proactive stress management behavior, fitness engagement, and openness to alternative wellness solutions. The leading segment driver is lifestyle-oriented preventive healthcare adoption among younger consumers who actively seek natural supplements to support work-life balance and physical performance. The 41–60 age group follows closely, supported by rising preventive health spending, chronic condition management, and increasing disposable income. Seniors aged 60+ constitute a growing niche segment as awareness around non-psychoactive CBD benefits expands in areas such as joint health and sleep support. Professional athletes and fitness enthusiasts represent high-frequency repeat purchasers, particularly within sports recovery applications. Cross-border demand from North America and Europe continues to stimulate export-driven consumption patterns, encouraging international brand expansion and product standardization.

Explore more data points, trends and opportunities Download Free Sample Report

CBD Supplements Market Segmentations

By Product Type

- Oils & Tinctures

- Capsules & Softgels

- Gummies & Chewables

- Powders & Drink Mixes

- Topical Supplements

- Other Edible Formats

By Source Type

- Hemp-Derived CBD

- Marijuana-Derived CBD

By Application

- Sleep & Stress Management

- Pain Management Support

- General Wellness & Preventive Health

- Sports Recovery & Performance

- Women’s Health & Hormonal Balance

By End-User

- Adults (18–40 years)

- Middle-Aged Consumers (41–60 years)

- Seniors (60+ years)

- Professional Athletes & Active Lifestyle Consumers

By Distribution Channel

- Online Retail

- Pharmacies & Drug Stores

- Specialty Wellness Stores

- Supermarkets & Hypermarkets

- Direct-to-Consumer Subscription Channels

Regional Insights

North America

North America accounts for approximately 39% of the global CBD supplements market in 2025, led by the United States due to progressive legalization frameworks, advanced retail infrastructure, and strong consumer awareness regarding hemp-derived wellness products. Regional growth is driven by regulatory clarity at the federal and state levels, high e-commerce penetration, product innovation, and strong venture capital participation. Canada remains a key contributor with a well-regulated hemp ecosystem, structured licensing models, and widespread retail adoption. Pharmaceutical channel integration, growing acceptance of non-psychoactive supplements, and increasing R&D investments further strengthen North America’s leadership position.

Europe

Europe represents approximately 29% of the global market, with Germany, the United Kingdom, and Switzerland leading regional demand. Germany accounts for nearly 24% of Europe’s market share, benefiting from pharmacy channel integration, structured reimbursement frameworks, and regulatory clarity under novel food regulations. The United Kingdom emphasizes online retail expansion, private-label development, and product innovation. Regional growth drivers include harmonization of CBD standards across the European Union, eco-certification trends, rising consumer trust in plant-based wellness, and increasing investment in GMP-certified production facilities. Sustainability initiatives and traceability requirements further enhance product credibility and long-term market stability.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market with a projected CAGR exceeding 20%, driven by regulatory evolution, urbanization, and expanding middle-class populations. China, India, Japan, and Australia are central growth engines due to increasing health consciousness, digital commerce expansion, and premium wellness consumption trends. Regional growth is supported by government-backed hemp cultivation programs, research initiatives, and export-oriented manufacturing capabilities. Rising disposable incomes and growing acceptance of scientifically validated nutraceuticals are encouraging consumers to adopt premium CBD formulations. Expanding cross-border trade and improved product standardization are further accelerating regional market penetration.

Latin America

Latin America is emerging as a high-potential market, with Brazil and Mexico leading regional adoption. Growth drivers include gradual regulatory liberalization, increasing awareness of plant-based therapeutics, and rising healthcare expenditure among affluent urban consumers. Expanding import channels, strategic partnerships with North American manufacturers, and localized marketing campaigns are strengthening product availability. The region’s agricultural capabilities also position it as a potential future cultivation hub, supporting long-term supply chain development and export competitiveness.

Middle East & Africa

The Middle East & Africa region holds strategic importance within the global CBD value chain. Africa remains central to hemp cultivation supply due to favorable climatic conditions and cost-effective agricultural infrastructure. South Africa leads regional adoption with progressive regulatory developments and domestic retail expansion. In the Middle East, the United Arab Emirates and Saudi Arabia are witnessing growing premium product demand driven by high disposable incomes, expanding medical tourism, and international trade connectivity. Regional growth is further supported by infrastructure development, regulatory alignment with global standards, foreign direct investment, and awareness campaigns promoting non-psychoactive wellness supplements.

Key Players in the CBD Supplements Market

- Charlotte's Web Holdings

- CV Sciences

- Irwin Naturals

- Medterra CBD

- Elixinol Global

- Canopy Growth Corporation

- Aurora Cannabis

- Tilray Brands

- Endoca

- CBDfx

- Garden of Life

- Gaia Herbs

- Isodiol International

- HempFusion Wellness

- Green Roads