Brazzein Market Size

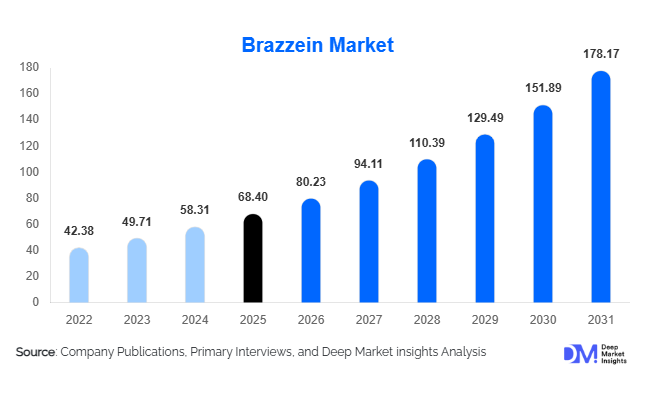

According to Deep Market Insights, the global brazzein market size was valued at USD 68.4 million in 2025 and is projected to grow from USD 80.23 million in 2026 to reach USD 178.17 million by 2031, expanding at a CAGR of 17.3% during the forecast period (2026–2031). The brazzein market growth is primarily driven by increasing global demand for natural high-intensity sweeteners, rapid reformulation efforts by food and beverage manufacturers to reduce sugar content, and regulatory pressure supporting clean-label and low-calorie ingredients. Brazzein, a plant-derived sweet protein originally discovered in Pentadiplandra brazzeana fruit, is gaining commercial momentum due to its superior sweetness profile, thermal stability, and compatibility with diverse food processing applications.

Key Market Insights

- Brazzein adoption is accelerating in sugar-reduction formulations across beverages, dairy alternatives, and functional nutrition products.

- Biotechnology-based fermentation production is enabling scalable commercialization and lowering production costs.

- North America leads commercialization due to strong demand for natural sweeteners and clean-label innovation.

- Asia-Pacific is the fastest-growing market, supported by rising diabetes awareness and expanding processed food consumption.

- Food & beverage manufacturers are shifting away from artificial sweeteners toward protein-based sweeteners with improved taste profiles.

- Precision fermentation and synthetic biology are reshaping ingredient manufacturing economics.

What are the latest trends in the brazzein market?

Shift Toward Protein-Based Sweeteners

The sweetener industry is undergoing structural transformation as food manufacturers transition from synthetic sweeteners toward naturally derived protein sweeteners. Brazzein stands out due to its clean taste, absence of bitterness, and extremely high sweetness intensity compared to sugar. Unlike stevia or monk fruit, brazzein provides a sugar-like sensory profile, enabling broader adoption in beverages and dairy formulations. Increasing consumer preference for recognizable ingredients and reduced artificial additives is encouraging global brands to experiment with brazzein-based formulations. Product launches incorporating brazzein blends are expanding particularly in zero-sugar beverages and functional foods.

Precision Fermentation Enabling Commercial Scale

Commercial production of brazzein has historically been constrained by limited natural extraction. Recent advances in precision fermentation and recombinant protein expression are transforming supply scalability. Biotechnology companies are engineering yeast and microbial platforms capable of producing brazzein efficiently at industrial scale. This technological shift is lowering production costs, improving supply consistency, and enabling regulatory approvals across major markets. As fermentation infrastructure expands globally, brazzein is transitioning from a niche innovation ingredient into a commercially viable sweetener alternative.

What are the key drivers in the brazzein market?

Global Sugar Reduction Policies

Governments worldwide are implementing sugar taxes and labeling regulations to combat obesity and diabetes. These policies are encouraging food manufacturers to reformulate products using low-calorie alternatives. Brazzein offers a strong advantage because very small quantities deliver high sweetness without glycemic impact, making it attractive for compliance-driven reformulation strategies.

Rising Demand for Clean-Label Ingredients

Consumers increasingly demand natural ingredients with minimal processing. Brazzein’s plant-origin positioning and protein-based composition align strongly with clean-label trends. Food companies are leveraging brazzein to replace artificial sweeteners while maintaining flavor quality, supporting premium product positioning.

Expansion of Functional and Health Foods

The rapid growth of functional beverages, sports nutrition, and diabetic-friendly foods is accelerating brazzein adoption. Manufacturers are integrating brazzein into protein shakes, nutraceutical drinks, and wellness foods where calorie reduction and taste optimization are critical.

What are the restraints for the global market?

High Production Costs

Despite fermentation advancements, brazzein production remains more expensive than conventional sweeteners. Scaling bioreactor capacity and downstream purification technologies remains essential to achieving price competitiveness.

Regulatory Approval Complexity

Novel protein ingredients require extensive safety validation across regulatory jurisdictions. Approval timelines in Europe and certain Asian markets may slow commercialization compared with established sweeteners.

What are the key opportunities in the brazzein industry?

Reformulation of Global Beverage Portfolios

Major beverage companies are actively reformulating portfolios to reduce sugar content while maintaining taste. Brazzein’s thermal stability and clean sweetness enable application in carbonated drinks, flavored waters, and ready-to-drink teas. Large-scale adoption by multinational beverage brands could rapidly expand market size.

Expansion into Medical and Diabetic Nutrition

Rising global diabetes prevalence creates strong opportunities for brazzein-based sweetening solutions in medical nutrition and specialized dietary foods. Brazzein’s zero-glycemic response positions it as a preferred ingredient for clinical nutrition products and elderly dietary solutions.

Emerging Market Demand and Localization

Developing economies in Asia-Pacific and Latin America are witnessing rapid growth in low-sugar packaged foods. Local manufacturing partnerships and fermentation facilities present opportunities for new entrants to capture regional demand while reducing logistics costs.

Product Type Insights

The global brazzein market is primarily dominated by fermentation-derived brazzein, which accounts for approximately 72% of total global revenue in 2025. The strong leadership of fermentation-based production is attributed to its superior scalability, cost efficiency, and ability to deliver highly consistent sweetness profiles compared with traditional plant extraction methods. Fermentation technology enables controlled production environments, reducing variability associated with agricultural cultivation, seasonal supply fluctuations, and raw material limitations. As food and beverage manufacturers increasingly require standardized ingredients for large-scale commercial formulations, fermentation-derived brazzein has emerged as the preferred solution. Additionally, advancements in precision fermentation and synthetic biology are improving yield efficiency and lowering production costs, further reinforcing this segment’s dominance. The growing demand for sustainable ingredient sourcing also supports fermentation adoption, as it significantly reduces land usage and environmental impact relative to plant harvesting.In terms of format, powdered brazzein leads application usage, capturing nearly 61% market share due to its versatility and compatibility across multiple industrial applications. Powdered formats offer extended shelf stability, simplified transportation logistics, and easy integration into dry mixes, bakery premixes, powdered beverages, and nutritional supplements. Manufacturers favor powdered brazzein for its uniform dispersion and formulation flexibility, especially in large-scale food processing environments. Meanwhile, liquid brazzein formulations are gaining increasing traction, particularly within beverage syrups, concentrates, and ready-to-drink (RTD) products. Liquid formats allow faster solubility, precise dosing, and seamless blending in high-throughput beverage manufacturing systems. As RTD beverages and functional drinks continue expanding globally, liquid brazzein adoption is expected to accelerate, supporting diversification within product formats while maintaining powdered variants as the leading segment.

Application Insights

Food and beverage applications represent the largest share of the global brazzein market, contributing nearly 64% of total demand in 2025. The dominance of this segment is primarily driven by the accelerating global transition toward sugar reduction and calorie-conscious consumption patterns. Beverage manufacturers are increasingly reformulating carbonated drinks, flavored waters, dairy beverages, and plant-based alternatives to meet consumer demand for natural, zero-calorie sweeteners without the bitterness or aftertaste commonly associated with artificial sweeteners. Brazzein’s high sweetness potency and clean sensory profile make it particularly suitable for premium reformulations where taste retention is critical. The rapid growth of zero-sugar beverages, functional hydration products, and clean-label packaged foods continues to strengthen adoption across multinational brands.Nutraceutical applications account for approximately 18% market share, supported by rising consumer focus on preventive healthcare and functional nutrition. Brazzein is increasingly incorporated into protein powders, dietary supplements, and wellness beverages, where manufacturers seek natural sweetness solutions compatible with health-oriented positioning. Its stability under varying pH and temperature conditions enhances suitability for fortified formulations. Pharmaceutical and medical nutrition applications are emerging as high-potential growth areas, particularly in diabetic-friendly products, pediatric nutrition, and therapeutic dietary solutions. As healthcare systems emphasize sugar management and metabolic health, brazzein’s ability to provide sweetness without glycemic impact positions it as an attractive ingredient for specialized nutrition markets.

Distribution Channel Insights

Direct B2B ingredient supply remains the dominant distribution channel, accounting for nearly 70% of the global market. Large ingredient manufacturers and biotechnology companies primarily supply brazzein directly to multinational food and beverage producers through long-term supply agreements and formulation partnerships. This direct sourcing model ensures consistent quality assurance, regulatory compliance, and customized formulation support, all of which are essential for large-scale product reformulations. Strategic collaboration between ingredient innovators and major consumer brands further accelerates commercialization and drives adoption across global product portfolios.Specialty ingredient distributors represent approximately 22% of market share and play a critical role in expanding market penetration among small and mid-sized manufacturers. These distributors provide technical guidance, smaller batch availability, and regional regulatory expertise, enabling emerging brands to experiment with next-generation sweeteners. As innovation increasingly shifts toward niche health-focused products and startup-driven food innovation, specialty distribution networks are expected to gain importance in supporting broader adoption across diverse geographic markets.

End-Use Industry Insights

The beverage industry represents the fastest-growing end-use segment, expanding at nearly 19% CAGR, and serves as the primary growth engine for brazzein demand. Global regulatory pressure to reduce sugar consumption, combined with rising consumer awareness regarding obesity and metabolic disorders, is forcing beverage companies to reformulate legacy products. Brazzein provides a compelling alternative due to its natural origin, high sweetness intensity, and minimal aftertaste, allowing manufacturers to maintain flavor integrity while reducing sugar content. The global functional beverage industry, valued at over USD 200 billion, continues to expand rapidly, directly supporting ingredient innovation and adoption.Dairy alternatives and plant-based foods also represent strong growth avenues as producers seek improved sweetness solutions that complement plant proteins without masking flavors. Brazzein’s compatibility with plant-based formulations enhances taste optimization in oat, almond, and soy-based products. Additionally, export-driven demand is increasing as multinational food companies standardize low-sugar product formulations across regions to align with global health strategies. This harmonization of product portfolios is accelerating ingredient adoption at scale and creating long-term growth opportunities across multiple food categories.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

North America

North America accounted for approximately 38% of the global brazzein market in 2025, with the United States leading regional demand due to its advanced food innovation ecosystem and strong consumer adoption of clean-label products. The region benefits from a mature biotechnology sector, significant investment in precision fermentation technologies, and an established functional food industry. Regulatory openness toward novel food ingredients and Generally Recognized as Safe (GRAS) pathways enable faster commercialization compared with many global markets. Increasing reformulation of carbonated beverages, sports drinks, and nutritional products to meet sugar-reduction targets remains a primary growth driver. Additionally, rising healthcare costs associated with obesity and diabetes are encouraging both policymakers and manufacturers to promote reduced-sugar alternatives, accelerating brazzein adoption across mainstream consumer products.

Europe

Europe holds nearly 24% market share, supported by strong regulatory and consumer momentum toward healthier food systems. Countries such as Germany, France, and the United Kingdom are leading adoption as governments implement sugar taxes, front-of-pack labeling requirements, and nutritional reformulation targets. European consumers demonstrate high preference for natural and sustainably sourced ingredients, aligning closely with brazzein’s positioning as a plant-inspired protein sweetener. Although regulatory approvals for novel ingredients often progress gradually, once authorized, adoption tends to scale rapidly due to strict compliance frameworks and retailer-driven clean-label standards. Growth is further supported by innovation in plant-based foods and premium functional beverages across Western Europe.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 20% CAGR, driven by rapid urbanization, expanding middle-class populations, and rising awareness of lifestyle-related health conditions. China, Japan, South Korea, and India serve as major demand centers due to increasing diabetes prevalence and strong growth in processed and convenience food sectors. Regional manufacturers are actively adopting next-generation sweeteners to differentiate premium and health-focused product offerings. Government initiatives promoting sugar reduction and healthier diets are further accelerating reformulation trends. Additionally, the region’s large-scale beverage manufacturing base and increasing investment in food biotechnology innovation are expected to significantly expand production capacity and market accessibility for brazzein over the forecast period.

Middle East & Africa

The Middle East & Africa market is experiencing gradual but steady expansion, supported by high rates of diabetes and obesity across Gulf Cooperation Council countries. Government-led public health initiatives encouraging sugar reduction are driving demand for alternative sweetening solutions. The United Arab Emirates and Saudi Arabia are emerging as early adopters, particularly within functional beverages, premium packaged foods, and wellness-oriented product categories. Rising disposable incomes, expanding modern retail infrastructure, and increasing awareness of preventive health nutrition are further contributing to regional growth. Import-driven ingredient supply chains currently dominate the market, but growing investment in food innovation hubs may strengthen local adoption in the coming years.

Latin America

Latin America is witnessing increasing adoption led by Brazil and Mexico, where sugar tax policies and public health campaigns are reshaping beverage and packaged food formulations. Multinational beverage companies operating in the region are actively introducing reduced-calorie and zero-sugar product variants to comply with evolving regulatory frameworks. Growing urban populations and rising demand for affordable healthier alternatives are encouraging manufacturers to explore high-intensity natural sweeteners such as brazzein. Although price sensitivity remains a moderating factor, improvements in production efficiency and supply availability are expected to gradually enhance market penetration across regional food and beverage industries.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Brazzein Market

- Ingredion Incorporated

- Sweegen Inc.

- Conagen Inc.

- Ginkgo Bioworks

- Amyris Inc.

- Cargill Incorporated

- ADM (Archer Daniels Midland)

- Tate & Lyle PLC

- Ajinomoto Co., Inc.

- DSM-Firmenich

- MycoTechnology Inc.

- Codexis Inc.

- Evonik Industries AG

- Kerry Group plc

- Roquette Frères