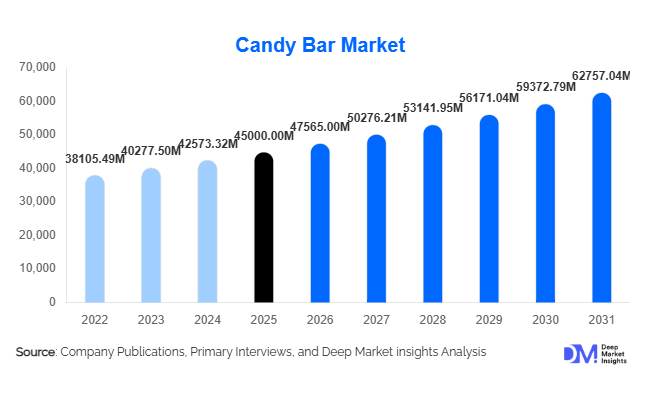

Global Candy Bar Market Size

According to Deep Market Insights, the global candy bar market size was valued at USD 45,000 million in 2026 and is projected to grow from USD 47,565.00 million in 2027 to reach USD 62,757.04 million by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The candy bar market growth is primarily driven by rising global snacking culture, increasing demand for on-the-go energy foods, and continuous innovation in indulgent as well as functional confectionery products. Expanding urban lifestyles, premiumization of chocolate-based products, and the rapid penetration of organized retail and e-commerce channels are further strengthening global demand.

Key Market Insights

- Chocolate-based candy bars dominate global consumption, supported by strong brand loyalty and widespread consumer preference for indulgent snacks.

- Milk chocolate formulations lead the ingredient segment, accounting for the largest share due to universal taste acceptance across age groups.

- Supermarkets and hypermarkets remain the primary distribution channel, driven by impulse purchases and high shelf visibility.

- Asia-Pacific is emerging as the fastest-growing region, supported by urbanization, rising disposable incomes, and expanding retail infrastructure.

- Health-oriented candy bar innovation is accelerating, with rising demand for protein bars and low-sugar confectionery options.

- Premium and functional candy bars are gaining traction, particularly in developed economies where consumers seek both indulgence and nutrition.

global candy bar market latest trends

Health-Oriented and Functional Candy Bar Innovation

The industry is witnessing a strong shift toward healthier formulations, including protein-enriched, low-sugar, and fiber-fortified candy bars. Manufacturers are reformulating traditional recipes using alternative sweeteners such as stevia and maltitol. This trend is driven by increasing consumer awareness of obesity, diabetes, and overall dietary health. Functional candy bars positioned as energy boosters or meal replacements are gaining traction, particularly among fitness-conscious consumers and working professionals.

Premiumization and Flavor Diversification

Premium candy bars infused with exotic ingredients such as nuts, caramel blends, single-origin cocoa, and gourmet flavors are experiencing rising demand. Brands are focusing on limited-edition and seasonal offerings to enhance consumer engagement. Additionally, regional flavor adaptation strategies—such as spicy chocolate in Asia and fruit-infused variants in Latin America—are expanding market penetration and strengthening brand differentiation.

global market drivers

Rising Global Snacking Culture

Urban lifestyles and busy work schedules have significantly increased demand for convenient, on-the-go snacks. Candy bars serve as an accessible indulgence product, making them a preferred choice among working professionals and students. This behavioral shift is particularly strong in North America and Europe, where snacking frequency is higher and brand loyalty is well established.

Product Innovation by Leading Manufacturers

Major confectionery players such as Mars Wrigley, Mondelez International, Nestlé, and Hershey are continuously investing in new product development. Innovations include reduced sugar formulations, protein-based candy bars, and plant-based ingredients. Seasonal and collaborative product launches are also strengthening brand visibility and driving repeat purchases across global markets.

Expansion of Modern Retail and E-commerce Channels

The rapid expansion of supermarkets, convenience stores, and online retail platforms is improving product accessibility. E-commerce is emerging as a high-growth channel, enabling personalized offerings, subscription snack boxes, and promotional pricing strategies. This is particularly impactful in emerging markets such as India, China, and Southeast Asia.

global market restraints

Rising Health Concerns and Regulatory Pressure

Increasing awareness regarding sugar consumption, obesity, and lifestyle-related diseases is negatively impacting traditional candy bar consumption. Governments in several regions are enforcing stricter labeling regulations and sugar taxes, forcing manufacturers to reformulate products and adjust pricing strategies.

Volatility in Raw Material Prices

Fluctuations in cocoa, sugar, dairy, and nut prices significantly impact production costs and profit margins. Climate-related disruptions in cocoa-producing regions further increase supply chain uncertainty, leading to pricing instability across global markets.

global candy bar industry key opportunities

Expansion of Health-Focused Product Lines

There is a significant opportunity for manufacturers to expand into functional and health-oriented candy bars. Products enriched with protein, vitamins, and natural ingredients are gaining popularity among fitness-conscious consumers. This segment is expected to expand the addressable consumer base beyond traditional confectionery buyers.

Rapid Growth of E-Commerce and D2C Models

Digital sales channels are transforming the candy bar market landscape. Direct-to-consumer platforms, subscription snack boxes, and online grocery platforms are enabling brands to improve margins and build stronger customer relationships. Emerging markets are witnessing particularly strong adoption of mobile-based shopping platforms.

Premiumization and Regional Flavor Localization

Rising disposable incomes and evolving taste preferences are driving demand for premium and localized flavor profiles. Companies that successfully adapt products to regional tastes while maintaining premium positioning are likely to capture higher margins and stronger brand loyalty across global markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 45000.00 Million |

| Market Size in 2026 | USD 47565.00 Million |

| Market Size in 2031 | USD 62757.04 Million |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chocolate-based candy bars continue to dominate the global market, accounting for approximately 42% share in 2025, supported by strong consumer inclination toward indulgent confectionery products and the long-standing dominance of established global brands. The sustained demand is primarily driven by emotional consumption patterns, widespread availability across retail formats, and continuous product innovation in flavors, fillings, and premium textures. In addition, aggressive marketing campaigns and seasonal launches further reinforce category leadership across developed and emerging economies.Nut-based and caramel-infused bars are witnessing increasing traction as consumers show a growing preference for texture-rich and multi-layered snacking experiences. The rising influence of premiumization and experiential eating is encouraging manufacturers to experiment with inclusions such as roasted nuts, sea salt caramel, and blended fillings. Protein and functional candy bars represent the fastest-growing category, largely fueled by the global fitness movement, increasing gym participation, and rising demand for convenient on-the-go nutrition. The expansion of health-conscious lifestyles and demand for high-protein alternatives to traditional snacks is significantly accelerating this segment’s growth. Meanwhile, wafer-based bars remain widely consumed in price-sensitive markets due to their affordability, light texture, and strong mass-market appeal. Sugar-free and reduced-sugar variants are also gaining consistent momentum, supported by rising awareness of lifestyle diseases, diabetic-friendly dietary needs, and tightening regulatory frameworks on sugar consumption across multiple regions.

Ingredient Type Insights

Milk chocolate-based formulations lead the ingredient segment with approximately 45% share, primarily driven by their smooth taste profile, universal consumer acceptance, and versatility across both mass-market and premium candy bar offerings. Their dominance is further reinforced by strong supply chain integration and widespread use in branded confectionery products across global markets. Dark chocolate variants are steadily expanding due to increasing consumer awareness regarding health benefits, antioxidant properties, and lower sugar content, making them particularly attractive among urban and health-conscious consumers.White chocolate maintains niche but stable demand, primarily concentrated in premium, seasonal, and dessert-inspired product offerings where sweetness and creaminess are key differentiators. Compound chocolate continues to be widely used in economy segments due to its cost efficiency, shelf stability, and ease of manufacturing, making it a preferred choice in emerging markets and value-oriented product lines. Meanwhile, sugar-free and alternative sweetener-based formulations are gaining strong momentum, supported by rising diabetic populations, fitness-driven consumption patterns, and increasing regulatory emphasis on sugar reduction. The ingredient landscape is increasingly shaped by innovation in natural sweeteners, clean-label trends, and consumer demand for healthier indulgence without compromising taste.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape with approximately 38% market share, driven by strong product visibility, extensive shelf space, and high impulse purchasing behavior. These retail formats continue to benefit from organized retail expansion, promotional bundling strategies, and strategic in-store placement of confectionery products near checkout zones. Convenience stores also remain a critical channel, particularly for on-the-go consumption, urban lifestyles, and high-frequency small-ticket purchases.Online retail is emerging as the fastest-growing distribution channel, supported by rapid digital penetration, increasing smartphone usage, attractive discounting strategies, and the expansion of subscription-based snack delivery models. The convenience of doorstep delivery and access to a wider variety of premium and niche products is significantly reshaping consumer purchasing behavior. Specialty confectionery stores cater to premium and artisanal demand, offering curated product assortments and experiential retail environments that enhance brand engagement. Vending machines continue to play a supportive role in impulse-driven consumption, particularly in transit hubs, corporate offices, and educational institutions, where accessibility and immediacy drive purchasing decisions.

Explore more data points, trends and opportunities Download Free Sample Report

Candy Bar Market Segmentations

By Product Type

- Chocolate-Based Candy Bars

- Wafer-Based Candy Bars

- Nut-Based Candy Bars

- Caramel & Nougat-Based Bars

- Protein & Functional Candy Bars

- Sugar-Free / Reduced-Sugar Candy Bars

By Ingredient Type

- Milk Chocolate-Based Bars

- Dark Chocolate-Based Bars

- White Chocolate-Based Bars

- Compound Chocolate-Based Bars

- Sugar-Free Sweetener-Based Formulations

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce Platforms

- Specialty Confectionery Stores

- Vending Machines & Impulse Retail Points

By Price Tier

- Economy Segment

- Mid-Range Segment

- Premium Segment

- Super-Premium / Artisanal Segment

Regional Insights

North America

North America accounts for approximately 28% of global demand, with the United States contributing nearly 20% of total consumption. The region’s strong performance is driven by high per capita confectionery intake, deep brand penetration, and a mature retail ecosystem that supports continuous product innovation. Growth is further supported by rising demand for premium chocolate bars, functional and protein-enriched snacks, and seasonal product launches tied to holidays and gifting occasions. Additionally, increasing consumer preference for indulgent yet functional snacking, along with strong e-commerce adoption and subscription snack services, is reinforcing regional market expansion.

Europe

Europe holds around 25% market share, with key contributions from Germany, the United Kingdom, and France. The region’s growth is strongly influenced by consumer preference for premium, artisanal, and ethically sourced confectionery products. Rising demand for sustainable cocoa sourcing, fair-trade certification, and environmentally responsible packaging is shaping product development strategies across manufacturers. Health-conscious consumption patterns, including reduced sugar intake and organic ingredient adoption, are also driving innovation in dark chocolate and functional candy bar categories. Strong regulatory frameworks and well-established confectionery traditions further support stable market growth across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for approximately 34% market share, driven by rapid urbanization, rising disposable incomes, and expanding modern retail infrastructure across China, India, and Japan. A young and increasingly urban population is fueling demand for convenient, affordable, and western-style confectionery products. The region is also experiencing strong influence from global brands and evolving lifestyle habits that favor packaged snacks. Growth is further supported by aggressive retail expansion, increasing penetration of e-commerce platforms, and rising demand for both mass-market and premium candy bars across tier-1 and tier-2 cities.

Latin America

Latin America contributes approximately 8% share, with Brazil and Mexico leading regional consumption. Market growth is supported by rising urbanization, improving economic conditions, and increasing availability of affordable confectionery products. Consumers in the region show strong preference for value-driven offerings and locally adapted flavors, which enhances product acceptance. Expansion of modern retail channels, coupled with growing penetration of international brands, is further supporting steady market development across urban centers.

Middle East & Africa

The Middle East & Africa region accounts for around 5% share, characterized by strong import dependency and increasing demand in GCC countries. Growth in this region is driven by rising disposable incomes, a strong gifting culture, and high consumption of premium confectionery products among affluent consumers in the UAE and Saudi Arabia. Seasonal demand peaks during festivals such as Ramadan and Eid also significantly boost sales of candy bars and chocolate products. Additionally, the expanding tourism sector and growing retail modernization efforts are enhancing product accessibility and brand visibility across key markets.

Key Players in the Global Candy Bar Market

- Mars Wrigley

- Mondelez International

- Nestlé

- Hershey

- Ferrero Group

- Lindt & Sprüngli

- Meiji Holdings

- Perfetti Van Melle

- Haribo

- Pladis Global

- Yildiz Holding

- August Storck

- Tootsie Roll Industries

- Ezaki Glico

- Grupo Bimbo