Cashew Nut Shell Oil Market Size

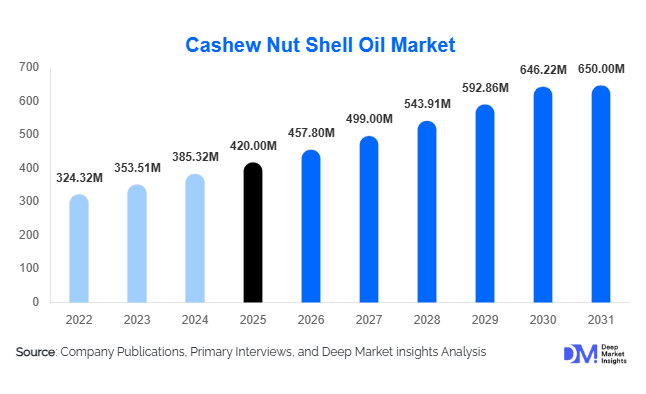

According to Deep Market Insights, the global cashew nut shell oil (CNSL) market size was valued at USD 420 million in 2026 and is projected to grow from USD 457.8 million in 2027 to reach USD 650 million by 2031, expanding at a CAGR of 9.0% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for bio-based chemicals, rising adoption of sustainable phenolic resins, and expanding applications in automotive friction materials, coatings, and industrial adhesives. Growing emphasis on circular economy practices and agro-waste valorization is further strengthening the market outlook globally.

Key Market Insights

- CNSL is gaining strong traction as a renewable substitute for petrochemical phenols, particularly in resin and coating applications.

- Automotive friction materials dominate end-use demand, driven by rising vehicle production and EV adoption.

- Asia-Pacific leads global production and consumption, supported by strong cashew processing industries in India and Vietnam.

- Europe is rapidly adopting bio-based chemicals due to strict environmental regulations and sustainability targets.

- Technological advancements in CNSL refining and chemical modification are improving product quality and expanding application scope.

What are the latest trends in the CNSL market?

Shift Toward Bio-Based Phenolic Resins

The market is witnessing a strong shift toward bio-based phenolic resins derived from CNSL as industries move away from petroleum-based phenol formaldehyde systems. This trend is especially strong in automotive, construction, and marine coatings, where environmental compliance and performance efficiency are critical. Manufacturers are investing in advanced polymerization techniques to enhance thermal stability, adhesion, and chemical resistance of CNSL-based resins. This transition is accelerating demand across both developed and emerging economies.

Expansion of High-Performance Friction Materials

CNSL is increasingly being used in brake pads and clutch facings due to its excellent heat resistance and friction stability. With global vehicle production exceeding 90 million units annually, demand for durable and low-toxicity friction materials is rising. The growth of electric vehicles is further boosting demand for advanced braking systems that rely on CNSL-based resins for consistent performance under high thermal stress conditions.

What are the key drivers in the CNSL market?

Rising Demand for Sustainable Industrial Feedstocks

The global push toward sustainable chemicals is a major driver of the CNSL market. Industries are increasingly replacing petroleum-based phenols with CNSL-derived alternatives to meet ESG targets and regulatory requirements. This shift is particularly strong in Europe and North America, where green chemistry adoption is accelerating across adhesives, coatings, and resin manufacturing sectors.

Growth in Automotive and Industrial Applications

The automotive sector remains the largest consumer of CNSL-based derivatives, particularly in brake linings, clutch facings, and friction materials. Increasing vehicle production and the expansion of EV manufacturing are driving demand for high-performance, thermally stable materials. Industrial applications such as epoxy modifiers and corrosion-resistant coatings are also contributing significantly to market growth.

Expansion of Cashew Processing in Emerging Economies

Countries such as India, Vietnam, and Ivory Coast are expanding cashew nut processing capacities, ensuring stable raw material availability for CNSL extraction. Government support for agro-processing industries and export-oriented production is strengthening supply chains and improving global market accessibility.

What are the restraints for the global market?

Raw Material Dependency and Supply Volatility

CNSL production is directly dependent on cashew nut shell availability, which fluctuates due to seasonal harvesting patterns, climate variability, and agricultural output changes. This creates price instability and supply uncertainty, affecting long-term planning for manufacturers.

High Processing Complexity and Limited Awareness

The extraction and refining of CNSL require advanced chemical processing capabilities, including distillation and catalytic modification. Limited awareness among small and mid-scale industries, particularly in developing regions, restricts wider adoption and slows market penetration.

What are the key opportunities in the CNSL industry?

Growth of Circular Economy and Agro-Waste Utilization

CNSL is derived from cashew nut shells, which are an agricultural byproduct. Increasing focus on waste-to-value models is creating strong opportunities for investment in extraction facilities. Governments are supporting agro-industrial valorization programs, particularly in India and Southeast Asia, promoting sustainable industrial ecosystems.

Expansion into EV-Compatible Materials

The rapid growth of electric vehicles is opening new opportunities for CNSL-based friction materials and composites. These materials provide thermal stability and reduced environmental impact, making them suitable for next-generation braking systems and lightweight automotive components.

Increasing Demand for Bio-Based Construction Materials

CNSL-based resins and coatings are gaining traction in construction due to their durability, water resistance, and eco-friendly properties. Infrastructure development in emerging economies is expected to significantly boost demand for CNSL-derived adhesives and protective coatings.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 420 Million |

| Market Size in 2026 | USD 457.8 Million |

| Market Size in 2031 | USD 650 Million |

| CAGR | 9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global Cashew Nut Shell Liquid (CNSL) market is primarily segmented into distilled CNSL, technical CNSL, and raw CNSL, each serving distinct industrial applications based on purity levels, chemical composition, and performance characteristics. Distilled CNSL dominates the global landscape with an estimated market share of approximately 38% in 2025. This dominance is largely attributed to its high purity, controlled phenolic content, and superior performance in advanced chemical formulations. Distilled CNSL is extensively utilized in high-performance resin systems, specialty coatings, and friction materials where consistency, thermal stability, and chemical resistance are critical. The growing demand for lightweight and high-durability materials in automotive manufacturing and construction composites has significantly strengthened the adoption of distilled CNSL. Furthermore, its increasing use as a sustainable alternative to petroleum-derived phenols is reinforcing its position in environmentally conscious manufacturing ecosystems.Raw CNSL, while less refined, continues to serve niche and low-cost industrial applications. It is primarily used in basic chemical processing and lower-grade resin production where high purity is not a strict requirement. However, its market share is gradually declining as industries shift toward refined and performance-oriented derivatives. The overall product evolution within the CNSL market is strongly influenced by sustainability trends, regulatory pressure to reduce petrochemical dependency, and rising performance standards across end-use industries.

Application Insights

The application landscape of the CNSL market is diverse, with resins and coatings emerging as the dominant segment, accounting for nearly 34% of global demand. This dominance is driven by the increasing use of CNSL-derived phenolic resins as eco-friendly substitutes for conventional petrochemical resins. These bio-based resins are widely valued for their excellent adhesion properties, thermal stability, and resistance to water and chemicals. The rapid expansion of green construction practices and sustainable infrastructure development has significantly contributed to the rising demand for CNSL-based coatings in industrial flooring, protective marine coatings, and corrosion-resistant surface treatments.In addition, adhesives and surfactants form an important application category, where CNSL derivatives are used to improve bonding strength, flexibility, and chemical resistance. Polymer modification is another rapidly growing application area, particularly in specialty plastics and composite materials used in aerospace, electronics, and construction industries. The increasing emphasis on renewable raw materials and circular economy principles is further expanding CNSL usage across industrial chemistry applications, making it a strategically important bio-based feedstock in modern manufacturing ecosystems.

End-Use Industry Insights

The automotive industry is the largest end-use sector for CNSL, accounting for approximately 29% of total consumption. This dominance is driven by the widespread use of CNSL-based friction materials in brake systems, clutch assemblies, and other high-stress automotive components. The growing global automotive production, coupled with the rapid transition toward electric and hybrid vehicles, is significantly reshaping material requirements. CNSL-based materials are increasingly preferred due to their ability to deliver high thermal resistance, reduced noise, and enhanced durability, making them suitable for both conventional and EV platforms. Additionally, sustainability goals within the automotive sector are accelerating the replacement of synthetic phenolic resins with bio-based alternatives such as CNSL derivatives.Industrial manufacturing and chemical processing industries also constitute significant end-use segments. CNSL derivatives are widely used in the production of specialty chemicals, surfactants, and polymer additives. Their chemical versatility and compatibility with various formulations make them valuable in multiple industrial processes. The shift toward bio-based chemical production is further reinforcing CNSL demand, particularly in regions with strong sustainability regulations and green chemistry initiatives.

Distribution Channel Insights

The CNSL market is predominantly driven by direct B2B sales channels, which account for nearly 72% of global distribution. This dominance is primarily due to the industrial nature of CNSL consumption, where bulk procurement agreements are established between manufacturers and large-scale end-users. Direct sourcing enables better price negotiation, consistent supply chains, and customized product formulations tailored to specific industrial requirements. Chemical manufacturers and processing companies prefer direct procurement to ensure quality control and supply stability, particularly for high-performance applications in automotive and coatings industries.Distributors and specialty chemical suppliers play a supporting role, particularly in fragmented regional markets where smaller manufacturers and end-users rely on intermediaries for procurement. These channels are essential in expanding market reach, especially in developing economies where direct manufacturer access may be limited. Additionally, the rise of digital procurement platforms is gradually transforming distribution dynamics by improving pricing transparency, reducing transaction costs, and enabling more efficient supplier-buyer interactions. This digital shift is expected to further streamline CNSL supply chains over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Cashew Nut Shell Oil Market Segmentations

By Product Type

- Raw Cashew Nut Shell Oil

- Technical Cashew Nut Shell Oil

- Distilled Cashew Nut Shell Oil

- Modified / Hydrogenated CNSL Derivatives

- Cardanol-Rich Fraction

- Cardol-Based Specialty Derivatives

By Application

- Resins & Phenolic Resins

- Coatings & Surface Protection

- Friction Materials

- Adhesives & Sealants

- Surfactants & Detergents

- Polymer Modification & Additives

- Industrial Lubricants

By End-Use Industry

- Automotive & Transportation

- Construction & Infrastructure

- Marine & Offshore

- Chemical & Petrochemical Industry

- Electrical & Electronics

- Industrial Manufacturing

By Distribution Channel

- Direct B2B Sales

- Industrial Chemical Distributors

- Specialty Chemical Suppliers

- Online Industrial Procurement Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global CNSL market with an estimated share of approximately 45% in 2025, making it the most influential regional market. The region’s leadership is primarily driven by strong cashew production and processing capabilities, particularly in India, Vietnam, and Indonesia. India remains a key global hub for CNSL extraction and export due to its well-established cashew processing industry and cost-effective labor force. Vietnam and Indonesia are rapidly expanding their processing capacities, supported by favorable agricultural conditions and growing investments in agro-based industries. The primary growth drivers in Asia-Pacific include abundant raw material availability, expanding chemical manufacturing infrastructure, and increasing demand from automotive and construction sectors. Additionally, rising industrialization, government support for bio-based industries, and the presence of large-scale export-oriented production facilities further strengthen regional dominance.

North America

North America accounts for approximately 25% of the global CNSL market, supported by strong demand from automotive manufacturing, industrial coatings, and adhesive production sectors. The United States is the largest importer and consumer of CNSL-based derivatives, driven by its advanced industrial base and growing emphasis on sustainable materials. The key growth driver in this region is the rapid shift toward environmentally friendly and bio-based chemical solutions, particularly in response to stringent environmental regulations and corporate sustainability commitments. The automotive sector plays a critical role, with increasing adoption of CNSL-based friction materials in both traditional and electric vehicles. Additionally, technological advancements in polymer chemistry and coatings formulation are supporting the integration of CNSL derivatives into high-performance industrial applications.

Europe

Europe holds around 20% of the global CNSL market share, with major contributions from Germany, France, and the United Kingdom. The region’s growth is strongly influenced by strict environmental regulations, carbon neutrality targets, and aggressive adoption of bio-based chemicals. The European Union’s sustainability frameworks are encouraging industries to reduce reliance on petroleum-derived feedstocks, thereby increasing demand for renewable alternatives such as CNSL. Key growth drivers include the expansion of green construction practices, increasing adoption of eco-friendly automotive materials, and strong research and development activities in bio-based polymer technologies. Germany leads industrial adoption due to its advanced automotive sector, while France and the UK are witnessing growing applications in coatings and specialty chemicals.

Middle East & Africa

The Middle East & Africa region holds nearly 5% of the global CNSL market, with growth primarily concentrated in South Africa and the United Arab Emirates. The construction and industrial development sectors are the primary drivers of demand in this region, supported by ongoing infrastructure expansion and urban development projects. The UAE is increasingly investing in sustainable construction materials as part of its long-term diversification strategies, while South Africa serves as both a consumer and sourcing hub for agricultural raw materials. Additionally, Africa plays an important role in raw cashew production, contributing indirectly to global CNSL supply chains. Rising industrialization and gradual adoption of bio-based materials are expected to support steady market growth in the region.

Latin America

Latin America accounts for approximately 5% of the global CNSL market, with Brazil emerging as the dominant country in the region. The growth of the automotive and coatings industries in Brazil is a major factor driving CNSL demand. The region benefits from strong agricultural output and increasing integration into global bio-based chemical supply chains. Brazil’s expanding industrial base and growing focus on sustainable material production are key drivers of CNSL adoption. Additionally, increasing foreign investment in chemical manufacturing and rising awareness of eco-friendly industrial solutions are expected to further support market growth in the coming years. The region’s proximity to raw material sources also provides a strategic advantage in supporting global CNSL trade dynamics.

Key Players in the CNSL Market

- Cardolite Corporation

- Emerald Performance Materials

- Senesel

- Satya Cashew Chemicals

- Palmer International

- Gokul Agro Resources

- Cireson Chemicals

- Golden Cashew Products

- LignoStar BioChem

- Cashew Chem India