Butter and Margarine Market Size

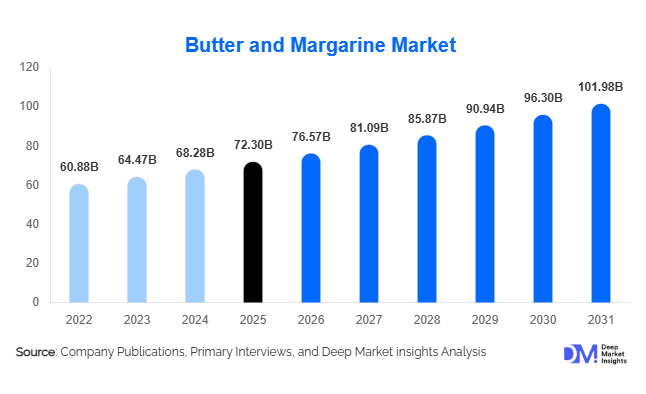

According to Deep Market Insights, the global butter and margarine market size was valued at USD 72.3 billion in 2025 and is projected to grow from USD 76.57 billion in 2026 to reach USD 101.98 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The butter and margarine market growth is primarily driven by rising bakery and confectionery consumption, increasing demand for premium dairy spreads, and growing adoption of plant-based and clean-label margarine products globally.

Key Market Insights

- Consumer preference is shifting toward premium and natural dairy fats, boosting demand for grass-fed, cultured, and organic butter products across developed markets.

- Plant-based and vegan margarine products are rapidly gaining popularity, supported by growing health consciousness, lactose intolerance awareness, and sustainability-focused purchasing behavior.

- Europe dominates the global butter and margarine market, driven by its strong dairy processing infrastructure, bakery industry expansion, and high per capita butter consumption.

- Asia-Pacific is the fastest-growing regional market, supported by rising urbanization, expanding foodservice sectors, and increasing consumption of western-style bakery products.

- Industrial bakery applications account for the largest share of demand, as butter and margarine remain essential ingredients in pastries, cakes, breads, cookies, and laminated dough products.

- Technological innovations in emulsification, shelf-life enhancement, and sustainable packaging are improving product quality and operational efficiency across the industry.

What are the latest trends in the butter and margarine market?

Premium and Artisanal Butter Demand Expanding Rapidly

The global butter market is increasingly moving toward premiumization as consumers prioritize natural ingredients, authentic flavors, and minimally processed dairy products. Premium categories such as grass-fed butter, cultured butter, organic butter, and specialty flavored butter are witnessing strong retail penetration across North America and Europe. Consumers perceive premium butter products as healthier and more authentic alternatives to heavily processed spreads, supporting higher pricing power for manufacturers. Retailers are also dedicating larger shelf spaces to imported European butter, gourmet spreads, and small-batch artisanal dairy products. Foodservice operators, luxury bakeries, and fine-dining restaurants are increasingly using premium butter variants to improve product quality and brand positioning.

Plant-Based Margarine Innovation Accelerating

Manufacturers are increasingly investing in plant-based margarine and dairy-free spread innovation to address changing dietary preferences and sustainability concerns. Margarine formulations using sunflower oil, olive oil, avocado oil, oat-based ingredients, and non-GMO vegetable oils are becoming increasingly popular among vegan and flexitarian consumers. Companies are also reformulating products to eliminate trans fats while improving texture, flavor, and nutritional value. Functional margarine products fortified with omega-3, vitamins, and heart-health ingredients are gaining traction in both retail and institutional foodservice channels. Digital labeling transparency, sustainable palm oil sourcing certifications, and recyclable packaging initiatives are also emerging as critical competitive differentiators within the plant-based segment.

What are the key drivers in the butter and margarine market?

Expansion of Global Bakery and Confectionery Industry

The rapid growth of the bakery and confectionery sector remains one of the strongest growth drivers for the butter and margarine market. Industrial bakeries rely heavily on butter and margarine for texture enhancement, flavor development, aeration, and shelf-life optimization in cakes, pastries, croissants, cookies, and breads. Rising urbanization, changing breakfast consumption habits, and increasing demand for convenience foods are supporting packaged bakery product sales globally. Emerging economies across Asia-Pacific and the Middle East are witnessing strong expansion of café chains, quick-service restaurants, and frozen bakery manufacturing, creating long-term industrial demand for butter and margarine products.

Growing Preference for Clean-Label and Natural Ingredients

Consumers are increasingly favoring clean-label food products containing recognizable and minimally processed ingredients. Butter has benefited significantly from changing consumer perceptions regarding dairy fats, with many consumers now viewing natural butter as a healthier alternative to artificial or highly processed fats. This trend is particularly strong in premium retail and gourmet food categories where organic, hormone-free, and grass-fed dairy products are achieving higher demand growth. Manufacturers are responding through transparency-focused labeling strategies, sustainable dairy sourcing, and premium product launches targeting health-conscious consumers.

What are the restraints for the global market?

Volatility in Dairy and Vegetable Oil Prices

Raw material price fluctuations remain a significant challenge for butter and margarine manufacturers globally. Butter production depends heavily on milk fat availability, while margarine production is closely linked to edible oil markets including palm oil, sunflower oil, soybean oil, and rapeseed oil. Climatic disruptions, livestock feed inflation, geopolitical tensions, and export restrictions frequently impact supply stability and production costs. These pricing fluctuations reduce manufacturer margins and increase retail pricing pressure, especially in price-sensitive developing markets.

Regulatory Pressure on Fat Content and Labeling

Governments and food safety authorities are increasingly implementing stricter regulations regarding saturated fats, trans fats, cholesterol disclosures, and processed food labeling. Margarine manufacturers face additional pressure to reformulate products while maintaining taste, texture, and shelf stability. Sustainability regulations concerning palm oil sourcing and carbon emissions are also increasing compliance costs across the industry. These regulatory challenges are particularly significant for smaller manufacturers with limited reformulation and certification capabilities.

What are the key opportunities in the butter and margarine industry?

Growth of Vegan and Functional Food Categories

The rapid expansion of vegan and plant-based food industries presents substantial opportunities for margarine manufacturers globally. Dairy-free spreads and functional margarine products are increasingly being incorporated into vegan bakery products, ready-to-eat meals, and healthy snack applications. Functional products fortified with omega-3 fatty acids, probiotics, vitamins, and cholesterol-lowering ingredients are also attracting health-conscious consumers seeking value-added nutritional benefits. Companies investing in clean-label plant-based formulations are expected to gain long-term competitive advantages in premium retail channels.

Industrial Bakery Expansion in Emerging Economies

Emerging economies such as China, India, Indonesia, Vietnam, Saudi Arabia, and the UAE are witnessing strong expansion in industrial bakery production and processed food manufacturing. Rising disposable income, urbanization, and westernized dietary preferences are increasing demand for breads, pastries, desserts, and convenience foods. Industrial bakeries require large-scale procurement of specialty butter and margarine products designed for laminated dough, puff pastry, confectionery fillings, and frozen bakery applications. Manufacturers expanding regional production facilities and foodservice partnerships within these high-growth economies are expected to benefit significantly from long-term demand expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 72.30 Billion |

| Market Size in 2026 | USD 76.57 Billion |

| Market Size in 2031 | USD 101.98 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global butter and margarine market demonstrates a highly diversified product landscape, driven by evolving dietary preferences, premiumization trends, innovation in fat-based formulations, and expanding food processing applications worldwide. Among all product categories, butter continues to dominate the global market and accounted for nearly 58% of total market value in 2025. The dominance of butter is strongly supported by increasing consumer preference for natural dairy ingredients, minimally processed foods, and premium culinary experiences. Consumers across developed economies increasingly perceive butter as a healthier and more authentic alternative to synthetic spreads, particularly as concerns surrounding artificial additives and trans fats continue to influence purchasing decisions. Growing consumer inclination toward traditional dairy products, combined with rising demand for gourmet bakery products and premium home cooking ingredients, continues to strengthen butter consumption globally.Butter blends and spreadable dairy products are gaining increasing popularity among consumers seeking a balance between taste, affordability, convenience, and improved nutritional characteristics. These blended products combine butter with vegetable oils to improve spreadability while reducing saturated fat content and retail prices. The category is particularly attractive among urban consumers and middle-income households seeking premium taste experiences at accessible price points. Continuous innovation in flavor profiles, texture enhancement, and functional ingredient integration is expected to further diversify the product landscape during the forecast period.

Application Insights

Bakery and confectionery applications continue to represent the largest application segment within the global butter and margarine market, accounting for approximately 36% of total global demand in 2025. The dominance of this segment is primarily driven by the essential functional role of butter and margarine in enhancing texture, moisture retention, flavor, mouthfeel, layering, and product consistency across a wide range of baked goods and desserts. The expanding global consumption of pastries, croissants, cakes, breads, cookies, biscuits, donuts, chocolates, and premium desserts continues to generate strong demand for high-quality bakery fats. Rapid growth in café culture, artisan bakery chains, and premium confectionery retail outlets is further supporting segment expansion globally.The industrial bakery sector remains one of the most important consumers of margarine products due to their operational efficiency and production stability in large-scale manufacturing environments. Laminated dough applications including puff pastries and croissants require specialized margarine formulations capable of maintaining structural integrity during repeated folding and baking processes. Meanwhile, butter continues to dominate premium bakery applications because of its superior flavor profile and consumer preference for authentic dairy ingredients. Rising consumer spending on indulgent bakery products and gourmet desserts across both developed and emerging economies continues to strengthen long-term market demand.Specialty applications including gourmet cooking, artisanal confectionery production, premium desserts, and luxury hospitality services are also supporting demand growth for high-margin butter and specialty margarine products. As consumers increasingly seek premium food experiences and authentic culinary products, manufacturers continue to invest in differentiated formulations targeting niche culinary and professional applications.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the global butter and margarine market due to their extensive product assortments, established cold-chain infrastructure, promotional capabilities, and high consumer footfall. These retail formats account for nearly half of global market sales and remain the primary purchasing destination for both mass-market and premium butter and margarine products. Consumers increasingly prefer supermarkets because they offer product variety, competitive pricing, convenient accessibility, and the ability to compare multiple brands within a single shopping environment. The expansion of organized retail infrastructure across developing economies is further contributing to channel growth.Online grocery platforms and direct-to-consumer distribution channels are emerging as some of the fastest-growing sales channels within the market. The rapid adoption of digital grocery shopping, accelerated by changing consumer behavior and growing smartphone penetration, is significantly transforming retail distribution dynamics. Consumers increasingly value the convenience of home delivery services, subscription-based grocery models, and digital product discovery. Manufacturers are actively strengthening partnerships with e-commerce retailers while simultaneously investing in direct-to-consumer websites, digital marketing campaigns, and personalized online engagement strategies to improve brand loyalty and customer retention.The integration of omnichannel retail strategies is becoming increasingly important as consumers seek seamless purchasing experiences across physical and digital platforms. Retailers and manufacturers are investing heavily in cold-chain logistics, digital payment systems, and real-time inventory management technologies to support efficient online dairy product distribution globally.

End-User Insights

Industrial food processors and commercial bakeries account for the largest share of global butter and margarine consumption due to their high-volume procurement requirements and continuous production operations. The industrial bakery sector represents a major demand driver because butter and margarine play essential roles in determining product texture, consistency, flakiness, moisture retention, and flavor quality across baked goods. Commercial bakeries utilize specialized margarine and butter formulations specifically designed for laminated dough products, pastries, confectionery items, cookies, cakes, and desserts.Household consumers continue to represent a stable and resilient demand base, especially across developed economies where dairy product penetration remains high. Retail butter consumption is supported by increasing interest in home cooking, premium meal preparation, and home baking activities. Consumers are increasingly willing to pay premium prices for organic butter, grass-fed dairy products, clean-label spreads, and functional margarine alternatives that align with healthier lifestyle preferences.Institutional buyers including schools, hospitals, military facilities, and large-scale catering companies also contribute significantly to global margarine demand due to cost efficiency, bulk procurement advantages, and extended storage capabilities. Margarine products remain particularly attractive within institutional foodservice operations because of their affordability and operational flexibility in large-scale meal preparation environments.

Nature Insights

Conventional products continue to dominate the global butter and margarine market, accounting for approximately 74% of total market share in 2025. The dominance of conventional products is primarily supported by their affordability, mass-market availability, extensive industrial usage, and well-established supply chain networks. Conventional butter and margarine products remain highly accessible across supermarkets, foodservice operations, and institutional purchasing channels worldwide. Industrial food manufacturers and commercial bakeries continue to rely heavily on conventional formulations due to lower procurement costs and consistent product availability.Vegan, plant-based, and non-GMO margarine products are experiencing substantial demand growth across developed markets where ethical consumption trends and plant-based dietary patterns continue to become mainstream. Increasing awareness regarding animal welfare, environmental sustainability, and carbon footprint reduction is accelerating adoption of dairy-free alternatives. Manufacturers are increasingly investing in innovative plant-oil formulations, fortified vegan spreads, and sustainable ingredient sourcing strategies to strengthen their competitive positioning within the rapidly growing plant-based food segment.Sustainability considerations are becoming increasingly important across the industry as consumers demand greater transparency regarding supply chain practices, packaging materials, and environmental impact. Manufacturers are investing heavily in certified organic dairy sourcing, environmentally responsible farming systems, recyclable packaging solutions, and carbon reduction initiatives to improve brand image and meet evolving regulatory standards. The growing influence of ESG-focused purchasing behavior is expected to continue reshaping product development and brand positioning strategies across the market.

Explore more data points, trends and opportunities Download Free Sample Report

Butter and Margarine Market Segmentations

By Product Type

- Butter

- Margarine

- Butter Blends & Dairy Spreads

- Plant-Based Margarine

- Functional Margarine

By Source

- Cow Milk

- Buffalo Milk

- Goat Milk

- Palm Oil

- Sunflower Oil

- Soybean Oil

- Canola/Rapeseed Oil

By Nature

- Conventional

- Organic

- Non-GMO

- Clean Label

- Vegan / Plant-Based

By Application

- Bakery & Confectionery

- Foodservice & Hospitality

- Processed Food Manufacturing

- Household Consumption

- Ready-to-Eat Meals

- Sauces, Dressings & Spreads

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Food Stores

- Wholesale Stores

- Online Retail

Regional Insights

North America

North America accounted for nearly 27% of the global butter and margarine market in 2025, led primarily by the United States and Canada. The region benefits from high consumption of packaged bakery products, frozen foods, processed meals, and premium dairy products. Consumer demand for grass-fed butter, organic dairy spreads, clean-label margarine products, and specialty culinary ingredients continues to rise steadily across the region. The United States remains one of the world’s largest consumers of processed bakery products and convenience foods, creating substantial industrial demand for butter and margarine products across bakery manufacturing and foodservice sectors.Several key drivers continue to support regional market growth. Rising consumer preference for premium and natural dairy products is encouraging higher consumption of artisanal butter and organic dairy spreads.

Europe

Europe remains the largest regional market, accounting for approximately 34% of global market share in 2025. Countries including Germany, France, the United Kingdom, Italy, and the Netherlands dominate regional demand due to their advanced dairy industries, strong bakery traditions, and high per capita dairy consumption levels. France remains a leading consumer of artisanal and premium butter products owing to its deeply rooted culinary culture and strong preference for high-quality dairy ingredients. Germany continues to maintain substantial industrial margarine demand through its highly developed processed food manufacturing and bakery sectors.In addition, increasing adoption of vegan and plant-based diets across countries such as the United Kingdom, Germany, and the Netherlands is accelerating demand for dairy-free margarine products and alternative spreads. Government regulations restricting trans fats and promoting healthier food formulations are also encouraging manufacturers to innovate with improved nutritional profiles. Premium retail expansion, strong tourism activity, and growing demand for gourmet culinary experiences continue to support market growth across the region.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market and is projected to expand at a CAGR exceeding 7% during the forecast period. China, India, Japan, South Korea, Indonesia, and Australia are among the major growth contributors driving regional expansion. Rapid urbanization, rising disposable incomes, westernization of dietary habits, and increasing demand for convenience foods are collectively transforming consumption patterns across the region.Japan and South Korea continue to demonstrate stable demand for premium imported butter products, functional margarine formulations, and specialty bakery ingredients due to strong consumer preference for high-quality processed foods. Meanwhile, Southeast Asian countries including Indonesia, Thailand, Vietnam, and the Philippines are witnessing rising demand for affordable margarine products supported by population growth and increasing processed food consumption. Expansion of organized retail infrastructure, growing cold-chain investments, rising digital grocery adoption, and increasing western influence on food consumption patterns remain major long-term growth drivers across the Asia-Pacific market.

Latin America

Latin America is experiencing moderate but steady market growth led by Brazil, Mexico, and Argentina. Rising processed food consumption, improving retail infrastructure, urbanization, and increasing demand for affordable spread products are supporting regional margarine market expansion. Brazil remains one of the largest regional consumers due to its extensive bakery, confectionery, and food processing industries. Increasing consumption of packaged bakery products and ready-to-eat foods continues to strengthen industrial demand for margarine products across the country.Mexico is also witnessing increasing demand for bakery fats due to the rapid expansion of fast-food chains, cafés, and convenience food manufacturing. The growth of modern supermarkets and organized retail chains across urban areas is improving consumer accessibility to premium butter products and imported dairy spreads. Rising middle-class incomes, increasing participation of women in the workforce, and growing demand for convenience foods are further supporting market growth across the region. Premium butter consumption is gradually increasing within hospitality sectors and urban retail markets as consumers become more receptive to premium culinary products and western-style food experiences.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential growth market due to increasing foodservice investments, tourism expansion, rising disposable incomes, and growing imports of premium dairy products. Countries including Saudi Arabia and the UAE are among the leading regional importers of butter and specialty bakery fats because of their rapidly expanding hospitality industries and strong demand from hotels, restaurants, and international bakery chains.Additionally, increasing investments in tourism, luxury hospitality projects, and international restaurant chains across Gulf Cooperation Council countries continue to generate strong commercial demand for premium butter products and specialty culinary fats. Growing consumer exposure to international cuisines, improving cold-chain infrastructure, and rising penetration of organized retail formats are expected to further accelerate long-term market growth across the Middle East & Africa region.

Key Players in the Butter and Margarine Market

- Arla Foods

- Fonterra

- Kerry Group

- FrieslandCampina

- Conagra Brands

- Upfield

- Associated British Foods

- Lactalis

- Land O'Lakes

- Ornua

- Saputo

- Bunge Global

- Fuji Oil Holdings

- Wilmar International

- Dairy Farmers of America