Bulk Nutritional Yeast Market Size

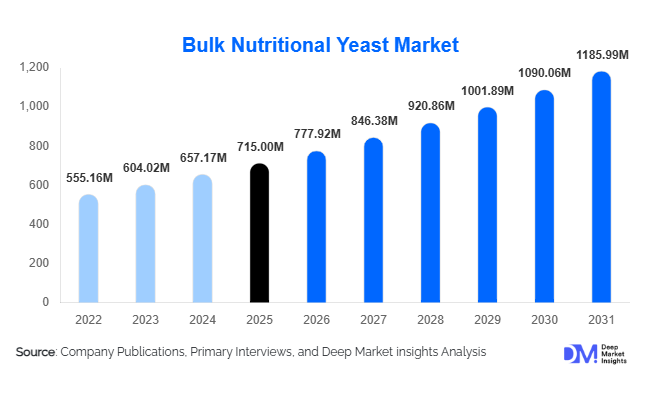

According to Deep Market Insights, the global bulk nutritional yeast market size was valued at USD 715 million in 2025 and is projected to grow from USD 777.92 million in 2026 to reach USD 1,185.99 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The bulk nutritional yeast market growth is primarily driven by rising global adoption of plant-based diets, increasing demand for clean-label protein ingredients, and expanding use of fortified yeast in functional foods and dietary supplements.

Key Market Insights

- Fortified nutritional yeast dominates global demand, accounting for over 60% of market share due to increasing vitamin B12 fortification requirements in vegan diets.

- Food & beverage manufacturers represent the largest end-use segment, particularly within plant-based meat and dairy alternatives.

- North America leads the market, supported by strong vegan penetration and developed alternative protein ecosystems.

- Asia-Pacific is the fastest-growing region, driven by expanding plant-based food industries in China and India.

- Direct B2B contracts dominate distribution, with large-scale manufacturers securing long-term procurement agreements.

- Fermentation technology advancements are improving yield efficiency and cost competitiveness globally.

What are the latest trends in the bulk nutritional yeast market?

Rise of Fortified and Functional Yeast Variants

Manufacturers are increasingly investing in micronutrient-fortified nutritional yeast variants enriched with vitamin B12, vitamin D, zinc, and iron. As vegan and flexitarian populations expand, demand for reliable non-animal vitamin sources is accelerating. Food processors are integrating fortified yeast into ready-to-eat meals, snack coatings, plant-based cheeses, and protein blends. This trend aligns with broader functional food expansion, where consumers seek immunity support, metabolic health, and protein enrichment in everyday diets.

Integration into Plant-Based Meat and Dairy Alternatives

Nutritional yeast is becoming a foundational ingredient in plant-based formulations due to its natural umami flavor profile and high protein content. It is widely used to replicate cheese flavors in dairy alternatives and enhance savory notes in plant-based meat analogues. As the global alternative protein industry expands at double-digit rates in several regions, bulk procurement volumes are increasing significantly. Manufacturers are also optimizing drying and milling processes to meet customized texture and solubility requirements for food applications.

What are the key drivers in the bulk nutritional yeast market?

Growth of Plant-Based and Vegan Diets

The rapid expansion of vegan, vegetarian, and flexitarian dietary patterns is one of the primary growth drivers. Nutritional yeast offers a non-animal, protein-rich, gluten-free ingredient that fits clean-label requirements. Increasing retail shelf space for plant-based products globally directly supports industrial yeast consumption.

Rising Demand for Clean-Label Protein Ingredients

Food manufacturers are reformulating products to remove artificial additives and synthetic flavor enhancers. Nutritional yeast naturally enhances savory flavor, allowing companies to reduce MSG usage while maintaining taste quality. This clean-label positioning strengthens long-term adoption across global markets.

What are the restraints for the global market?

Raw Material Price Volatility

Molasses and sugar substrates used in fermentation are subject to agricultural price fluctuations, impacting production costs. Energy-intensive drying processes further influence margin stability during periods of high utility prices.

Limited Awareness in Emerging Markets

Despite growing adoption in developed economies, awareness of nutritional yeast remains limited in several developing regions. Education and marketing investments are necessary to unlock full potential in price-sensitive markets.

What are the key opportunities in the bulk nutritional yeast industry?

Expansion in Asia-Pacific Manufacturing Hubs

Rapid industrialization in China and India is creating strong opportunities for localized fermentation facilities. Government initiatives supporting food processing and alternative protein development provide favorable conditions for capacity expansion. Export-driven production models in Asia are strengthening global supply chains.

Animal Nutrition and Premium Pet Food Applications

Nutritional yeast is increasingly used as a palatability enhancer and protein supplement in premium pet food. Rising global pet ownership and premiumization trends present high-margin opportunities for ingredient suppliers. Livestock feed applications focusing on gut health also offer long-term growth potential.

Product Type Insights

Fortified nutritional yeast dominates the global market, accounting for approximately 63% of the total market share in 2025. The leading position of this segment is primarily driven by the accelerating demand for vitamin B12-enriched food ingredients, particularly among vegan, vegetarian, and flexitarian consumers who seek reliable non-animal micronutrient sources. Increasing prevalence of B12 deficiency, growing clinical awareness, and the expansion of fortified functional foods have strengthened the adoption of fortified variants across both developed and emerging economies. Food manufacturers prefer fortified nutritional yeast due to its dual functionality as a flavor enhancer and micronutrient fortifier, enabling clean-label formulation without synthetic additives. Additionally, fortified variants command premium pricing and deliver higher margins, making them attractive to producers targeting dietary supplements, plant-based dairy alternatives, savory snacks, and meal replacements. The segment’s growth is further supported by regulatory encouragement for micronutrient fortification and rising consumer preference for health-oriented food products.

Form Insights

Flakes represent the leading form segment, capturing nearly 48% of the global market share in 2025. The dominance of flakes is primarily driven by their superior sensory appeal, including desirable texture, ease of sprinkling, and visual resemblance to grated cheese, which makes them highly suitable for seasoning applications, pasta toppings, salads, and plant-based cheese alternatives. The rapid growth of plant-based culinary trends and home cooking experimentation has further strengthened demand for flake formats in retail channels. Foodservice operators also favor flakes due to their consistent dispersion and enhanced mouthfeel in prepared dishes. Powdered nutritional yeast follows closely, supported by its strong applicability in dietary supplements, beverage premixes, protein blends, and large-scale industrial food processing where uniform mixing is critical. The versatility of powdered formats in automated production lines continues to support steady growth across functional food and nutraceutical segments.

Nature Insights

Conventional nutritional yeast accounts for roughly 72% of the total market share in 2025, largely driven by cost advantages, scalable production processes, and broad industrial usage across mainstream food manufacturing. Its affordability and consistent supply chain availability make it the preferred option for bulk buyers and large processed food companies. However, organic nutritional yeast is emerging as a high-growth segment, expanding at a CAGR exceeding 10%, supported by rising consumer demand for clean-label, non-GMO, and sustainably produced ingredients. The leading growth driver for the organic segment is increasing regulatory scrutiny on synthetic additives and heightened consumer preference for certified organic products, particularly in Western Europe and North America. Premium pricing, strong retail positioning, and alignment with sustainable food trends are expected to accelerate the penetration of organic variants in specialty and health-focused markets.

Distribution Channel Insights

Direct B2B sales dominate the distribution landscape, accounting for nearly 67% of the global market share. The leading driver for this segment is the strategic procurement model adopted by large food and beverage manufacturers, who secure long-term bulk contracts directly from producers to ensure price stability, quality consistency, and uninterrupted supply. As nutritional yeast becomes a core ingredient in plant-based and fortified food formulations, manufacturers increasingly prioritize integrated supply agreements to manage cost volatility and meet regulatory compliance standards. Ingredient distributors continue to play a critical role in expanding regional penetration, particularly in emerging markets where local sourcing networks and smaller manufacturers rely on intermediary supply chains. E-commerce retail platforms are gradually expanding in importance for consumer-packaged formats, though bulk industrial demand remains the primary revenue contributor.

End-Use Insights

The food and beverage manufacturing segment leads the market, accounting for approximately 58% of the total share in 2025. The primary driver for this dominance is the rapid expansion of plant-based meat alternatives, dairy substitutes, ready-to-eat meals, and savory snack formulations that utilize nutritional yeast for its umami flavor profile and natural fortification properties. As consumer demand shifts toward clean-label and protein-enriched foods, manufacturers increasingly incorporate nutritional yeast to enhance taste while improving nutritional content. Dietary supplements represent the fastest-growing end-use category, expanding at nearly 10% CAGR, supported by growing micronutrient fortification requirements, rising preventive healthcare awareness, and increasing adoption of vegan multivitamins. The ingredient’s high protein content and bioavailable B-vitamin profile further strengthen its application across sports nutrition and wellness products.

| By Product Type | By Form | By Nature | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, with the United States accounting for nearly 27% individually. Regional growth is primarily driven by a highly developed plant-based food ecosystem, strong consumer awareness regarding micronutrient fortification, and advanced fermentation and biotechnology infrastructure. The presence of leading plant-based food innovators, expanding vegan and flexitarian populations, and widespread retail availability of nutritional yeast products contribute to sustained demand. Additionally, favorable regulatory frameworks supporting food fortification and the rapid expansion of functional snack and supplement categories reinforce the region’s market leadership. Strong distribution networks and high per capita health expenditure further accelerate adoption.

Europe

Europe accounts for around 29% of global demand, led by Germany, the United Kingdom, and France. Regional growth is driven by stringent clean-label regulations, sustainability-focused food policies, and growing demand for alternative proteins. Western Europe demonstrates particularly strong adoption of organic nutritional yeast, supported by consumer preference for certified organic and non-GMO ingredients. The expansion of plant-based dairy and meat alternatives across retail shelves, coupled with government initiatives promoting sustainable food systems, continues to stimulate demand. Additionally, high awareness of vitamin deficiencies and established health food retail chains support steady consumption growth across the region.

Asia-Pacific

Asia-Pacific holds roughly 23% of the global market share and is the fastest-growing region, expanding at over 10% CAGR. Growth is primarily fueled by expanding food processing industries, rising disposable incomes, and increasing awareness of plant-based nutrition in urban centers. China leads regional production capacity due to its strong fermentation industry base and cost-efficient manufacturing capabilities, while India is emerging as one of the fastest-growing consumption markets driven by expanding vegetarian populations, rapid retail modernization, and growing investments in plant-based food startups. Rising demand for fortified packaged foods and government initiatives to address micronutrient deficiencies further strengthen regional growth prospects.

Latin America

Latin America represents approximately 8% of the global market, led by Brazil and Mexico. Regional growth is supported by the gradual expansion of processed food manufacturing, increasing urbanization, and rising middle-class purchasing power. Growing interest in plant-based diets and expanding modern retail infrastructure are creating new opportunities for nutritional yeast incorporation in savory snacks and ready meals. Improvements in regional supply chain integration and food ingredient imports are expected to support steady market expansion over the forecast period.

Middle East & Africa

The Middle East & Africa region contributes about 6% of global demand. Growth is primarily driven by rising health awareness, increasing demand for premium imported food ingredients, and expanding urban retail sectors in countries such as the UAE and South Africa. The region is witnessing gradual adoption of fortified and plant-based food products, particularly among expatriate populations and health-conscious consumers. Investments in food manufacturing infrastructure and expanding supermarket chains are expected to enhance product accessibility and stimulate moderate but steady market growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Bulk Nutritional Yeast Market

- Lesaffre Group

- Angel Yeast Co., Ltd.

- Lallemand Inc.

- AB Mauri

- Alltech Inc.

- DSM-Firmenich

- Leiber GmbH

- Ohly GmbH

- BioSpringer

- Kerry Group

- Cargill, Incorporated

- Synergy Flavors

- Pakmaya

- Oriental Yeast Co., Ltd.

- Halcyon Proteins