Bitters Market Size

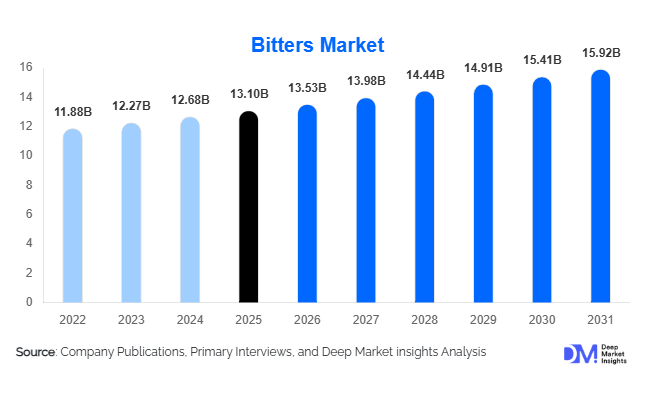

According to Deep Market Insights, the global bitters market size was valued at USD 13.1 billion in 2025 and is projected to grow from USD 13.53 billion in 2026 to reach USD 15.92 billion by 2031, expanding at a CAGR of 3.3 % during the forecast period (2026–2031). The bitters market growth is primarily driven by the rising global cocktail culture, increasing demand for premium and craft beverages, and growing consumer awareness of botanical and digestive wellness products. Expanding adoption of non-alcoholic bitters in functional beverages and zero-proof cocktails is further accelerating market expansion across both developed and emerging economies.

Key Market Insights

- Premium cocktail culture continues to drive bitters consumption, with bars and mixologists using specialized bitters to enhance flavor complexity and differentiation.

- Non-alcoholic and functional bitters are emerging as high-growth categories, aligned with mindful drinking and wellness trends.

- North America dominates global demand, supported by mature cocktail ecosystems and strong craft beverage innovation.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, hospitality expansion, and rising disposable income.

- E-commerce channels are reshaping distribution, enabling small craft brands to reach global consumers directly.

- Botanical innovation and premiumization strategies are allowing manufacturers to command higher margins and build brand differentiation.

What are the latest trends in the bitters market?

Rise of Non-Alcoholic and Functional Bitters

The global shift toward low-alcohol and alcohol-free lifestyles is significantly influencing bitters innovation. Consumers increasingly seek complex flavor profiles without alcohol consumption, creating strong demand for zero-proof cocktail ingredients. Functional bitters infused with botanicals such as gentian root, citrus peel, and adaptogenic herbs are gaining popularity as digestive and wellness supplements. Beverage companies are incorporating bitters into functional sodas, kombucha, and botanical tonics, expanding their role beyond traditional mixology applications. This convergence of wellness and beverage innovation is transforming bitters into a cross-category ingredient spanning hospitality, retail, and nutraceutical sectors.

Craft and Artisanal Flavor Innovation

Small-batch and craft bitters producers are reshaping market dynamics through experimentation with exotic botanicals, regional ingredients, and unique flavor combinations. Consumers increasingly value authenticity, heritage recipes, and premium packaging, encouraging brands to emphasize storytelling and transparency in sourcing. Limited-edition releases and bartender collaborations are becoming common strategies for differentiation. Sustainable ingredient sourcing and organic certifications are also emerging as competitive advantages, particularly among younger consumers prioritizing ethical consumption.

What are the key drivers in the bitters market?

Expansion of Global Cocktail Culture

The rapid growth of craft cocktail bars and premium hospitality venues worldwide remains the strongest driver of bitters demand. Mixologists rely on bitters to balance sweetness, acidity, and aroma, making them essential ingredients in modern beverage preparation. Urban nightlife expansion, tourism recovery, and premium dining experiences continue to increase consumption volumes across developed and emerging markets.

Growing Interest in Botanical Wellness

Consumers are increasingly adopting natural digestive solutions and herbal remedies, boosting demand for non-alcoholic bitters positioned as functional wellness products. Rising awareness of gut health and plant-based formulations has expanded bitters consumption beyond alcoholic beverages into health-focused retail channels. Nutraceutical companies are leveraging botanical extracts traditionally used in bitters to develop innovative functional products.

What are the restraints for the global market?

Regulatory Complexity Across Markets

Bitters often fall into overlapping regulatory categories involving alcohol, herbal supplements, and food additives. Differences in taxation, labeling requirements, and alcohol content regulations across countries create operational challenges for global expansion, particularly for small craft producers.

Limited Consumer Awareness in Emerging Economies

In several developing markets, bitters remain a niche product with limited consumer understanding. Educational marketing and bartender-led promotion are required to build adoption, increasing initial market entry costs for brands.

What are the key opportunities in the bitters industry?

Functional Beverage Integration

The rapid expansion of functional beverages presents significant growth opportunities. Manufacturers are integrating bitters into ready-to-drink beverages, botanical sodas, and wellness tonics targeting digestion and immunity support. As consumers seek healthier alternatives to sugary drinks, bitters offer flavor complexity without excessive calories, enabling product innovation across beverage categories.

Premium Hospitality and Tourism Expansion

The growth of luxury hotels, craft bars, and experiential dining concepts globally is creating sustained institutional demand for bitters. Hospitality operators increasingly develop signature cocktails using proprietary bitters blends, opening opportunities for private-label partnerships and customized formulations. Emerging tourism markets across Asia and the Middle East further strengthen long-term demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.10 Billion |

| Market Size in 2026 | USD 13.53 Billion |

| Market Size in 2031 | USD 15.92 Billion |

| CAGR | 3.30% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global bitters market is primarily led by alcoholic bitters, which continue to account for the largest market share owing to their integral role in cocktail formulation, aperitif culture, and premium beverage experiences. The leading segment growth is strongly driven by the global resurgence of craft cocktails, expanding mixology culture, and increasing consumer preference for complex flavor profiles in alcoholic beverages. Professional bartenders and hospitality establishments rely heavily on alcoholic bitters as foundational flavor enhancers, ensuring consistent demand across developed and emerging markets. Additionally, premiumization trends within the spirits industry are encouraging manufacturers to introduce small-batch and artisanal bitters with unique botanical blends, further strengthening segment dominance.Non-alcoholic bitters are emerging as the fastest-growing product category, supported by the rapid expansion of the zero-alcohol and low-alcohol beverage movement. Increasing health awareness, moderation trends, and demand for functional beverages are encouraging consumers to seek sophisticated flavor alternatives without alcohol content. Herbal digestive bitters are also witnessing rising adoption among wellness-oriented consumers who associate botanical ingredients with digestive and metabolic benefits. Meanwhile, specialty craft bitters are expanding through flavor experimentation, localized ingredient sourcing, and premium branding strategies, appealing particularly to younger consumers seeking authenticity and differentiated taste experiences.

Application Insights

Alcoholic beverage preparation remains the leading application segment, primarily driven by the expanding global cocktail culture and increasing investments in premium hospitality experiences. The leading segment driver is the continuous innovation within bars, lounges, and restaurants, where bitters are essential for balancing flavor, enhancing aroma, and enabling signature drink creation. As mixology evolves into an experiential element of dining and nightlife, bitters usage has expanded significantly across both classic and contemporary cocktail recipes.Functional consumption applications are growing rapidly as bitters gain recognition for digestive health support and botanical wellness positioning. Consumers are increasingly incorporating bitters into daily routines as digestive tonics or functional beverage additives. Culinary applications are also gaining momentum, with chefs integrating bitters into sauces, marinades, desserts, and gourmet recipes to introduce depth and complexity of flavor. Additionally, beverage manufacturers are incorporating bitters into ready-to-drink cocktails, botanical sodas, flavored sparkling beverages, and premium tonics, expanding the application landscape beyond traditional alcohol-based usage and supporting long-term market diversification.

Distribution Channel Insights

On-trade distribution channels dominate bitters sales globally, supported by large-volume procurement from bars, restaurants, hotels, and premium hospitality venues. The leading segment driver is the continued expansion of experiential dining and nightlife industries, where cocktail innovation directly influences bitters consumption levels. Hospitality operators increasingly emphasize premium beverage offerings, which drives recurring demand for diverse bitters formulations.Off-trade retail channels, including specialty liquor stores, gourmet retailers, and premium supermarkets, remain essential for household consumption and gift purchases. Consumer interest in home mixology has strengthened retail sales, particularly in urban markets. E-commerce represents the fastest-growing distribution channel, driven by digital purchasing behavior, broader product accessibility, and the ability of niche craft brands to reach global audiences without traditional distribution barriers. Subscription-based beverage platforms and online specialty retailers are further influencing purchasing decisions by offering curated selections, educational content, and personalized recommendations that appeal to younger and digitally engaged consumers.

End-User Insights

The commercial hospitality sector represents the largest end-user segment within the bitters market, supported by ongoing innovation in cocktail menus and the growing importance of premium beverage experiences in customer engagement strategies. The leading segment driver is the rising global demand for experiential consumption, where bars and restaurants differentiate themselves through signature cocktails and customized flavor profiles enabled by bitters.Household consumers are increasingly adopting bitters as part of home mixology trends, fueled by social media influence, online tutorials, and increased availability of professional-grade ingredients through retail and e-commerce channels. Beverage manufacturers and nutraceutical companies are emerging as important institutional buyers, integrating bitters into functional beverages, botanical formulations, and wellness-focused drinks. Furthermore, the expansion of ready-to-drink cocktail production is strengthening industrial demand, as manufacturers incorporate bitters to achieve balanced flavor consistency at scale.

Explore more data points, trends and opportunities Download Free Sample Report

Bitters Market Segmentations

By Type

- Cocktail Bitters

- Aperitif Bitters

- Digestif Bitters

- Medicinal Bitters

By Application

- Restaurant Service

- Retail Service

Regional Insights

North America

North America holds the largest share of the global bitters market, accounting for approximately 32% of total demand. The United States leads regional consumption due to its mature craft cocktail ecosystem, extensive hospitality infrastructure, and strong presence of artisanal bitters manufacturers. Regional growth is driven by continued premiumization of alcoholic beverages, rising consumer interest in mixology culture, and increasing adoption of non-alcoholic spirits. The expansion of cocktail-focused restaurants, growing popularity of home bartending, and strong e-commerce penetration further accelerate market development. Canada is also witnessing steady growth supported by premium bar expansion, evolving consumer tastes, and increasing demand for low- and no-alcohol beverage alternatives.

Europe

Europe represents nearly 30% of global bitters demand, supported by longstanding aperitif and digestive traditions across Italy, Germany, and France. Regional growth is driven by deep-rooted cultural consumption patterns, strong heritage brands, and increasing innovation within premium cocktail establishments. The resurgence of classic European aperitif culture among younger consumers is revitalizing bitters usage, while craft distilleries continue to experiment with botanical formulations. Countries such as the United Kingdom and Spain are experiencing increased demand through modern cocktail bar expansion and tourism-driven hospitality growth. Europe’s well-established beverage manufacturing ecosystem and strong export capabilities further reinforce its position as a major global production and innovation hub.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, rising disposable income, and expanding hospitality sectors across China, India, Japan, and Australia. Regional growth is strongly supported by increasing Western beverage influence, growing middle-class populations, and rising demand for premium dining and nightlife experiences. India is emerging as a particularly high-growth market due to the rapid expansion of premium restaurants, increasing cocktail adoption in metropolitan cities, and a young consumer demographic exploring global beverage trends. Additionally, the growing popularity of functional beverages and botanical wellness products is encouraging the adoption of both alcoholic and non-alcoholic bitters throughout the region.

Latin America

Latin America is experiencing steady bitters market expansion led by Brazil and Mexico, where cocktail experimentation and tourism recovery are supporting increased consumption. Regional growth is driven by the revival of hospitality industries, expanding urban bar culture, and rising interest in premium spirits and craft beverages. Increasing international tourism and the influence of global mixology trends are encouraging bartenders to adopt bitters as essential flavor components. Local producers are also introducing regionally inspired botanical blends, contributing to product diversification and gradual market penetration.

Middle East & Africa

The Middle East and Africa region is witnessing growing demand supported by luxury hospitality development, particularly in the United Arab Emirates and South Africa. Regional growth is driven by expanding high-end hotels, fine-dining establishments, and tourism-focused infrastructure investments. In markets with alcohol consumption restrictions, non-alcoholic bitters are gaining traction as functional and premium beverage ingredients, supporting innovation in alcohol-free cocktails and botanical drinks. Increasing consumer exposure to global culinary and beverage trends, combined with rising disposable income in urban centers, is expected to further strengthen market adoption across the region.

Key Players in the Bitters Market

- Angostura Limited

- Campari Group

- Fee Brothers

- Pernod Ricard

- Underberg AG

- Mast-Jägermeister SE

- The Bitter Truth GmbH

- Scrappy’s Bitters

- Bittermens LLC

- Sazerac Company

- Giffard

- Hella Cocktail Co.

- Dashfire Bitters

- Dr. Adam Elmegirab’s Bitters

- Ms. Better’s Bitters