Black Tea Market Size

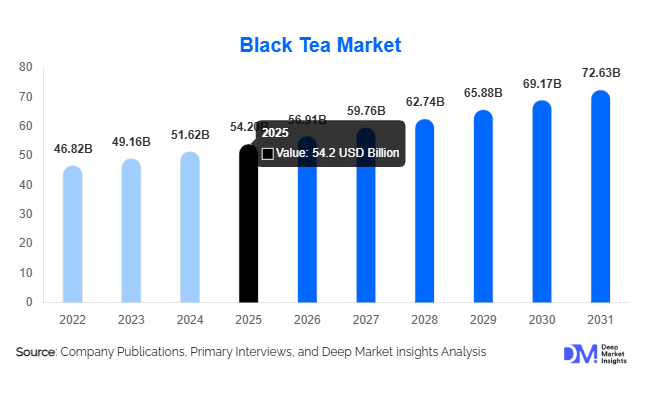

According to Deep Market Insights, the global black tea market size was valued at USD 54.2 billion in 2025 and is projected to grow from USD 56.8 billion in 2026 to reach USD 72.5 billion by 2031, expanding at a CAGR of 5.0% during the forecast period (2026–2031). The black tea market growth is primarily driven by strong global consumption patterns, increasing demand for convenient beverage formats such as ready-to-drink (RTD) tea, and rising consumer awareness of health benefits associated with antioxidant-rich beverages.

Key Market Insights

- Black tea remains the most widely consumed tea globally, driven by strong cultural preferences in Asia, Europe, and Africa.

- Ready-to-drink (RTD) black tea is rapidly expanding, supported by urban lifestyles and demand for convenience beverages.

- Asia-Pacific dominates the market, accounting for nearly 45% of global consumption led by India and China.

- Europe is witnessing premiumization trends, with increasing demand for specialty and organic black teas.

- Online retail channels are growing significantly, driven by e-commerce expansion and direct-to-consumer strategies.

- Functional and flavored tea innovations are reshaping consumer preferences, particularly among younger demographics.

What are the latest trends in the black tea market?

Premiumization and Specialty Tea Demand

The global black tea market is witnessing a strong shift toward premium and specialty tea variants, including single-origin teas such as Darjeeling, Assam, and Nilgiri. Consumers are increasingly prioritizing quality, authenticity, and ethical sourcing, driving demand for organic and fair-trade certified teas. This trend is particularly prominent in Europe and North America, where consumers are willing to pay higher prices for artisanal and sustainably sourced products. Premium packaging formats, storytelling around origin, and traceability are becoming key differentiators for brands. Additionally, tea tasting experiences and curated blends are gaining popularity, enhancing consumer engagement and brand loyalty.

Growth of Ready-to-Drink (RTD) Tea

The RTD black tea segment is emerging as one of the fastest-growing categories within the market. Driven by urbanization, busy lifestyles, and the shift away from carbonated beverages, consumers are increasingly opting for convenient and healthier beverage alternatives. RTD black tea products infused with flavors, herbs, and functional ingredients such as vitamins and antioxidants are gaining traction. This trend is particularly strong in North America and Asia-Pacific, where beverage innovation is rapidly evolving. Companies are also investing in sustainable packaging solutions such as recyclable PET bottles and eco-friendly cartons, aligning with consumer preferences for environmentally responsible products.

What are the key drivers in the black tea market?

Strong Global Consumption Base

Black tea continues to benefit from a deeply entrenched consumption base across major markets such as India, China, the United Kingdom, and Turkey. Daily consumption habits, cultural traditions, and affordability make black tea a staple beverage in many households. This consistent demand provides a stable foundation for market growth and reduces volatility compared to other beverage categories.

Rising Health Awareness

Increasing awareness of health and wellness is driving demand for black tea due to its antioxidant properties and perceived benefits related to heart health, digestion, and metabolism. Consumers are increasingly shifting from sugary beverages to healthier alternatives, positioning black tea as a preferred choice. Functional black tea variants with added health benefits are further accelerating this trend.

What are the restraints for the global market?

Volatility in Raw Material Prices

Climate change and unpredictable weather patterns in key tea-producing regions such as India, Kenya, and Sri Lanka are impacting tea yields and quality. This leads to fluctuations in raw material prices, creating challenges for manufacturers in maintaining consistent pricing and supply stability.

Competition from Alternative Beverages

The growing popularity of green tea, herbal infusions, coffee, and functional beverages poses a challenge to black tea consumption, particularly among younger consumers. Diversified beverage preferences and increasing experimentation with new flavors and formats may limit the growth potential of traditional black tea products.

What are the key opportunities in the black tea industry?

Expansion of RTD and Functional Beverages

The integration of black tea into functional beverages presents a significant growth opportunity. RTD teas fortified with vitamins, minerals, and herbal extracts are gaining popularity among health-conscious consumers. This segment is expected to witness strong growth as companies continue to innovate and diversify product offerings to cater to evolving consumer preferences.

Growth in Emerging Markets

Emerging economies in Asia-Pacific, the Middle East, and Africa offer substantial growth potential due to rising population, increasing disposable incomes, and expanding urbanization. Governments in these regions are also supporting tea production and exports, further strengthening market expansion. Export-driven demand from countries like Kenya and Sri Lanka continues to play a critical role in global supply dynamics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 54.20 Billion |

| Market Size in 2026 | USD 56.91 Billion |

| Market Size in 2031 | USD 72.63 Billion |

| CAGR | 5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global black tea market is strongly shaped by product segmentation, with CTC (Crush, Tear, Curl) black tea continuing to dominate the industry, accounting for approximately 38% of the total market share in 2025. Its dominance is rooted in its highly efficient processing method, which produces a strong, brisk flavor profile that is particularly well-suited for mass-market consumption. The affordability of CTC tea, combined with its quick infusion characteristics, makes it the preferred choice in high-volume, price-sensitive markets such as India, Kenya, and other parts of Africa where tea is consumed multiple times daily as a staple beverage rather than a luxury product. The leading driver behind the dominance of CTC black tea is its scalability and cost efficiency in production. Large tea estates and plantations favor CTC processing because it allows for mechanized production while maintaining consistent flavor strength, which is essential for blending and packaging in mass-market tea bags. Additionally, the rapid urbanization in emerging economies and the expansion of low-cost retail distribution channels have reinforced the consumption of CTC tea in both household and foodservice environments. Orthodox black tea, while holding a smaller share compared to CTC, is experiencing steady growth due to rising global interest in premium and artisanal tea products. Orthodox tea production emphasizes traditional hand-plucking and careful oxidation, resulting in a more nuanced flavor profile. This segment is increasingly favored in developed markets such as Europe and North America, where consumers are willing to pay a premium for quality, origin-specific teas. The key growth driver in this segment is the rising demand for authenticity, traceability, and single-origin sourcing, which aligns with broader trends in specialty beverages. Flavored black tea and decaffeinated variants are also expanding rapidly, driven by evolving consumer preferences for functional and sensory diversity. Flavored teas incorporating spices, fruits, and floral notes are gaining traction among younger consumers who seek novel taste experiences. Meanwhile, decaffeinated black tea is benefiting from the increasing focus on wellness and reduced caffeine intake, particularly among health-conscious urban populations. The premium segment is further supported by the growing popularity of single-origin teas, which emphasize terroir, sustainability, and ethical sourcing practices, thereby enhancing brand differentiation in an increasingly competitive global market.

Application Insights

Household consumption remains the largest application segment in the global black tea market, contributing nearly 55% of total demand. This dominance is deeply embedded in cultural consumption patterns, especially in countries such as India, China, the United Kingdom, and parts of Africa where tea is an essential daily beverage consumed multiple times throughout the day. The primary driver of household consumption growth is the entrenched cultural habit of tea drinking, combined with increasing population levels and rising disposable incomes in emerging economies, which continue to support steady volume expansion. The food and beverage industry represents the fastest-growing application segment, fueled by the rapid expansion of ready-to-drink (RTD) tea products, flavored tea beverages, and café-based tea innovations. Beverage manufacturers are increasingly leveraging black tea as a base ingredient for functional drinks, combining it with vitamins, antioxidants, and natural extracts to appeal to health-conscious consumers. The key driver in this segment is the global shift toward convenience-oriented consumption and on-the-go lifestyles, particularly among urban populations. Hospitality applications, including hotels, cafés, restaurants, and specialty tea houses, are also witnessing consistent growth. The expansion of global café culture, particularly in Asia-Pacific and North America, has led to a greater emphasis on curated tea menus and premium tea experiences. This segment is driven by the premiumization of dining experiences, where consumers increasingly expect high-quality beverage offerings alongside food services. Emerging applications in nutraceuticals and cosmetics are creating new demand avenues for black tea extracts. The high antioxidant content of black tea makes it a valuable ingredient in skincare products, dietary supplements, and functional wellness formulations. The leading driver for this segment is the global wellness trend, which emphasizes natural and plant-based ingredients that support health, anti-aging, and holistic well-being. As research continues to highlight the bioactive properties of black tea polyphenols, its application scope is expected to expand further beyond traditional beverage consumption.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels in the global black tea market, accounting for approximately 35% of total market share. These retail formats offer extensive product variety, competitive pricing, and convenient accessibility, making them the preferred purchasing point for a wide range of consumers. The primary driver for this segment is the strong presence of organized retail infrastructure in both developed and emerging economies, combined with consumer preference for physical product evaluation before purchase. However, online retail is emerging as the fastest-growing distribution channel, driven by the rapid expansion of e-commerce platforms and digital payment ecosystems. Consumers are increasingly purchasing tea products through online marketplaces and direct-to-consumer brand websites, attracted by convenience, subscription models, and access to niche and premium products. The key driver in this segment is digital penetration and changing consumer behavior, particularly among younger demographics who prefer personalized shopping experiences and doorstep delivery. Specialty stores continue to play an important role in the premium tea segment, offering curated selections, expert recommendations, and experiential retail environments. These outlets are particularly influential in developed markets where consumers seek high-quality, artisanal, and single-origin teas. The growth driver here is the increasing consumer willingness to explore premiumization and experiential purchasing rather than purely price-based decisions. Foodservice channels, including cafés, restaurants, and hotels, are also contributing significantly to market expansion. The rise of café culture and specialty tea menus has elevated tea consumption beyond traditional home usage, positioning it as a lifestyle beverage. This segment is driven by experiential consumption trends and the integration of tea into social and hospitality experiences.

Form Insights

Tea bags continue to dominate the global black tea market with approximately 42% share, primarily due to their convenience, portability, and standardized portioning. The widespread adoption of tea bags is supported by busy urban lifestyles, where consumers prioritize ease of preparation and minimal cleanup. The leading driver for this segment is convenience-oriented consumption, particularly in office environments and households with time constraints. Loose leaf tea maintains a strong presence in traditional and premium markets, appealing to consumers who value authenticity, flavor depth, and brewing control. This segment is particularly popular among tea connoisseurs and specialty tea retailers. The primary driver of growth in loose leaf tea is the premiumization trend, where consumers associate loose tea with higher quality and artisanal craftsmanship. Instant black tea powder and ready-to-drink (RTD) formats are experiencing rapid growth due to increasing demand for on-the-go consumption. RTD teas, in particular, are benefiting from innovations in packaging, flavor diversification, and functional beverage formulations. The key driver in this segment is lifestyle convenience, combined with the rising demand for functional beverages that offer both refreshment and health benefits. The growing innovation in product formats is reshaping the competitive landscape, encouraging manufacturers to diversify beyond traditional tea offerings.

Explore more data points, trends and opportunities Download Free Sample Report

Black Tea Market Segmentations

By Product Type

- Orthodox Black Tea

- CTC (Crush, Tear, Curl) Black Tea

- Specialty Black Tea

- Flavored & Decaffeinated Black Tea

By Form

- Loose Leaf Tea

- Tea Bags

- Instant Black Tea Powder

- Ready-to-Drink (RTD) Black Tea

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail/E-commerce

- Specialty Stores

- Foodservice Channels

By End-Use

- Household Consumption

- Food & Beverage Industry

- Hospitality Sector

- Nutraceutical & Pharmaceutical Applications

- Cosmetics & Personal Care

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global black tea market with approximately 45% share in 2025, driven primarily by strong consumption in India and China. India remains both the largest consumer and one of the leading producers of black tea globally, supported by a deeply embedded tea-drinking culture and extensive domestic production infrastructure. China, while traditionally associated with green tea, has significantly expanded its black tea production and consumption, particularly in urban centers where Western-style beverages are gaining popularity. The leading growth drivers in Asia-Pacific include rapid urbanization, population expansion, rising disposable incomes, and strong cultural affinity for tea consumption. Additionally, increasing export activity from countries such as Sri Lanka, Indonesia, and Vietnam further strengthens the region’s position as a global supply hub. The expansion of organized retail and e-commerce platforms has also improved accessibility, driving higher per capita consumption across both rural and urban populations.

Europe

Europe accounts for approximately 20% of the global black tea market, with the United Kingdom, Germany, and Russia serving as major consumption centers. The United Kingdom remains a mature yet stable market with deeply ingrained tea consumption habits, where tea is considered a daily staple across all age groups. Germany is witnessing rising demand for organic, fair-trade, and specialty teas, reflecting broader sustainability and health-conscious consumption trends. Russia continues to be one of the largest importers of black tea, driven by consistently high consumption levels. The key drivers in Europe include premiumization, sustainability concerns, and growing interest in ethical sourcing. Consumers are increasingly prioritizing environmentally responsible production methods, organic certification, and transparent supply chains. Additionally, the diversification of tea offerings in cafés and retail outlets is contributing to sustained demand growth in the region.

North America

North America holds nearly 15% of the global market share, with the United States and Canada leading consumption. The region is experiencing strong growth in ready-to-drink tea products and functional beverages, driven by increasing consumer focus on health and wellness. Black tea is being repositioned as a functional ingredient in energy drinks, detox beverages, and antioxidant-rich formulations. The primary driver in North America is the shift toward health-oriented consumption patterns, combined with rising demand for convenient beverage options. Younger consumers, in particular, are driving innovation in flavored and functional tea categories, while premium tea shops and specialty cafés are expanding the cultural footprint of tea consumption.

Middle East & Africa

The Middle East & Africa region accounts for approximately 12% of the global market, with strong import demand from countries such as the United Arab Emirates and Saudi Arabia. Tea is a deeply embedded cultural beverage across many African nations, particularly in Kenya, which is one of the world’s largest exporters of black tea. Key growth drivers in this region include strong cultural consumption patterns, expanding trade networks, and increasing urbanization. Kenya’s dominance in production ensures a stable supply base, while rising population growth and expanding retail infrastructure continue to support domestic consumption growth across African markets.

Latin America

Latin America represents approximately 8% of the global black tea market, with Brazil and Argentina leading regional consumption. While traditional consumption levels remain lower compared to other regions, the market is gradually expanding due to changing beverage preferences and increasing awareness of tea’s health benefits. The primary drivers in Latin America include growing health consciousness, diversification of beverage choices beyond coffee, and increasing availability of imported tea products. Urbanization and exposure to global beverage trends are also contributing to gradual but steady market expansion across the region.