Canned Fruits and Vegetables Market Size

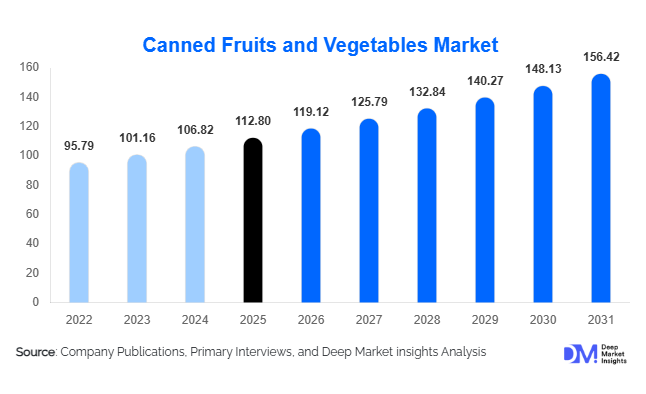

According to Deep Market Insights, the global canned fruits and vegetables market size was valued at USD 112.8 billion in 2025 and is projected to grow from USD 119.12 billion in 2026 to reach USD 156.42 billion by 2031, expanding at a CAGR of 5.6% during the forecast period (2026–2031). The market is witnessing stable expansion driven by rising urbanization, increasing demand for long-shelf-life food products, and the growing adoption of convenient packaged foods across both developed and emerging economies. Changing consumer lifestyles, particularly among working populations, have accelerated demand for ready-to-use fruits and vegetables that reduce preparation time while maintaining nutritional value.

Growth is further supported by advancements in canning technologies that improve flavor retention, texture preservation, and nutrient stability. Manufacturers are increasingly introducing low-sodium, preservative-free, and organic canned offerings to align with health-conscious consumption trends. Expansion of organized retail, e-commerce grocery platforms, and foodservice chains has strengthened global distribution networks, allowing canned products to penetrate new regional markets. Emerging economies in Asia-Pacific, Latin America, and the Middle East are experiencing rising consumption due to growing middle-class populations and improved cold-chain and logistics infrastructure. Additionally, export-oriented production hubs continue to expand capacity to meet global demand fluctuations caused by seasonal agricultural output variability.

Key Market Insights

- Convenience-driven consumption remains the primary growth driver as consumers seek time-saving food solutions.

- Vegetable-based canned products dominate due to higher everyday usage in household cooking and foodservice applications.

- Asia-Pacific is the fastest-growing regional market, supported by urban population expansion and rising disposable income.

- Private-label brands are gaining share through competitive pricing strategies in supermarkets and hypermarkets.

- Sustainability initiatives, including recyclable packaging and reduced food waste, are reshaping product innovation.

- Foodservice and institutional demand continues to expand globally, supporting bulk packaging growth.

What are the latest trends in the canned fruits and vegetables market?

Health-Oriented Reformulation and Clean Label Products

Consumers increasingly prefer minimally processed foods with transparent ingredient labeling. Manufacturers are responding by reducing sodium, eliminating artificial preservatives, and introducing BPA-free packaging. Organic canned fruits and vegetables are gaining traction, particularly in North America and Europe, where health-conscious consumers prioritize nutritional integrity alongside convenience. Functional product positioning, including vitamin-enriched canned vegetables and fruit packed in natural juices rather than syrup, is becoming a major differentiator. Clean-label innovation has also enabled premium pricing strategies, improving profitability across branded product portfolios.

Automation and Smart Processing Technologies

Food processing facilities are adopting automation, AI-driven quality inspection, and advanced sterilization systems to enhance efficiency and reduce waste. Smart canning technologies allow precise temperature control, improving shelf life while maintaining taste and texture. Robotics integration in sorting, peeling, and packaging operations is reducing labor dependency and increasing throughput capacity. Digital traceability systems are also emerging, enabling manufacturers to track agricultural sourcing and ensure compliance with food safety regulations across export markets.

What are the key drivers in the canned fruits and vegetables market?

Growing Demand for Convenience Foods

Urban lifestyles and dual-income households have increased reliance on ready-to-cook and ready-to-eat food ingredients. Canned fruits and vegetables offer extended shelf life without refrigeration, making them attractive for modern consumers and retailers alike. Rising demand from quick-service restaurants and institutional kitchens further strengthens consumption volumes.

Food Waste Reduction and Supply Stability

Canning allows surplus agricultural production to be preserved and distributed year-round, minimizing food waste. Governments and food processors increasingly promote preserved foods as part of sustainable food systems. This capability stabilizes supply chains during seasonal fluctuations and climate-related crop disruptions.

Expansion of Organized Retail and E-Commerce Grocery Channels

Modern retail formats and online grocery platforms have significantly improved product accessibility. Subscription grocery models and bulk purchasing options encourage household stocking behavior, boosting recurring demand for canned staples globally.

What are the restraints for the global market?

Perception of Fresh Food Superiority

Some consumers perceive canned foods as less nutritious compared to fresh or frozen alternatives. Despite technological improvements, this perception continues to influence purchasing behavior in premium urban markets.

Volatility in Raw Material Prices

Fluctuations in agricultural commodity prices, steel packaging costs, and energy expenses impact production margins. Climate variability affecting crop yields also introduces supply instability for processors.

What are the key opportunities in the canned fruits and vegetables industry?

Emerging Market Consumption Expansion

Rapid urbanization across India, Southeast Asia, Africa, and Latin America presents strong opportunities for market penetration. Rising disposable incomes and modern retail development enable wider adoption of packaged food products. Localization strategies, including region-specific flavors and smaller pack sizes, are helping manufacturers enter price-sensitive markets.

Foodservice and Institutional Supply Growth

Hotels, restaurants, airlines, and catering services increasingly rely on canned ingredients for consistency and reduced preparation time. Bulk packaging formats and long shelf life make canned vegetables particularly attractive for commercial kitchens, creating long-term B2B demand stability.

Sustainable Packaging and Circular Economy Integration

Metal cans are among the most recyclable packaging formats globally. Investments in lightweight cans, recycled aluminum usage, and eco-label certifications create opportunities for brands to align with sustainability goals while improving consumer perception.

Product Type Insights

The global canned food market continues to be strongly anchored by canned vegetables, which accounted for nearly 62% of the total market share in 2025. The dominance of this segment is primarily driven by its role as a daily-use cooking ingredient across both developed and emerging economies. Canned vegetables such as tomatoes, corn, peas, beans, and mixed vegetable assortments offer long shelf life, price stability, and year-round availability independent of seasonal agricultural cycles. The leading driver for this segment is the increasing consumer preference for convenient yet nutritionally preserved food solutions that reduce preparation time while maintaining cooking flexibility. Urban households, dual-income families, and time-constrained consumers increasingly rely on canned vegetables as pantry essentials, while foodservice operators benefit from standardized quality and reduced food wastage. Furthermore, rising volatility in fresh produce supply caused by climate variability has strengthened reliance on preserved vegetable formats, reinforcing long-term demand stability.Canned fruits represent approximately 38% of the global market share, supported by expanding consumption in desserts, bakery fillings, breakfast applications, and snack categories. Growth in this segment is increasingly shaped by premiumization trends, including fruit mixes packed in natural juices, low-sugar variants, and clean-label offerings targeting health-conscious consumers. The leading driver for canned fruits is the rapid expansion of ready-to-eat and on-the-go consumption patterns, particularly among younger demographics seeking convenient yet perceived healthier snack alternatives. Demand is also strengthened by food manufacturers incorporating canned fruits into yogurts, cereals, confectionery, and frozen dessert products, thereby expanding industrial usage alongside household consumption.

Form Insights

Whole and cut vegetables emerged as the leading product form, accounting for nearly 44% of the global market share in 2025. Their dominance is primarily attributed to versatility across cuisines and meal formats, allowing consumers and professional kitchens to integrate products into soups, curries, salads, and ready meals without extensive preparation. The key driver supporting this segment is culinary adaptability combined with minimal processing perception, which aligns with consumer demand for foods perceived as closer to fresh ingredients while still offering convenience benefits.Purees and pastes constitute the second-largest segment, with tomato paste serving as a critical input for sauces, processed meals, and packaged food manufacturing worldwide. The expansion of processed and packaged food industries across emerging markets continues to accelerate industrial demand for concentrated canned ingredients. Meanwhile, ready-meal integrated canned mixes are witnessing accelerated adoption as modern consumers increasingly favor simplified meal preparation solutions. These formats align with growing demand for semi-prepared cooking bases, particularly in urban markets where cooking time reduction remains a primary purchasing motivation.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global distribution channels, contributing nearly 48% of total market share in 2025. Their leadership is supported by strong private-label product penetration, competitive pricing strategies, and consumer preference for bulk purchasing during routine grocery shopping. The leading growth driver for this channel is organized retail expansion combined with improved shelf visibility and promotional bundling strategies that encourage higher purchase volumes. Large-format retailers also provide extensive product assortments, enabling consumers to compare brands, packaging formats, and price tiers in a single shopping environment.Online retail is emerging as the fastest-growing distribution channel, expanding at a CAGR exceeding 8%, fueled by rapid digital grocery adoption, subscription delivery services, and improvements in last-mile logistics. The growth of e-commerce platforms has significantly enhanced accessibility to bulk canned products, particularly in urban areas where convenience-driven purchasing behaviors are accelerating. Increasing smartphone penetration and integration of quick-commerce delivery models further strengthen online channel expansion, reshaping traditional grocery purchasing patterns.

Packaging Type Insights

Metal cans remain the dominant packaging format, accounting for approximately 71% of total packaging usage globally. Their continued leadership is driven by durability, superior barrier protection against light and oxygen, extended shelf stability, and high recyclability rates. The leading driver for metal packaging adoption is its efficiency in preserving nutritional value while enabling large-scale transportation and storage with minimal spoilage risk. Advances in lightweight can manufacturing and BPA-free lining technologies are further improving consumer perception and sustainability credentials.Glass jars occupy a smaller yet increasingly premium market segment, particularly within organic, specialty, and gourmet fruit categories. Glass packaging appeals strongly to consumers prioritizing transparency, product visibility, and chemical-free storage perceptions. Growth in this segment is supported by premium branding strategies and rising demand for clean-label and environmentally conscious packaging solutions, particularly in developed markets.

End-Use Insights

Household consumption continues to dominate global demand, contributing nearly 58% of total market volume. The primary driver for this segment is the increasing need for long-lasting pantry staples that support meal planning flexibility and reduce food waste. Economic uncertainty in several regions has also reinforced consumer preference for shelf-stable foods that offer affordability and storage convenience.The foodservice sector represents the fastest-growing end-use category, driven by the rapid expansion of quick-service restaurants, cloud kitchens, catering businesses, and institutional dining operations. Canned vegetables enable consistent portion control, predictable costs, and operational efficiency, making them highly attractive for commercial kitchens. Institutional buyers including schools, hospitals, airlines, and corporate cafeterias increasingly rely on canned ingredients to ensure supply reliability and food safety compliance.Export-oriented demand is also expanding steadily as major agricultural processing countries supply canned foods to regions with limited domestic production capacity. The continued growth of the global processed food industry, valued at over USD 3 trillion, indirectly strengthens demand for canned ingredients used as foundational inputs across multiple food manufacturing categories.

| By Product Type | By Packaging Type | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 28% of the global market share in 2025, led primarily by the United States, where canned vegetables remain deeply integrated into household consumption habits. Regional growth is driven by strong consumer acceptance of shelf-stable foods, high penetration of organized retail networks, and widespread adoption of private-label brands offering competitive pricing. Increasing demand for convenient meal solutions among working populations continues to sustain consumption levels. Additionally, advanced food processing infrastructure and technological innovation in packaging and preservation support product quality improvements, reinforcing consumer trust. Canada contributes stable demand supported by mature retail ecosystems and increasing preference for sustainable and recyclable packaging formats.

Europe

Europe holds nearly 24% of global market share, supported by well-established processed food industries across Germany, France, Italy, and Spain. Regional growth is driven by rising demand for organic and premium canned products aligned with health-conscious consumption trends. Stringent environmental regulations encouraging recyclable materials and reduced food waste further strengthen canned food adoption due to its long shelf life and sustainability advantages. The expansion of private-label premium offerings and increasing consumer interest in Mediterranean cooking styles also contribute to steady regional demand growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 7%. Growth is primarily driven by rapid urbanization, rising disposable incomes, and the expansion of modern retail infrastructure across China, India, and Southeast Asia. China dominates regional production and export activities due to large-scale agricultural output and competitive processing capabilities. India and Southeast Asian markets are witnessing accelerated adoption as changing lifestyles increase demand for convenient cooking solutions. Japan maintains stable premium demand characterized by high quality standards and preference for portion-controlled, convenience-oriented food products. The leading regional driver remains dietary modernization combined with increasing participation of women in the workforce, which boosts demand for time-saving food formats.

Latin America

Latin America demonstrates steady market expansion led by Brazil and Mexico, where growing middle-class populations and urbanization are accelerating packaged food consumption. Regional growth is driven by improving retail infrastructure and rising consumer awareness regarding food preservation benefits. Chile and Peru play significant roles in global trade through strong export-oriented fruit canning industries supported by favorable agricultural conditions and international demand for tropical fruit products. Currency fluctuations and seasonal supply variability in fresh produce further encourage adoption of shelf-stable alternatives.

Middle East & Africa

The Middle East & Africa region is experiencing increasing demand driven primarily by rising food imports and expanding urban populations. Limited domestic agricultural processing capacity in several countries increases reliance on imported canned foods to ensure food security and supply consistency. Saudi Arabia, the UAE, and South Africa represent key consumption markets supported by growing hospitality, tourism, and institutional catering sectors. Government-led food security initiatives and investments in distribution infrastructure are strengthening regional accessibility to processed foods. Additionally, harsh climatic conditions that restrict year-round fresh produce availability make canned foods a practical and reliable dietary component across the region.

Investment & CapEx Trends

Investment activity across the global canned food industry is accelerating as governments and private stakeholders prioritize food security, supply chain resilience, and reduction of post-harvest losses. National initiatives focused on agricultural modernization, including programs similar to “Make in India” and large-scale food processing upgrades in China, are encouraging expansion of domestic processing capacity. Private-sector capital expenditure is increasingly directed toward automation technologies, robotics-enabled sorting systems, energy-efficient sterilization processes, and advanced packaging innovations aimed at extending shelf life while reducing environmental impact.

Expansion of integrated processing hubs combining storage, processing, and logistics capabilities is becoming a major investment trend across emerging markets. Companies are also investing in cold-chain connectivity and digital inventory management systems to enhance operational efficiency and minimize waste. Sustainability-focused investments, including recyclable materials, lightweight packaging, and reduced energy consumption manufacturing processes, are expected to shape future competitive differentiation as regulatory pressure and consumer awareness continue to increase globally.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Canned Fruits and Vegetables Market

- Dole Food Company

- Del Monte Foods, Inc.

- Conagra Brands, Inc.

- Bonduelle Group

- Greenyard NV

- Kraft Heinz Company

- General Mills, Inc.

- Campbell Soup Company

- B&G Foods, Inc.

- Seneca Foods Corporation

- JBT Marel Corporation

- Princes Group

- Orkla ASA

- Ayam Brand

- La Doria S.p.A.