Bottled Spring Water Market Size

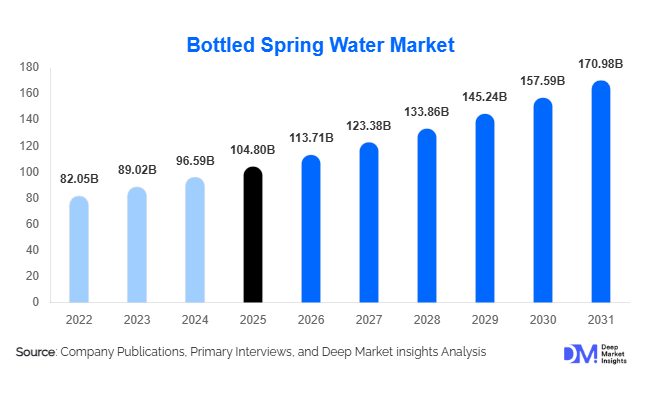

According to Deep Market Insights, the global bottled spring water market size was valued at USD 104.8 billion in 2025 and is projected to grow from USD 113.71 billion in 2026 to reach USD 170.98 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The bottled spring water market growth is primarily driven by rising consumer preference for healthier hydration alternatives, increasing concerns regarding tap water quality, growing premium beverage consumption, and expanding demand for sustainable and naturally sourced packaged water products worldwide.

Key Market Insights

- Premium and naturally sourced spring water products are witnessing rising global demand, driven by consumer preference for clean-label and health-focused beverages.

- Sustainable packaging adoption is accelerating across the industry, with manufacturers investing in recyclable PET, aluminum bottles, biodegradable materials, and refillable glass formats.

- Europe dominates the global bottled spring water market, supported by strong premium water consumption and large-scale exports from France, Italy, Germany, and Switzerland.

- Asia-Pacific remains the fastest-growing regional market, fueled by rapid urbanization, rising disposable incomes, and increasing concerns regarding water safety.

- Online retail and direct-to-consumer subscription delivery models are expanding rapidly, particularly across urban markets in North America, China, and the Middle East.

- Functional and flavored spring water categories are gaining popularity, especially among fitness-focused and younger consumer demographics seeking enhanced hydration options.

What are the latest trends in the bottled spring water market?

Premiumization and Luxury Hydration Trends

The bottled spring water industry is increasingly shifting toward premium and ultra-premium hydration offerings. Consumers are showing growing willingness to pay higher prices for naturally sourced mountain spring water, glacier water, and mineral-rich products associated with purity, exclusivity, and wellness. Luxury hospitality chains, fine-dining restaurants, airlines, and wellness resorts are actively incorporating premium bottled spring water into customer experiences. Brands are focusing heavily on source storytelling, mineral composition transparency, and sustainable sourcing certifications to differentiate products in highly competitive markets. Glass packaging, designer bottles, and limited-edition collections are also becoming important branding tools in premium segments. Demand for imported European spring water products remains particularly strong across Asia-Pacific and the Middle East, where affluent consumers increasingly associate premium bottled water with lifestyle and status.

Sustainable Packaging and Circular Economy Adoption

Environmental sustainability has emerged as one of the most influential trends shaping the bottled spring water market. Governments and consumers are increasingly pressuring beverage manufacturers to reduce plastic waste and carbon emissions. As a result, companies are investing heavily in recyclable PET materials, lightweight packaging, biodegradable bottles, aluminum cans, and refillable glass packaging systems. Closed-loop recycling initiatives and carbon-neutral bottling operations are becoming increasingly common among leading global brands. Several manufacturers are also adopting renewable energy-powered production facilities and water-efficient bottling technologies to strengthen sustainability credentials. Consumers are increasingly prioritizing brands that demonstrate environmental responsibility, especially in Europe and North America, where sustainability purchasing behavior is highly developed.

What are the key drivers in the bottled spring water market?

Growing Health and Wellness Awareness

The increasing global focus on healthy lifestyles and wellness-oriented consumption patterns remains one of the strongest growth drivers for the bottled spring water market. Consumers are actively reducing consumption of sugary beverages, carbonated soft drinks, and artificially flavored drinks due to growing concerns regarding obesity, diabetes, and cardiovascular health. Bottled spring water is increasingly perceived as a healthier and calorie-free hydration alternative. Fitness enthusiasts, athletes, and wellness-focused consumers are driving demand for natural hydration products, electrolyte-enhanced spring water, and functional hydration beverages. Rising participation in sports, gym memberships, and wellness activities globally continues to accelerate consumption volumes.

Rising Concerns Regarding Water Quality and Safety

Deteriorating confidence in municipal water infrastructure and growing concerns regarding contamination are significantly supporting bottled spring water demand globally. Aging water pipelines, industrial pollution, microplastic contamination, and inconsistent purification standards in several developing economies are encouraging consumers to shift toward packaged drinking water products perceived as safer and more reliable. In highly urbanized regions, bottled spring water has become an essential daily consumption product. Rapid population growth, tourism expansion, and increasing travel activity are also strengthening demand for portable and hygienic hydration solutions across residential and commercial sectors.

What are the restraints for the global market?

Environmental Concerns Related to Plastic Waste

One of the biggest restraints facing the bottled spring water market is increasing environmental scrutiny regarding single-use plastic packaging. Governments worldwide are implementing stricter recycling regulations, plastic taxation policies, and sustainability compliance standards for beverage manufacturers. Public criticism regarding ocean plastic pollution and landfill waste continues to impact industry perception. Compliance with evolving environmental standards requires substantial investments in packaging redesign, recycling infrastructure, and sustainable material sourcing, potentially pressuring operating margins for manufacturers.

High Logistics and Transportation Costs

The bottled spring water industry faces considerable logistical and transportation challenges due to the heavy weight and relatively low value-density of bottled water products. Natural spring water sources are geographically concentrated, requiring long-distance transportation to major consumer markets. Fuel price volatility, rising freight costs, and increasing carbon emission regulations significantly impact profitability. Premium glass packaging further increases shipping expenses due to added weight and handling complexity. These operational challenges are especially significant for international premium spring water exporters serving global luxury beverage markets.

What are the key opportunities in the bottled spring water industry?

Expansion of Functional and Enhanced Hydration Products

The growing consumer preference for functional beverages presents major opportunities for bottled spring water manufacturers. Companies are increasingly launching electrolyte-enriched spring water, vitamin-infused hydration products, alkaline spring water, and naturally flavored variants targeting health-conscious consumers. Younger demographics and fitness-oriented consumers are driving strong demand for hydration products that offer additional wellness benefits beyond basic water consumption. Manufacturers integrating clean-label ingredients, natural flavor infusions, and performance hydration positioning are expected to gain higher profit margins and stronger brand differentiation in premium beverage categories.

Growth of Digital Retail and Subscription Delivery Models

The rapid expansion of e-commerce and direct-to-consumer beverage delivery services is creating substantial opportunities within the bottled spring water market. Urban consumers increasingly prefer home-delivered hydration solutions due to convenience and recurring consumption patterns. Subscription-based delivery platforms for households and corporate offices are expanding rapidly across North America, Europe, and Asia-Pacific. Digital commerce channels also enable smaller premium spring water brands to access international consumer bases without requiring extensive traditional retail distribution networks. Integration of AI-driven inventory systems, smart vending machines, and digital consumer engagement platforms is further enhancing market accessibility and operational efficiency.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 104.80 Billion |

| Market Size in 2026 | USD 113.71 Billion |

| Market Size in 2031 | USD 170.98 Billion |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The still spring water segment continues to dominate the global bottled spring water market, accounting for the largest share of overall consumption due to its broad appeal across residential, commercial, institutional, and hospitality applications. The dominance of still spring water is primarily driven by growing consumer preference for clean-label hydration products that are perceived as healthier alternatives to carbonated beverages, sugary soft drinks, and artificially flavored drinks. Rising health awareness among consumers worldwide, combined with increasing concerns regarding obesity, diabetes, and excessive sugar consumption, has significantly accelerated demand for naturally sourced still spring water products. In both developed and emerging economies, consumers increasingly view bottled spring water as an essential daily hydration solution, supporting stable long-term demand across supermarkets, convenience retail, workplaces, fitness centers, and travel channels.Electrolyte-enhanced spring water products are gaining considerable traction among athletes, gym-goers, and fitness-focused consumers due to their perceived benefits related to hydration recovery and physical performance support. The rising popularity of sports nutrition beverages and wellness-focused consumption patterns continues to encourage manufacturers to expand their functional spring water portfolios. At the premium end of the market, luxury artisanal spring water brands sourced from glacier springs, volcanic aquifers, and protected mountain reserves are strengthening their position within luxury hospitality, premium retail, and high-income urban consumer segments. The premiumization trend across the global beverage industry continues to support demand for high-end bottled spring water products with unique mineral compositions, sustainable sourcing claims, and premium packaging aesthetics.

Packaging Type Insights

PET bottles continue to dominate the bottled spring water packaging landscape due to their lightweight structure, durability, convenience, and cost-effectiveness across large-scale retail distribution systems. The leading position of PET packaging is primarily driven by its compatibility with high-volume manufacturing operations, efficient transportation economics, and widespread consumer familiarity. Single-serve PET bottles remain particularly popular across convenience stores, transportation hubs, educational institutions, vending machines, and travel retail channels where portability and affordability are major purchasing considerations. Large-capacity PET containers are also witnessing strong household demand as consumers increasingly purchase bulk packaged water products for regular daily consumption.Aluminum cans are rapidly emerging as a high-growth packaging segment within the bottled spring water market. The expansion of aluminum packaging is largely driven by increasing sustainability awareness, high recyclability rates, and consumer preference for environmentally responsible packaging solutions. Beverage companies are increasingly introducing canned spring water products targeting younger environmentally conscious demographics seeking alternatives to conventional plastic bottles. Aluminum cans also provide logistical advantages including stackability, durability, and reduced transportation inefficiencies, supporting broader adoption across retail and foodservice distribution channels.Paper-based cartons and biodegradable packaging solutions are gaining momentum as governments worldwide implement stricter environmental regulations aimed at reducing single-use plastic waste. Manufacturers are increasingly investing in sustainable packaging innovation to improve brand image and comply with evolving sustainability mandates. Plant-based packaging materials, compostable containers, refillable bottle programs, and closed-loop recycling initiatives are becoming increasingly important competitive differentiators within the global bottled spring water market. The growing influence of ESG commitments and corporate sustainability initiatives continues to accelerate investment in next-generation eco-friendly packaging technologies.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels within the global bottled spring water market due to their extensive product assortment, high consumer traffic, and strong retail penetration across urban and suburban markets. The leadership of supermarkets and hypermarkets is primarily supported by consumer preference for bulk purchasing, promotional pricing strategies, and convenient access to both economy and premium bottled spring water brands under a single retail platform. Large-format retailers continue expanding private-label bottled water offerings, further intensifying competition while increasing product accessibility across middle-income consumer groups.The rapid expansion of organized retail infrastructure in developing economies is further strengthening supermarket and hypermarket distribution growth. Retail chains increasingly allocate larger shelf space to bottled water and functional hydration products as health-conscious beverage demand continues to rise globally. Seasonal demand spikes, promotional campaigns, and premium product launches also contribute significantly to sales growth within modern retail environments.Foodservice distribution across hotels, restaurants, cafés, airlines, and catering services is witnessing substantial growth due to rising tourism activity, premium dining trends, and increasing hospitality investments worldwide. Premium bottled spring water brands continue strengthening partnerships with luxury hotels, airlines, and fine-dining establishments to enhance brand visibility and premium positioning. Tourism recovery across international travel markets is further contributing to bottled spring water demand within hospitality-focused commercial channels.Vending machine distribution also maintains strong market presence across offices, educational institutions, healthcare facilities, fitness centers, and transportation infrastructure. The growing deployment of smart vending technologies, cashless payment systems, and automated beverage dispensing solutions continues supporting channel modernization and accessibility.

Consumer Category Insights

Household consumers account for the largest share of bottled spring water consumption globally due to increasing health awareness, growing packaged water penetration, and rising concerns regarding drinking water quality. The dominance of household consumption is largely driven by consumers’ increasing preference for safe, convenient, and ready-to-drink hydration products. Rapid urbanization, changing lifestyles, and growing disposable incomes continue to support higher bottled spring water consumption across both developed and emerging economies. Families increasingly purchase bottled spring water in bulk formats for daily home use, particularly in regions facing concerns regarding aging municipal water infrastructure or inconsistent tap water quality.Corporate offices and institutional consumers are increasingly adopting bottled spring water as part of employee wellness programs, workplace hospitality services, conferences, and corporate events. Businesses are placing greater emphasis on employee health and workplace experience, encouraging higher demand for premium hydration products within office environments. Educational institutions, healthcare facilities, government buildings, and commercial establishments also contribute significantly to institutional bottled water consumption.Luxury lifestyle consumers are supporting rapid expansion within the premium bottled spring water segment, particularly across high-income urban markets and luxury hospitality establishments. Imported artisanal spring water brands featuring unique mineral compositions, sustainable sourcing narratives, and premium packaging aesthetics are increasingly popular among affluent consumers seeking exclusivity and premium beverage experiences. The premiumization trend within the global beverage industry continues creating significant opportunities for high-end bottled spring water brands targeting luxury-oriented customer segments.

Explore more data points, trends and opportunities Download Free Sample Report

Bottled Spring Water Market Segmentations

By Product Type

- Still Spring Water

- Sparkling Spring Water

- Flavored Spring Water

- Electrolyte-Enriched Spring Water

- Premium & Artisanal Spring Water

- Organic Certified Spring Water

By Packaging Type

- PET Bottles

- Glass Bottles

- Aluminum Cans

- Cartons & Paper-Based Packaging

- Bulk Containers

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & E-Commerce

- Foodservice Distribution

- Vending Machines

- Direct-to-Consumer Subscription Delivery

- Institutional Sales

By Consumer Category

- Household Consumers

- Health & Fitness Consumers

- Travelers & On-the-Go Consumers

- Corporate & Office Consumers

- Hospitality Consumers

- Luxury Lifestyle Consumers

By End Use

- Residential Consumption

- Commercial Consumption

Regional Insights

North America

North America represents one of the largest bottled spring water markets globally, supported by strong consumer preference for healthy hydration products, high packaged beverage consumption, and widespread retail accessibility. The United States dominates regional demand due to rising health consciousness, strong fitness culture adoption, and increasing consumer preference for sugar-free beverage alternatives. Growing concerns regarding obesity, diabetes, and artificial beverage ingredients are encouraging consumers to shift toward natural spring water products for everyday hydration.Sustainability trends remain a major growth driver across the North American bottled spring water market. Beverage manufacturers are investing heavily in recyclable packaging, lightweight PET bottles, recycled content integration, and carbon reduction initiatives to align with evolving environmental regulations and consumer expectations. Canada also maintains strong demand for premium natural mountain spring water products, supported by outdoor lifestyle culture, premium retail demand, and growing interest in environmentally sustainable beverage consumption.

Europe

Europe remains the dominant regional market, accounting for approximately 33% of global bottled spring water consumption in 2025. The region benefits from a long-established bottled mineral water culture, strong consumer trust in natural spring water products, and significant presence of globally recognized premium water brands. France, Germany, Italy, Switzerland, and Spain continue to represent major production and consumption hubs due to strong regional demand for naturally sourced mineral-rich spring water.The expansion of premium hospitality, wellness tourism, luxury dining, and fine beverage culture continues supporting strong demand for artisanal spring water products throughout Europe. Functional hydration products and flavored premium spring water are also gaining increasing traction among younger consumers seeking healthier beverage alternatives.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market for bottled spring water, driven by rapid urbanization, expanding middle-class populations, rising disposable incomes, and increasing concerns regarding municipal water quality. The region’s large population base and accelerating economic development continue creating substantial opportunities for bottled spring water manufacturers across both mature and emerging economies.China remains the largest market within the Asia-Pacific region due to rising premium beverage consumption, increasing awareness regarding safe drinking water, and strong expansion of organized retail infrastructure. Rapid urban development and changing consumer lifestyles are encouraging higher packaged water consumption across households, workplaces, and commercial establishments. Premium imported spring water brands are also witnessing rising popularity among affluent Chinese consumers.Japan and South Korea maintain stable demand for premium hydration products, functional beverages, and wellness-oriented spring water categories due to strong consumer preference for health-focused lifestyles and advanced beverage innovation. Southeast Asian countries including Indonesia, Thailand, and Vietnam are witnessing rising bottled spring water consumption due to tourism growth, increasing urbanization, expanding retail infrastructure, and improving household purchasing power.

Latin America

Latin America is experiencing steady bottled spring water market growth led primarily by Brazil and Mexico. Increasing urbanization, improving retail infrastructure, rising disposable incomes, and growing consumer awareness regarding healthy hydration are contributing significantly to regional demand expansion. Consumers throughout the region are increasingly shifting away from sugar-sweetened beverages toward healthier bottled water alternatives.Brazil remains the dominant regional market due to its large population base, expanding packaged beverage industry, and growing middle-class consumer segment. Rising demand for premium bottled water products among affluent urban consumers is supporting category diversification and premiumization trends across metropolitan areas. Expanding tourism activity and hospitality sector investments are also contributing to increased bottled spring water demand across hotels, resorts, restaurants, and entertainment venues.Mexico continues to represent a major bottled water consumption market due to long-standing concerns regarding tap water quality and strong consumer reliance on packaged drinking water products. Increasing penetration of convenience retail networks and modern grocery channels further supports broader product accessibility across urban and suburban regions.

Middle East & Africa

The Middle East & Africa region is witnessing strong bottled spring water demand growth due to high temperatures, water scarcity concerns, rapid urbanization, expanding tourism infrastructure, and rising population levels. Climatic conditions throughout much of the region naturally support high per-capita bottled water consumption as consumers rely heavily on packaged hydration products for daily use.The UAE and Saudi Arabia remain major regional consumption hubs because of heavy dependence on bottled drinking water, strong premium hospitality sectors, and growing luxury tourism industries. Large-scale investments in hotels, airlines, resorts, entertainment complexes, and tourism infrastructure continue driving substantial commercial bottled spring water demand throughout the Gulf region.South Africa represents one of the leading African bottled spring water markets, supported by organized retail growth, increasing urbanization, and rising consumer health awareness. Across several African economies, growing concerns regarding water safety and improving retail accessibility are encouraging higher bottled water adoption rates. Governments and beverage manufacturers throughout the region are increasingly investing in sustainable water infrastructure, recycling programs, and environmentally responsible packaging solutions to address long-term environmental and water resource challenges.

Key Players in the Bottled Spring Water Market

- Nestlé Waters

- Danone

- PepsiCo

- The Coca-Cola Company

- Primo Brands Corporation

- Fiji Water

- CG Roxane

- Voss Water

- Ferrarelle Società Benefit

- Gerolsteiner Brunnen

- Nongfu Spring

- Suntory Beverage & Food

- Tata Consumer Products

- Icelandic Glacial

- Highland Spring Group