Bottled Water Testing Equipment Market Size

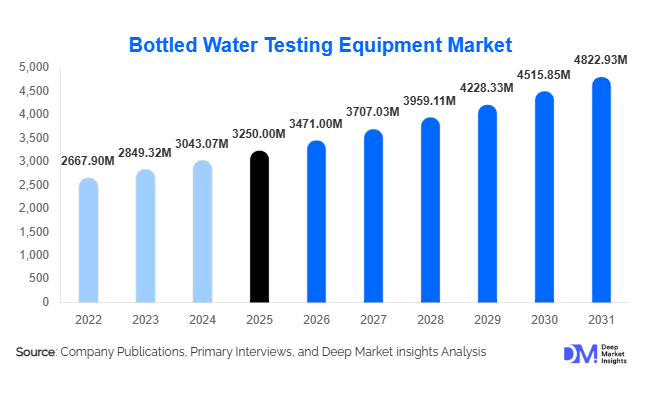

According to Deep Market Insights, the global bottled water testing equipment market size was valued at USD 3,250 million in 2025 and is projected to grow from USD 3,471.00 million in 2026 to reach USD 4,822.93 million by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The bottled water testing equipment market growth is primarily driven by tightening global water quality regulations, increasing bottled water consumption worldwide, and rising investments by manufacturers in advanced laboratory automation and contaminant detection technologies.

Key Market Insights

- Microbiological testing equipment accounts for nearly 32% of the total market share, driven by mandatory pathogen testing across all production batches.

- Spectroscopy-based systems (ICP-MS, Atomic Absorption) hold approximately 28% share, supported by stringent heavy metal monitoring regulations.

- North America dominates with about 34% market share in 2025, led by strong FDA and EPA compliance requirements.

- Asia-Pacific is the fastest-growing region, expanding at nearly 7.8% CAGR due to rising bottled water exports and regulatory tightening.

- The top five companies collectively account for around 52% of global revenue, reflecting moderate market consolidation.

- Automation and real-time inline monitoring systems are gaining adoption, particularly among large multinational bottled water brands.

What are the latest trends in the bottled water testing equipment market?

Rising PFAS and Emerging Contaminant Monitoring

Recent regulatory updates in the United States and Europe have significantly lowered permissible limits for per- and polyfluoroalkyl substances (PFAS) in drinking and bottled water. As a result, manufacturers are upgrading laboratory infrastructure with LC-MS/MS and high-resolution chromatography systems capable of detecting contaminants at parts-per-trillion levels. Demand for advanced trace analysis solutions is increasing, particularly among export-oriented producers seeking compliance with multi-regional standards. Equipment suppliers are responding by introducing bundled contaminant panels that simultaneously detect heavy metals, pesticides, and organic residues, improving testing efficiency while reducing per-sample costs.

Shift Toward Automated and Inline Testing Systems

Bottled water manufacturers are increasingly investing in semi-automated and fully automated testing platforms to reduce turnaround time and labor dependency. Inline sensors measuring pH, turbidity, conductivity, and total dissolved solids (TDS) are being integrated directly into production lines, enabling real-time quality control. Fully automated multi-parameter analyzers are particularly popular among large-scale bottlers, helping reduce human error and improve batch traceability. Digital dashboards, cloud-based compliance reporting, and AI-enabled data analytics are further transforming laboratory workflows, aligning with Industry 4.0 initiatives across food and beverage manufacturing.

What are the key drivers in the bottled water testing equipment market?

Strengthening Global Water Quality Regulations

Regulatory frameworks such as FDA bottled water standards, the EU Drinking Water Directive (2020/2184), and WHO guidelines are compelling manufacturers to adopt high-precision analytical systems. Frequent revisions to contaminant thresholds, especially for heavy metals and emerging pollutants, have increased testing frequency and equipment replacement cycles. Compliance requirements for exports further amplify demand for internationally accredited laboratory infrastructure.

Rising Global Bottled Water Production

Global bottled water production surpassed 350 billion liters in 2025 and continues expanding at over 5% annually. Higher production volumes directly correlate with increased batch testing, microbiological screening, and chemical analysis. Growth in premium, functional, and mineral water segments further necessitates comprehensive testing to validate product purity claims and brand positioning.

What are the restraints for the global market?

High Capital Investment Costs

Advanced systems such as ICP-MS and LC-MS/MS instruments range between USD 150,000 and USD 400,000 per unit. For small and medium-scale bottled water producers, such capital expenditures can be prohibitive. Although financing models and leasing programs are emerging, upfront costs remain a key adoption barrier in developing economies.

Shortage of Skilled Laboratory Professionals

Operation and calibration of high-end chromatography and spectroscopy equipment require trained chemists and microbiologists. Emerging markets often face workforce gaps, limiting optimal utilization of installed systems. Training and certification requirements further increase operational costs for producers.

What are the key opportunities in the bottled water testing equipment industry?

Export-Oriented Compliance Upgrades

Countries such as China, Mexico, Turkey, and the UAE are expanding bottled water exports to North America and Europe. Export certification demands adherence to multi-regional safety standards, driving investments in internationally accredited testing laboratories. Equipment vendors offering turnkey compliance solutions, calibration services, and digital audit support stand to benefit from this export-driven demand.

Rapid Microbiological Testing and Molecular Diagnostics

Rapid PCR-based testing platforms are emerging as high-growth sub-segments. Compared to traditional culture methods, PCR significantly reduces detection time for pathogens such as E. coli and Salmonella. Faster turnaround enhances production efficiency and reduces storage costs. This technological shift is expected to accelerate replacement demand over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3250 Million |

| Market Size in 2026 | USD 3471 Million |

| Market Size in 2031 | USD 4822.93 Million |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Equipment Type Insights

Microbiological testing equipment leads the bottled water testing equipment market with approximately 32% share in 2025, primarily due to mandatory pathogen screening requirements across all bottled water production batches globally. Regulatory authorities such as the FDA, EFSA, and WHO require routine monitoring for contaminants, including E. coli, coliform bacteria, Salmonella, and Legionella, making microbiological testing non-discretionary. The rise in contamination-related recalls and increasing consumer sensitivity toward waterborne pathogens further reinforce investment in rapid microbial detection platforms. Additionally, the growing adoption of PCR-based rapid testing systems is accelerating replacement demand within this segment.

Chemical and contaminant analysis systems represent the second-largest revenue contributor, particularly driven by heavy metal detection requirements for arsenic, lead, mercury, and cadmium. With tightening PFAS regulations and revised permissible thresholds across North America and Europe, demand for high-sensitivity chemical analysis equipment such as ICP-MS and LC-MS/MS systems is rising steadily.

Technology Platform Insights

Spectroscopy technologies, including ICP-MS and atomic absorption systems, hold nearly 28% of the market share, making them the leading technology platform in 2025. Their dominance is driven by increasing heavy metal and trace contaminant monitoring mandates requiring parts-per-billion and parts-per-trillion detection capabilities. As regulatory thresholds continue to decline globally, high-precision spectroscopy systems remain indispensable for compliance-driven laboratories. Chromatography platforms such as HPLC, GC, and ion chromatography are extensively used for organic contaminant detection, including pesticides, volatile organic compounds (VOCs), and PFAS compounds. The rise in multi-residue contaminant screening requirements has strengthened demand for advanced chromatography systems integrated with mass spectrometry.

PCR and molecular diagnostic systems are among the fastest-growing technology categories, supported by demand for faster microbial detection turnaround times. Compared to traditional culture-based methods, PCR significantly reduces testing cycles from 24–72 hours to a few hours, enhancing production throughput and reducing inventory holding costs. Biosensors and rapid detection kits are increasingly adopted in semi-automated laboratory setups, particularly in emerging markets where cost-effective and portable solutions are preferred. These technologies provide scalable options for small and mid-sized producers transitioning toward improved compliance standards.

End-Use Insights

Bottled water manufacturers account for approximately 48% of overall demand, making them the leading end-use segment. The primary driver for this dominance is the growing internalization of quality control processes by multinational brands seeking brand protection, traceability, and faster compliance reporting. Large-scale producers are investing heavily in in-house laboratories equipped with automated and integrated multi-parameter systems to reduce reliance on third-party labs and improve operational efficiency.

Third-party testing laboratories are growing at nearly 7.5% annually, driven by outsourcing trends among small and mid-sized producers that lack capital for high-end equipment investments. Accreditation requirements and export certifications further strengthen this segment. Government and regulatory laboratories generate steady baseline demand due to periodic compliance audits and environmental monitoring programs. Meanwhile, contract manufacturing facilities and private-label producers are upgrading laboratory capabilities to meet stringent retailer-driven quality benchmarks, especially in North America and Europe.

Explore more data points, trends and opportunities Download Free Sample Report

Bottled Water Testing Equipment Market Segmentations

By Equipment Type

- Microbiological Testing Equipment

- Chemical & Contaminant Analysis Equipment

- Physical Parameter Testing Equipment

- Radiological Testing Equipment

- Integrated & Multi-Parameter Testing Systems

By Technology Platform

- Spectroscopy

- Chromatography

- PCR & Molecular Diagnostic Systems

- Biosensors & Rapid Detection Kits

- Traditional Culture & Membrane Filtration Methods

By End Use

- Bottled Water Manufacturers

- Third-Party Testing Laboratories

- Government & Regulatory Laboratories

- Contract Manufacturing & Private Label Facilities

By Automation Level

- Manual Laboratory Equipment

- Semi-Automated Systems

- Fully Automated & Online Monitoring Systems

By Distribution Channel

- Direct Sales

- Authorized Distributors

- Online Scientific Equipment Platforms

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, with the United States alone contributing nearly 30% of total global demand. The region’s dominance is driven by strict FDA oversight, EPA regulatory enforcement, and aggressive PFAS monitoring initiatives. Increasing state-level legislation mandating lower contaminant thresholds is accelerating laboratory modernization across bottled water plants. Additionally, high bottled water per capita consumption in the U.S., combined with frequent product recalls and strong litigation risks, compels manufacturers to invest in advanced testing technologies. Canada demonstrates steady growth supported by environmental testing reforms, water safety awareness, and export quality control requirements.

Europe

Europe accounts for approximately 28% of global market share, led by Germany, France, Italy, and the UK. The implementation of the revised EU Drinking Water Directive has strengthened heavy metal, pesticide, and emerging contaminant monitoring requirements. European producers are also early adopters of laboratory automation and digital compliance documentation systems, aligning with sustainability and traceability objectives. Growing consumer demand for mineral and premium bottled water products further drives sophisticated testing infrastructure investments across the region.

Asia-Pacific

Asia-Pacific represents nearly 26% of global demand and is the fastest-growing region at approximately 7.8% CAGR. China leads regional demand due to its large-scale bottled water production and export orientation. Increasing government scrutiny over food and beverage safety standards is pushing domestic producers to upgrade testing infrastructure. India is witnessing rapid expansion driven by rising packaged water consumption, urbanization, and improving regulatory enforcement. Japan and South Korea maintain stable demand supported by stringent quality benchmarks and advanced manufacturing ecosystems.

Middle East & Africa

The Middle East & Africa region contributes around 8% of the global market share. The UAE and Saudi Arabia are key growth engines, driven by heavy reliance on desalinated water bottling and strong investments in premium water brands. Tourism expansion and luxury hospitality growth in the Gulf region further stimulate bottled water production and associated testing requirements. In Africa, countries such as South Africa and Kenya are upgrading regulatory frameworks to strengthen export competitiveness and public health safety standards.

Latin America

Latin America accounts for nearly 4% of global demand, with Mexico and Brazil leading regional consumption. Mexico’s strong bottled water export base to North America is driving investments in compliance-focused laboratory equipment. Brazil is witnessing moderate growth supported by rising domestic bottled water consumption and evolving regulatory frameworks. Increasing focus on food and beverage safety modernization across the region is expected to gradually accelerate testing equipment adoption over the forecast period.

Key Players in the Bottled Water Testing Equipment Market

- Thermo Fisher Scientific

- Agilent Technologies

- Danaher Corporation

- Shimadzu Corporation

- PerkinElmer

- Waters Corporation

- Bruker Corporation

- Mettler-Toledo

- Sartorius AG

- Merck KGaA

- Bio-Rad Laboratories

- Horiba Ltd.

- Metrohm AG

- Hach Company

- Eurofins Scientific