Bottled Water Delivery Service Market Size

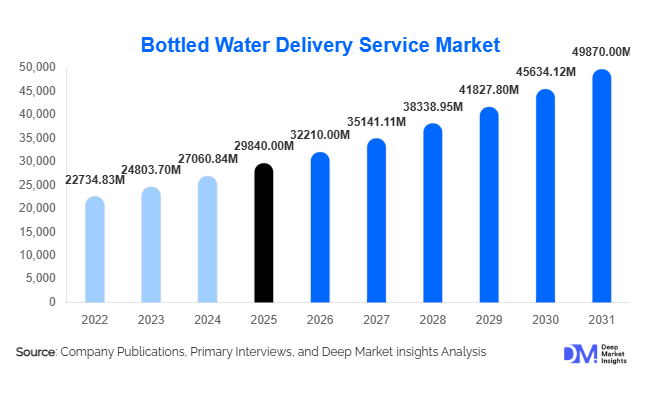

According to Deep Market Insights, the global bottled water delivery service market size was valued at USD 29,840 million in 2025 and is projected to grow from USD 32,210 million in 2026 to reach USD 49,870 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The bottled water delivery service market is witnessing sustained expansion driven by rising health awareness, increasing urbanization, workplace hydration programs, and growing concerns regarding municipal water quality across both developed and emerging economies. Businesses and households are increasingly shifting toward scheduled water delivery subscriptions that ensure consistent access to purified drinking water without logistical inconvenience.

Key Market Insights

- Subscription-based bottled water delivery models are becoming the dominant revenue stream, supported by recurring consumer demand and predictable consumption cycles.

- Commercial offices and institutional buyers remain the largest demand generators, accounting for a significant portion of bulk water dispenser installations globally.

- Asia-Pacific leads volume growth due to rapid urbanization, rising middle-class populations, and water safety concerns in densely populated cities.

- Smart dispensers and IoT-enabled refill tracking are improving delivery efficiency and customer retention.

- Sustainability initiatives, including reusable containers and electric delivery fleets, are reshaping operational models.

- Residential adoption is accelerating as hybrid work culture increases home-based consumption patterns.

What are the latest trends in the bottled water delivery service market?

Shift Toward Subscription and Smart Delivery Ecosystems

Bottled water delivery providers are transitioning from transactional supply models toward subscription-based ecosystems supported by predictive analytics and automated scheduling. Companies increasingly deploy mobile applications that allow customers to track consumption, modify delivery frequency, and manage billing seamlessly. Smart dispensers equipped with sensors automatically notify suppliers when refills are required, reducing missed deliveries and optimizing logistics planning. These technologies lower operational costs while enhancing customer convenience and retention rates. Enterprise customers, particularly co-working spaces and corporate offices, increasingly prefer integrated hydration management solutions rather than one-time product purchases, transforming water delivery into a service-oriented industry.

Sustainability and Circular Packaging Models

Environmental sustainability has become a defining trend within the bottled water delivery market. Companies are investing heavily in reusable polycarbonate containers, bottle return programs, and recycling infrastructure to minimize plastic waste. Many operators now maintain closed-loop logistics systems where containers are sanitized and reused multiple times, significantly reducing packaging costs and carbon emissions. Electric delivery vehicles and route optimization software further reduce environmental footprints. Consumers and corporate clients increasingly select suppliers based on sustainability credentials, pushing service providers to adopt eco-labeling, carbon reporting, and water-source transparency initiatives.

What are the key drivers in the bottled water delivery service market?

Rising Concerns Over Drinking Water Quality

Concerns surrounding contamination, aging municipal infrastructure, and inconsistent water purification standards are driving households and businesses toward reliable bottled water delivery services. Urban populations increasingly perceive delivered purified water as safer than tap water, particularly in emerging economies. Governments’ tightening water quality regulations have indirectly boosted demand for certified purified and mineral water supply solutions.

Expansion of Commercial and Institutional Infrastructure

The rapid expansion of office complexes, healthcare facilities, educational institutions, and hospitality establishments has significantly increased bulk hydration demand. Workplace wellness programs encouraging regular hydration are further supporting dispenser installations. Corporate contracts often involve long-term supply agreements, creating stable revenue streams for service providers.

Urban Lifestyle Convenience and E-Commerce Integration

Consumers increasingly prioritize convenience-driven services aligned with digital lifestyles. Online ordering platforms and app-based scheduling reduce manual purchasing efforts. Integration with e-commerce ecosystems enables automated replenishment, flexible subscription tiers, and bundled appliance leasing models, accelerating market penetration globally.

Market Restraints

Despite strong growth, high logistics costs remain a major restraint due to transportation expenses, fuel price volatility, and reverse logistics requirements for bottle collection. Additionally, environmental scrutiny surrounding plastic usage continues to challenge industry perception, requiring continuous investment in recycling infrastructure and sustainable packaging alternatives.

What are the key opportunities in the bottled water delivery service industry?

Smart Hydration Solutions for Corporate Clients

The integration of IoT-enabled dispensers and AI-based consumption analytics presents significant opportunities for service providers. Enterprises increasingly demand centralized hydration monitoring systems capable of tracking water usage across multiple facilities. These systems enable predictive delivery scheduling, reduce waste, and support corporate ESG reporting initiatives. Vendors offering digital dashboards and automated compliance reporting can secure long-term enterprise contracts.

Expansion in Emerging Urban Markets

Rapid urban expansion across Southeast Asia, Africa, and Latin America creates untapped demand for organized water delivery services. Many cities experience unreliable municipal water supply, encouraging adoption of subscription-based purified water delivery. New entrants can leverage localized bottling facilities and micro-distribution hubs to penetrate underserved urban neighborhoods.

Sustainable Packaging and Premium Water Segments

Premium mineral and alkaline water delivery services represent a growing niche opportunity. Health-conscious consumers increasingly seek functional hydration products, including electrolyte-enhanced or pH-balanced water. Companies investing in glass containers, biodegradable materials, and carbon-neutral delivery operations can differentiate themselves while commanding higher margins.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 29840 Million |

| Market Size in 2026 | USD 32210 Million |

| Market Size in 2031 | USD 49870 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

The global bottled water delivery market continues to evolve toward service-oriented consumption models, with scheduled subscription delivery emerging as the dominant service category and accounting for approximately 46% of the global market share in 2025. The leadership of subscription-based delivery models is closely linked to shifting consumer expectations surrounding convenience, reliability, and automation. Both residential and commercial customers increasingly prefer predictable hydration solutions that eliminate the need for repeated manual purchasing decisions. Subscription services allow providers to establish long-term contractual relationships, ensuring recurring revenue streams while reducing customer acquisition costs over time.The rise of digital commerce ecosystems has significantly strengthened subscription adoption. Mobile applications, automated billing platforms, AI-driven consumption forecasting, and route optimization technologies enable companies to manage inventory and delivery schedules with high precision. Businesses benefit from uninterrupted water supply, particularly in offices, healthcare facilities, and educational institutions where hydration availability directly impacts productivity and operational efficiency. For households, automated replenishment aligns with modern lifestyle trends characterized by time constraints and preference for home delivery services.While on-demand delivery continues to serve occasional buyers and emergency requirements, its share remains comparatively smaller due to fluctuating demand patterns and higher fulfillment costs. Nevertheless, hybrid service models combining subscription stability with flexible top-up ordering options are gaining traction, reflecting the industry’s transition toward customer-centric service customization. As digital transformation accelerates globally, subscription delivery is expected to remain the structural backbone of the bottled water delivery industry.

Water Type Insights

By water type, purified drinking water dominates the global market, capturing nearly 52% market share in 2025. The segment’s leadership is primarily driven by affordability, scalability, and consistent quality assurance enabled by advanced purification technologies such as reverse osmosis (RO), ultraviolet sterilization, and ozone treatment systems. These technologies allow providers to produce large volumes of safe drinking water while maintaining cost efficiency, making purified water the preferred option across both residential and commercial applications.The economic advantage of purified water lies in its adaptability to local water sources. Providers can purify municipal or groundwater supplies at centralized facilities, reducing dependency on geographically limited natural springs. This flexibility allows rapid market expansion in densely populated urban areas where demand volumes are high and logistics efficiency is critical. Additionally, standardized purification processes enable regulatory compliance and quality consistency, strengthening consumer trust and brand reliability.Health awareness trends also support the segment’s dominance. Consumers increasingly prioritize safe hydration solutions amid rising concerns regarding water contamination, aging infrastructure, and environmental pollutants. Purified water offers an accessible solution positioned between low-cost tap water and premium natural alternatives. Its neutral taste profile further enhances acceptance across diverse consumer demographics.Functional and enhanced water variants containing electrolytes or added minerals are emerging as niche growth areas, especially among fitness-oriented consumers. Despite this innovation, purified water remains the leading segment due to its balance of cost efficiency, availability, and universal applicability.

Container Size Insights

The 18–20 liter bulk container segment dominates the bottled water delivery market, accounting for approximately 61% of total market revenue in 2025. The leadership of this segment is strongly associated with cost efficiency, operational practicality, and compatibility with dispenser-based hydration systems widely used in offices and households. Large-format containers significantly reduce packaging material usage per liter, lowering overall production and transportation costs while supporting sustainability objectives.Reusable container ecosystems represent a major driver of segment growth. Companies operate closed-loop collection and sanitation systems in which empty bottles are retrieved, sterilized, and refilled multiple times before recycling. This circular logistics model reduces environmental impact and aligns with global regulatory pressures aimed at minimizing single-use plastic waste. Businesses and institutions increasingly adopt reusable bulk containers as part of corporate sustainability commitments and environmental, social, and governance (ESG) initiatives.Smaller container formats such as 5-liter and single-serve bottles continue to serve retail and travel applications but are less dominant within delivery-based models due to higher logistics complexity and waste generation. The long-term outlook indicates continued expansion of bulk container systems supported by smart dispensers, IoT-enabled consumption tracking, and automated reorder capabilities that further enhance efficiency.

Distribution Channel Insights

Distribution dynamics within the bottled water delivery market increasingly favor direct-to-customer delivery models, which account for nearly 58% of total market share. This leadership is driven by digital transformation, allowing companies to interact directly with consumers through online platforms, mobile applications, and subscription management systems. By bypassing traditional intermediaries such as wholesalers and retailers, suppliers achieve improved margin control while maintaining ownership of customer relationships.Technology adoption plays a central role in this segment’s expansion. Advanced route optimization software reduces fuel consumption and delivery times, while predictive analytics help companies anticipate consumption patterns based on historical usage data, weather trends, and occupancy rates. These innovations enable efficient fleet deployment and minimize operational costs, strengthening the economic viability of direct distribution models.Third-party retail and distributor channels remain relevant in emerging markets where logistics infrastructure is fragmented; however, rapid urbanization and smartphone penetration are accelerating the shift toward direct ordering models. As e-commerce adoption expands globally, direct-to-consumer distribution is expected to remain the primary growth engine of the industry.

End-Use Insights

The commercial segment represents the most significant and fastest-growing end-use category within the bottled water delivery market, supported by expanding global service economies and institutional hydration requirements. Corporate workplaces alone contributed over 38% of total market demand in 2025, reflecting widespread adoption of dispenser-based hydration systems designed to enhance employee wellness and productivity. Organizations increasingly recognize hydration as a component of workplace health programs, driving consistent bulk water consumption.Healthcare facilities are emerging as a particularly high-growth segment due to strict hygiene regulations and patient safety standards. Hospitals, clinics, and long-term care centers require reliable access to safe drinking water for patients, staff, and visitors, creating stable long-term contracts for delivery providers. The COVID-era emphasis on sanitation awareness continues to influence institutional purchasing behavior, reinforcing demand stability.Educational institutions also contribute significantly to commercial demand growth. Universities, schools, and training centers increasingly adopt centralized hydration solutions to reduce reliance on disposable plastic bottles while ensuring continuous water availability for large populations.The hospitality and tourism sectors represent an additional growth avenue. Hotels, resorts, and serviced apartments increasingly rely on large-format bottled water delivery to maintain international service standards and guest satisfaction. As global travel recovers and expands, hospitality-driven demand is expected to contribute steadily to overall market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Bottled Water Delivery Service Market Segmentations

By Service Type

- Residential/Home Bottled Water Delivery

- Office & Workplace Delivery

- Institutional Delivery

- Subscription-Based Scheduled Delivery

- On-Demand & App-Based Delivery

By Water Type

- Purified Drinking Water

- Natural Spring Water

- Mineral Water

- Alkaline & Functional Water

- Flavored & Enhanced Bottled Water

By Packaging Format

- Large Gallon Bottles

- Single-Serve Bottles

- Returnable & Refillable Containers

- Sustainable/Recyclable Packaging

By Distribution Channel

- Direct Company Delivery Fleets

- Online Platforms & Mobile Applications

- Retailer-Integrated Delivery Services

- Corporate & Institutional Contracts

By End-Use

- Residential Consumers

- Commercial Offices

- Hospitality & Foodservice

- Healthcare & Educational Institutions

- Industrial & Manufacturing Facilities

Regional Insights

North America

North America accounted for approximately 29% of global market share in 2025, led primarily by the United States and Canada. The region benefits from mature infrastructure, widespread adoption of dispenser-based hydration systems, and a deeply entrenched subscription consumption culture. Corporate offices, co-working spaces, and institutional facilities form the backbone of demand, supported by strong corporate wellness initiatives emphasizing employee health and sustainability.High consumer purchasing power enables premiumization trends, including mineral water subscriptions and environmentally friendly reusable container programs. Technological sophistication among service providers supports advanced logistics optimization, automated billing systems, and predictive delivery scheduling. Additionally, growing environmental awareness encourages adoption of refillable large containers over single-use packaging.Regulatory frameworks promoting recycling and waste reduction further strengthen reusable delivery models. The rise of remote and hybrid work arrangements has also expanded residential subscriptions, balancing previously office-centric consumption patterns. Continuous innovation in smart dispensers and touchless hydration technologies is expected to sustain regional growth.

Europe

Europe represents around 23% of the global bottled water delivery market, with strong demand across Germany, the United Kingdom, France, Italy, and Spain. Sustainability remains the primary growth driver within the region. Stringent environmental regulations encourage reusable packaging systems, carbon footprint reduction, and circular economy practices, all of which favor large-container delivery services.Institutional hydration policies across workplaces and public facilities contribute to stable demand. European consumers demonstrate strong environmental consciousness, prompting companies to invest in biodegradable packaging innovations, electric delivery fleets, and localized production facilities to reduce emissions. Western Europe exhibits high market penetration and steady replacement demand, while Eastern Europe presents faster growth potential due to improving economic conditions and urbanization.

Asia-Pacific

Asia-Pacific is both the largest and fastest-growing regional market, contributing nearly 34% of global demand in 2025. Rapid urban population expansion, infrastructure disparities, and rising concerns regarding potable water availability are major growth drivers. China and India lead regional consumption due to large populations and increasing middle-class households seeking reliable drinking water alternatives.Urbanization plays a central role in market expansion. High-density residential complexes and commercial hubs create favorable conditions for centralized delivery logistics. Rising disposable incomes enable households to transition from boiling or filtering tap water toward professionally delivered purified water solutions. Digital payment adoption and app-based ordering platforms further accelerate subscription penetration.Southeast Asian markets, including Indonesia, Vietnam, and the Philippines, are experiencing double-digit growth supported by expanding urban middle classes and increasing awareness of waterborne health risks. Rapid development of e-commerce ecosystems and last-mile delivery networks strengthens accessibility even in previously underserved areas. Government initiatives focused on improving public health standards indirectly encourage adoption of safe drinking water services.

Middle East & Africa

The Middle East and Africa region represents a high-growth market characterized by structural water scarcity and climatic challenges. In the Middle East, dependence on desalinated water sources drives strong reliance on bottled water delivery services. Countries such as the United Arab Emirates and Saudi Arabia demonstrate high per-capita consumption levels, supported by premium lifestyle preferences and extreme weather conditions that increase hydration needs.Rapid urban development, hospitality expansion, and large expatriate populations further contribute to demand growth. Commercial establishments, particularly hotels and corporate offices, rely heavily on bulk water delivery to maintain service quality standards.Across Africa, growth is driven by urban infrastructure limitations and inconsistent municipal water supply quality. Countries including South Africa, Nigeria, and Kenya are witnessing increasing adoption of delivered drinking water solutions as urban populations expand. Rising investments in local bottling facilities and distribution networks improve accessibility and reduce logistics costs, enabling broader market penetration.

Latin America

Latin America is steadily expanding, led by Brazil and Mexico, where urban households increasingly depend on bottled water delivery due to concerns regarding municipal water reliability. Population growth in metropolitan areas and rising middle-class incomes support sustained demand for subscription-based hydration services.Regional providers are investing in localized bottling infrastructure to reduce transportation expenses and improve delivery efficiency. The strong presence of large family households favors bulk container adoption, reinforcing the dominance of 18–20 liter formats. Additionally, expanding foodservice and hospitality industries contribute to commercial consumption growth.Economic modernization and digital payment adoption are improving accessibility to subscription services, while growing environmental awareness encourages reusable container systems. As logistics networks continue to improve, Latin America is expected to demonstrate stable long-term growth within the global bottled water delivery market.

Key Players in the Bottled Water Delivery Service Market

- Nestlé Waters

- Primo Brands Corporation

- Culligan International

- Danone Waters

- BlueTriton Brands

- DS Services of America

- Eden Springs

- Quench USA

- Waterlogic Holdings

- Primo Water Corporation

- Tingyi Holding Corp.

- Wahaha Group

- Bisleri International

- Al Ain Water

- National Beverage Corp.