Botanical Supplements Market Size

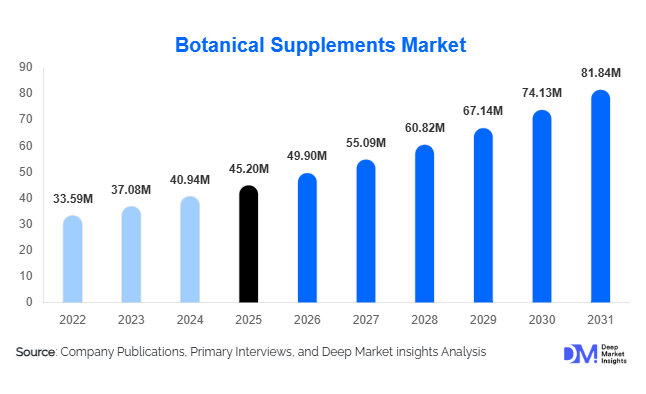

According to Deep Market Insights, the global botanical supplements market size was valued at USD 45.2 billion in 2025 and is projected to grow from USD 48.60 billion in 2026 to reach USD 79.80 billion by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The botanical supplements market growth is primarily driven by rising consumer preference for plant-based healthcare solutions, increasing adoption of preventive nutrition, and expanding scientific validation of herbal ingredients across global wellness industries. Growing awareness regarding immunity enhancement, stress management, and holistic health practices has transformed botanical supplements from traditional remedies into mainstream nutraceutical products.

Key Market Insights

- Preventive healthcare adoption is accelerating demand, with consumers increasingly integrating botanical supplements into daily wellness routines.

- Standardized herbal extracts are gaining dominance due to improved clinical validation and dosage consistency.

- North America leads global consumption, supported by strong nutraceutical penetration and premium product adoption.

- Asia-Pacific is the fastest-growing region, driven by Ayurveda and Traditional Chinese Medicine commercialization.

- E-commerce channels are reshaping distribution, enabling direct-to-consumer botanical brands to scale globally.

- Technological innovation in extraction and bioavailability is enhancing product efficacy and supporting premium pricing strategies.

What are the latest trends in the botanical supplements market?

Rise of Adaptogenic and Functional Botanicals

Adaptogenic herbs such as ashwagandha, rhodiola, and medicinal mushrooms are experiencing strong global adoption as consumers seek natural solutions for stress, cognitive health, and energy balance. Functional mushroom supplements including reishi and lion’s mane are rapidly transitioning from niche wellness products into mainstream dietary supplementation. Increasing clinical research supporting adaptogens’ role in cortisol regulation and mental wellness is reinforcing consumer trust. Brands are also introducing multi-functional blends combining immunity, mood, and metabolic health benefits into single formulations, aligning with convenience-driven purchasing behavior.

Digital Commerce and Personalized Nutrition Platforms

The botanical supplements industry is witnessing rapid digital transformation through subscription models, AI-based supplement recommendations, and microbiome-driven personalization. Online platforms allow consumers to access customized botanical regimens tailored to lifestyle and health goals. Direct-to-consumer models are improving brand loyalty while reducing reliance on traditional retail distribution. Companies are leveraging data analytics, health tracking apps, and telehealth integrations to create personalized botanical wellness ecosystems, significantly enhancing consumer engagement and repeat purchases.

What are the key drivers in the botanical supplements market?

Growing Preference for Natural and Clean-Label Products

Consumers increasingly prefer plant-derived ingredients over synthetic alternatives due to perceived safety and sustainability benefits. Clean-label movements emphasizing transparency, organic sourcing, and minimal processing are significantly boosting botanical supplement demand. Manufacturers are responding by highlighting traceability, non-GMO certification, and sustainably harvested raw materials, strengthening brand differentiation.

Expansion of Preventive Healthcare and Wellness Spending

Rising healthcare costs globally are encouraging consumers to adopt preventive nutrition solutions. Botanical supplements are increasingly positioned as daily health maintenance products supporting immunity, cardiovascular health, digestion, and mental wellness. Employers and healthcare providers are integrating wellness programs that include nutraceutical supplementation, further expanding market penetration.

What are the restraints for the global market?

Regulatory Fragmentation Across Regions

Regulatory frameworks for botanical supplements vary significantly between countries, with products classified differently as foods, nutraceuticals, or herbal medicines. This inconsistency increases compliance costs, complicates labeling requirements, and slows international expansion for manufacturers.

Raw Material Supply Volatility

Dependence on agricultural cultivation exposes botanical ingredients to climate variability, overharvesting risks, and fluctuating yields. Price instability for herbs such as ginseng and turmeric affects manufacturing margins and supply reliability, creating operational challenges for companies operating at scale.

What are the key opportunities in the botanical supplements industry?

Integration with Clinical and Practitioner Channels

Healthcare professionals increasingly recommend botanical supplements as complementary therapies. Practitioner-grade formulations supported by clinical research are opening opportunities in medical nutrition and integrative healthcare markets. Companies investing in evidence-based products can expand beyond retail into high-value clinical distribution channels.

Emerging Market Expansion

Rapid urbanization and rising disposable incomes in India, Southeast Asia, Latin America, and the Middle East are generating new demand for packaged herbal wellness solutions. Localization strategies combining traditional medicine heritage with modern branding are enabling companies to capture untapped consumer segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 45.20 Million |

| Market Size in 2026 | USD 49.90 Million |

| Market Size in 2031 | USD 81.84 Million |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global botanical supplements market demonstrates strong diversification across product categories, with herbal extract supplements maintaining clear leadership and accounting for approximately 34% of the global market share in 2025. The dominance of this segment is primarily supported by increasing consumer preference for standardized formulations that ensure consistent potency, measurable bioactive compound concentration, and scientifically validated efficacy. Standardized extracts allow manufacturers to align traditional herbal usage with modern nutraceutical quality standards, strengthening trust among healthcare practitioners and informed consumers. Advances in extraction technologies, including solvent-free and bioavailability-enhancing processes, have further improved absorption efficiency, reinforcing demand for concentrated herbal extracts over raw botanical powders.Single-herb supplements continue to maintain strong global adoption due to high consumer familiarity and long-established therapeutic associations. Ingredients such as turmeric, ginseng, ashwagandha, and green tea extracts benefit from extensive clinical research visibility and strong digital health awareness campaigns. At the same time, botanical blend formulations are expanding rapidly as consumers increasingly seek multifunctional wellness solutions addressing immunity, stress management, metabolic health, and energy support within a single product. The rise of personalized nutrition and condition-specific supplementation programs is accelerating innovation in blended botanical formulations.Functional mushroom supplements represent one of the fastest-growing product categories within the market, supported by increasing scientific research linking adaptogenic mushrooms to cognitive performance, immune modulation, and stress resilience. Ingredients such as reishi, lion’s mane, and cordyceps are transitioning from niche wellness products into mainstream nutraceutical offerings as consumer awareness grows through social media health communities and integrative medicine practices. Additionally, botanicals rooted in traditional medicine systems, particularly Ayurveda and Traditional Chinese Medicine, are gaining global traction as cultural wellness traditions increasingly merge with modern evidence-based nutraceutical science. This convergence is encouraging multinational companies to invest in clinically validated traditional formulations, expanding cross-border acceptance and commercial scalability.

Application Insights

Immunity support remains the leading application segment, accounting for nearly 22% market share, driven by sustained consumer behavioral shifts toward preventive healthcare following global health crises. Consumers increasingly prioritize daily supplementation to maintain immune resilience rather than reactive treatment approaches, resulting in consistent long-term demand. The leading position of this segment is further supported by growing scientific validation of plant-derived antioxidants, adaptogens, and anti-inflammatory compounds that align with preventive wellness strategies promoted by healthcare professionals and public health organizations.Cognitive health and stress management applications are expanding rapidly as mental wellness becomes a central component of holistic health. Rising workplace stress levels, digital fatigue, and sleep-related disorders are encouraging adoption of botanicals such as adaptogens and nootropic herbs designed to support mood balance, focus, and emotional resilience. Increased consumer openness toward natural alternatives to pharmaceutical interventions is accelerating growth within this application category, particularly among younger professionals and urban populations.Digestive health botanicals continue to experience widespread adoption across developed markets, supported by growing awareness of the gut–microbiome connection and its influence on immunity, metabolism, and mental health. Herbal ingredients traditionally used for digestive balance are increasingly incorporated into functional foods and supplement regimens. Meanwhile, beauty-from-within applications are emerging strongly among younger consumers seeking skin health, anti-aging benefits, and hair vitality through antioxidant-rich botanical supplementation. The convergence of nutraceuticals and cosmetic wellness trends is creating new product innovation opportunities.Weight management and metabolic health applications are also gaining traction as botanical ingredients are incorporated into functional nutrition programs targeting blood sugar balance, energy metabolism, and appetite regulation. Rising global obesity concerns and lifestyle-related metabolic disorders are encouraging consumers to adopt plant-based supportive solutions as part of broader wellness routines rather than short-term dieting approaches.

Distribution Channel Insights

Online retail channels dominate distribution, accounting for roughly 31% of global sales, supported by rapid digitalization of health product purchasing behavior. E-commerce platforms enable consumers to access extensive product information, clinical evidence, ingredient sourcing transparency, and peer reviews, which significantly influence purchasing decisions in the supplement category. Subscription-based purchasing models, personalized recommendations powered by digital health platforms, and cross-border accessibility to niche botanical brands continue to accelerate online channel expansion.Pharmacies and drugstores remain essential distribution channels, particularly for clinically positioned botanical supplements marketed for specific health conditions. Consumers often associate pharmacy availability with higher product credibility and safety assurance, supporting steady demand within regulated retail environments. Health specialty stores maintain relevance through curated premium offerings, in-store education, and personalized consultation services that enhance consumer confidence in complex botanical formulations.Practitioner-based distribution is expanding steadily as integrative healthcare models gain acceptance globally. Nutritionists, naturopaths, and functional medicine practitioners increasingly recommend botanical supplementation within preventive and therapeutic protocols, strengthening professional endorsement and driving higher-value product adoption. This channel also contributes to consumer education and long-term supplementation adherence.

End-User Insights

Adults aged 18–45 represent the largest consumer segment, contributing approximately 38% of total demand, driven by proactive health management, fitness-oriented lifestyles, and increasing awareness of long-term wellness optimization. This demographic demonstrates strong engagement with digital health content and preventive supplementation strategies aimed at enhancing energy levels, stress resilience, and overall performance. The growth of plant-based lifestyles and clean-label preferences further reinforces botanical supplement adoption within this age group.Aging populations constitute a high-value consumer segment as longevity-focused healthcare becomes a global priority. Older adults increasingly adopt botanical supplements targeting joint mobility, cardiovascular health, cognitive preservation, and immune maintenance. Rising life expectancy and healthcare cost concerns encourage preventive supplementation as a strategy to support healthy aging and maintain independence.Sports and fitness consumers are increasingly incorporating plant-based performance recovery and endurance-support products into training routines, reflecting broader shifts toward natural alternatives to synthetic performance enhancers. Clinical nutrition users are also integrating botanicals into therapeutic wellness plans, particularly within integrative oncology, metabolic care, and chronic disease management frameworks. Preventive healthcare consumers represent the fastest-growing demographic globally, driven by increasing health literacy and early intervention approaches.

Explore more data points, trends and opportunities Download Free Sample Report

Botanical Supplements Market Segmentations

By Product Type

- Herbal Extract Supplements

- Single Herb Supplements

- Botanical Blends Formulated Supplements

- Functional Mushroom Supplements

- Traditional Medicine-Based Botanicals

By Application

- Immunity Support

- Cognitive Health Stress Management

- Digestive Health

- Cardiovascular Health

- Beauty Skin Health

- Weight Management Metabolic Health

- Sports Nutrition Performance Support

By Distribution Channel

- Online Retail Direct-to-Consumer Platforms

- Pharmacies Drugstores

- Health Nutrition Specialty Stores

- Supermarkets Hypermarkets

- Practitioner Clinical Channels

By End User

- Adults

- Aging Population

- Sports Fitness Consumers

- Clinical Preventive Healthcare Users

Regional Insights

North America

North America holds approximately 32% market share in 2025, led primarily by the United States, where nutraceutical adoption rates and premium wellness expenditure remain among the highest globally. Regional growth is supported by strong consumer awareness of preventive healthcare, widespread acceptance of dietary supplements, and advanced retail infrastructure enabling omnichannel distribution. Increasing clinical research investments and regulatory clarity surrounding botanical ingredients enhance consumer confidence in standardized extracts and evidence-backed formulations. The growing integration of supplements into mainstream healthcare recommendations, combined with rising demand for clean-label, organic, and sustainably sourced products, continues to drive market expansion across both the U.S. and Canada. Canada contributes steady growth through high demand for certified organic botanicals and strong government oversight that reinforces product safety perceptions.

Europe

Europe accounts for nearly 27% of the global market, with Germany, France, Italy, and the United Kingdom serving as key consumption hubs. Regional growth is strongly supported by deep-rooted herbal medicine traditions combined with stringent regulatory frameworks that enhance product quality assurance and consumer trust. Increasing adoption of sustainability certifications, traceable sourcing practices, and environmentally responsible production methods aligns closely with European consumer values, strengthening market stability. Rising aging populations and preventive healthcare initiatives across Western Europe further stimulate demand for botanical supplements addressing cognitive health, cardiovascular wellness, and immune support. Additionally, expanding interest in plant-based lifestyles and natural therapeutics continues to reinforce long-term regional market expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at nearly 12.8% CAGR, driven by strong cultural acceptance of traditional herbal medicine systems and rapidly evolving healthcare consumption patterns. China leads regional growth through deep integration of Traditional Chinese Medicine into modern healthcare and increasing commercialization of standardized botanical extracts for domestic and export markets. India is emerging as a major growth engine supported by Ayurveda commercialization, government promotion of traditional medicine, expanding manufacturing capabilities, and rising global exports of herbal formulations. Japan and South Korea demonstrate strong demand fueled by aging demographics, high healthcare awareness, and widespread adoption of preventive supplementation practices. Increasing disposable income, urbanization, and rapid expansion of e-commerce health platforms further accelerate regional adoption.

Latin America

Latin America is experiencing steady expansion led by Brazil and Mexico, where cultural familiarity with herbal remedies supports strong consumer acceptance. Regional growth is driven by rising middle-class healthcare spending, improved retail penetration, and growing awareness of natural health solutions as affordable preventive alternatives. Local biodiversity and availability of native medicinal plants encourage domestic product innovation, while increasing investments from international nutraceutical companies enhance product accessibility and brand visibility. Expanding pharmacy chains and digital retail platforms are also improving consumer access to botanical supplements across urban and semi-urban markets.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential market, with the United Arab Emirates and Saudi Arabia leading premium segment growth. Rising disposable income, increasing lifestyle-related health concerns, and expanding wellness tourism ecosystems are supporting demand for natural health products. Government initiatives promoting healthcare diversification and preventive wellness awareness are encouraging adoption of nutraceutical supplementation. Growing import volumes of international botanical brands, combined with expanding modern retail infrastructure and digital commerce penetration, are gradually strengthening regional market maturity. In Africa, improving healthcare access and increasing awareness of traditional plant-based remedies are contributing to gradual but sustained market development.

Key Players in the Botanical Supplements Market

- Nature’s Way Products LLC

- Gaia Herbs

- Himalaya Wellness Company

- NOW Foods

- Herbalife Ltd.

- Amway Corporation

- Nestlé Health Science

- GNC Holdings LLC

- Blackmores Limited

- Dabur India Ltd.

- Swanson Health Products

- Bio-Botanica Inc.

- Arkopharma Laboratories

- Integria Healthcare

- Nature’s Sunshine Products