Cassava Flour Market Size

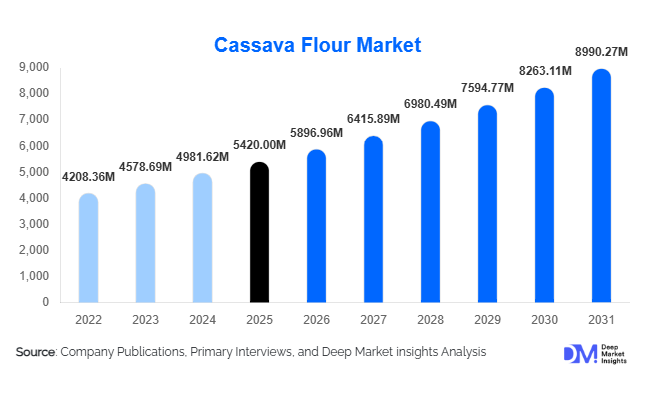

According to Deep Market Insights, the global cassava flour market size was valued at USD 5,420 million in 2025 and is projected to grow from USD 5,896.96 million in 2026 to reach USD 8,990.27 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The cassava flour market growth is primarily driven by the increasing demand for gluten-free food products, rising consumer preference for clean-label and natural ingredients, and expanding applications across food processing and industrial sectors such as adhesives and bioethanol.

Key Market Insights

- Gluten-free and allergen-free food demand is a major growth catalyst, positioning cassava flour as a preferred alternative to wheat-based products.

- Asia-Pacific and Africa dominate production, supported by abundant cassava cultivation and government-backed agricultural initiatives.

- Food processing applications account for the majority of demand, particularly in bakery, snacks, and processed foods.

- North America is the fastest-growing consumption market, driven by health-conscious consumers and premium product demand.

- Industrial applications such as bioethanol and biodegradable materials are expanding, creating new revenue streams for producers.

- Technological advancements in drying and processing methods are improving product consistency and shelf life.

What are the latest trends in the cassava flour market?

Rising Demand for Gluten-Free and Clean-Label Products

The growing global shift toward gluten-free and clean-label diets is significantly influencing cassava flour demand. Consumers are increasingly avoiding synthetic additives and allergens, driving food manufacturers to adopt cassava flour in bakery, snacks, and packaged foods. Its neutral taste and functional versatility make it ideal for product reformulation. This trend is particularly strong in North America and Europe, where awareness around celiac disease and food sensitivities is high. Additionally, organic cassava flour is gaining traction as consumers prioritize transparency and sustainability in food sourcing.

Expansion into Industrial and Bio-Based Applications

Cassava flour is increasingly being used beyond food applications, particularly in adhesives, textiles, paper, and bioethanol production. With global emphasis on sustainability and renewable resources, cassava-based inputs are gaining attention as eco-friendly alternatives to petroleum-based materials. Governments and private players are investing in bioeconomy initiatives, further boosting demand. This trend is expected to diversify market growth and reduce dependence on traditional food-based demand cycles.

What are the key drivers in the cassava flour market?

Growing Health Awareness and Dietary Shifts

Rising awareness of gluten intolerance, digestive health, and clean eating is driving consumers toward cassava flour as a healthier alternative. Its gluten-free and grain-free properties make it suitable for specialized diets such as paleo and vegan, significantly boosting demand across developed markets.

Expansion of Food Processing Industry

The rapid growth of the global food processing industry is increasing demand for versatile and cost-effective ingredients like cassava flour. Its ability to enhance texture, binding, and shelf stability makes it a preferred ingredient in processed foods, snacks, and ready-to-eat meals.

Government Support for Cassava Cultivation

Several countries, particularly in Africa and Asia, are promoting cassava cultivation through subsidies, infrastructure development, and export incentives. These initiatives are strengthening supply chains and encouraging large-scale processing, thereby supporting market growth.

What are the restraints for the global market?

Supply Chain and Raw Material Volatility

Cassava production is highly dependent on climatic conditions and agricultural practices, leading to inconsistent supply and price fluctuations. This volatility affects production planning and profit margins for manufacturers.

Competition from Alternative Flours

The market faces strong competition from other gluten-free flours such as almond, coconut, rice, and oat flour. These alternatives often have established consumer bases, particularly in premium segments, limiting cassava flour’s penetration in certain markets.

What are the key opportunities in the cassava flour industry?

Expansion in Emerging Markets

Emerging economies in Asia and Africa present significant opportunities due to rising urbanization, increasing disposable incomes, and growing food processing industries. Local production combined with export potential can drive market expansion.

Integration into Bioeconomy and Sustainable Materials

The growing focus on sustainability is opening opportunities for cassava flour in biodegradable materials and biofuels. Companies investing in bio-based solutions can leverage cassava as a renewable raw material.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5420 Million |

| Market Size in 2026 | USD 5896.96 Million |

| Market Size in 2031 | USD 8990.27 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Native cassava flour continues to dominate the global cassava flour market, accounting for approximately 62% of the total market share in 2025. This dominance is primarily attributed to its widespread applicability across both traditional and modern industrial uses. Native cassava flour is minimally processed, retaining its natural characteristics, which makes it highly suitable for use in staple foods, bakery items, and local cuisines across emerging economies. Its affordability, easy availability, and lower processing requirements significantly reduce production costs, making it the preferred choice for manufacturers and consumers alike. Additionally, the increasing demand for naturally sourced and clean-label ingredients further supports the growth of native cassava flour, especially among health-conscious consumers who seek minimally processed food alternatives.On the other hand, modified cassava flour is gaining notable traction and is expected to witness robust growth over the forecast period. This type of flour undergoes physical, chemical, or enzymatic modification to enhance its functional properties such as improved viscosity, stability, binding capacity, and resistance to temperature and pH variations. These enhanced characteristics make modified cassava flour particularly suitable for industrial applications, including processed foods, adhesives, textiles, and biodegradable materials. As industries increasingly shift toward sustainable and bio-based alternatives, the demand for modified cassava flour is projected to rise substantially. Furthermore, technological advancements in food processing and the need for improved product consistency are encouraging manufacturers to adopt modified variants.

Application Insights

The food and beverages segment leads the cassava flour market, holding nearly 65% of the total share in 2025. This segment’s dominance is driven by the growing demand for gluten-free products, which has transformed cassava flour into a key ingredient in bakery products, snacks, confectionery, and ready-to-eat meals. Its neutral taste, fine texture, and high carbohydrate content make it an ideal substitute for traditional flours such as wheat, particularly in regions where gluten-free diets are gaining popularity. Additionally, the increasing consumption of processed and convenience foods, especially in urban areas, has further fueled demand within this segment.The industrial segment is emerging as one of the fastest-growing application areas for cassava flour. Its use in adhesives, paper production, textiles, and bioethanol manufacturing is expanding due to its biodegradable nature and cost efficiency. As industries focus on reducing their environmental footprint, cassava flour-based products are gaining preference over synthetic alternatives. Government policies promoting bio-based industries and renewable resources are further supporting this growth.Animal feed applications also represent a steady and reliable segment within the market. Cassava flour serves as an energy-rich feed ingredient, particularly in regions with abundant cassava production. Its affordability and high carbohydrate content make it a suitable alternative to traditional feed components such as corn. With the expansion of livestock farming and increasing demand for meat and dairy products, the use of cassava flour in animal nutrition is expected to grow steadily.

Distribution Channel Insights

B2B distribution channels dominate the cassava flour market, accounting for approximately 68% of the total share. This dominance is largely due to the bulk procurement practices of food manufacturers, industrial processors, and large-scale buyers who require consistent supply and quality. Cassava flour is extensively used as a raw material in various industries, including food processing, textiles, and bio-based manufacturing, which necessitates large-volume transactions typically facilitated through B2B channels.The key driver for the B2B segment is the strong demand from food processing and industrial manufacturing sectors, where cassava flour is utilized as a primary ingredient. Long-term supply contracts, cost advantages in bulk purchasing, and streamlined logistics further strengthen the position of B2B distribution.Meanwhile, B2C channels are witnessing steady growth, driven by increasing household consumption and the rising popularity of cassava flour among health-conscious consumers. Supermarkets, hypermarkets, specialty stores, and online retail platforms are expanding their offerings to include cassava flour-based products. The growth of e-commerce, coupled with improved accessibility and product awareness, is significantly contributing to the expansion of B2C distribution. In developed markets, consumers are increasingly experimenting with alternative flours, further boosting retail sales.

End-Use Industry Insights

The food processing industry accounts for approximately 60% of the global cassava flour market, making it the largest end-use segment. The extensive use of cassava flour in bakery products, snacks, noodles, and packaged foods is a major factor driving this segment. Its functional properties, such as thickening, binding, and moisture retention, make it a valuable ingredient in large-scale food production. The rapid growth of the processed food industry, particularly in emerging economies, is further strengthening the demand for cassava flour.The leading driver for this segment is the expansion of the global food processing industry, supported by increasing urbanization, changing dietary habits, and rising disposable incomes. Consumers are increasingly opting for convenient and ready-to-eat food options, which in turn drives the demand for cassava flour as a key ingredient.Retail consumption is also growing rapidly, particularly in developed regions where consumers are actively seeking gluten-free and organic food alternatives. The availability of packaged cassava flour in retail stores and online platforms has made it more accessible to households, contributing to increased adoption.Industrial applications represent the fastest-growing end-use segment, driven by the rising demand for sustainable and eco-friendly materials. Cassava flour is increasingly being used in the production of biodegradable plastics, adhesives, and biofuels. As industries transition toward greener alternatives, the demand for cassava-based industrial products is expected to accelerate significantly.

Explore more data points, trends and opportunities Download Free Sample Report

Cassava Flour Market Segmentations

By Product Type

- Native Cassava Flour

- Modified Cassava Flour

- Physically Modified Cassava Flour

- Chemically Modified Cassava Flour

- Enzyme-Modified Cassava Flour

By Application

- Food & Beverages

- Animal Feed

- Industrial Applications

- Bioethanol Production

By Distribution Channel

- B2B

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global cassava flour market, accounting for around 38% in 2025. The region’s dominance is driven by countries such as Thailand, Indonesia, Vietnam, China, and India, which are both major producers and consumers of cassava. The strong agricultural base, favorable climatic conditions, and availability of low-cost labor contribute significantly to cassava cultivation and processing in the region.The key drivers for regional growth include government support for agricultural development, increasing investments in food processing infrastructure, and rising demand for gluten-free and convenience foods. Additionally, the expansion of export-oriented cassava processing industries in countries like Thailand and Vietnam is boosting regional market growth. Rapid urbanization and changing dietary patterns are also contributing to increased consumption of cassava-based products.

Africa

Africa accounts for approximately 30% of the global cassava flour market, with Nigeria being the largest producer of cassava worldwide. The region has a long-standing tradition of cassava cultivation and consumption, making it a staple food source for millions of peopleThe primary growth drivers in Africa include high domestic consumption, government initiatives to promote cassava as a food security crop, and increasing investments in processing infrastructure. Efforts to reduce post-harvest losses and improve value addition are enhancing the competitiveness of cassava flour in both domestic and international markets. Additionally, the rising demand for cassava-based exports is encouraging local producers to scale up production and improve quality standards.

North America

North America holds approximately 12% of the global cassava flour market, with the United States leading regional demand. The region is also the fastest-growing market, driven by shifting consumer preferences toward healthier and specialty food products.The key growth drivers include the increasing popularity of gluten-free diets, rising awareness about food allergies, and growing demand for organic and clean-label products. The expansion of health-conscious consumer segments and the availability of premium cassava flour products in retail and online channels are further supporting market growth. Additionally, innovation in food products and the introduction of cassava-based alternatives in mainstream markets are accelerating adoption.

Europe

Europe accounts for nearly 10% of the global market, with countries such as Germany, the United Kingdom, and France leading demand. The region is characterized by a strong preference for organic, natural, and sustainably sourced food products.The main drivers for growth in Europe include increasing consumer awareness regarding healthy eating habits, rising demand for gluten-free and allergen-free products, and stringent regulations promoting clean-label ingredients. The expansion of specialty food stores and the growing presence of cassava flour in bakery and snack products are also contributing to market growth. Additionally, sustainability initiatives and the demand for eco-friendly raw materials in industrial applications are supporting the adoption of cassava flour.

Latin America

Latin America represents around 7% of the global cassava flour market, with Brazil being the key contributor. The region benefits from favorable climatic conditions for cassava cultivation and a strong tradition of cassava-based food consumption.The key growth drivers include increasing domestic consumption, expansion of cassava processing industries, and rising export opportunities. Government initiatives to support agricultural development and improve processing capabilities are also contributing to market growth. Furthermore, the growing demand for cassava flour in both food and industrial applications is strengthening the region’s position in the global market.

Middle East & Africa

The Middle East & Africa region contributes approximately 3% to the global cassava flour market. Although relatively smaller in size, the market is experiencing steady growth due to increasing demand for alternative flours and expanding industrial applications.The primary growth drivers include rising food imports, increasing urbanization, and growing awareness of gluten-free diets in countries such as the UAE and South Africa. Additionally, the expansion of food service industries and the adoption of cassava flour in processed foods are supporting market growth. Industrial demand for bio-based materials is also emerging as a key factor driving the adoption of cassava flour in the region.

Key Players in the Cassava Flour Market

- Cargill Inc.

- Ingredion Incorporated

- Tate & Lyle PLC

- Archer Daniels Midland Company

- Grain Millers Inc.

- Thai Wah Public Company

- Psaltry International Ltd.

- Venus Starch Suppliers

- AGRANA Beteiligungs AG

- Roquette Frères

- Emsland Group

- Asia Modified Starch Co. Ltd.

- Universal Starch-Chem Allied Ltd.

- Banpong Tapioca Flour Industrial Co.

- PT Budi Starch & Sweetener