Cappuccino Market Size

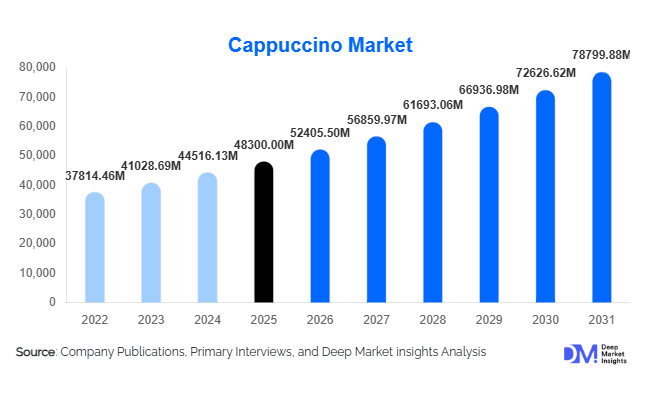

According to Deep Market Insights, the global cappuccino market size was valued at USD 48,300 million in 2025 and is projected to grow from USD 52,405.50 million in 2026 to reach USD 78,799.88 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The cappuccino market growth is primarily driven by the rapid expansion of global café culture, increasing demand for premium coffee experiences, and the rising popularity of convenient formats such as ready-to-drink (RTD) beverages and capsule-based systems.

Key Market Insights

- Ready-to-drink cappuccino formats are witnessing strong growth, driven by convenience and on-the-go consumption trends among urban consumers.

- Premiumization and flavor innovation are reshaping the market, with increasing demand for gourmet and customized cappuccino variants.

- North America dominates the global market, supported by high per capita coffee consumption and established café chains.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, western lifestyle adoption, and rising disposable incomes.

- Commercial end-use, particularly cafés and coffee chains, leads demand, accounting for a majority share of global consumption.

- Technological advancements in coffee machines and capsule systems are enhancing product accessibility and consumer experience.

What are the latest trends in the cappuccino market?

Rising Popularity of Ready-to-Drink (RTD) Cappuccino

The demand for RTD cappuccino is rapidly increasing due to changing consumer lifestyles and the need for convenience. These products are widely available in supermarkets, convenience stores, and vending machines, making them highly accessible. Manufacturers are focusing on improving shelf life, enhancing taste profiles, and introducing low-sugar and plant-based variants to cater to health-conscious consumers. Sustainable packaging solutions such as recyclable bottles and cans are also being adopted, aligning with global environmental trends.

Growth of Capsule-Based Coffee Systems

Single-serve coffee machines and capsule-based systems are gaining traction, especially in developed markets. These systems offer consistent quality and convenience, making them popular among households and offices. Companies are investing in proprietary capsule technologies and expanding their flavor portfolios to strengthen brand loyalty. This trend is also supported by the increasing penetration of smart kitchen appliances and connected coffee machines.

What are the key drivers in the cappuccino market?

Expansion of Global Café Culture

The rapid growth of café chains and specialty coffee outlets worldwide is significantly driving cappuccino consumption. Urban consumers increasingly view coffee shops as social and professional spaces, leading to higher demand for premium beverages such as cappuccino. This trend is particularly prominent in emerging markets where café culture is still developing.

Increasing Demand for Convenience Products

Consumers are shifting toward easy-to-prepare and portable beverage options. Instant cappuccino mixes and RTD beverages cater to this demand, enabling consumption at home, in offices, and on the move. The growing work-from-home culture has further accelerated demand for convenient coffee solutions.

What are the restraints for the global market?

Volatility in Raw Material Prices

Fluctuations in coffee bean and dairy prices due to climate change and supply chain disruptions pose a challenge for manufacturers. These cost variations can impact profit margins and pricing strategies, especially for premium products.

Competition from Alternative Beverages

The increasing popularity of alternatives such as cold brew coffee, energy drinks, and plant-based beverages is creating competitive pressure. Health-conscious consumers are exploring low-caffeine or caffeine-free options, which may limit cappuccino demand growth in certain segments.

What are the key opportunities in the cappuccino industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, the Middle East, and Latin America present significant growth opportunities. Rising middle-class populations, urbanization, and exposure to Western consumption patterns are driving demand. Localized product offerings and competitive pricing strategies can help companies capture these markets effectively.

Innovation in Flavors and Functional Ingredients

There is growing demand for flavored and functional cappuccino products, including options with added protein, vitamins, and plant-based ingredients. Companies investing in product innovation can differentiate themselves and attract health-conscious consumers, expanding their market reach.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48300.00 Million |

| Market Size in 2026 | USD 52405.50 Million |

| Market Size in 2031 | USD 78799.88 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product landscape of the global cappuccino market is increasingly shaped by evolving consumer lifestyles, technological integration in beverage preparation, and a strong inclination toward convenience-oriented formats. Ready-to-drink (RTD) cappuccino continues to lead the product segment, accounting for approximately 34% of the global market share in 2025. This leadership position is primarily driven by the accelerating pace of urbanization and the growing preference for on-the-go consumption among working professionals and younger demographics. RTD cappuccino products are widely available across convenience stores, supermarkets, and vending channels, making them highly accessible. Additionally, innovations in packaging, such as resealable bottles and eco-friendly materials, further enhance their appeal. The leading driver for this segment remains the convergence of convenience and premiumization, as manufacturers increasingly introduce barista-style formulations with enhanced flavors and functional ingredients such as protein and plant-based milk alternatives.Capsule-based cappuccino is emerging as a rapidly expanding niche, particularly in developed markets characterized by higher disposable incomes and technological adoption. This segment is supported by the rising installation of single-serve coffee machines in households and offices, enabling consumers to replicate café-quality beverages at home. The leading driver for capsule-based cappuccino is the increasing consumer demand for customization and consistency in taste, coupled with the convenience of automated brewing systems. Sustainability concerns related to capsule waste are prompting manufacturers to invest in recyclable and biodegradable solutions, which is expected to further support long-term growth.

Application (End-Use) Insights

The application spectrum of the cappuccino market reflects a strong dominance of commercial consumption, with the segment contributing nearly 60% of total demand. This dominance is largely attributed to the global proliferation of cafés, quick-service restaurants, and premium hospitality establishments. The leading driver for the commercial segment is the continuous expansion of international and regional coffee chains, which are capitalizing on evolving consumer preferences for premium coffee experiences. The integration of digital ordering systems, loyalty programs, and experiential store formats further enhances customer engagement and repeat consumption. Additionally, tourism growth and urban foot traffic significantly contribute to the sustained demand for cappuccino in commercial settings.Offices and co-working spaces are emerging as significant consumption hubs, reflecting broader changes in workplace culture. Employers are increasingly investing in high-quality beverage solutions to enhance employee satisfaction and productivity. This trend is particularly pronounced in urban centers, where hybrid work models and flexible office environments are gaining traction. As a result, the demand for automated coffee machines and bulk cappuccino supplies is steadily increasing within this segment.

Distribution Channel Insights

The distribution landscape of the cappuccino market is characterized by the continued dominance of traditional retail formats alongside the rapid expansion of digital commerce. Supermarkets and hypermarkets account for the largest share, representing approximately 41% of global sales. Their leadership is driven by extensive shelf space, diverse product assortments, and strong consumer trust. The leading driver for this channel is the ability to offer competitive pricing through bulk purchasing and promotional campaigns, which attract a broad customer base. In-store visibility and product sampling initiatives further influence purchasing decisions, particularly for new product launches.Specialty coffee shops and foodservice outlets continue to play a critical role in shaping consumer perceptions and brand positioning. These channels provide an experiential platform where consumers can explore premium cappuccino offerings and innovative flavor profiles. The influence of skilled baristas and personalized service enhances the perceived value of products, encouraging consumers to replicate similar experiences through retail purchases.

Explore more data points, trends and opportunities Download Free Sample Report

Cappuccino Market Segmentations

By Product Type

- Traditional Cappuccino

- Instant Cappuccino Mix

- Ready-to-Drink (RTD) Cappuccino

- Capsule/Pod-Based Cappuccino

By Form

- Powdered

- Liquid

By Flavor Type

- Unflavored/Classic

- Flavored

By Caffeine Content

- Regular

- Decaffeinated

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail/E-commerce

- Specialty Coffee Shops

- Foodservice (HoReCa)

Regional Insights

North America

North America holds around 32% of the global cappuccino market share in 2025, with the United States serving as the primary growth engine. The region’s mature coffee culture, characterized by high per capita consumption and strong brand presence, underpins its dominant position. One of the key drivers of regional growth is the increasing consumer preference for premium and specialty coffee beverages, including organic and sustainably sourced cappuccino. The widespread adoption of advanced coffee machines in households and workplaces further accelerates demand. Additionally, the strong presence of established coffee chains and continuous product innovation, such as plant-based and functional cappuccino variants, contribute significantly to market expansion. The region also benefits from well-developed retail infrastructure and high digital penetration, which supports both offline and online distribution channels.

Europe

Europe accounts for approximately 29% of the global cappuccino market, with countries such as Germany, Italy, and France playing pivotal roles. The region’s deep-rooted coffee heritage and cultural affinity for espresso-based beverages provide a stable foundation for sustained demand. A major driver of growth in Europe is the increasing trend toward premiumization and artisanal coffee consumption, where consumers seek high-quality ingredients and authentic preparation methods. The expansion of private-label offerings in supermarkets, coupled with strong café networks, further supports market growth. Additionally, rising awareness of sustainability and ethical sourcing is influencing purchasing decisions, prompting brands to adopt environmentally friendly practices. The growing popularity of at-home coffee consumption, supported by advanced brewing equipment, is also contributing to the steady expansion of the cappuccino market across the region.

Asia-Pacific

Asia-Pacific represents about 24% of the global market and stands as the fastest-growing region, with a compound annual growth rate exceeding 10%. Rapid urbanization, rising disposable incomes, and the westernization of dietary habits are key factors driving demand in countries such as China, India, and Japan. One of the most significant growth drivers in the region is the expanding middle-class population, which is increasingly inclined toward premium lifestyle products, including specialty coffee beverages. The proliferation of international coffee chains and the emergence of local café brands are further accelerating market penetration. Additionally, the increasing influence of social media and digital marketing is shaping consumer preferences and driving brand awareness. The growth of e-commerce platforms and mobile payment systems also facilitates easy access to a wide range of cappuccino products, supporting overall market expansion.

Latin America

Latin America holds nearly 7% of the global cappuccino market, with Brazil and Mexico leading regional demand. The region’s strong coffee production base provides a natural advantage, enabling cost-effective sourcing and fostering a deep cultural connection to coffee consumption. A key driver of growth is the gradual shift from traditional coffee consumption to value-added beverages such as cappuccino, driven by changing consumer preferences and increasing urbanization. The expansion of retail infrastructure and the growing presence of international coffee chains are also contributing to market development. Additionally, rising disposable incomes and the influence of global consumption trends are encouraging consumers to explore premium coffee formats, supporting steady growth in the cappuccino segment.

Middle East & Africa

The Middle East & Africa region accounts for around 8% of the global cappuccino market, with the United Arab Emirates and Saudi Arabia emerging as key markets. The region is characterized by a rapidly evolving coffee culture, driven by high consumer spending and a strong preference for premium experiences. One of the primary drivers of growth is the expansion of upscale cafés and international coffee chains, which are introducing diverse cappuccino offerings to a growing customer base. Additionally, increasing urbanization and a young population demographic are contributing to higher consumption levels. The rising popularity of specialty coffee and the influence of global lifestyle trends further support market expansion. In Africa, improving economic conditions and increasing awareness of modern coffee products are gradually driving demand, particularly in urban centers.

Key Players in the Cappuccino Market

- Nestlé S.A.

- Starbucks Corporation

- JDE Peet’s

- The Kraft Heinz Company

- Tata Consumer Products

- Luigi Lavazza S.p.A.

- Tchibo GmbH

- Strauss Group Ltd.

- Dunkin’ Brands Group

- McCafé (McDonald’s)

- illycaffè S.p.A.

- Jacobs Douwe Egberts

- Peet’s Coffee

- Gloria Jean’s Coffees

- Costa Coffee