Bread Crumbs Market Size

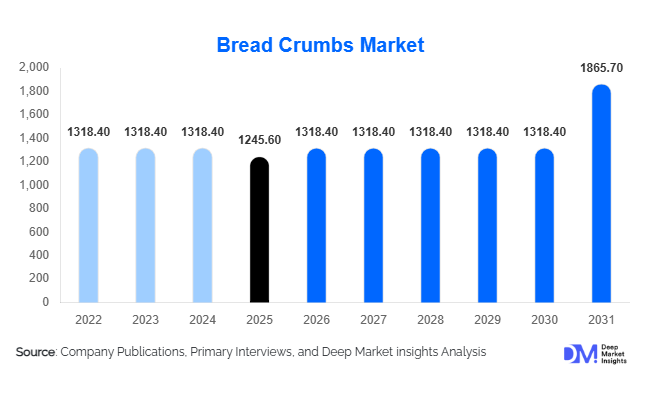

According to Deep Market Insights, the global bread crumbs market size was valued at USD 1,245.6 million in 2025 and is projected to grow from USD 1,335.28 million in 2026 to reach USD 1,890.37 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The market growth is supported by rising global consumption of processed and convenience foods, expanding quick-service restaurant (QSR) chains, and increasing adoption of coated and breaded food products across retail and foodservice sectors. Bread crumbs have evolved from a traditional bakery by-product into a specialized functional ingredient used for coating, binding, and texture enhancement across meat, seafood, plant-based foods, and ready-to-cook meals.

The global market is witnessing structural transformation as food manufacturers increasingly demand customized crumb textures, consistent granulation, and clean-label formulations. Industrial food processors are integrating standardized crumb solutions to improve frying efficiency, moisture retention, and product appearance. Meanwhile, growing urbanization and dual-income households are accelerating demand for frozen snacks, ready meals, and packaged foods, directly increasing bread crumb consumption. Asia-Pacific is emerging as a high-growth production hub due to expanding processed food manufacturing, while North America and Europe continue to lead in value consumption owing to mature foodservice ecosystems. Technological innovation in drying, grinding, and seasoning processes is enabling premium product differentiation, positioning bread crumbs as a strategic ingredient category within the global food ingredients industry.

Key Market Insights

- Processed and convenience food consumption is the primary growth catalyst, particularly frozen appetizers and coated meat products.

- Panko bread crumbs are gaining global popularity due to superior crispiness and premium positioning in foodservice applications.

- Foodservice channels account for the largest demand share, driven by global QSR expansion.

- Asia-Pacific is the fastest-growing production region, supported by rising industrial food manufacturing capacity.

- Clean-label and gluten-free crumbs are emerging as high-value niche segments.

- Automation and precision drying technologies are improving consistency and reducing production waste.

What are the latest trends in the bread crumbs market?

Premiumization Through Texture and Functional Customization

Food manufacturers increasingly demand bread crumbs engineered for specific cooking outcomes such as enhanced crunchiness, oil absorption control, and extended holding time after frying. Panko crumbs, coarse-texture crumbs, and specialty seasoned variants are gaining traction as restaurants and frozen food brands compete on product quality and sensory experience. Customized crumb blends designed for air frying and baked applications are also emerging, aligning with healthier cooking trends. Manufacturers are investing in controlled granulation technology to produce uniform particle size distribution, ensuring consistent coating adhesion across high-speed processing lines.

Shift Toward Clean Label and Allergen-Free Ingredients

Consumers increasingly prefer recognizable ingredients and allergen-conscious products, prompting manufacturers to develop gluten-free, whole-grain, and organic bread crumbs. Rice-based and corn-based crumbs are expanding in Western markets, while clean-label certifications are influencing procurement decisions among large food processors. Reduced sodium formulations and non-GMO ingredients are also becoming important differentiators. Retail brands are leveraging these attributes to position breaded products as healthier indulgence options without compromising texture.

What are the key drivers in the bread crumbs market?

Expansion of Quick-Service Restaurants and Frozen Foods

The rapid global expansion of QSR chains and frozen food consumption significantly drives bread crumb demand. Breaded chicken, seafood, cheese snacks, and plant-based nuggets require consistent coating materials for large-scale production. Global fast-food chains are standardizing coating systems across regions, boosting demand for industrial-grade crumbs. Increasing takeaway culture and online food delivery ecosystems further amplify consumption volumes.

Growth of Processed Protein and Plant-Based Foods

The rise of plant-based meat alternatives has created new applications for bread crumbs as binding and coating agents. Manufacturers use crumbs to replicate texture and mouthfeel comparable to traditional meat products. Expansion of alternative protein manufacturing across North America, Europe, and Asia has created incremental demand streams beyond conventional applications.

Industrial Automation in Food Processing

Modern food processing facilities require ingredients compatible with automated coating systems. Bread crumb producers are adopting advanced drying and milling technologies that deliver consistent particle size and moisture control, improving yield efficiency for processors. This compatibility with automation enhances operational efficiency, making standardized crumb products essential for industrial food production.

What are the restraints for the global market?

Volatility in Wheat and Bakery Raw Material Prices

Bread crumbs depend heavily on wheat flour and bakery surplus supply chains. Fluctuations in wheat prices driven by climate variability, geopolitical disruptions, and export restrictions directly impact production costs and margins. Producers often face pricing pressure due to long-term contracts with food manufacturers.

Shift Toward Low-Carbohydrate Diet Trends

Growing consumer awareness regarding carbohydrate intake may limit consumption of breaded foods in certain developed markets. Health-conscious consumers increasingly prefer grilled or minimally processed foods, compelling manufacturers to innovate healthier crumb formulations or diversify applications.

What are the key opportunities in the bread crumbs industry?

Expansion in Emerging Asian Food Processing Markets

Rapid urbanization and rising disposable incomes in countries such as India, Indonesia, Vietnam, and Thailand are accelerating demand for packaged and frozen foods. Governments promoting domestic food manufacturing are encouraging investments in processing facilities, creating strong demand for coating ingredients including bread crumbs. Localization of production reduces import dependence and enables regional customization of flavors and textures.

Gluten-Free and Specialty Ingredient Innovation

The gluten-free food category presents a high-margin opportunity. Manufacturers developing crumbs from alternative grains such as rice, quinoa, or millet can capture premium retail segments. Specialty crumbs targeting vegan, organic, and allergen-free product lines enable differentiation and higher pricing power.

Technological Integration and Value-Added Processing

Adoption of advanced drying technologies, automated grinding systems, and seasoning integration allows producers to supply ready-to-use functional ingredients rather than commodity crumbs. Integration of AI-based quality inspection and moisture monitoring enhances product consistency, strengthening partnerships with multinational food manufacturers.

Product Type Insights

The global bread crumbs market demonstrates strong diversification across product categories; however, panko bread crumbs continue to dominate the competitive landscape, accounting for nearly 34% of the global market share in 2025. The leadership of panko crumbs is primarily attributed to their unique structural characteristics, including a light, flaky texture and superior oil absorption control that enables crispier coatings compared to conventional crumbs. These functional advantages have made panko the preferred choice among food processors and quick-service restaurant (QSR) operators seeking consistent texture, enhanced visual appeal, and improved mouthfeel in fried products. As consumer expectations shift toward restaurant-quality textures in packaged and frozen foods, manufacturers increasingly adopt panko crumbs for applications ranging from breaded shrimp and chicken tenders to premium appetizers and plant-based alternatives.The growth of panko bread crumbs is further supported by the globalization of Asian culinary influences, particularly Japanese-style frying techniques that emphasize lightness and crunch. Food manufacturers across North America and Europe have integrated panko coatings into ready-to-cook and ready-to-eat offerings to differentiate products in highly competitive frozen food categories. Additionally, advancements in automated coating equipment have enabled large-scale adoption of panko crumbs without compromising production efficiency, strengthening their dominance in industrial processing environments. Rising consumer demand for premiumization within convenience foods continues to reinforce the leading position of this segment.Traditional dry bread crumbs remain a significant contributor to market revenue, supported by their affordability, versatility, and widespread use as binding agents in processed meat products such as meatballs, patties, sausages, and meatloaf formulations. Food processors favor dry crumbs due to their consistent particle size, extended shelf life, and ability to improve moisture retention while reducing formulation costs. In developing markets, where cost sensitivity remains high, dry bread crumbs continue to represent a practical ingredient solution for both industrial and household applications. Their adaptability across cuisines ensures steady baseline demand despite the premiumization trend observed in developed economies.Seasoned bread crumbs are emerging as one of the fastest-expanding product categories, driven by consumer demand for convenience-oriented cooking solutions. Pre-seasoned formulations infused with herbs, spices, cheese flavors, or regional seasonings reduce preparation time for households while ensuring flavor consistency. Retail brands increasingly launch customized seasoning blends aligned with regional tastes, enabling product differentiation and higher profit margins. The growing popularity of home cooking, fueled by digital recipe platforms and culinary experimentation, continues to accelerate adoption of seasoned crumbs across supermarkets and e-commerce platforms. Collectively, product innovation, texture optimization, and premium culinary positioning remain central drivers shaping product type evolution within the bread crumbs market.

Application Insights

Coating and breading applications represent the largest application segment, accounting for approximately 46% of global demand in 2025, and serve as the primary growth engine for the bread crumbs industry. The dominance of this segment is closely linked to the rapid expansion of frozen foods, processed poultry products, seafood items, and ready-to-fry snacks worldwide. Bread crumbs function as a critical coating component that enhances texture, protects moisture during cooking, and improves visual appeal, all of which are essential characteristics in large-scale commercial food production. As consumer lifestyles increasingly favor convenience foods requiring minimal preparation time, manufacturers continue to scale up breaded product portfolios, directly stimulating crumb consumption.The leading driver for coating and breading applications lies in the global proliferation of quick-service restaurants and takeaway culture. Fried chicken, breaded seafood, mozzarella sticks, and coated vegetable snacks have become staple menu items across international food chains. Consistency in texture and performance during high-volume cooking environments necessitates standardized coating ingredients, positioning bread crumbs as an indispensable processing input. Technological innovations in pre-dusting, battering, and coating systems further enhance product adhesion and cooking efficiency, strengthening demand within industrial manufacturing lines.Binding and filler applications maintain stable and resilient demand across processed meat production. Bread crumbs are widely used to improve product structure, enhance juiciness, and reduce raw material costs without compromising taste or texture. This functionality is particularly important in value-added meat products where manufacturers aim to balance affordability with sensory quality. Increasing consumption of processed protein foods in emerging economies continues to sustain this application segment, ensuring consistent long-term growth.Stuffing and topping applications are experiencing moderate expansion, supported by rising interest in home cooking and diversified culinary experimentation. Consumers increasingly use bread crumbs as toppings for casseroles, baked vegetables, pasta dishes, and gratins, particularly across Western markets. The popularity of recipe-sharing platforms and cooking tutorials has broadened awareness of crumb-based culinary applications, encouraging retail purchases. Although smaller in volume compared to coating uses, this segment contributes to product diversification and retail channel growth.Additionally, emerging applications in plant-based and hybrid protein products are creating new demand pathways. Bread crumbs improve texture and structural integrity in meat alternatives, helping replicate traditional meat mouthfeel. As plant-based innovation accelerates globally, crumb formulations tailored for vegan and allergen-free applications are expected to gain importance, expanding the functional scope of the market.

Distribution Channel Insights

The bread crumbs market remains heavily influenced by industrial procurement dynamics, with business-to-business (B2B) supply channels accounting for nearly 62% of global revenue in 2025. Large food manufacturers represent the backbone of demand, purchasing bread crumbs in bulk quantities for automated production lines. Industrial buyers prioritize consistency, cost efficiency, and supply reliability, prompting suppliers to invest in large-scale manufacturing capabilities and standardized quality control systems. Long-term supply contracts between crumb producers and frozen food manufacturers further reinforce the dominance of this distribution channel.The leading driver behind B2B dominance is the continuous expansion of processed food manufacturing worldwide. As frozen meals, ready-to-cook snacks, and breaded protein products gain popularity, industrial processors require stable ingredient sourcing to maintain uninterrupted production. Automation trends in food processing also favor standardized crumb products designed for compatibility with high-speed coating equipment. Consequently, industrial partnerships and private-label manufacturing arrangements remain central to market growth.Retail distribution channels, including supermarkets, hypermarkets, and online grocery platforms, are witnessing steady expansion driven by evolving consumer cooking habits. Increased interest in convenient meal preparation and experimentation with restaurant-style recipes at home has elevated demand for packaged bread crumbs. Manufacturers are introducing smaller pack sizes, resealable packaging, and premium flavor variants tailored for household consumption. E-commerce platforms further accelerate accessibility, allowing consumers to explore diverse crumb varieties previously limited to professional kitchens.Foodservice distribution continues to play a vital supporting role, supplying restaurants, catering companies, and institutional kitchens. The recovery and expansion of hospitality industries globally have restored demand volumes following pandemic-related disruptions. Foodservice operators rely on bulk crumb supplies to ensure consistency across menu offerings, particularly for fried and baked dishes requiring uniform coating performance. Growth in cloud kitchens and delivery-focused restaurant models is also contributing to sustained demand through this channel.

End-Use Insights

Food processing manufacturers represent the largest end-use segment, accounting for approximately 48% of total market share in 2025. The leadership of this segment is primarily driven by the global expansion of frozen foods and convenience meal categories, which rely heavily on bread crumbs for coating, binding, and texture enhancement. Industrial processors benefit from the functional versatility of bread crumbs, enabling cost optimization while maintaining product quality. The rapid growth of ready-to-eat and ready-to-cook food categories across urban populations continues to strengthen demand from this end-use group.The primary driver supporting food processing manufacturers is large-scale industrialization of food production combined with increasing consumer reliance on packaged meals. Urbanization, dual-income households, and time-constrained lifestyles encourage consumption of frozen snacks and prepared foods, indirectly boosting crumb utilization. Manufacturers also increasingly develop customized crumb blends optimized for specific cooking methods such as air frying or oven baking, reflecting changing consumer preferences toward healthier preparation techniques.Quick-service restaurants represent the fastest-growing end-use segment as global fried food consumption expands. International and regional QSR chains continuously introduce new breaded menu items to attract consumers seeking indulgent yet affordable dining experiences. Standardized crumb coatings ensure consistent product quality across franchise locations, making bread crumbs a critical operational ingredient. Expansion of delivery services and digital ordering ecosystems further supports restaurant-driven demand growth.Household consumption is increasing gradually as consumers experiment with cooking solutions that replicate restaurant-quality meals at home. Packaged meal kits, recipe-based cooking trends, and growing culinary awareness encourage retail purchases of bread crumbs. Although smaller compared to industrial usage, household adoption plays an important role in brand visibility and product innovation.Emerging applications within plant-based protein manufacturing are expected to reshape future demand dynamics. Bread crumbs enhance texture and structural cohesion in alternative protein formulations, supporting innovation within vegetarian and vegan food categories. As sustainability and alternative protein adoption accelerate globally, crumb manufacturers are likely to develop specialized formulations catering to evolving dietary preferences.

| By Product Type | By Application | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for nearly 29% of the global bread crumbs market in 2025, with the United States serving as the primary consumption hub. The region’s dominance is largely driven by high penetration of frozen foods, widespread adoption of convenience meals, and the extensive presence of quick-service restaurant chains. Consumers demonstrate strong preference for breaded poultry, seafood, and snack products, encouraging food manufacturers to maintain large-scale crumb procurement. Advanced food processing infrastructure and well-established cold chain logistics further enable efficient production and distribution of breaded products.Regional growth is supported by continuous product innovation within frozen food categories, including premium coated products and healthier oven-ready options. Increasing demand for air-fryer-compatible foods has also encouraged manufacturers to develop specialized crumb coatings optimized for reduced oil cooking. Canada contributes steady growth through its robust seafood processing industry and expanding packaged food sector. Additionally, rising interest in plant-based alternatives across North America is creating new opportunities for crumb suppliers to develop gluten-free and vegan formulations aligned with changing dietary preferences.

Europe

Europe held approximately 26% of global market share in 2025, supported by strong culinary traditions and mature processed food industries. Countries such as Germany, the United Kingdom, France, Italy, and Spain represent major consumption centers due to their established bakery cultures and high demand for coated meat and seafood products. Bread crumbs are widely integrated into traditional recipes as well as modern convenience foods, ensuring consistent regional demand.Regional growth drivers include stringent clean-label regulations and increasing consumer preference for natural and organic ingredients. European manufacturers are actively reformulating crumb products using simplified ingredient lists, whole grain bases, and allergen-conscious formulations to comply with regulatory standards and consumer expectations. Premiumization trends also encourage development of artisanal-style crumbs with unique textures and flavors. Expansion of private-label retail brands across supermarkets further accelerates market penetration by offering affordable yet high-quality crumb products.The strong presence of foodservice culture, including casual dining and bakery cafés, supports stable demand across hospitality channels. Sustainability initiatives across Europe also encourage manufacturers to optimize production efficiency and reduce food waste, indirectly influencing ingredient sourcing patterns and innovation strategies.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by rapid urbanization, rising disposable incomes, and expanding processed food manufacturing industries. Japan remains a key producer and exporter of panko bread crumbs, contributing technological expertise and product innovation to global markets. Meanwhile, China and India are experiencing significant growth in frozen food production and quick-service restaurant expansion, creating substantial demand for coating ingredients.The region’s growth is fueled by changing dietary habits as consumers increasingly adopt Western-style convenience foods alongside traditional cuisines. Rapid expansion of retail infrastructure and modern supermarkets improves accessibility to packaged ingredients, supporting household adoption. Additionally, increasing investment in food processing facilities across Southeast Asia enhances local production capacity, reducing dependence on imports and stimulating regional supply chains.The proliferation of international restaurant brands and delivery platforms has accelerated demand for breaded snacks and fried menu items across urban centers. Population growth combined with a rising middle class further strengthens long-term consumption potential. As manufacturers introduce localized seasoning variants tailored to regional tastes, Asia-Pacific is expected to remain the most dynamic growth engine for the global bread crumbs market.

Middle East & Africa

Demand across the Middle East and Africa is expanding steadily, supported by growth in hospitality, tourism, and foodservice industries. Countries such as the United Arab Emirates and Saudi Arabia are witnessing rapid restaurant expansion driven by tourism development and urban lifestyle changes. Increasing consumption of fried chicken and breaded seafood dishes contributes to rising crumb utilization across commercial kitchens.Regional growth is also supported by rising imports of frozen foods and expanding domestic food processing capabilities. South Africa leads African market development due to its comparatively advanced food manufacturing sector and growing retail distribution networks. Urbanization and changing dietary patterns encourage adoption of convenience foods, gradually strengthening demand for bread crumbs across both industrial and household segments.Government initiatives aimed at improving food security and local production are encouraging investment in food processing infrastructure, which is expected to further enhance regional market growth over the forecast period.

Latin America

Latin America demonstrates strong growth potential, with Brazil and Mexico serving as primary demand centers. The region’s expanding poultry processing industry represents a key driver, as bread crumbs are extensively used in coated chicken products destined for both domestic consumption and export markets. Rising fast-food consumption and increasing urbanization further stimulate demand for breaded snacks and ready-to-cook meals.Export-oriented meat processing facilities play a crucial role in sustaining industrial crumb demand, particularly as Latin American producers strengthen their presence in global protein trade. Improvements in cold chain infrastructure and retail modernization are enhancing product availability across supermarkets, supporting gradual growth in household consumption. Additionally, economic recovery trends and increasing consumer spending on convenience foods are expected to reinforce regional expansion throughout the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Bread Crumbs Market

- Upper Crust Enterprises Inc.

- Kikkoman Corporation

- Yamazaki Baking Co., Ltd.

- George DeLallo Company

- 4C Foods Corp.

- La Lorraine Bakery Group

- Gonnella Baking Company

- Bauducco Foods Inc.

- Bakels Worldwide

- Grissol Food Products

- Edward & Sons Trading Company

- JFC International Inc.

- Pereg Natural Foods

- General Mills Inc.

- Ajinomoto Co., Inc.