Caffeine Alternatives Market Size

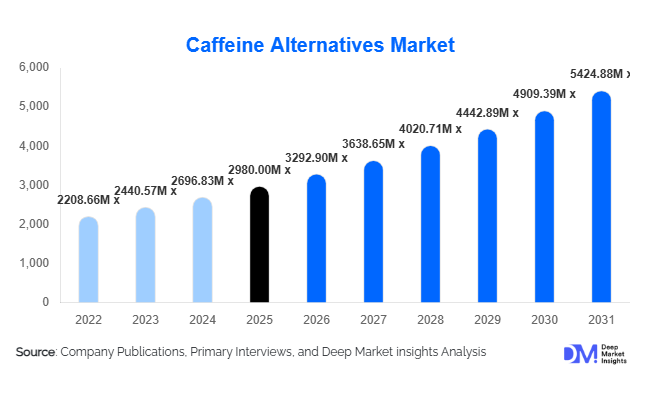

According to Deep Market Insights, the global caffeine alternatives market size was valued at USD 2,980 million in 2025 and is projected to grow from USD 3,292.90 million in 2026 to reach USD 5,424.88 million by 2031, expanding at a CAGR of 10.5% during the forecast period (2026–2031). The caffeine alternatives market growth is primarily driven by increasing consumer awareness regarding caffeine-related side effects, rising preference for clean-label and plant-based functional ingredients, and growing demand for sustained energy solutions without jitters or crashes. The market is transitioning from niche adaptogen-based beverages to mainstream retail acceptance across supermarkets, online platforms, and specialty wellness stores. Expanding innovation in mushroom-based formulations, amino acid blends, and herbal adaptogens is further strengthening product differentiation globally.

Key Market Insights

- Herbal and botanical extracts account for nearly 34% of the global market, driven by strong demand for ginseng and ashwagandha-based formulations.

- Ready-to-drink (RTD) beverages dominate with 38% share, reflecting consumer preference for convenience and on-the-go functional energy products.

- North America leads with approximately 38% market share in 2025, supported by high adoption of functional beverages and D2C wellness brands.

- Asia-Pacific is the fastest-growing region, expanding at over 12% CAGR due to rising nutraceutical demand in China and India.

- Online retail contributes nearly 29% of total revenue, driven by subscription-based wellness models and digital-first brands.

- The top five players collectively hold around 41% market share, indicating moderate fragmentation with strong innovation-led competition.

What are the latest trends in the caffeine alternatives market?

Rise of Adaptogen and Mushroom-Based Energy Solutions

Adaptogenic herbs and functional mushrooms such as lion’s mane, cordyceps, and reishi are rapidly gaining traction as sustainable caffeine substitutes. Consumers increasingly seek “calm focus” products that enhance cognitive performance without overstimulation. Clinical validation and improved extraction technologies are enhancing ingredient standardization and bioavailability, strengthening consumer trust. Mushroom-based coffee alternatives are particularly popular in North America and Europe, supported by premium positioning and strong digital marketing.

Premiumization and Clean-Label Positioning

Consumers are shifting toward clean-label, vegan-certified, and organic-certified products. Brands are emphasizing transparent sourcing, non-GMO claims, and sugar-free formulations. Premium pricing strategies—especially in RTD beverages and nutraceutical capsules—are enabling gross margins between 35–55%. Subscription-based sales models are increasing recurring revenue streams while reducing reliance on traditional retail distribution.

What are the key drivers in the caffeine alternatives market?

Growing Focus on Mental Wellness and Sleep Health

Rising awareness of anxiety, sleep disruption, and adrenal fatigue linked to high caffeine consumption is a major driver. Consumers are increasingly adopting non-stimulant alternatives such as L-theanine and B-vitamin blends to maintain productivity without impacting sleep cycles. The broader sleep supplement industry’s expansion is indirectly accelerating demand for caffeine-free energy products.

Expansion of Functional Beverage Industry

The global functional beverage sector is growing at approximately 9–10% annually, providing a strong foundation for caffeine alternatives. Beverage manufacturers are reformulating portfolios in response to regulatory scrutiny around high-caffeine energy drinks. This shift is opening retail shelf space for adaptogen-infused sparkling waters, herbal tonics, and nootropic blends.

What are the restraints for the global market?

High Ingredient and Production Costs

Standardized botanical extracts and mushroom cultivation involve higher production costs compared to synthetic caffeine. Organic certification and clinical validation further increase operational expenditure, limiting penetration in price-sensitive markets.

Limited Consumer Awareness in Emerging Economies

In developing regions where coffee and tea are culturally entrenched, awareness of adaptogens and mushroom-based alternatives remains relatively low. Educational marketing investments are necessary to accelerate adoption.

What are the key opportunities in the caffeine alternatives industry?

Corporate and Institutional Wellness Integration

Workplace wellness programs and university campuses are increasingly adopting stimulant-free focus beverages. Bulk procurement contracts from corporate clients create stable revenue channels and long-term growth opportunities.

Technological Advancements in Fermentation and Extraction

Precision fermentation and advanced botanical extraction technologies are improving ingredient consistency and scalability. Companies investing in proprietary blends with clinical backing can command premium pricing and differentiate in competitive retail environments.

Product Type Insights

Herbal and botanical extracts lead the market with 34% share of 2025 revenue, equivalent to over USD 1,010 million. Ginseng and ashwagandha dominate due to established consumer familiarity and cross-category adoption. Mushroom-based alternatives are the fastest-growing sub-segment, particularly lion’s mane and cordyceps, driven by cognitive enhancement claims. Amino acid-based solutions such as L-theanine blends are gaining popularity in nootropic formulations. Adaptogen blends combining multiple botanicals are increasingly used in RTD beverages to enhance perceived efficacy.

Application Insights

Functional beverages account for approximately 42% of total market demand, making them the largest application segment. Dietary supplements represent the second-largest segment, supported by capsule and powder formats. Sports nutrition applications are expanding at over 11% CAGR as athletes seek non-jitter performance enhancers. Emerging applications include military and tactical use, where sustained focus without overstimulation is critical.

Distribution Channel Insights

Online retail holds nearly 29% of global market share, fueled by D2C brands and subscription-based delivery models. Supermarkets and hypermarkets remain key channels for RTD beverages, particularly in North America and Europe. Specialty health stores and pharmacies maintain importance for nutraceutical capsules and premium adaptogen blends.

Consumer Demographic Insights

Millennials represent the largest consumer demographic, accounting for approximately 36% of global demand. This group prioritizes mental clarity, stress management, and clean-label products. Gen Z is the fastest-growing demographic, strongly influenced by social media marketing and wellness trends. Health-conscious seniors are emerging as a stable consumer base, particularly for sleep-supporting and anxiety-reducing formulations.

| By Product Type | By Form | By Distribution Channel | By End-Use Application | By Consumer Demographic |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America dominates the caffeine alternatives market with 38% share in 2025. The United States represents the largest national market, driven by strong functional beverage penetration and high online sales. Canada shows steady growth supported by regulatory clarity around natural health products.

Europe

Europe accounts for approximately 27% of global revenue, led by Germany, the U.K., and France. Germany is the largest European market due to its strong herbal supplement tradition. Clean-label regulations and high consumer awareness support market expansion.

Asia-Pacific

Asia-Pacific holds nearly 24% market share and is the fastest-growing region with over 12% CAGR. China leads in production and export of adaptogenic ingredients, while India shows strong domestic demand growth supported by Ayurvedic heritage. Japan demonstrates consistent demand for functional beverages.

Latin America

Latin America contributes around 5% of global revenue, with Brazil leading regional demand. Increasing urban wellness adoption is gradually expanding market penetration.

Middle East & Africa

The Middle East & Africa account for approximately 6% of global demand. The UAE leads regional consumption due to premium retail infrastructure and high disposable income.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Caffeine Alternatives Market

- Four Sigmatic

- Mud\Wtr

- Rasa

- Rebbl

- Kin Euphorics

- Gaia Herbs

- Himalaya Wellness

- Om Mushroom Superfood

- Laird Superfood

- Ancient Nutrition

- Sun Potion

- Neuro Drinks

- Peak and Valley

- H.V.M.N.

- Teatulia