Bulk Bread Flour Market Size

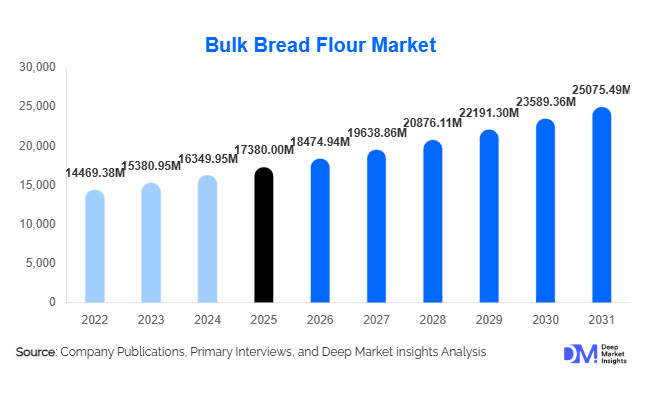

According to Deep Market Insights,the global bulk bread flour market size was valued at USD 17,380 million in 2025 and is projected to grow from USD 18,474.94 million in 2026 to reach USD 25,075.49 million by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The bulk bread flour market growth is primarily driven by rising industrial bread production, expansion of organized bakery chains, increasing demand for frozen and par-baked bakery products, and growing foodservice consumption across emerging economies. Bulk bread flour, characterized by high protein content and standardized gluten strength, is a critical raw material for industrial bakeries and QSR chains that require consistency, volume scalability, and cost efficiency.

Key Market Insights

- Industrial bread manufacturers account for the largest demand share, contributing nearly 46% of global consumption in 2025.

- Asia-Pacific leads the global market, holding approximately 34% share, supported by strong demand in China and India.

- High-protein flour (12.5%+ protein) dominates, representing over 41% of the 2025 market due to superior gluten strength.

- Direct B2B contracts account for more than 57% of distribution, reflecting long-term supply agreements between millers and industrial bakeries.

- Fortified and enriched flour demand is rising, particularly in developing economies with mandatory micronutrient programs.

- Top five global millers control nearly 40% of market revenue, indicating moderate consolidation.

What are the latest trends in the bulk bread flour market?

Rising Demand for Frozen & Par-Baked Applications

The expansion of frozen bakery products is significantly influencing bulk flour specifications. Manufacturers increasingly demand high-gluten, enzyme-optimized flour capable of maintaining structure during freezing and thawing cycles. The global frozen bakery industry, valued at over USD 35 billion, is driving innovation in flour blends tailored for shelf-life stability and volume consistency. Emerging markets in Southeast Asia and the Middle East are importing frozen dough and par-baked bread, increasing export-oriented flour milling capacity.

Fortification and Functional Standardization

Governments across Africa, South Asia, and Latin America are mandating iron and folic acid fortification in wheat flour. This trend has led millers to invest in micronutrient blending systems and automated dosage controls. Industrial buyers also demand consistent protein content with minimal batch variance, prompting adoption of real-time gluten analysis and digital milling technologies. Standardized flour enhances automated baking line efficiency and reduces waste, reinforcing long-term supply contracts.

What are the key drivers in the bulk bread flour market?

Growth in Industrial Bread Production

Global bread production exceeds 110 million tons annually, with packaged sandwich bread leading volume consumption. Urbanization and increasing reliance on convenience foods are accelerating demand for standardized bulk flour. Industrial bakeries prefer tanker-based bulk delivery systems that reduce handling costs and improve operational efficiency.

Expansion of QSR and Foodservice Chains

Rapid growth of global sandwich chains, burger outlets, and institutional catering services is boosting demand for consistent bread quality. Emerging economies such as India, Indonesia, and Saudi Arabia are witnessing strong QSR expansion, directly increasing bulk flour procurement volumes.

What are the restraints for the global market?

Volatility in Wheat Prices

Wheat accounts for nearly 70–75% of flour production cost. Climate variability, geopolitical disruptions, and export restrictions from major wheat-producing countries create pricing instability, impacting miller margins which typically range between 6–10%.

Shifting Consumer Preferences Toward Gluten-Free Products

In developed markets such as the U.S. and parts of Europe, increasing awareness of gluten sensitivity has marginally slowed growth in traditional wheat-based bread categories, although the impact remains limited to niche segments.

What are the key opportunities in the bulk bread flour industry?

Export-Oriented Milling Expansion

Countries such as Turkey, Canada, and Russia are expanding export-focused flour mills to serve import-dependent nations including Indonesia, Egypt, and Nigeria. Long-term government trade agreements are strengthening cross-border bulk supply contracts.

Premium & Clean Label Flour Variants

Industrial buyers are increasingly demanding Non-GMO and organic-certified bulk flour. Premium bakeries are willing to pay 10–18% higher prices for traceable, sustainably milled wheat, creating margin expansion opportunities for specialized millers

Wheat Type Insights

Hard Red Spring wheat flour dominates the global bulk bread flour market, accounting for approximately 32% of total market share in 2025. The segment’s leadership is primarily driven by its high protein content ranging between 13–14%, which delivers superior gluten strength, improved dough elasticity, and enhanced loaf volume. These characteristics are critical for large-scale industrial sandwich bread manufacturing, where uniform crumb structure, machinability, and shelf stability are essential. The rising demand for standardized baking inputs in automated production facilities further strengthens the adoption of Hard Red Spring wheat flour across North America, Europe, and export-oriented milling hubs. Hard Red Winter wheat follows closely, particularly across North America and key export markets, owing to its balanced protein profile and versatile baking performance. Its adaptability across diverse bread formulations makes it a preferred option for both industrial and large regional bakeries, supporting stable segment growth globally.

Protein Content Insights

High-protein flour (12.5% and above) leads the global market with around 41% share in 2025. The segment’s growth is driven by increasing industrial automation in commercial bakeries, where consistent gluten networks are essential for maintaining uniform product quality across high-speed production lines. High-protein variants ensure better gas retention, improved dough tolerance during mechanical handling, and longer fermentation stability, making them indispensable for industrial bread, burger buns, and packaged loaves. As frozen and par-baked bakery applications expand globally, the need for strong flour performance under cold-chain conditions further accelerates demand for high-protein flour. Medium-protein flour remains widely used in regional bakeries and specialty bread segments due to its balanced texture and cost-effectiveness, while lower-protein variants are largely confined to niche soft bread and specialty applications, limiting their overall revenue contribution.

Distribution Channel Insights

Direct B2B supply dominates distribution, representing nearly 57% of global revenue in 2025. The leadership of this channel is driven by long-term procurement contracts between millers and industrial bread manufacturers, ensuring supply continuity, price stability, and consistent quality specifications. Industrial bakeries increasingly prefer integrated supply agreements that include customized protein levels and quality assurance standards, strengthening miller-bakery partnerships. Institutional wholesalers and commodity export contracts account for the remaining share, particularly in import-dependent regions across Asia-Pacific, the Middle East, and Africa. Growth in international trade flows and government-backed food security programs continues to reinforce bulk contract-based flour distribution globally.

End-Use Insights

Industrial bread manufacturers represent the largest end-use segment, holding approximately 46% of total demand in 2025. The segment’s dominance is supported by rising consumption of packaged bread, expanding quick-service restaurant chains, and increasing urbanization driving demand for convenient staple foods. The frozen and par-baked bakery segment is the fastest-growing application, expanding at over 7% annually, fueled by modern retail penetration, foodservice expansion, and cold-chain logistics development. Bakery premix manufacturers and centralized baking hubs are also increasing bulk flour procurement to support standardized production across multiple retail outlets. Additionally, export-driven demand from Middle Eastern and Southeast Asian markets continues to support production growth in major milling and wheat-exporting countries such as Canada, Turkey, and the European Union, reinforcing global trade integration.

| By Wheat Type | By Protein Content | By Processing Type | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 34% of the global market share in 2025, making it the largest regional market. Growth is primarily driven by rapid urbanization, expanding middle-class populations, and increasing adoption of Western-style packaged bread products. China accounts for nearly 15% of global demand due to its large-scale industrial bread production capacity and modernization of milling infrastructure. India is the fastest-growing country in the region, expanding at around 8% CAGR, supported by rising organized bakery chains, growth in quick-service restaurants, and increasing demand for packaged staple foods in tier-II and tier-III cities. Southeast Asia is witnessing rapid import growth due to limited domestic wheat production and rising consumption of sandwich bread and burger buns, further supporting regional expansion.

North America

North America contributes nearly 26% of global market revenue, with the United States accounting for about 21% individually. The region benefits from a highly developed industrial baking infrastructure, advanced milling technologies, and strong export contracts to Latin America and Asia. High per capita bread consumption, stable demand for packaged bakery goods, and innovation in fortified and specialty flour variants support sustained market growth. Additionally, strong supply chain integration between wheat producers, millers, and industrial bakeries ensures consistent production and pricing stability across the region.

Europe

Europe represents roughly 23% of the global market, driven by established bakery traditions and strong demand for premium and fortified flour variants. Germany, France, and the United Kingdom lead regional demand, supported by a mature industrial bakery sector and growing consumer preference for high-quality packaged bread. Regulatory emphasis on food fortification, clean-label formulations, and traceability standards further supports the adoption of high-grade bulk bread flour. Export activity within the European Union and to neighboring Middle Eastern markets also strengthens regional production volumes.

Middle East & Africa

The Middle East & Africa region is characterized by high reliance on wheat and flour imports due to limited domestic production capacity. Countries such as Saudi Arabia and the UAE depend heavily on imported wheat and processed flour to meet staple food requirements. Government-backed food subsidy programs and strategic grain reserves play a crucial role in maintaining steady bread consumption growth. Egypt and Nigeria rank among the world’s major flour importers, driven by large populations and strong dependence on bread as a dietary staple. Infrastructure investments in milling facilities and storage capacity are further supporting regional market expansion.

Latin America

Latin America demonstrates stable growth, with Brazil and Mexico dominating regional demand. Brazil acts as both a major consumer and exporter, supported by its expanding commercial bakery sector and regional trade linkages. Mexico benefits from strong packaged bread consumption, driven by urban lifestyles and the presence of large industrial bakery brands. Rising supermarket penetration and growth in convenience food consumption across urban centers continue to support bulk flour demand throughout the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Bulk Bread Flour Market

- Archer Daniels Midland Company

- Cargill Incorporated

- Ardent Mills

- General Mills Inc.

- Conagra Brands Inc.

- King Arthur Baking Company

- Grain Craft

- Bay State Milling Company

- Allied Pinnacle

- Wilmar International

- Goodman Fielder

- Siemer Milling Company

- Hodgson Mill

- Nisshin Seifun Group

- Associated British Foods plc