Blue Star Nutraceuticals Market Size

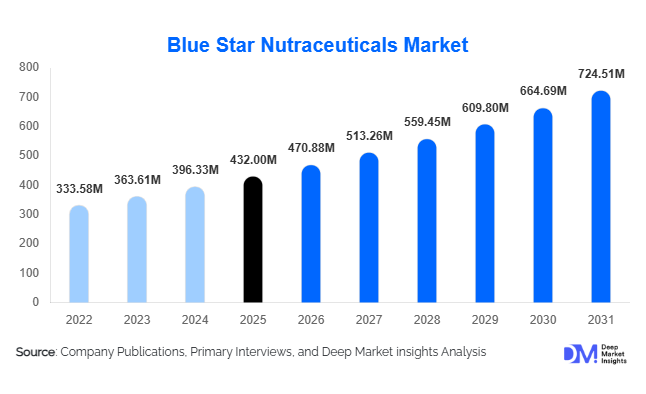

According to Deep Market Insights,The global Blue Star Nutraceuticals market size was valued at USD 432 million in 2025 and is projected to grow from USD 470.88 million in 2026 to reach USD 724.51 million by 2031, expanding at a CAGR of 9.0% during the forecast period (2026–2031). Market growth is primarily driven by increasing consumer inclination toward preventive healthcare, rising awareness of micronutrient deficiencies, expanding aging populations, and rapid penetration of e-commerce channels for health supplements. Growing demand for immunity-boosting, digestive health, and lifestyle-disease management formulations is accelerating innovation across vitamins, probiotics, botanical extracts, and specialty nutrition products.

Key Market Insights

- Dietary supplements dominate the market, accounting for nearly 41% of 2025 revenue, supported by strong demand for vitamins and mineral-based formulations.

- Online retail and D2C platforms contribute over 30% of global sales, reflecting rapid digital transformation and subscription-based wellness models.

- North America leads the market, holding approximately 34% share in 2025, driven by high consumer awareness and established regulatory frameworks.

- Asia-Pacific is the fastest-growing region, expanding at nearly 11% CAGR due to rising middle-class income and urban health awareness.

- Immunity-support products represent 24% of total application demand, maintaining post-pandemic momentum.

- Capsule formulations remain the most preferred format, accounting for nearly 26% share owing to dosage precision and longer shelf stability.

What are the latest trends in the Blue Star Nutraceuticals market?

Personalized and Precision Nutrition Solutions

One of the most significant trends shaping the Blue Star Nutraceuticals market is the rise of personalized nutrition. Companies are integrating AI-based diagnostics, microbiome testing, and wearable health data to design tailored supplement regimens. Consumers increasingly prefer customized vitamin packs aligned with genetic profiles and lifestyle indicators. Subscription-based personalized supplement kits are gaining traction in North America and Europe, allowing brands to command premium pricing and improve long-term customer retention.

Clean-Label and Plant-Based Formulations

Demand for clean-label nutraceuticals is expanding rapidly. Consumers are seeking non-GMO, vegan, allergen-free, and sustainably sourced ingredients. Botanical extracts, plant-based omega alternatives, and naturally derived collagen substitutes are witnessing higher adoption. Companies are also focusing on biodegradable packaging and transparent labeling to align with global ESG expectations. Europe in particular is driving regulatory-backed clean-label compliance, strengthening consumer confidence and brand credibility.

What are the key drivers in the Blue Star Nutraceuticals market?

Growing Preventive Healthcare Awareness

Rising healthcare costs and increasing lifestyle disorders have encouraged consumers to proactively manage health through supplementation. Immunity support, cardiovascular wellness, metabolic balance, and cognitive enhancement are key health priorities. Governments and health organizations promoting preventive healthcare campaigns have further stimulated product adoption, especially in developed economies.

Expansion of E-Commerce and Digital Health Platforms

The rapid growth of digital retail ecosystems has significantly expanded market accessibility. Online platforms enable global reach, transparent pricing, customer reviews, and subscription delivery models. In developed markets, online channels account for over 30% of total nutraceutical revenue, reshaping distribution strategies and enabling small brands to compete globally.

What are the restraints for the global market?

Regulatory Complexity and Compliance Costs

Regulatory classification of nutraceuticals varies across regions, creating compliance challenges. Differences in permissible health claims, labeling standards, and ingredient approvals increase time-to-market and operational costs. Companies must navigate complex regulatory frameworks in the U.S., EU, China, and India to ensure product legitimacy and consumer trust.

Raw Material Price Volatility

Fluctuations in prices of botanical extracts, marine-based omega oils, specialty proteins, and probiotics directly impact profit margins. Climate change and supply chain disruptions further exacerbate sourcing challenges, particularly for plant-derived and marine ingredients.

What are the key opportunities in the Blue Star Nutraceuticals industry?

Emerging Market Expansion

Asia-Pacific and Latin America present strong expansion opportunities. Rapid urbanization, rising disposable incomes, and growing health awareness in India, China, Brazil, and Mexico are driving demand. Government initiatives supporting domestic manufacturing and export-oriented nutraceutical production create favorable conditions for global players.

Corporate Wellness and Institutional Adoption

Corporate wellness programs and fitness institutions are increasingly incorporating nutraceutical supplementation into employee health initiatives. This segment is growing at over 11% CAGR and offers opportunities for bulk contracts, customized formulations, and long-term supply agreements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 432 Million |

| Market Size in 2026 | USD 470.88 Million |

| Market Size in 2031 | USD 724.51 Million |

| CAGR | 9.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Dietary supplements dominate the Blue Star Nutraceuticals market, accounting for approximately 41% of total revenue in 2025. The leadership of this segment is primarily driven by increasing consumer preference for preventive healthcare, rising micronutrient deficiencies across both developed and developing economies, and growing clinical validation of vitamin and mineral supplementation. Within this category, multivitamin and vitamin D formulations lead demand due to heightened awareness of widespread vitamin deficiencies, immune health concerns, and bone health management, particularly among aging populations and urban working professionals. The convenience of capsule, tablet, and softgel formats, combined with expanding direct-to-consumer distribution, further reinforces segment dominance. Functional foods and beverages are steadily expanding as consumers shift toward fortified daily consumption formats that integrate nutrition into routine diets. Meanwhile, medical nutrition products are gaining traction in hospital and geriatric applications, especially for metabolic disorders, cardiovascular support, diabetes management, and oncology-related nutritional care, reflecting the increasing convergence of nutraceuticals and clinical therapeutics.

Application Insights

Immunity support represents nearly 24% of overall demand, making it the leading application segment in 2025. This dominance is driven by sustained post-pandemic consumer focus on immune resilience, increased supplementation of vitamin C, vitamin D, zinc, and herbal extracts, and broader acceptance of daily preventive regimens. Digestive health products containing probiotics, prebiotics, and synbiotics are rapidly expanding due to heightened awareness of the gut–immune axis and the growing prevalence of gastrointestinal disorders linked to sedentary lifestyles and processed diets. Heart health and bone and joint formulations remain foundational segments, particularly among aging populations vulnerable to cardiovascular disease and osteoporosis. At the same time, beauty and skin health nutraceuticals are gaining significant popularity among younger demographics, fueled by collagen peptides, biotin, antioxidants, and plant-based extracts that align with holistic wellness and aesthetic nutrition trends. The diversification of application areas reflects increasing consumer demand for targeted, condition-specific solutions rather than generalized supplementation.

Distribution Channel Insights

Online retail and direct-to-consumer platforms account for approximately 32% of total revenue in 2025, leading all distribution channels. The rapid growth of this segment is supported by expanding e-commerce penetration, personalized recommendation algorithms, subscription-based delivery models, and influencer-driven marketing strategies that directly engage health-conscious consumers. Digital platforms enable brands to provide educational content, product transparency, and bundled wellness programs, strengthening brand loyalty and repeat purchases. Pharmacies and drug stores continue to maintain strong credibility in regulated markets due to professional guidance, product authentication, and established trust among older consumers. Supermarkets and specialty health stores serve the mass-market segment by offering convenient access and diversified product portfolios. The evolving omnichannel strategy adopted by major players integrates digital engagement with offline credibility, reshaping global purchasing behavior and accelerating market penetration.

End-Use Insights

Household consumption represents the largest end-use segment, contributing nearly 62% of total demand in 2025. The segment’s leadership is driven by increasing self-care awareness, higher disposable incomes, and the normalization of daily supplementation as part of preventive health routines. Rising chronic disease prevalence and lifestyle-related health risks further encourage long-term supplement use at the household level. Hospitals and clinical nutrition centers are witnessing faster growth, supported by the integration of nutraceuticals into preventive and adjunct therapeutic care models, particularly in oncology, cardiology, and metabolic disease management. Fitness centers and sports institutions are expanding demand for protein powders, amino acids, creatine, and recovery supplements, backed by the rapidly growing global sports nutrition industry valued at over USD 50 billion. The increasing participation in organized sports, gym memberships, and performance training programs globally continues to strengthen this segment’s contribution.

Explore more data points, trends and opportunities Download Free Sample Report

Blue Star Nutraceuticals Market Segmentations

By Product Category

- Dietary Supplements

- Functional Foods

- Functional Beverages

- Medical Nutrition

By Ingredient Type

- Vitamins

- Minerals

- Proteins & Amino Acids

- Probiotics & Prebiotics

- Omega Fatty Acids

- Botanical Extracts

- Specialty Nutrients

By Formulation Format

- Tablets

- Capsules

- Softgels

- Powders

- Gummies

- Liquid Formulations

By Distribution Channel

- Online Retail & D2C

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Health Stores

By Application

- Immunity Support

- Digestive Health

- Heart Health

- Bone & Joint Health

- Weight Management

- Cognitive Health

- Beauty & Skin Health

- Sports Nutrition

By End-Use

- Household Consumption

- Hospitals & Clinical Nutrition

- Fitness Centers & Sports Institutions

- Corporate Wellness Programs

Regional Insights

North America

North America holds approximately 34% of the global Blue Star Nutraceuticals market in 2025, with the United States contributing nearly 28% alone. Regional dominance is supported by strong consumer awareness regarding preventive healthcare, high per capita supplement expenditure, advanced retail and e-commerce infrastructure, and well-established regulatory frameworks that ensure product quality and transparency. The presence of leading nutraceutical manufacturers and robust research and development activities further stimulate product innovation. Canada demonstrates stable growth driven by expanding digital health platforms, increasing plant-based supplement adoption, and supportive regulatory clarity. The region also benefits from widespread sports nutrition consumption and corporate wellness initiatives that encourage routine supplementation.

Asia-Pacific

Asia-Pacific accounts for around 29% market share and represents the fastest-growing region, expanding at nearly 11% CAGR. Growth is primarily driven by rising disposable incomes, expanding middle-class populations, rapid urbanization, and increasing health awareness across emerging economies. China leads regional demand due to strong domestic manufacturing capacity, government support for health industries, and growing demand for immunity and traditional herbal formulations. India benefits from rising urban health consciousness, expanding e-commerce penetration, and cost-effective production capabilities that enhance export potential. Japan remains a mature yet innovation-driven market characterized by functional foods, aging population-driven demand, and high product standardization. Overall, demographic shifts and evolving dietary habits continue to accelerate regional expansion.

Europe

Europe represents approximately 23% of the global market, with Germany, the United Kingdom, France, and Italy serving as major contributors. Regional growth is supported by stringent regulatory compliance that enhances consumer trust and product credibility. The rising adoption of plant-based, clean-label, and sustainably sourced supplements aligns with environmentally conscious consumer preferences. Increasing aging demographics across Western Europe further drive demand for cardiovascular, bone, and cognitive health supplements. Innovation in botanical extracts and personalized nutrition solutions strengthens competitive dynamics, while established pharmacy networks ensure stable distribution.

Latin America

Latin America accounts for roughly 6% of the market, led by Brazil and Mexico. Regional growth is fueled by expanding urban middle-class populations, increasing awareness of sports and fitness culture, and growing availability of affordable supplement brands. Rising gym memberships and youth participation in athletic activities significantly contribute to sports nutrition demand. Improvements in retail infrastructure and digital commerce adoption are enhancing product accessibility across metropolitan areas. Economic stabilization efforts in key countries are further supporting long-term market expansion.

Middle East & Africa

The Middle East and Africa hold approximately 8% market share, with the United Arab Emirates and Saudi Arabia leading regional consumption. Growth drivers include rising disposable incomes, government initiatives promoting preventive healthcare, and increasing lifestyle-related disorders such as diabetes and obesity. Expanding retail modernization and cross-border trade facilitate product availability, while imports from Europe and Asia complement domestic production capabilities. In Africa, gradual urbanization and expanding healthcare awareness are supporting steady demand growth, positioning the region as an emerging opportunity market over the forecast period.

Key Players in the Blue Star Nutraceuticals Market

- Amway Corporation

- Herbalife Ltd.

- Nestlé Health Science

- Glanbia plc

- Abbott Laboratories

- GNC Holdings

- Bayer AG

- Pfizer Inc.

- Archer Daniels Midland Company

- DSM-Firmenich

- Otsuka Holdings Co., Ltd.

- Blackmores Limited

- NOW Health Group

- Nature’s Sunshine Products

- Himalaya Wellness Company