Bottled Beer Market Size

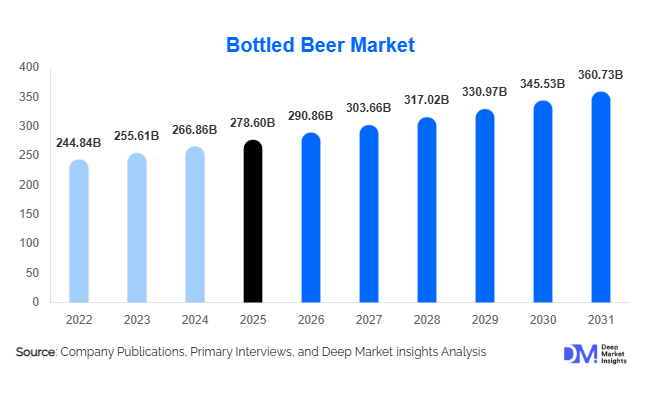

According to Deep Market Insights, the global bottled beer market size was valued at USD 278.6 billion in 2025 and is projected to grow from USD 290.86 billion in 2026 to reach USD 360.73 billion by 2031, expanding at a CAGR of 4.4% during the forecast period (2026–2031). The bottled beer market growth is driven by premiumization trends, rising urban consumption patterns, strong brand loyalty across developed markets, and expanding middle-class purchasing power in emerging economies. Bottled beer continues to maintain a strong position within the global alcoholic beverage industry due to its perceived product quality, portability, longer shelf stability, and premium brand positioning compared to alternative packaging formats.

Consumer demand is increasingly shifting toward premium, craft, and flavored beer variants, particularly among younger demographics seeking differentiated taste experiences. Glass bottle packaging remains closely associated with authenticity and freshness, supporting sustained demand across retail and hospitality channels. Growth in organized retail, expanding cold-chain logistics, and rapid penetration of modern trade outlets across Asia-Pacific and Latin America further reinforce bottled beer consumption. Additionally, rising tourism, nightlife expansion, and sports-driven consumption occasions continue to strengthen global demand.

Developed markets such as North America and Europe demonstrate stable consumption supported by premium offerings, while Asia-Pacific represents the fastest-growing region due to urbanization, demographic expansion, and evolving drinking cultures. Technological advancements in brewing, sustainable packaging innovations, and digital marketing strategies are also reshaping competitive dynamics. Overall, the bottled beer market is transitioning from volume-led expansion toward value-driven growth, characterized by premium pricing strategies, craft innovation, and regional brand diversification.

Key Market Insights

- Premium and craft bottled beer segments are expanding rapidly, driven by consumer preference for quality and differentiated flavors.

- Glass bottles remain the dominant packaging format due to brand perception and product preservation benefits.

- Asia-Pacific leads volume growth, supported by rising disposable incomes and urban consumption trends.

- On-trade consumption recovery is strengthening bottled beer demand globally.

- Sustainability initiatives, including lightweight bottles and recycling programs, are influencing manufacturer investments.

- Digital retail and direct-to-consumer channels are reshaping distribution strategies w

What are the latest trends in the bottled beer market?

Premiumization and Craft Beer Expansion

Premium bottled beer continues to outperform standard lager categories globally as consumers increasingly value authenticity, heritage branding, and distinctive taste profiles. Craft breweries are expanding beyond local markets through partnerships with global distributors, enabling wider availability of specialty beers. Limited-edition flavors, seasonal brews, and locally inspired ingredients are attracting younger consumers and driving higher profit margins. Premiumization also allows manufacturers to offset slowing volume growth in mature markets through price optimization strategies.

Sustainable Packaging and Circular Economy Adoption

Brewers are investing heavily in returnable glass bottle systems, recycled glass usage, and lightweight packaging technologies to reduce carbon footprints. Governments in Europe and parts of Asia are promoting deposit-return schemes, encouraging higher recycling rates. Sustainability labeling and environmentally responsible production practices are becoming key purchase drivers, particularly among environmentally conscious consumers. Manufacturers are also integrating renewable energy into bottling plants and optimizing logistics networks to reduce emissions.

What are the key drivers in the bottled beer market?

Urban Lifestyle and Social Consumption Growth

Rapid urbanization and expanding hospitality sectors have significantly increased social drinking occasions. Bars, restaurants, sporting events, and entertainment venues favor bottled beer due to ease of storage and premium presentation. Rising youth populations in emerging markets continue to support consistent consumption growth.

Brand Loyalty and Premium Brand Positioning

Global beer brands maintain strong consumer loyalty supported by decades of marketing investments and sponsorships. Bottled beer is widely perceived as higher quality compared to canned alternatives, allowing producers to command premium pricing and maintain stable margins even during economic fluctuations.

Expansion of Organized Retail Channels

Modern supermarkets, liquor chains, and e-commerce alcohol platforms are improving product availability worldwide. Cold storage infrastructure expansion in developing markets has enhanced distribution efficiency, enabling premium bottled beers to penetrate secondary cities.

What are the restraints for the global market?

Rising Raw Material and Packaging Costs

Fluctuations in barley, hops, and glass manufacturing costs continue to pressure brewer margins. Energy-intensive bottle production further increases operational costs, particularly in regions facing energy price volatility.

Regulatory Restrictions and Health Awareness

Increasing alcohol taxation, advertising regulations, and growing consumer awareness regarding health impacts are moderating consumption growth in several developed markets. Governments are tightening regulations related to alcohol marketing and distribution, creating compliance challenges.

What are the key opportunities in the bottled beer industry?

Emerging Market Penetration

Rapid income growth across Southeast Asia, Africa, and Latin America presents substantial opportunities for new entrants and global brewers. Expanding urban populations and evolving drinking habits support long-term demand expansion. Localization strategies, including region-specific flavors and pricing tiers, allow companies to capture new consumer segments.

Low-Alcohol and Specialty Beer Innovation

Health-conscious consumers are driving demand for low-alcohol, alcohol-free, and functional beer variants packaged in premium bottles. Innovation in fermentation technologies enables brewers to maintain flavor while reducing alcohol content, expanding consumer inclusivity.

Digital Commerce and Direct Distribution Models

E-commerce alcohol sales and app-based delivery platforms are creating new revenue streams. Breweries are increasingly leveraging digital marketing analytics and subscription-based models to strengthen customer engagement and brand loyalty.

Product Type Insights

Lager bottled beer dominates the global market, accounting for approximately 52% of total market share in 2025, supported by widespread consumer familiarity, standardized taste profiles, and highly efficient large-scale brewing operations. The leadership of lager is primarily driven by its mass-market accessibility, longer shelf stability, and compatibility with diverse climatic conditions and food cultures across both developed and emerging economies. Multinational brewers continue to prioritize lager production due to optimized supply chains, predictable demand cycles, and strong brand recognition built through decades of marketing investments. The segment’s dominance is further reinforced by affordability across income groups and its strong presence in retail distribution networks, where high-volume sales drive consistent revenue generation.Ale and craft beer segments are expanding rapidly as consumers increasingly shift toward premium and differentiated drinking experiences. Growth in these categories is strongly supported by rising consumer preference for artisanal beverages, localized brewing identities, and experimentation with flavors, brewing techniques, and seasonal releases. North America and Europe remain innovation hubs for craft brewing, where microbreweries and independent producers continue to reshape consumer expectations toward authenticity and quality. Specialty beers, including wheat beers, flavored beers, and hybrid formulations, are gaining traction among younger demographics seeking experiential consumption rather than traditional volume-driven drinking patterns. This diversification of product offerings is encouraging breweries to expand bottled product portfolios to capture premium margins and niche consumer segments.

Packaging Type Insights

Glass bottles lead with nearly 68% share of the bottled beer market, driven by superior product preservation, enhanced carbonation retention, and strong premium brand perception among consumers. Glass packaging remains the preferred format for brewers due to its non-reactive properties, which protect flavor integrity and extend product freshness throughout distribution cycles. The leading driver behind this segment’s dominance is consumer association of glass bottles with authenticity, heritage branding, and higher-quality beer experiences, particularly in premium and imported beer categories.Returnable glass bottle systems are especially prominent in Europe and Latin America, where established recycling infrastructure and deposit-return schemes significantly reduce packaging costs while supporting sustainability objectives. These systems allow breweries to maintain cost efficiency while aligning with environmental regulations and circular economy initiatives. PET and specialty bottles occupy smaller but strategically important niches, particularly in price-sensitive and high-volume markets where lightweight logistics and reduced transportation costs provide economic advantages. Innovation in lightweight glass manufacturing and recyclable materials continues to strengthen the long-term viability of glass packaging as sustainability regulations tighten globally.

Distribution Channel Insights

Off-trade retail channels hold around 57% market share, emerging as the dominant distribution pathway due to convenience, competitive pricing, and broad product availability. Supermarkets, liquor stores, hypermarkets, and convenience outlets enable consumers to access a wide variety of domestic and international beer brands in a single purchasing environment. The leading growth driver for this segment is the increasing trend toward home-based consumption, supported by evolving social behaviors, promotional pricing strategies, and expansion of organized retail infrastructure in emerging economies.Digital retail and e-commerce platforms are further strengthening off-trade growth by enabling direct-to-consumer delivery models and subscription-based beverage purchasing. Meanwhile, on-trade channels such as bars, pubs, restaurants, and entertainment venues remain strategically important for brand positioning, consumer engagement, and product trial experiences. Premium and craft beer brands particularly benefit from on-trade visibility, where curated menus and experiential consumption environments encourage higher-margin sales. Urbanization and nightlife expansion across metropolitan regions continue to support gradual recovery and long-term growth of on-trade distribution networks.

End-Use Insights

Individual consumption accounts for nearly 72% of bottled beer demand, reflecting strong household purchasing patterns, informal social gatherings, and growing preference for convenient packaged beverages. The primary driver behind this segment’s leadership is the global shift toward at-home entertainment and casual consumption occasions, supported by retail accessibility and multi-pack purchasing formats. Bottled beer’s portability and portion control advantages further enhance its suitability for personal consumption across diverse demographic groups.Commercial consumption through hospitality venues is experiencing strong recovery momentum following pandemic-related disruptions. Restaurants, bars, and hotels increasingly utilize bottled beer as a premium beverage offering due to branding visibility, ease of storage, and consistent serving quality. Rising tourism activity, expanding entertainment districts, and increasing disposable incomes are collectively contributing to renewed growth in commercial consumption channels worldwide.

End-Use Analysis

The hospitality and foodservice industry represents the fastest-growing end-use segment, expanding at nearly 5.2% annually as global tourism rebounds and urban entertainment culture strengthens. Restaurants, pubs, hotels, and event venues rely heavily on bottled beer for premium positioning, standardized serving quality, and enhanced brand presentation. Investments in tourism infrastructure, international travel recovery, and large-scale hospitality developments across Asia-Pacific and the Middle East are directly supporting bottled beer consumption growth. Premium imported beers and craft varieties are particularly benefiting from increased exposure within experiential dining environments.Retail consumption remains the largest overall contributor to market revenue, supported by continued growth of modern retail infrastructure, expansion of organized supermarkets, and rising consumer preference for purchasing beverages for home consumption. Export-driven demand is also expanding steadily, with premium European and Mexican beer brands experiencing strong international shipments due to globalization of taste preferences. Emerging consumption models such as brewery taprooms, experiential beverage retail spaces, and hybrid hospitality concepts are further diversifying end-use applications, creating new revenue streams and strengthening direct consumer engagement for brewers.

| By Product Type | By Packaging Type | By Distribution Channel | By Alcohol Content | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 21% of the global bottled beer market in 2025, led primarily by the United States and Canada. Regional growth is driven by premiumization trends, strong craft brewing ecosystems, and evolving consumer preference toward quality-focused beverages rather than volume consumption. High disposable income levels allow consumers to explore specialty and imported bottled beers, while innovation in flavor profiles and limited-edition releases sustains market dynamism. The expansion of brewery taprooms, direct-to-consumer sales models, and growing demand for sustainable packaging solutions further support regional market expansion. Regulatory clarity and well-established distribution infrastructure also enable efficient nationwide brand penetration.

Europe

Europe held nearly 28% market share in 2025, supported by deep-rooted beer traditions and mature consumption cultures across Germany, the United Kingdom, Spain, Poland, and neighboring markets. Regional growth is primarily driven by strong returnable bottle ecosystems, sustainability regulations encouraging reusable packaging, and continuous innovation within specialty and premium beer categories. Consumers increasingly favor heritage brands and geographically protected brewing styles, reinforcing bottled beer demand. Cross-border trade within the European Union facilitates premium imports, while tourism-driven consumption across Southern Europe further accelerates on-trade sales. The region’s focus on environmental sustainability and circular packaging systems strengthens long-term demand stability.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, fueled by rapid urbanization, rising disposable incomes, and expanding middle-class populations across China, India, Vietnam, Japan, and South Korea. Growth is strongly driven by increasing westernization of consumption habits, expansion of modern retail channels, and aggressive market entry strategies by global brewers. China remains the largest volume market globally due to population scale and widespread beer affordability, while India demonstrates the fastest growth rate exceeding 6% annually, supported by urban youth demographics and evolving social lifestyles. Infrastructure investments in cold-chain logistics and retail modernization are significantly improving bottled beer availability across tier-2 and tier-3 cities, accelerating regional demand.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth supported by expanding urban populations, rising middle-class income levels, and increasing development of hospitality and tourism sectors in markets such as South Africa, Nigeria, and Kenya. Demand growth is largely concentrated in urban centers where nightlife culture and international tourism influence beverage consumption patterns. Regulatory environments vary widely across countries, shaping market penetration strategies for brewers. Premium imports and international brands are gaining traction among affluent consumers, while localized production investments help improve affordability and supply stability. Infrastructure development and retail modernization continue to enhance long-term market accessibility.

Latin America

Latin America remains a key growth contributor, with Brazil and Mexico dominating regional demand due to strong beer-drinking culture and presence of major brewing companies. Regional growth is primarily driven by affordability enabled through returnable bottle systems, which reduce packaging costs and encourage repeat purchases. Economic recovery trends, expansion of modern retail outlets, and increasing popularity of social gatherings and festivals further stimulate bottled beer consumption. Export-oriented production in Mexico also strengthens international market participation, positioning the region as both a major consumption hub and a global supply base for bottled beer products.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Bottled Beer Market

- Anheuser-Busch InBev

- Heineken N.V.

- Carlsberg Group

- China Resources Beer Holdings

- Molson Coors Beverage Company

- Asahi Group Holdings

- Kirin Holdings

- Constellation Brands

- Tsingtao Brewery Group

- Grupo Modelo

- Diageo

- Thai Beverage Public Company

- San Miguel Corporation

- Efes Beverage Group

- United Breweries Limited