Brewery Equipment Market Size

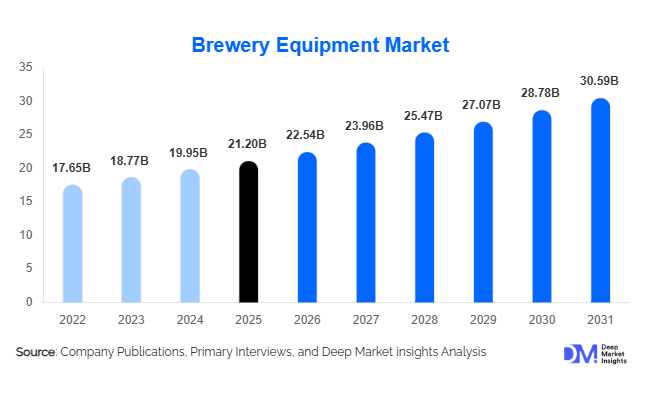

According to Deep Market Insights, the global brewery equipment market size was valued at USD 21.2 billion in 2025 and is projected to grow from USD 22.54 billion in 2026 to reach USD 30.59 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The brewery equipment market growth is primarily driven by the rapid expansion of craft and microbreweries, rising global beer consumption, and increased adoption of automation and digital process control in brewing operations.

Key Market Insights

- Fermentation and conditioning equipment dominate, accounting for a significant portion of the market due to their central role in beer production and quality control.

- Automation and digitalization are accelerating the adoption of high-efficiency brewing systems, including smart CIP, IoT-based monitoring, and predictive maintenance platforms.

- North America and Europe hold the largest market shares, with the U.S., Germany, and the U.K. driving demand for premium, automated, and compliance-focused equipment.

- Asia-Pacific is the fastest-growing region, driven by rising craft beer culture, growing disposable income, and expanding urban populations in China, India, and Japan.

- Microbreweries and craft breweries are creating new market opportunities for modular, flexible, and small-batch equipment designed for quality and customization.

- Regulatory compliance and sustainability trends are reshaping demand for energy-efficient, hygienic, and water-saving brewing technologies.

What are the latest trends in the brewery equipment market?

Automation and Digital Process Integration

Breweries worldwide are increasingly adopting automated and digitally controlled equipment to ensure consistency, reduce labor dependency, and improve operational efficiency. Smart brewery solutions, incorporating sensors, PLCs, and cloud-based analytics, allow real-time monitoring of fermentation, temperature, and flow rates. Predictive maintenance technologies minimize downtime, while IoT-enabled systems facilitate remote oversight of multiple production lines. Automation is particularly prominent in large-scale breweries and high-volume craft breweries, where precise control over brewing parameters directly affects product quality and cost-efficiency.

Modular and Flexible Equipment for Craft Breweries

The growing global craft beer segment is fueling demand for modular brewing systems that can be scaled according to production volume. Compact brewhouses, small fermentation tanks, and portable filtration units enable microbreweries and brewpubs to experiment with recipes and produce specialty beers without major capital expenditure. Flexible equipment designs also support retrofitting in older facilities and allow brewers to expand capacity incrementally, reducing financial risk while meeting growing consumer demand for artisanal beers.

What are the key drivers in the brewery equipment market?

Growing Global Beer Consumption and Craft Beer Popularity

Increasing beer consumption globally, combined with the surging popularity of craft and premium beers, is driving breweries to expand production capacity and modernize equipment. Consumers are seeking diverse beer flavors, specialty brews, and locally-produced artisanal options, compelling brewers to invest in specialized fermentation, conditioning, and packaging systems. This trend is most pronounced in North America and Europe, but is rapidly spreading to APAC markets like China and India.

Rising Demand for Automated and Hygienic Systems

Automation and hygiene compliance are key growth enablers in brewery operations. Automated brewing, cleaning, and packaging systems reduce human error, ensure consistent product quality, and adhere to stringent regulatory standards. Clean-in-Place (CIP) and sterilization technologies have become essential in modern breweries, particularly in regions with strict food safety regulations such as the U.S., Germany, and Japan.

Expansion in Emerging Markets

Emerging regions such as APAC and LATAM are witnessing increasing beer consumption, urbanization, and the establishment of new breweries. Government initiatives supporting food and beverage manufacturing, coupled with growing disposable income, encourage local breweries to invest in modern equipment. This expansion presents opportunities for both global equipment manufacturers and local suppliers to capture rising demand.

What are the restraints for the global market?

High Capital Expenditure Requirements

Brewery equipment requires substantial upfront investment, particularly for automated and high-capacity systems. Smaller brewers and startups may face financial constraints that delay the adoption of advanced technologies. High equipment costs can limit market penetration, especially in emerging regions with price-sensitive segments.

Raw Material Price Volatility and Supply Chain Challenges

Production of brewery equipment depends heavily on stainless steel, specialized alloys, and precision components. Fluctuations in raw material prices and global supply chain disruptions can increase manufacturing costs and delivery times, impacting overall market growth. Smaller brewers with limited budgets are particularly affected by these constraints.

What are the key opportunities in the brewery equipment market?

Expansion of Craft and Microbreweries

The proliferation of craft and microbreweries worldwide is creating demand for specialized, small-scale, and modular brewing systems. Equipment tailored for low-volume, high-quality production offers premium margins and recurring service opportunities. This segment is particularly attractive in North America, Europe, and rapidly growing APAC markets.

Adoption of Smart and Energy-Efficient Technologies

Breweries are increasingly investing in IoT-based monitoring, AI-driven process control, and energy-efficient solutions. These technologies enhance operational efficiency, minimize waste, and improve environmental compliance. Governments incentivizing sustainability further strengthen demand for smart brewing systems.

Emerging Market Growth

Regions such as China, India, and Brazil are experiencing rising beer consumption and new brewery establishments. Entry-level and mid-range equipment demand is rising, creating opportunities for manufacturers to expand geographically while introducing innovative and affordable solutions for growing markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 21.2 Billion |

| Market Size in 2026 | USD 22.54 Billion |

| Market Size in 2031 | USD 30.59 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fermentation and conditioning tanks represent the leading product segment, accounting for approximately 30% of the global brewery equipment market in 2025. Their dominance is primarily driven by their direct impact on beer quality, flavor consistency, alcohol content, and production scalability. As breweries increasingly focus on premiumization and differentiated taste profiles, particularly in craft and specialty beer categories, investment in advanced stainless-steel fermentation systems with automated temperature and pressure control has accelerated. These tanks also experience higher replacement and upgrade cycles compared to foundational brewhouse equipment, further strengthening revenue contribution.

Brewing process systems, including mash tuns, lauter tuns, wort kettles, and integrated brewhouses, form the second-largest segment. These systems are essential capital investments for new brewery establishments and capacity expansions. Growth in this segment is strongly linked to the rising number of microbreweries and regional production facilities globally. Modular and turnkey brewhouse systems are particularly in demand, as they reduce installation time and allow incremental expansion. Packaging and filling equipment is witnessing a strong technological evolution, driven by the need for automation, efficiency, and multi-format packaging flexibility. Increasing consumer preference for canned beer, sustainable packaging, and export-ready bottling solutions has accelerated investments in automated filling lines, labeling systems, and robotic palletizers. As breweries diversify product portfolios and scale exports, demand for high-speed, precision packaging systems continues to expand.

Application Insights

Macrobreweries remain the largest application segment, contributing approximately 75–80% of total market revenue in 2025. Their dominance is attributed to high production volumes, continuous modernization programs, and significant capital expenditure capabilities. Large breweries prioritize fully automated brewing lines, high-capacity fermentation vessels, and integrated packaging systems to maintain operational efficiency and quality consistency across global supply chains. Automation investments are particularly strong in developed markets, where labor costs are high and regulatory compliance requirements are stringent.

Craft breweries and microbreweries represent the fastest-growing application segment, expanding at a rate notably higher than the overall market CAGR. This growth is fueled by consumer preference for artisanal, locally brewed, and experimental beer varieties. Craft brewers typically demand compact, flexible, and modular equipment that allows small-batch production and recipe experimentation. This segment also supports higher margins for equipment manufacturers due to customization requirements. Brewpubs are gaining traction in urban centers, tourism hubs, and hospitality-driven economies. Their demand centers around integrated brewing systems designed for limited space and direct-to-consumer production models. Growth in this segment is closely tied to rising experiential dining trends and premium hospitality investments.

Distribution Channel Insights

Direct sales remain the dominant distribution channel, accounting for the majority of large-scale brewery equipment transactions globally. Major equipment manufacturers engage directly with macrobreweries and large craft producers through customized engineering contracts, turnkey installations, and long-term service agreements. These direct relationships allow suppliers to provide end-to-end solutions, including system integration, installation, operator training, and maintenance support. Regional distributors and system integrators play a critical role in serving small and mid-sized breweries, particularly in emerging markets. These intermediaries provide technical consultation, localized installation services, and aftermarket support, enabling smaller brewers to access global brands without extensive procurement complexity.

Digital sourcing platforms are gradually emerging as a complementary channel, particularly for modular systems and standardized components such as pumps, valves, and smaller fermentation units. Additionally, long-term OEM partnerships and preventive maintenance contracts are becoming central to revenue stability, as recurring service income enhances profitability and customer retention.

End-Use Insights

Macrobreweries constitute the largest end-use segment, driven by high-volume production requirements and consistent capital reinvestment. These facilities frequently upgrade equipment to improve energy efficiency, automation integration, and regulatory compliance. Their scale enables the adoption of Industry 4.0 technologies, predictive maintenance systems, and advanced CIP solutions. Microbreweries and craft breweries represent the fastest-growing end-use category, supported by strong consumer demand for premium and locally produced beer. This segment benefits from urbanization, tourism growth, and changing lifestyle preferences. Equipment demand in this segment is characterized by modularity, scalability, and flexibility.

Export-driven demand is emerging as an important growth factor, particularly in APAC and Latin America. As breweries in China, India, Brazil, and Mexico expand exports to neighboring markets, they invest in higher-quality fermentation and packaging systems that meet international safety and labeling standards. Premium and specialty breweries, in particular, prioritize automated and compliance-ready equipment, offering higher margins for suppliers.

Explore more data points, trends and opportunities Download Free Sample Report

Brewery Equipment Market Segmentations

By Product Type

- Brewing Process Systems

- Fermentation & Conditioning Tanks

- Filtration & Clarification Systems

- Packaging & Filling Equipment

- Cleaning & Sanitization

- Cooling & Temperature Control Systems

- Support & Utility Equipment

By Application

- Macrobreweries

- Craft Breweries

- Microbreweries

- Brewpubs

- Contract Brewing Facilities

By Automation Level

- Fully Automatic Systems

- Semi-Automatic Systems

- Manual Systems

By Distribution Channel

- Direct Sales

- Regional Distributors & System Integrators

- Online & Digital Equipment Platforms

- Aftermarket & Service Contracts

By Material Type

- Stainless Steel Equipment

- Copper & Alloy Equipment

- Carbon Steel Equipment

- Modular/Prefabricated Systems

Regional Insights

North America

North America accounted for approximately 28% of the global brewery equipment market in 2025, with the United States representing the dominant share within the region. Growth is primarily driven by a mature yet dynamic craft beer industry, continuous modernization of large-scale brewing facilities, and strong demand for automated and energy-efficient systems. The U.S. benefits from advanced manufacturing capabilities, high capital investment capacity, and strict food safety regulations that encourage the adoption of hygienic, stainless-steel, and automated brewing technologies. Canada supports steady growth through the expansion of regional microbreweries and provincial-level incentives for local beverage manufacturing. Additionally, high labor costs across North America further accelerate automation investments.

Europe

Europe holds the largest regional share at approximately 32% in 2025, led by Germany, the United Kingdom, Belgium, and Italy. The region’s dominance stems from its deep-rooted brewing heritage, high per-capita beer consumption, and strong export orientation. Germany remains a key equipment manufacturing hub, while the U.K. drives craft brewery expansion. Strict EU regulations on hygiene, sustainability, and energy efficiency stimulate continuous upgrades to advanced brewing and packaging systems. Sustainability initiatives, including carbon-reduction targets and water conservation mandates, are key regional growth drivers. Additionally, Europe’s strong presence of global brewery equipment manufacturers reinforces technological innovation and market maturity.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for roughly 22–24% of global revenue in 2025. China leads in production capacity expansion, driven by rising urban beer consumption and premiumization trends. India is witnessing rapid growth in microbreweries, particularly in metropolitan cities, supported by evolving consumer preferences and regulatory relaxation in select states. Japan and South Korea emphasize technological sophistication and premium brewing standards. Regional growth is fueled by rising disposable income, expanding middle-class populations, foreign investment in beverage manufacturing, and increasing export ambitions. Government-backed manufacturing initiatives and industrial modernization programs further stimulate equipment demand.

Latin America

Latin America contributes approximately 9–10% of the global market, with Brazil and Mexico as primary growth engines. Rising disposable income, tourism expansion, and the increasing popularity of craft and premium beers are driving new brewery establishments. Modernization of legacy brewing facilities and growing export activity to North America and Europe encourage investment in automated fermentation and packaging systems. However, dependence on imported high-end equipment remains a structural characteristic of the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6–7% of the global market. South Africa leads African demand due to a relatively mature brewing sector and an expanding craft beer ecosystem. Nigeria is emerging as a growth hub, supported by rising urban populations and domestic beer production expansion. In the Middle East, regulatory restrictions limit alcohol production in certain countries; however, the UAE and Saudi Arabia show growing investment in premium hospitality-driven brewing facilities and non-alcoholic beer production lines. Infrastructure development, tourism diversification strategies, and rising regional manufacturing investments serve as long-term growth drivers.

Key Players in the Brewery Equipment Market

- Alfa Laval

- GEA Group Aktiengesellschaft

- Krones AG

- Paul Mueller Company

- Praj Industries

- Meura

- Della Toffola

- Criveller Group

- Schulz

- Hypro

- Ampco Pumps Company

- ABE Equipment

- Brewbilt Manufacturing

- Lehui

- Deutsche Beverage Technology