Bread Improver Market Size

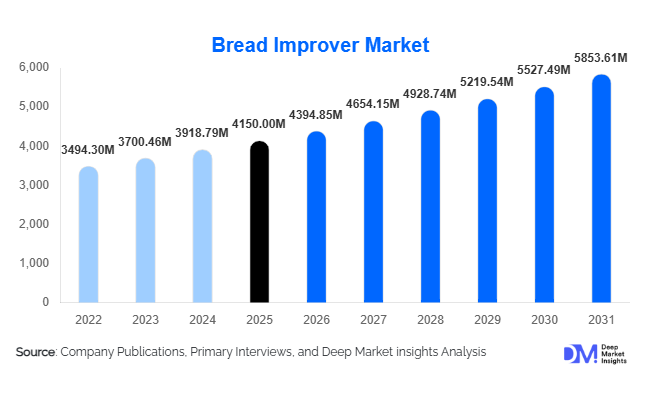

According to Deep Market Insights, the global bread improver market size was valued at USD 4,150 million in 2025 and is projected to grow from USD 4394.85 million in 2026 to reach USD 5,853.61 million by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The bread improver market growth is primarily driven by rising industrial bakery automation, increasing demand for clean-label enzyme-based formulations, and growing consumption of packaged and frozen bakery products worldwide.

Key Market Insights

- Enzyme-based bread improvers dominate the market, accounting for nearly 42% of global revenue in 2025, supported by clean-label trends and regulatory shifts away from chemical oxidants.

- Industrial bakeries represent over 63% of total demand, driven by automation and the need for standardized dough performance.

- Europe leads the global market with approximately 32% share, supported by strong enzyme innovation and regulatory compliance requirements.

- Asia-Pacific is the fastest-growing region, expanding at over 7% CAGR due to rising packaged bread consumption in China and India.

- Powdered formulations account for nearly 68% of the total market share, owing to ease of storage and dosing efficiency.

- Frozen dough and par-baked segments are emerging as high-growth applications, requiring advanced freeze-tolerant improver systems.

What are the latest trends in the bread improver market?

Shift Toward Clean-Label and Enzyme-Only Systems

Manufacturers are increasingly reformulating bread improvers to eliminate chemical oxidizing agents such as azodicarbonamide and replace them with enzyme-based systems. Regulatory scrutiny and consumer preference for “natural” ingredients are accelerating this transition. Multi-enzyme blends combining amylase, xylanase, and protease are gaining adoption for improving dough stability and crumb softness without chemical additives. Suppliers are investing in biotechnology research to develop precision enzyme solutions that address flour variability while maintaining label transparency.

Growth of Frozen and Par-Baked Bakery Products

The rapid expansion of frozen dough and par-baked bread production is reshaping demand patterns. These applications require improvers capable of maintaining dough strength and gas retention during freeze-thaw cycles. Industrial bakeries are adopting advanced improver systems that enhance fermentation tolerance and extend shelf life. This trend is particularly strong in North America, Europe, and emerging Asian markets, where modern retail formats and QSR chains are expanding.

What are the key drivers in the bread improver market?

Expansion of Industrial Bakery Automation

Industrial bakeries increasingly rely on automated production lines, which require consistent dough behavior and reduced batch variability. Bread improvers help maintain uniform crumb structure, volume, and texture, minimizing waste and improving production efficiency. As large-scale bakeries account for the majority of global bread production, demand for performance-enhancing improvers continues to rise steadily.

Rising Demand for Specialty and Premium Breads

Whole grain, multigrain, gluten-modified, and high-fiber bread varieties often require structural reinforcement due to weaker gluten networks. Bread improvers enable manufacturers to maintain texture and softness in these premium formulations. The premiumization of packaged bread in both developed and developing economies is significantly contributing to market expansion.

What are the restraints for the global market?

Volatility in Raw Material Prices

Key ingredients such as enzymes, emulsifiers, and ascorbic acid are subject to price fluctuations due to fermentation input costs and chemical feedstock volatility. These fluctuations can compress margins for manufacturers and create pricing instability across the value chain.

Regulatory Compliance Challenges

Stringent food additive regulations in Europe and North America require continuous reformulation and compliance investments. Restrictions on certain oxidants and labeling requirements may increase R&D costs and limit traditional product portfolios.

What are the key opportunities in the bread improver industry?

Emerging Market Flour Standardization

Countries such as India, Indonesia, Brazil, and Egypt experience flour quality variability due to climate conditions and wheat import dependence. Bread improvers offer flour correction capabilities, presenting strong growth opportunities in these markets. Establishing regional technical support centers can enhance market penetration.

Customized Solutions for Frozen Bakery Expansion

The frozen bakery segment is expanding at over 7% annually, creating demand for freeze-tolerant improver systems. Suppliers offering tailored solutions for frozen and par-baked products can capture premium pricing and long-term contracts with industrial bakery chains.

Product Type Insights

Enzyme-based bread improvers lead the global market, accounting for approximately 42% of total revenue in 2025. Their leadership is primarily driven by the global shift toward clean-label formulations, increasing regulatory restrictions on chemical oxidizing agents, and rising demand for natural dough conditioning solutions. Enzymes such as amylase, xylanase, and protease improve dough tolerance, gas retention, and crumb softness without chemical additives, making them highly attractive in Europe and North America, where regulatory oversight is stringent. Additionally, enzyme systems allow bakeries to compensate for wheat protein variability caused by climate fluctuations, further strengthening their adoption.

Emulsifier-based improvers hold the second-largest share and remain widely used in high-volume packaged sandwich bread production due to their ability to enhance dough stability and extend shelf life. However, some synthetic emulsifiers face regulatory and consumer scrutiny, gradually shifting innovation toward enzyme-emulsifier hybrid systems. Oxidizing and reducing agents maintain niche demand, particularly in cost-sensitive emerging markets, but their share is gradually declining. Meanwhile, completely formulated improver systems are gaining momentum among large industrial bakeries seeking turnkey solutions that reduce formulation complexity, ensure batch consistency, and optimize operational efficiency. These systems are increasingly customized to specific flour qualities and processing conditions.

Form Insights

Powdered bread improvers dominate the market with nearly 68% share in 2025, supported by superior storage stability, longer shelf life, ease of transport, and compatibility with automated dry dosing systems. Powder formats are particularly favored in large industrial bakeries where production lines operate continuously and require consistent ingredient flow. Their cost-effectiveness and simplified logistics further reinforce their leadership position globally.

Liquid bread improvers are witnessing steady growth, particularly in North America and Western Europe, where high-capacity bakeries use automated injection and metering systems. Liquids allow for improved dispersion and uniform mixing, especially in high-speed production environments. Meanwhile, paste and gel formats occupy a smaller niche, primarily within artisan bakeries and specialty bread producers who require flexibility in small-batch production.

Application Insights

Industrial sandwich bread accounts for approximately 35% of total market demand, making it the leading application segment. This dominance stems from high global consumption of packaged bread through supermarkets and modern retail channels. Industrial sandwich bread production requires consistent volume, crumb softness, and extended shelf life, attributes directly enhanced by bread improvers. The segment’s growth is particularly strong in North America, Europe, and rapidly urbanizing Asia-Pacific economies.

Buns and rolls represent a significant segment driven by QSR expansion and growing fast-food consumption worldwide. However, the fastest-growing application is frozen dough, expanding at over 7% CAGR. Freeze-thaw stability requirements create a higher dependency on advanced improver systems. Specialty breads such as whole grain, multigrain, and high-fiber variants are also expanding, as these formulations require structural reinforcement due to weaker gluten networks, increasing improver usage per unit of flour.

End-Use Insights

Industrial bakeries represent nearly 63% of total global demand, making them the dominant end-use segment. Automation, export-oriented packaged bread production, and stringent quality control standards drive consistent improver usage. Large bakery chains prioritize yield optimization, reduced waste, and production efficiency, key benefits delivered by advanced improver systems.

Artisan bakeries maintain stable demand, particularly in Europe, where traditional bread varieties remain culturally significant. QSR chains and retail in-store bakeries are growing steadily due to urbanization and rising demand for fresh, ready-to-eat bakery products. The fastest-growing end-use segment is frozen and par-baked manufacturers, supported by expanding global trade in semi-finished bakery goods and rising convenience food consumption. This segment is expected to grow at over 7% CAGR, significantly influencing overall market expansion.

Distribution Channel Insights

Direct B2B sales account for approximately 55% of global revenue, reflecting the technical nature of bread improvers and the need for customized formulations. Large industrial bakeries prefer direct collaboration with manufacturers for product optimization, technical trials, and performance benchmarking. Ingredient distributors play a critical role in emerging markets where small and medium-sized bakeries lack direct procurement capabilities. Contract blenders provide localized formulation solutions, particularly in Asia-Pacific and Latin America. Additionally, specialized ingredient platforms and digital B2B procurement systems are gradually emerging, especially in developed markets, improving supply chain efficiency and pricing transparency.

| By Product Type | By Form | By Application | By End-Use | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Europe

Europe leads the global bread improver market with approximately 32% share, driven by strong bakery traditions, high per capita bread consumption, and advanced enzyme innovation capabilities. Germany, France, the U.K., and Italy are major demand centers. Strict EU regulations on food additives have accelerated the shift toward enzyme-based clean-label improvers, strengthening regional demand. Additionally, Europe’s strong frozen and par-baked export industry significantly contributes to improver consumption. Continuous R&D investments and biotechnology advancements further reinforce regional leadership.

North America

North America accounts for nearly 28% of global revenue, led by the United States. High industrial bakery penetration, strong packaged sandwich bread consumption, and expanding frozen dough production drive regional growth. The clean-label movement is rapidly influencing reformulation strategies. Growth in QSR chains and private-label bakery products further increases demand for performance-enhancing improvers. Technological adoption in automated baking facilities also supports consistent market expansion.

Asia-Pacific

Asia-Pacific represents approximately 27% of global demand and is the fastest-growing region. China and India are primary growth engines due to urbanization, rising disposable incomes, and increasing adoption of Western-style packaged bread. Rapid expansion of modern retail and foodservice chains fuels demand for industrial bakery production. Additionally, flour quality variability across Southeast Asia encourages higher reliance on improvers for dough correction. Investments in domestic food processing infrastructure further accelerate regional growth.

Latin America

Latin America accounts for around 7% of global revenue, with Brazil and Mexico leading consumption. Growth is supported by increasing packaged bread demand, urban expansion, and wheat import dependency. Climatic variability impacts wheat quality, making flour correction through improvers increasingly important. Expanding supermarket chains and bakery franchising also contribute to regional demand.

Middle East & Africa

The Middle East & Africa represent approximately 6% of the global share. Saudi Arabia, the UAE, and South Africa are key markets. High reliance on wheat imports results in flour inconsistency, driving improver usage for quality standardization. Industrial bakery investments, population growth, and rising consumption of packaged bread products support steady demand. Infrastructure development and food security initiatives across Gulf countries further stimulate market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Bread Improver Market

- Lesaffre

- Puratos

- IFF

- DSM-Firmenich

- Kerry Group

- Corbion

- AB Mauri

- Bakels Worldwide

- Lallemand

- Angel Yeast

- Novozymes

- Mühlenchemie

- Fazer Ingredients

- Oriental Yeast

- Watson Inc.