Breadfruit Market Size

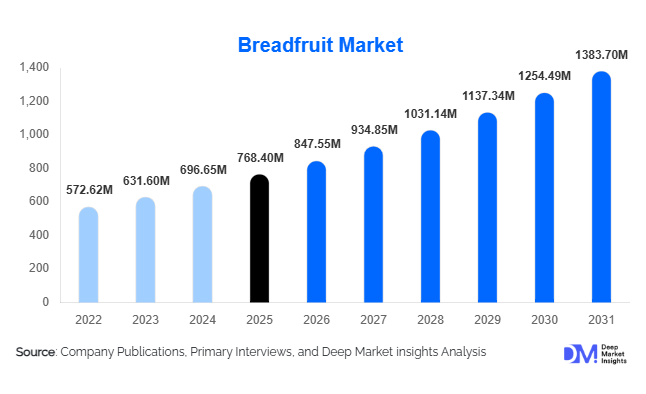

According to Deep Market Insights, the global breadfruit market size was valued at USD 768.4 million in 2025 and is projected to grow from USD 847.55 million in 2026 to reach USD 1383.70 billion by 2031, expanding at a CAGR of 10.3% during the forecast period (2026–2031). The breadfruit market growth is primarily driven by rising demand for gluten-free ingredients, increasing adoption of sustainable food crops, and the expanding use of breadfruit flour and processed breadfruit products across the global food and beverage industry.

Key Market Insights

- Breadfruit flour is emerging as a major gluten-free ingredient, increasingly utilized in bakery products, nutrition blends, snacks, and plant-based food formulations.

- Agroforestry and climate-resilient agriculture initiatives are accelerating breadfruit cultivation across tropical economies including the Caribbean, Southeast Asia, and Africa.

- Asia-Pacific dominates the global breadfruit market, supported by strong cultivation volumes, domestic consumption, and expanding tropical food processing infrastructure.

- North America remains one of the fastest-growing import-driven markets, driven by rising health-conscious consumer demand for functional tropical ingredients.

- Organic and minimally processed breadfruit products are gaining popularity, particularly among premium health food consumers in Europe and North America.

- Technological advancements in dehydration, freeze-drying, and flour processing are improving shelf life, export potential, and commercial scalability of breadfruit-based products.

What are the latest trends in the breadfruit market?

Expansion of Gluten-Free and Functional Food Applications

Breadfruit is increasingly being integrated into gluten-free and functional food formulations due to its high fiber content, resistant starch composition, and natural nutritional profile. Food manufacturers are launching breadfruit-based bakery products, snack foods, pancake mixes, pasta products, and nutritional supplements targeting health-conscious consumers. Demand for alternative flours has accelerated significantly as consumers seek allergen-friendly and clean-label ingredients. Breadfruit flour is also being positioned as a low-glycemic carbohydrate alternative suitable for wellness-focused diets. This trend is particularly strong across North America and Europe where gluten-free product innovation continues to expand rapidly. Functional food companies are further investing in research related to breadfruit’s digestive health benefits, prebiotic properties, and potential applications in sports nutrition and wellness foods.

Sustainable Agroforestry and Climate-Resilient Cultivation

Breadfruit cultivation is increasingly being promoted as part of sustainable agriculture and climate adaptation programs. Breadfruit trees are highly productive perennial crops requiring relatively low agricultural inputs compared to conventional staple crops. Governments and agricultural organizations are supporting breadfruit agroforestry initiatives due to their ability to improve biodiversity, reduce soil erosion, and support carbon sequestration. Tropical economies in the Caribbean, Pacific Islands, Southeast Asia, and Africa are expanding breadfruit plantation programs to strengthen domestic food security and reduce dependence on imported grains. Sustainable sourcing certifications and regenerative agriculture practices are becoming important market differentiators for exporters and processed food manufacturers targeting premium international markets.

What are the key drivers in the breadfruit market?

Growing Demand for Plant-Based and Gluten-Free Foods

The global rise in plant-based and gluten-free dietary preferences is one of the strongest growth drivers for the breadfruit market. Breadfruit flour provides a nutritious and naturally gluten-free alternative to conventional wheat flour, making it attractive for bakery manufacturers and food processors. Increasing prevalence of gluten intolerance, celiac disease, and consumer preference for clean-label ingredients are accelerating commercial adoption. Food companies are increasingly incorporating breadfruit into premium snack products, baking mixes, frozen foods, and health-focused packaged meals. Rising awareness regarding functional carbohydrates and digestive wellness is also strengthening consumer interest in breadfruit-based ingredients globally.

Rising Focus on Sustainable Food Security

Governments and development agencies are increasingly recognizing breadfruit as a strategic crop for food security and sustainable agriculture. Breadfruit trees can produce large volumes of food with minimal fertilizer and irrigation requirements while remaining resilient to climate variability. Tropical nations are promoting breadfruit cultivation to diversify food systems and reduce import dependency on grains and processed foods. International agricultural organizations are funding breadfruit agroforestry projects to improve rural incomes, strengthen local food systems, and support environmental sustainability. This increasing institutional support is accelerating investments across cultivation, processing, and export infrastructure.

What are the restraints for the global market?

Limited Commercial Supply Chain Infrastructure

The breadfruit market continues to face challenges associated with fragmented supply chains and limited commercial-scale processing infrastructure. Production remains heavily dependent on smallholder farmers in tropical regions where harvesting, storage, and transportation systems are often underdeveloped. Seasonal variability and inconsistent raw material quality create operational challenges for large-scale food manufacturers seeking standardized ingredient supply. Limited cold-chain networks and post-harvest processing facilities also contribute to product losses and export inefficiencies, restricting broader market scalability.

Low Consumer Awareness in Developed Markets

Although breadfruit awareness is gradually increasing globally, the product remains relatively niche across many developed economies. Consumers outside traditional breadfruit-producing regions are still unfamiliar with its culinary uses, nutritional value, and processing applications. This creates marketing and educational challenges for food manufacturers and retailers attempting to commercialize breadfruit products internationally. Companies must invest significantly in branding, consumer education, product innovation, and retail positioning to increase mainstream adoption. In addition, varying food safety regulations and certification requirements across export markets create compliance complexities for smaller processors.

What are the key opportunities in the breadfruit industry?

Expansion of Breadfruit Flour Processing

The growing demand for alternative flour products presents significant opportunities for breadfruit processors globally. Breadfruit flour is increasingly used across gluten-free bakery products, nutritional supplements, snacks, and health-oriented packaged foods. Investments in dehydration, freeze-drying, and milling technologies are improving product quality and export viability. Manufacturers capable of producing standardized, shelf-stable breadfruit flour can access premium international markets with higher profit margins. The expansion of health food retail channels and e-commerce platforms further supports the commercialization of breadfruit-based ingredients among wellness-focused consumers.

Export-Oriented Tropical Food Value Chains

Rising international demand for tropical superfoods and functional ingredients is creating opportunities for export-oriented breadfruit processing industries. Caribbean, Pacific Island, African, and Southeast Asian producers are increasingly investing in frozen breadfruit, chips, starches, and minimally processed products for export markets. Improvements in cold-chain logistics, packaging technologies, and food safety certifications are enabling year-round exports to North America and Europe. Organic breadfruit products and sustainably sourced ingredients are particularly attractive within premium health food retail channels. Strategic partnerships between farmers, processors, and food manufacturers are expected to strengthen long-term export competitiveness.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 768.40 Million |

| Market Size in 2026 | USD 847.55 Million |

| Market Size in 2031 | USD 1383.70 Million |

| CAGR | 10.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

The global breadfruit market is experiencing significant transformation across multiple product formats as manufacturers, food processors, and ingredient suppliers increasingly commercialize breadfruit into value-added applications. Among all product categories, breadfruit flour continues to dominate the market, accounting for approximately 29% of the global market value. The segment’s leadership is primarily driven by the accelerating global demand for gluten-free, clean-label, and plant-based functional ingredients. Breadfruit flour has emerged as a highly attractive alternative to conventional wheat flour and other gluten-free substitutes due to its nutritional composition, including high dietary fiber, resistant starch, potassium, antioxidants, and complex carbohydrates. Food manufacturers are increasingly incorporating breadfruit flour into bakery products, pancake mixes, nutrition bars, breakfast cereals, snacks, pasta, infant nutrition products, and meal replacement formulations. The rising prevalence of gluten intolerance, celiac disease awareness, and digestive wellness trends continues to strengthen demand for alternative flour solutions, positioning breadfruit flour as an increasingly important ingredient within the functional food industry.Dried breadfruit products are gaining substantial traction across export-oriented markets due to their cost-efficient transportation, lower spoilage rates, and extended shelf stability. Dehydrated breadfruit slices, powders, flakes, and dried cubes are increasingly exported to international food manufacturers, ingredient processors, and specialty retailers. The segment benefits significantly from the expansion of cross-border e-commerce and specialty tropical food distribution channels. In addition, dried breadfruit products align well with the growing demand for shelf-stable healthy food ingredients and emergency food reserves, particularly in regions focused on food security and disaster resilience planning.Industrial starch applications currently represent a relatively niche yet promising segment within the broader breadfruit market. Breadfruit-derived starch is gaining attention for its potential applications across food processing, biodegradable packaging materials, pharmaceutical binders, and specialty industrial formulations. Increasing environmental concerns regarding petroleum-based plastics and rising investments in biodegradable materials are expected to create new growth opportunities for breadfruit starch applications over the forecast period. Research institutions and food technology companies are actively exploring the functional properties of breadfruit starch to support broader commercial adoption across industrial sectors.

Application Insights

The food and beverage sector remains the dominant application segment within the global breadfruit market, accounting for nearly 64% of total market demand. The segment’s leadership is supported by the growing incorporation of breadfruit into mainstream food formulations, functional nutrition products, and plant-based product portfolios. Breadfruit’s versatility, nutritional profile, and compatibility with gluten-free and clean-label food trends have significantly expanded its commercial applications across both developed and emerging markets. Food manufacturers increasingly utilize breadfruit ingredients in bakery products, soups, frozen foods, breakfast items, snacks, pasta products, beverage formulations, and nutritional supplements.Bakery and snack applications are witnessing particularly strong growth as manufacturers continue diversifying their alternative flour and plant-based ingredient portfolios. Breadfruit flour offers favorable textural properties and nutritional benefits that make it highly suitable for breads, muffins, cookies, crackers, tortillas, and snack products. Increasing consumer interest in ancient grains, tropical superfoods, and non-traditional carbohydrates is further accelerating market adoption. In addition, the rapid expansion of specialty gluten-free product categories across supermarkets, health food retailers, and online grocery platforms is creating additional growth opportunities for breadfruit-based bakery applications.Cosmetics and personal care applications currently represent a relatively smaller segment but are gradually emerging due to growing consumer preference for botanical, plant-based, and naturally sourced ingredients. Breadfruit extracts are being explored for their antioxidant properties, skin hydration benefits, and potential applications in natural skincare formulations. Clean beauty trends, organic cosmetics demand, and increasing consumer scrutiny regarding synthetic ingredients are expected to encourage further research and commercialization within this segment. Manufacturers are increasingly focusing on tropical botanical branding strategies to differentiate premium skincare and wellness products in competitive global markets.

Distribution Channel Insights

Distribution dynamics within the global breadfruit market are evolving rapidly as manufacturers and suppliers adopt increasingly diversified sales strategies to expand international market reach. Direct B2B sales remain one of the most significant distribution channels, accounting for approximately 37% of total global market revenue. Large-scale food manufacturers, bakery chains, commercial ingredient processors, and institutional buyers increasingly procure breadfruit flour and processed breadfruit ingredients through long-term procurement agreements with regional processors and exporters. The growing commercialization of breadfruit within mainstream food manufacturing has strengthened the importance of stable industrial supply relationships, particularly for gluten-free and functional food production.Online retail channels are witnessing some of the fastest growth rates within the global breadfruit market. The rapid expansion of e-commerce platforms, direct-to-consumer food brands, and digital grocery services has significantly improved accessibility for niche tropical food products. Consumers increasingly rely on online platforms to purchase specialty gluten-free ingredients, wellness products, and exotic food items that may not be widely available through conventional retail channels. E-commerce has also enabled smaller tropical food brands and regional breadfruit processors to access broader international consumer bases while reducing dependence on traditional brick-and-mortar retail networks. Subscription-based wellness food services and health-focused online marketplaces are further accelerating digital sales growth.Foodservice and institutional distribution channels are also expanding steadily as restaurants, hotels, catering providers, and hospitality operators increasingly incorporate breadfruit-based dishes into sustainable and locally inspired menu offerings. Culinary innovation involving tropical ingredients, plant-based cuisine, and ethnic food experiences is creating new commercial opportunities for breadfruit suppliers globally. Tourism-driven economies, particularly across the Caribbean and Southeast Asia, are actively promoting breadfruit as a culturally authentic and environmentally sustainable ingredient within hospitality sectors. Institutional demand from schools, healthcare facilities, and government-supported nutrition programs may also contribute to future market expansion as food security initiatives increasingly emphasize resilient local crops.

End-Use Industry Insights

The food processing industry remains the largest end-use sector within the global breadfruit market, accounting for approximately 41% of overall market demand. The segment continues to benefit from rising consumer demand for gluten-free foods, clean-label ingredients, and plant-based nutrition products. Food manufacturers are increasingly integrating breadfruit flour and processed breadfruit ingredients into frozen meals, snack foods, bakery products, soups, ready-to-eat meals, and nutritional formulations. Ongoing innovation in alternative carbohydrates and sustainable food ingredients is expected to further strengthen breadfruit’s role within global food manufacturing operations.The nutraceutical and dietary supplement industry is among the fastest-growing end-use sectors due to increasing global interest in digestive health, gut microbiome support, metabolic wellness, and plant-based functional nutrition. Breadfruit’s resistant starch content and fiber composition make it highly attractive for digestive wellness applications. As preventive healthcare spending continues to rise globally, manufacturers are investing in research and development initiatives focused on incorporating breadfruit-derived ingredients into functional wellness products.The hospitality and foodservice sector is also increasing its adoption of breadfruit products, particularly in tourism-driven economies where sustainable local ingredients are becoming important components of culinary branding strategies. Restaurants and hotels are increasingly incorporating breadfruit into gourmet dishes, vegan cuisine, traditional recipes, and healthy menu offerings. The growing popularity of experiential dining and regional cuisine exploration is expected to further enhance breadfruit utilization within foodservice industries.Emerging industrial starch applications and pet nutrition uses may create additional long-term growth opportunities for the breadfruit market. As sustainability concerns and circular economy initiatives continue shaping industrial innovation, breadfruit-derived starches may witness broader adoption across biodegradable materials and specialty industrial applications. Similarly, increasing demand for natural pet nutrition ingredients may encourage manufacturers to explore breadfruit-based formulations within premium pet food categories.

Explore more data points, trends and opportunities Download Free Sample Report

Breadfruit Market Segmentations

By Product Form

- Fresh Breadfruit

- Frozen Breadfruit

- Dried Breadfruit

- Breadfruit Flour

- Breadfruit Puree & Paste

- Breadfruit Chips & Snacks

- Breadfruit Starch

- Breadfruit-Based Ingredients

By Nature

- Conventional Breadfruit

- Organic Breadfruit

By Application

- Food & Beverage

- Animal Feed

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

- Industrial Starch Applications

By Distribution Channel

- Direct/B2B Sales

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Health Food Stores

- Online Retail

- Foodservice & Institutional Sales

By End-Use Industry

- Household Consumption

- Food Processing Industry

- Bakery & Confectionery Industry

- Nutraceutical Industry

- Hospitality & Foodservice

- Animal Nutrition Industry

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 34% of the global breadfruit market in 2025, making it the leading regional market worldwide. The region benefits from favorable tropical climatic conditions, strong agricultural production capabilities, expanding food processing industries, and rising consumer awareness regarding functional nutrition. Countries including the Philippines, Indonesia, Thailand, Vietnam, and India are witnessing increasing breadfruit cultivation activity alongside rising investments in tropical food processing infrastructure and export-oriented agricultural development.Southeast Asian countries continue benefiting from strong export opportunities for tropical processed foods, increasing tourism-related food demand, and growing investments in value-added agricultural processing industries. Expanding regional trade agreements, improving cold-chain infrastructure, and rising international demand for tropical functional ingredients are expected to support Asia-Pacific’s continued market leadership over the forecast period.

North America

North America held nearly 24% of the global breadfruit market in 2025, driven primarily by strong consumer demand for gluten-free, plant-based, and functional food ingredients across the United States and Canada. The region’s advanced health and wellness food sector, rising prevalence of specialized diets, and increasing consumer awareness regarding sustainable nutrition continue to support market growth.Rising investment in functional food innovation, growing awareness regarding digestive health, and increasing multicultural food consumption patterns are also contributing to market growth across North America. Foodservice innovation, ethnic cuisine popularity, and the growing demand for plant-based convenience foods are expected to further strengthen long-term regional demand.

Europe

Europe accounted for approximately 21% of the global breadfruit market, supported by rising demand for sustainable, organic, and clean-label food ingredients. The region’s strong regulatory focus on food quality, environmental sustainability, and health-conscious consumption patterns continues to create favorable conditions for breadfruit market expansion.Across Europe, government sustainability initiatives, rising vegan populations, and strong growth in natural food retailing are expected to further support market development. Increasing investments in specialty food imports, expanding multicultural culinary trends, and growing consumer experimentation with exotic ingredients are also contributing to long-term regional growth.

Latin America

Latin America remains an important production and export region for breadfruit products, particularly across Caribbean economies such as Jamaica, Trinidad & Tobago, and the Dominican Republic. Favorable climatic conditions, established breadfruit cultivation traditions, and growing export-oriented food processing activities continue supporting regional market development.Regional processors are increasingly investing in flour production, frozen products, packaged snacks, and export-oriented value-added processing facilities to improve global competitiveness. Rising tourism activity across the Caribbean is also contributing to regional demand through hospitality and foodservice applications. In addition, increasing international recognition of Caribbean cuisine and tropical superfoods is expected to support future export growth for breadfruit-based products.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but steady breadfruit market expansion supported by food security initiatives, agricultural diversification efforts, and increasing interest in tropical functional foods. Several African countries including Ghana, Nigeria, and Kenya are promoting breadfruit cultivation to diversify agricultural systems, strengthen rural incomes, and improve climate resilience within local food production systems.The UAE serves as an important import-driven market for premium tropical food products due to rising consumer demand for health-oriented, organic, and exotic food ingredients. Expanding modern retail infrastructure, increasing expatriate populations, and strong growth in wellness-focused food retailing are further supporting regional demand. Over the long term, increasing investments in food processing infrastructure, agricultural innovation, and sustainable food supply chains are expected to create additional growth opportunities across the Middle East & Africa breadfruit market.

Key Players in the Breadfruit Market

- Natural Products of the Caribbean

- Caribbean Breadfruit Company

- Hawaiian Breadfruit Company

- Jamaica Producers Group

- Tropical Sun Foods

- Good Food Foods

- Amazi Foods

- Nature’s Legacy Exports

- Pure Ocean

- Vinaka Agriculture

- Island Foods Limited

- Earthinks

- Tropical Exporters International

- Global Breadfruit

- Pacific Harvest Foods