Cashew Nuts Market Size

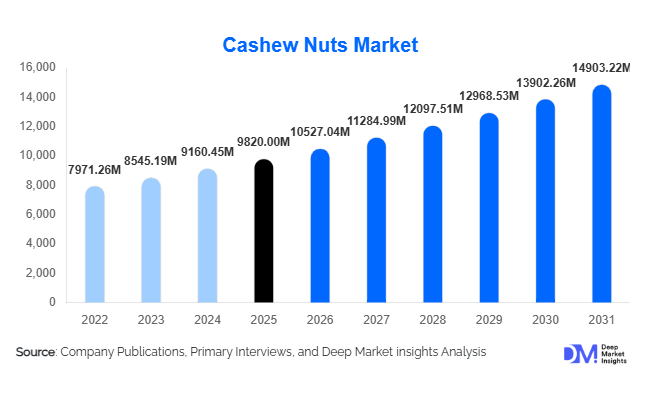

According to Deep Market Insights, the global cashew nuts market size was valued at USD 9,820 million in 2025 and is projected to grow from USD 10,527.04 million in 2026 to reach approximately USD 14,903.22 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The global cashew nuts market growth is supported by rising consumer demand for plant-based nutrition, increasing adoption of healthy snacking habits, and expanding applications of cashew-derived ingredients across food processing, dairy alternatives, and confectionery industries. Growing awareness regarding protein-rich diets and clean-label foods has positioned cashew nuts as a premium ingredient across developed and emerging economies.

Key Market Insights

- Healthy snacking trends are driving global demand, with roasted and flavored cashews gaining popularity among urban consumers.

- Asia-Pacific dominates production and consumption, led by India and Vietnam’s strong processing and export ecosystems.

- Plant-based dairy alternatives are accelerating cashew utilization in milk, cheese, and cream substitutes.

- Premiumization and flavored variants are increasing average selling prices globally.

- E-commerce and direct-to-consumer channels are expanding retail accessibility in emerging markets.

- Sustainability and ethical sourcing certifications are influencing purchasing decisions among Western consumers.

What are the latest trends in the cashew nuts market?

Shift Toward Plant-Based and Functional Foods

The global transition toward plant-based diets has significantly increased the adoption of cashew nuts as a versatile ingredient. Cashews are widely used in vegan dairy alternatives such as cashew milk, cheese spreads, and cream substitutes due to their creamy texture and neutral flavor profile. Food manufacturers are incorporating cashew-based formulations into ready-to-eat meals, protein snacks, and nutritional bars. Functional food innovation is further strengthening demand as cashews are naturally rich in healthy fats, magnesium, and antioxidants, appealing to health-conscious consumers worldwide.

Premiumization and Value-Added Processing

Value-added processing is reshaping market profitability. Instead of exporting raw kernels, processors increasingly focus on roasted, salted, flavored, organic, and coated cashew products. Premium offerings such as honey-roasted, peri-peri flavored, and chocolate-coated cashews are witnessing strong retail traction. Packaging innovation, including resealable pouches and single-serve snack packs, enhances convenience and shelf appeal. These trends are enabling manufacturers to achieve higher margins while differentiating products in competitive retail environments.

What are the key drivers in the cashew nuts market?

Rising Global Demand for Healthy Snacks

Consumers are increasingly replacing traditional fried snacks with nutrient-dense alternatives. Cashew nuts provide protein, unsaturated fats, and micronutrients, making them a preferred option in health-oriented diets. Urbanization and rising disposable incomes, particularly in Asia and North America, are accelerating packaged nut consumption. The snackification trend—frequent small meals replacing traditional eating patterns—continues to strengthen demand.

Expansion of Plant-Based Food Industry

The rapid growth of vegan and lactose-free food categories has positioned cashews as a key raw material for plant-based dairy manufacturers. Cashew-based beverages and spreads are expanding shelf space across supermarkets globally. Foodservice operators are also adopting cashew cream alternatives for culinary applications, further boosting industrial consumption.

Strong Export Ecosystems in Processing Countries

Countries such as Vietnam and India have invested heavily in processing automation, export infrastructure, and quality certifications. These developments have improved global supply reliability and supported trade expansion into Europe and North America, positively influencing overall market growth.

What are the restraints for the global market?

Volatility in Raw Cashew Nut Prices

Cashew production depends heavily on climatic conditions across West Africa and Southeast Asia. Weather variability and fluctuating farm yields often lead to raw material price instability, affecting processor margins and retail pricing consistency.

Labor-Intensive Processing Requirements

Cashew processing remains partially labor-intensive despite automation advancements. Shelling and grading processes require specialized handling, increasing operational costs. Labor shortages and wage inflation in processing hubs may constrain profitability for smaller processors.

What are the key opportunities in the cashew nuts industry?

Expansion in Emerging Consumer Markets

Rapid income growth across Southeast Asia, the Middle East, and Latin America is opening new consumption markets. Governments promoting nutritional awareness are encouraging nut consumption as part of balanced diets. Retail penetration in Tier-2 and Tier-3 cities offers significant growth potential for packaged cashew brands.

Technology Integration in Processing and Traceability

Automation technologies, AI-enabled sorting systems, and blockchain-based traceability solutions are improving processing efficiency and transparency. Buyers increasingly demand traceable supply chains ensuring ethical sourcing and sustainability compliance. Companies investing in smart processing facilities gain export advantages and premium pricing opportunities.

Growth of Cashew-Based Ingredients Industry

Cashew paste, butter, flour, and dairy substitutes represent high-growth ingredient categories. Food manufacturers increasingly source processed cashew derivatives rather than raw kernels, creating opportunities for vertical integration and value-added product innovation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9820 Million |

| Market Size in 2026 | USD 10527.04 Million |

| Market Size in 2031 | USD 14903.22 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global cashew nuts market demonstrates strong product diversification, with white whole cashew kernels (W320 grade) maintaining market leadership and accounting for nearly 38% of global market share in 2025. The dominance of this segment is primarily driven by its consistent size, visual appeal, and versatility across retail snack packaging, confectionery manufacturing, and premium gifting categories. Increasing consumer preference for visually uniform and high-quality nuts in organized retail continues to strengthen demand for W320 kernels. The leading segment growth is supported by expanding middle-class consumption, premiumization of packaged snacks, and strong export demand from developed markets seeking standardized grades for large-scale distribution.Roasted and flavored cashews represent the fastest-growing product category as manufacturers introduce innovative seasoning formats aligned with evolving consumer taste preferences. Rising urbanization, increasing disposable incomes, and demand for convenient ready-to-eat snacks are accelerating adoption across both developed and emerging markets. Additionally, higher retail margins associated with value-added flavored products are encouraging processors and brands to expand their product portfolios. Broken kernels continue to hold significant demand within bakery, confectionery, and processed food industries due to cost efficiency, ease of incorporation into recipes, and suitability for bulk industrial procurement, ensuring stable long-term utilization within food manufacturing supply chains.

Application Insights

Snacking applications dominate the global cashew nuts market, accounting for approximately 46% share of total demand in 2025. The leadership of this segment is driven by the global shift toward healthier snack alternatives, increasing on-the-go consumption patterns, and growing awareness of protein-rich plant-based foods. Cashews are increasingly positioned as premium functional snacks due to their nutritional profile, including healthy fats, minerals, and plant protein content. Expansion of branded snack portfolios, innovative packaging formats, and retail penetration in emerging economies further reinforce segment leadership.Confectionery and bakery applications represent the second-largest demand segment, benefiting from rising consumption of premium desserts, chocolates, and artisanal baked goods worldwide. Cashews are widely used as inclusions, toppings, and fillings due to their texture and flavor compatibility with high-value products. Meanwhile, dairy alternatives constitute the fastest-growing application segment as vegan and lactose-free dietary adoption accelerates globally. Increasing production of cashew milk, plant-based cheese, spreads, and sauces is significantly expanding industrial demand, supported by investments in alternative protein innovation and clean-label product development.

Distribution Channel Insights

Offline retail channels, including supermarkets, hypermarkets, and specialty food stores, account for nearly 52% of global sales, supported by strong consumer preference for physical product evaluation, impulse purchasing behavior, and established retail infrastructure. Large-format retail stores continue to dominate in developing markets where organized retail expansion enhances product visibility and accessibility. Promotional pricing strategies, in-store sampling, and private-label product offerings further strengthen offline channel performance.However, online retail is emerging as the fastest-expanding distribution channel, driven by the rapid growth of e-commerce ecosystems and digital grocery platforms. Subscription-based snack delivery services, direct-to-consumer brand strategies, and health-focused online marketplaces are improving consumer access to premium and specialty cashew products. Digital platforms also enable transparency regarding sourcing, certifications, and nutritional benefits, which increasingly influence purchasing decisions among health-conscious consumers.

End-Use Industry Insights

The food processing industry remains the dominant end-use sector, contributing nearly 58% of global demand. The leading segment growth is driven by rapid expansion in plant-based food manufacturing, increased incorporation of nuts into functional foods, and rising global demand for clean-label ingredients. Cashews serve as a key raw material in snack bars, dairy alternatives, confectionery fillings, and ready-to-eat meal formulations, making them essential to modern food innovation trends.Foodservice demand is also expanding steadily as restaurants, quick-service chains, and premium dining establishments incorporate cashew-based sauces, vegan curries, and dairy substitutes into menus. Growth in international cuisines and fusion dining concepts further supports adoption. Additionally, export-driven demand remains a critical industry driver, with large volumes of processed cashews shipped from Asia to Europe and North America, where consumption growth significantly exceeds domestic production capacity. This global trade dependency reinforces processing investments in producing regions.

Explore more data points, trends and opportunities Download Free Sample Report

Cashew Nuts Market Segmentations

By Product Type

- White Whole Cashew Kernels

- Roasted & Flavored Cashews

- Broken Cashew Kernels

- Cashew-Based Ingredients

By Application

- Snacking

- Confectionery & Bakery

- Dairy Alternatives

- Food Processing & Culinary Applications

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & E-commerce

- Foodservice & HoReCa Distribution

- Wholesale & Bulk Industrial Supply

Regional Insights

Asia-Pacific

Asia-Pacific leads the global cashew nuts market with approximately 41% market share in 2025, supported by its dual role as both the largest processing hub and a rapidly expanding consumption market. India and Vietnam dominate global processing and exports due to established supply chains, skilled labor availability, and government-backed processing infrastructure development. Regional growth is driven by increasing domestic consumption, rising disposable income levels, expansion of organized retail, and strong cultural integration of cashews into traditional sweets and cuisine. China’s market expansion is fueled by premium snacking trends, growing e-commerce penetration, and rising demand for nutritious packaged foods. Government initiatives supporting agricultural value addition and export competitiveness further strengthen Asia-Pacific’s leadership position.

North America

North America accounts for nearly 22% market share, led by the United States where plant-based dietary adoption and health-focused snacking habits significantly drive import demand. Regional growth is supported by increasing consumer awareness of nutritional benefits, expansion of vegan food categories, and strong demand for organic and sustainably sourced cashews. Innovation in flavored snacks, protein-rich foods, and dairy alternatives continues to expand product applications. Retail consolidation, advanced cold-chain logistics, and strong private-label penetration also contribute to steady market expansion across the region.

Europe

Europe represents a mature yet steadily growing market led by Germany, the United Kingdom, France, and the Netherlands. Regional growth is primarily driven by stringent ethical sourcing standards, sustainability certifications, and increasing consumer preference for plant-based diets. The expansion of vegan confectionery, dairy-free alternatives, and premium snack products is strengthening demand. Additionally, rising regulatory emphasis on traceability and fair-trade sourcing encourages long-term supplier partnerships with producing nations, ensuring consistent import flows and market stability.

Middle East & Africa

The Middle East & Africa region presents a unique market structure combining strong consumption growth with dominant raw material production. Rising disposable incomes, tourism expansion, and premium snack consumption trends in countries such as the UAE and Saudi Arabia are supporting regional demand growth. Meanwhile, West Africa remains the world’s largest raw cashew producing region, including Ivory Coast and Nigeria, supplying significant volumes to global processors. Investments in local processing capabilities, government initiatives promoting agricultural exports, and infrastructure development aimed at reducing raw nut exports are expected to enhance regional value addition and economic diversification.

Latin America

Latin America shows steady market expansion led by Brazil, which serves as both a major producer and consumer within the region. Regional growth is supported by increasing health awareness, expanding modern retail networks, and rising adoption of nutritious snack options. Countries such as Mexico and Chile are witnessing growing demand driven by urbanization, higher disposable income levels, and evolving dietary preferences favoring plant-based ingredients. Development of regional food processing industries and export opportunities further supports long-term market growth.

Key Players in the Cashew Nuts Market

- Olam Group

- ofI (Olam Food Ingredients)

- Vietnam National Cashew Corporation (VINACAS members)

- John B. Sanfilippo & Son Inc.

- Blue Diamond Growers

- Hershey Company (snacking nuts division)

- Mariani Nut Company

- Sunbeam Foods

- Intersnack Group

- Royal Nut Company

- Besana Group

- Germack Pistachio Company

- Nutty Bavarian

- Wonderful Pistachios & Almonds

- Planters (Hormel Foods)