Bluefin Tuna Market Size

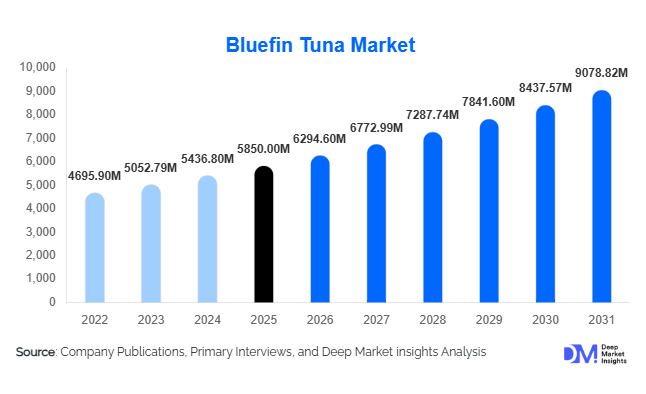

According to Deep Market Insights, the global bluefin tuna market size was valued at USD 5,560 million in 2025 and is projected to grow from USD 6,294.60 million in 2026 to reach USD 9,078.82 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The bluefin tuna market growth is primarily driven by rising global demand for premium seafood, expansion of sushi and sashimi consumption worldwide, increasing adoption of aquaculture-based tuna farming, and strong export-led demand from Asia-Pacific and North America. Supply constraints due to strict fishing quotas and sustainability regulations continue to support high price realization and premium positioning across global markets.

Key Market Insights

- Asia-Pacific dominates global consumption, with Japan remaining the largest single-country market for sashimi-grade bluefin tuna.

- Premium foodservice channels drive demand, especially sushi restaurants, fine dining chains, and luxury hotels globally.

- Aquaculture and tuna ranching are expanding rapidly, helping stabilize supply amid declining wild catch quotas.

- Sashimi-grade tuna remains the highest value segment, commanding premium pricing in international auctions.

- North America and Europe are growing consumption markets, driven by rising popularity of Japanese cuisine and seafood protein diets.

- Sustainability certifications and traceability systems are becoming critical for export compliance and premium pricing.

What are the latest trends in the global bluefin tuna market?

Expansion of Sustainable Tuna Aquaculture

The bluefin tuna industry is witnessing a structural shift toward aquaculture and ranching systems as wild catch quotas tighten globally. Countries such as Japan, Spain, and Australia are investing heavily in closed-cycle breeding technologies and fattening farms to reduce reliance on wild fisheries. These systems help stabilize supply, improve yield predictability, and ensure year-round availability for high-value export markets. The adoption of sustainable feed systems and controlled marine environments is also improving fish quality consistency, making farmed bluefin increasingly competitive with wild-caught varieties. This trend is reshaping supply chains and attracting significant institutional investment.

Traceability and Blockchain-Based Supply Chain Transparency

Growing regulatory pressure and consumer demand for sustainable seafood are accelerating the adoption of digital traceability systems. Blockchain-enabled tracking solutions are being integrated across fishing, processing, and export stages to verify origin, fishing method, and compliance with quotas. This is especially important for export markets like the EU and US, where certification requirements are stringent. Advanced labeling systems and QR-code-based verification tools are enhancing transparency, allowing end consumers to trace tuna back to vessel or farm level. This technological transformation is enabling premium pricing and reducing illegal fishing risks in global trade.

What are the key drivers in the global bluefin tuna market?

Rising Global Demand for Premium Seafood

The growing popularity of Japanese cuisine, particularly sushi and sashimi, is a major driver of bluefin tuna demand. High-end restaurants and premium foodservice chains across the US, Europe, and Asia are expanding rapidly, creating consistent demand for sashimi-grade tuna. Rising disposable incomes and changing dietary preferences toward protein-rich and omega-3-rich foods are further strengthening consumption. The luxury seafood segment continues to expand, with bluefin tuna positioned as one of the highest-value seafood commodities globally.

Growth of Aquaculture and Supply Stabilization Efforts

Aquaculture development has significantly improved supply reliability in the bluefin tuna market. Tuna ranching and controlled fattening systems are helping bridge the gap between demand and limited wild supply. These advancements reduce seasonal volatility and enable exporters to meet increasing international demand. Government-backed fisheries programs and private investments in marine farming infrastructure are accelerating this shift, particularly in Japan and Mediterranean countries.

Expansion of Global Sushi and Fine Dining Culture

The globalization of sushi culture has played a pivotal role in expanding bluefin tuna consumption beyond Asia. Urbanization, tourism growth, and lifestyle changes have led to a surge in Japanese restaurants worldwide. This cultural diffusion is particularly strong in North America and Europe, where sushi chains and premium dining formats are growing steadily. As a result, bluefin tuna has transitioned from a regional delicacy to a globally traded luxury seafood product.

What are the restraints for the global market?

Strict Fishing Regulations and Quota Limitations

The bluefin tuna market is heavily regulated due to historical overfishing and declining wild stocks. International bodies enforce strict catch quotas, seasonal restrictions, and vessel monitoring requirements. While these measures support sustainability, they significantly limit supply availability and restrict market expansion. New entrants face high barriers due to licensing limitations and restricted fishing rights in key oceans.

High Price Volatility and Supply Constraints

Bluefin tuna prices are highly volatile, influenced by auction dynamics, seasonal catch variations, and global demand fluctuations. Premium sashimi-grade tuna can reach extremely high auction prices, making it unaffordable for broader consumer segments. This volatility creates revenue uncertainty for suppliers and complicates long-term contract pricing in export markets.

What are the key opportunities in the global bluefin tuna industry?

Expansion of High-Value Export Markets

Rising demand in emerging economies such as China, India, and Southeast Asia presents significant export growth opportunities. Increasing disposable incomes and the spread of premium dining culture are driving demand for sushi-grade seafood. Exporters who establish strong supply chain networks in these regions can capture high-margin opportunities in fast-growing urban markets.

Premium Branding and Sustainability Certification

Certification-based branding strategies are becoming a major opportunity in the bluefin tuna market. Eco-labeling, sustainable fishing certifications, and traceability verification allow producers to differentiate products and achieve premium pricing. This is particularly important in European and North American markets, where consumers prioritize ethically sourced seafood.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5850.00 Million |

| Market Size in 2026 | USD 6294.60 Million |

| Market Size in 2031 | USD 9078.82 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Species Type Insights

The global bluefin tuna market is strongly shaped by species differentiation, with each variety contributing uniquely to supply dynamics, pricing structures, and consumer preference patterns. Among these, Pacific Bluefin Tuna continues to dominate the global landscape, accounting for approximately 42% of the total market share in 2025. This leadership position is primarily attributed to its exceptional fat content, superior marbling, and highly desirable texture, which make it the preferred choice for high-end sashimi and sushi preparations. The species is particularly favored in Japan, which remains the largest consumer market globally, where culinary traditions and consumer willingness to pay premium prices reinforce demand stability. Additionally, advancements in aquaculture and ranching practices in countries such as Japan and Mexico have improved supply consistency, further strengthening the position of Pacific Bluefin Tuna in the global market.Atlantic Bluefin Tuna also represents a significant segment within the industry, particularly in Europe and the Mediterranean region. Its market presence is supported by established fishing and ranching operations in countries such as Spain, Italy, and Malta. The species benefits from strong regional culinary traditions that emphasize premium seafood consumption, especially in Mediterranean cuisine. Furthermore, strict regulatory frameworks and quota systems imposed to protect Atlantic Bluefin stocks have contributed to its premium positioning, as limited availability enhances perceived value. This controlled supply environment ensures that Atlantic Bluefin Tuna remains a high-margin product, catering to upscale foodservice establishments and export markets.Southern Bluefin Tuna, although accounting for a comparatively smaller share, plays a critical role in the premium segment of the market. Highly valued in Japan and Australia, this species is known for its rich flavor profile and consistent quality. Its limited availability, driven by stringent fishing quotas and conservation efforts, positions it as an exclusive product within international trade. The increasing adoption of sustainable fishing practices and traceability systems is further enhancing its appeal among environmentally conscious consumers. As sustainability becomes a more prominent factor in purchasing decisions, Southern Bluefin Tuna is expected to witness steady demand growth despite supply constraints.

Product Form Insights

Product form segmentation is a key determinant of value creation and market accessibility within the bluefin tuna industry. Fresh and chilled bluefin tuna dominates the market, capturing nearly 48% of the total share, driven by its essential role in sushi and sashimi consumption. The demand for freshness and high quality is particularly pronounced in Asia-Pacific markets, where consumers prioritize taste, texture, and visual appeal. The ability to deliver fresh tuna through efficient cold chain logistics and rapid transportation networks has significantly expanded the reach of this segment, enabling exporters to serve distant markets while maintaining product integrity.The frozen segment plays a crucial supporting role in global trade by enabling long-distance transportation and reducing supply chain risks. Frozen bluefin tuna is widely used in regions where immediate access to fresh seafood is limited, as it ensures year-round availability and price stability. Technological advancements in freezing techniques, such as ultra-low temperature storage, have improved product quality, making frozen tuna increasingly competitive with fresh alternatives. This segment is particularly important for international markets such as North America and Europe, where imports constitute a significant portion of consumption.Processed and canned tuna segments cater to broader consumer bases, including retail and industrial applications. While bluefin tuna is less commonly used in canned products compared to other tuna species due to its premium status, there is a growing niche market for high-end processed offerings. These products are gaining traction among consumers seeking convenience without compromising on quality. Sashimi-grade cuts remain the highest-value category across all product forms, commanding premium prices in global markets. Their demand is closely linked to the expansion of fine dining establishments and the globalization of Japanese cuisine, which continues to influence consumption patterns worldwide.

Distribution Channel Insights

The distribution landscape of the bluefin tuna market is characterized by a strong dominance of direct business-to-business (B2B) trade, which accounts for approximately 55% of the total market share. This channel is driven by seafood auctions, long-term supplier contracts, and bulk export arrangements that connect producers with wholesalers, distributors, and large-scale buyers. Major fish markets, particularly in Japan, play a pivotal role in price discovery and global trade flows, reinforcing the importance of direct channels in maintaining market efficiency and transparency.Indirect distribution channels, including supermarkets, specialty seafood stores, and online retail platforms, are witnessing rapid growth, particularly in urban and developed markets. The increasing availability of premium seafood products in retail settings reflects changing consumer preferences, as more individuals seek to replicate restaurant-quality dining experiences at home. E-commerce platforms are further accelerating this trend by offering convenient access to high-quality seafood, supported by improved packaging and delivery solutions that preserve freshness.The expansion of indirect channels is also driven by rising disposable incomes and growing awareness of the health benefits associated with tuna consumption. As consumers become more informed about nutritional value, particularly the high protein and omega-3 fatty acid content of bluefin tuna, retail demand is expected to increase steadily. Despite this growth, direct B2B trade is likely to remain the dominant distribution channel due to its efficiency in handling large volumes and its critical role in international trade.

End-Use Insights

The end-use segmentation of the bluefin tuna market highlights the overwhelming dominance of the foodservice industry, which accounts for around 60% of the total market share. This segment is primarily driven by the global proliferation of sushi restaurants, fine dining establishments, and luxury hotel chains that rely heavily on high-quality tuna for their offerings. The experiential nature of dining, combined with the premium positioning of bluefin tuna, makes it a staple ingredient in upscale culinary settings. The continued expansion of international cuisine, particularly Japanese food, is further reinforcing the growth of this segment.Retail consumption is emerging as a significant growth area, supported by evolving consumer lifestyles and increasing interest in home cooking. The availability of ready-to-use tuna cuts and improved cold chain infrastructure has made it easier for consumers to access premium seafood products. This trend gained momentum during recent years as more individuals experimented with cooking at home, leading to sustained demand for high-quality ingredients. The retail segment is also benefiting from the rise of health-conscious consumers who view tuna as a nutritious and versatile protein source.Food processing applications, while relatively niche, provide a stable demand base for bluefin tuna. This segment includes the production of value-added products such as smoked tuna, marinated fillets, and specialty packaged goods. Although the use of bluefin tuna in processing is limited by its high cost, there is growing interest in premium processed offerings that cater to affluent consumers. As innovation in product development continues, the food processing segment is expected to maintain steady growth, albeit at a slower pace compared to foodservice and retail channels.

Explore more data points, trends and opportunities Download Free Sample Report

Bluefin Tuna Market Segmentations

By Species Type

- Atlantic Bluefin Tuna

- Pacific Bluefin Tuna

- Southern Bluefin Tuna

By Product Form

- Fresh

- Chilled Bluefin Tuna

- Frozen Bluefin Tuna

- Processed Bluefin Tuna

- Sashimi-Grade Cuts

By Fishing Method

- Wild-Caught Tuna

- Aquaculture

- Ranching Tuna

By Distribution Channel

- B2B Direct Trade

- Supermarkets & Hypermarkets

- Specialty Seafood Stores

- Online Retail Platforms

By End-Use Industry

- Foodservice

- Retail

- Household Consumption

- Food Processing Industry

Regional Insights

Asia-Pacific

Asia-Pacific remains the dominant region in the global bluefin tuna market, holding approximately 62% of the total market share, with Japan alone accounting for nearly 40% of global demand. The region's leadership is deeply rooted in cultural and culinary traditions that emphasize the consumption of raw and minimally processed seafood. Sushi and sashimi are integral components of daily diets in several countries, particularly Japan, where bluefin tuna is regarded as a delicacy. The presence of well-established seafood markets, advanced cold chain logistics, and strong supplier networks further supports the region’s dominance.In addition to cultural factors, economic growth and rising disposable incomes across Asia-Pacific are driving increased consumption of premium seafood products. China, in particular, is emerging as a high-growth market, fueled by expanding middle-class populations and a growing appetite for luxury dining experiences. The rapid development of hospitality infrastructure, including high-end restaurants and international hotel chains, is creating new avenues for bluefin tuna consumption. Furthermore, government initiatives aimed at improving food safety standards and supply chain efficiency are enhancing consumer confidence, thereby supporting market expansion.

North America

North America accounts for approximately 18% of the global bluefin tuna market, with the United States serving as the primary driver of regional demand. The growth of this market is closely linked to the rising popularity of sushi and Japanese cuisine, which has become mainstream across major metropolitan areas. The proliferation of sushi chains, premium seafood restaurants, and fusion dining concepts is significantly contributing to increased consumption of bluefin tuna.Another key growth driver in North America is the increasing focus on health and wellness. Consumers are actively seeking high-protein, nutrient-rich food options, and bluefin tuna is well-positioned to meet this demand due to its nutritional profile. The expansion of retail channels, including specialty seafood stores and online platforms, is further facilitating access to premium tuna products. Canada also contributes to regional growth through its steady demand and role in seafood trade.Additionally, stringent regulatory frameworks and sustainability initiatives are shaping the market landscape in North America. Efforts to promote responsible sourcing and traceability are enhancing consumer trust and supporting long-term market growth. As awareness of environmental issues continues to rise, demand for sustainably sourced bluefin tuna is expected to increase, creating opportunities for certified producers and suppliers.

Europe

Europe holds around 12% of the global market share, with countries such as Spain, Italy, and France serving as key consumption hubs. The region benefits from a strong culinary heritage that emphasizes high-quality seafood, particularly in Mediterranean cuisine. Spain plays a dual role as both a major consumer and a leading producer, with well-established tuna ranching operations that support domestic and export markets.The growth of the European market is driven by several factors, including increasing demand for gourmet dining experiences and a growing emphasis on sustainability. Consumers in the region are highly conscious of environmental and ethical considerations, which is influencing purchasing decisions and encouraging the adoption of certified seafood products. Regulatory frameworks within the European Union are also promoting sustainable fishing practices, ensuring long-term resource management and market stability.Furthermore, the expansion of tourism and hospitality sectors across Europe is contributing to increased demand for premium seafood offerings. As international visitors seek authentic culinary experiences, restaurants and hotels are incorporating high-quality bluefin tuna into their menus. This trend is expected to continue, supporting steady market growth in the region.

Latin America

Latin America accounts for approximately 8% of the global bluefin tuna market, with Brazil and Mexico emerging as key markets. The region is experiencing gradual growth, driven by increasing urbanization and the expansion of the middle class. As disposable incomes rise, consumers are becoming more open to exploring premium food options, including bluefin tuna.The development of modern retail infrastructure and the growth of the restaurant industry are also supporting market expansion. Urban centers are witnessing a surge in international dining establishments, including sushi and fusion restaurants, which are introducing consumers to new culinary experiences. Additionally, the region’s proximity to major tuna fishing areas provides opportunities for local sourcing and export activities.Despite these positive trends, the market in Latin America remains relatively underdeveloped compared to other regions. Challenges such as limited consumer awareness and price sensitivity continue to restrain growth. However, ongoing economic development and increasing exposure to global food trends are expected to create new opportunities for market participants in the coming years.

Middle East & Africa

The Middle East & Africa region is emerging as one of the fastest-growing markets for bluefin tuna, driven by a combination of economic prosperity, luxury tourism, and evolving consumer preferences. High-income countries such as the United Arab Emirates and Saudi Arabia are leading the growth trajectory, supported by a strong demand for premium dining experiences. The presence of world-class hotels, fine dining restaurants, and international culinary brands is significantly boosting consumption of high-quality seafood products, including bluefin tuna.One of the key drivers of regional growth is the increasing reliance on imports to meet domestic demand. Limited local production capabilities necessitate the import of premium seafood, creating opportunities for global suppliers. The expansion of logistics and cold chain infrastructure is further facilitating the efficient distribution of fresh and frozen tuna products across the region.In addition, the growing expatriate population and rising exposure to global cuisines are influencing dietary preferences, leading to increased acceptance of sushi and sashimi. Governments in the region are also investing in tourism and hospitality development as part of broader economic diversification strategies, which is expected to sustain demand for premium seafood in the long term. As a result, the Middle East & Africa region is poised to experience robust growth, supported by favorable economic and demographic factors.

Key Players in the Global Bluefin Tuna Market

- Mitsubishi Corporation

- Maruha Nichiro Corporation

- Nippon Suisan Kaisha

- Thai Union Group

- Dongwon Industries

- Kyokuyo Co. Ltd.

- Bolton Group

- Austevoll Seafood ASA

- SalMar ASA

- Tassal Group

- Tri Marine Group

- Empresas AquaChile

- Grupo Fuentes

- Cooke Aquaculture

- Clearwater Seafoods