Bitterness Suppressor & Flavor Carrier Market Size

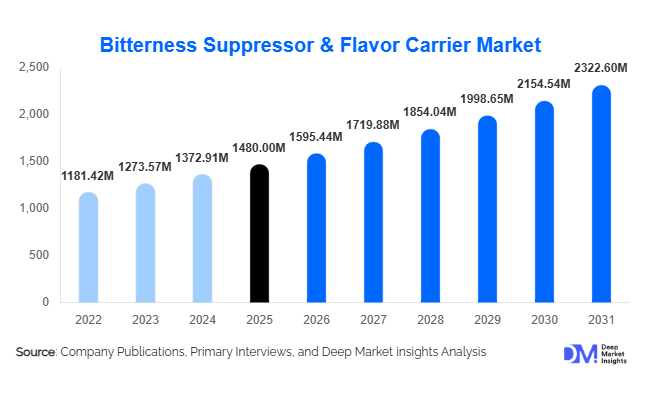

According to Deep Market Insights, the global bitterness suppressor & flavor carrier market size was valued at USD 1,480 million in 2025 and is projected to grow from USD 1,595.44 million in 2026 to reach USD 2,322.60 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). Market growth is primarily driven by rising demand for palatable pharmaceutical formulations, increasing reformulation of sugar-reduced beverages, and the rapid expansion of functional foods and nutraceutical products globally.

Bitterness suppressors are widely used to mask unpleasant taste profiles of active pharmaceutical ingredients (APIs), plant proteins, caffeine, and high-intensity sweeteners. Flavor carriers, including encapsulation systems and solubilizers, enhance flavor stability, improve bioavailability, and enable controlled release in complex formulations. As global regulatory bodies emphasize patient compliance and sugar reduction, manufacturers are increasingly integrating advanced taste modulation and delivery systems into product development pipelines.

Key Market Insights

- Pharmaceutical applications account for nearly 35% of global demand, driven by pediatric and geriatric oral formulations requiring advanced taste masking.

- Bitterness suppressors represent approximately 58% of total market revenue, reflecting strong adoption in both medicines and sugar-free beverages.

- Natural and bio-based suppressors are the fastest-growing segment, supported by clean-label and plant-based product trends.

- North America leads with around 34% market share in 2025, supported by strong pharmaceutical R&D and beverage reformulation initiatives.

- Asia-Pacific is the fastest-growing region, expanding at nearly 9.5% CAGR due to pharmaceutical manufacturing growth in China and India.

- The top five companies account for approximately 48% of global revenue, indicating moderate consolidation and high technological intensity.

What are the latest trends in the bitterness suppressor & flavor carrier market?

Shift Toward Natural and Fermentation-Derived Modulators

Consumer demand for clean-label ingredients has accelerated the development of fermentation-derived and plant-based bitterness suppressors. Food and beverage brands are increasingly replacing synthetic masking agents with natural alternatives that comply with GRAS and EFSA standards. Fermentation platforms enable scalable production of taste receptor blockers while maintaining label-friendly positioning. This shift is particularly visible in functional beverages, plant-protein drinks, and botanical supplements, where synthetic additives face consumer resistance.

Advanced Microencapsulation and Controlled Release Technologies

Microencapsulation systems, such as lipid-based, cyclodextrin-based, and spray-dried carriers, are gaining traction across the pharmaceutical and nutraceutical industries. These technologies protect volatile compounds, enhance solubility, and provide targeted release mechanisms. In pediatric syrups and chewable tablets, encapsulated systems improve patient compliance while preserving API stability. Innovation in nano-encapsulation and hybrid carrier matrices is further strengthening performance in ready-to-drink (RTD) beverages and high-active supplement formats.

What are the key drivers in the bitterness suppressor & flavor carrier market?

Expansion of the Global Pharmaceutical Industry

The global pharmaceutical industry, valued at over USD 1.5 trillion in 2025, continues to expand oral solid and liquid dosage production. Many APIs possess inherently bitter taste profiles, necessitating masking systems to ensure adherence. Pediatric formulations, antibiotics, and mineral supplements represent high-volume applications. Growing generic drug manufacturing in the Asia-Pacific further strengthens demand for cost-effective yet efficient suppressor systems.

Sugar Reduction and Functional Beverage Reformulation

Regulatory sugar taxes across North America and Europe are compelling beverage manufacturers to adopt high-intensity sweeteners such as stevia and monk fruit. However, these sweeteners often introduce bitterness and aftertaste. Bitterness suppressors restore sensory balance, enabling large-scale reformulation without compromising flavor profiles. Functional beverages fortified with vitamins, caffeine, or plant extracts further rely on flavor carriers to maintain product stability.

What are the restraints for the global market?

High R&D and Customization Costs

Bitterness suppression often requires molecule-specific research and sensory validation. Receptor-level studies and encapsulation trials increase development costs, posing entry barriers for smaller manufacturers. Customized pharmaceutical-grade systems require strict quality compliance, adding further cost pressures.

Regulatory Variability Across Regions

Approval standards differ significantly between the U.S., Europe, and Asia-Pacific. Novel taste modulators may face prolonged review timelines, delaying commercialization. Compliance costs and labeling restrictions remain ongoing challenges.

What are the key opportunities in the bitterness suppressor & flavor carrier industry?

Pediatric and Geriatric Drug Formulations

Aging populations and expanding pediatric drug access programs are creating consistent demand for palatable medicines. Governments are encouraging compliance-focused formulation, offering strong long-term growth prospects for pharmaceutical-grade suppressors and encapsulated carriers.

Plant-Based and Functional Nutrition Expansion

The rapid rise of plant-based proteins and botanical supplements presents significant opportunity. These ingredients often contain bitter polyphenols and alkaloids, requiring advanced masking systems. Companies investing in natural and hybrid carrier technologies can capture high-growth segments within sports nutrition, immunity boosters, and protein beverages.

Product Type Insights

Bitterness suppressors remain the leading product category, accounting for approximately 58% of total market revenue in 2025, driven primarily by expanding pharmaceutical formulations and large-scale sugar-reduction initiatives in beverages. The dominant growth driver for this segment is the rising demand for taste masking in oral solid dosages, pediatric syrups, and nutraceutical chewables, where unpleasant API profiles directly impact patient compliance. In addition, beverage manufacturers reformulating with stevia, monk fruit, and caffeine rely heavily on suppressors to eliminate lingering aftertaste, further strengthening this segment’s leadership position. Within this category, natural and receptor-based suppressors are gaining accelerated adoption due to clean-label requirements and regulatory acceptance.

Flavor carriers account for approximately 42% of global revenue, with encapsulation systems emerging as the fastest-growing sub-segment. The key driver here is the need for improved stability, solubility, and controlled release of volatile or reactive ingredients in functional beverages and nutraceuticals. Lipid-based and cyclodextrin encapsulation technologies are particularly expanding in high-moisture and ready-to-drink (RTD) applications. By form, powder-based systems hold nearly 46% share, supported by their superior shelf stability, compatibility with tablet compression, and suitability for dry beverage mixes and sachets. Powder dominance is further reinforced by lower transportation costs and ease of integration into automated manufacturing lines.

Application Insights

Pharmaceuticals represent the largest application segment, accounting for nearly 35% of total revenue in 2025. The primary driver for this leadership is regulatory emphasis on patient adherence, particularly in pediatric and geriatric medicine. Antibiotics, mineral supplements, and alkaloid-based APIs require advanced taste masking, making bitterness suppressors and encapsulated carriers essential excipients. Rising generic drug production in Asia-Pacific and North America further accelerates demand.

Food and beverages constitute a significant secondary application, driven by global sugar reduction mandates and growth in functional drinks. Nutraceuticals are among the fastest-growing segments, expanding at over 8% CAGR, supported by a global supplements market exceeding USD 450 billion. High-active formulations containing botanicals, plant proteins, and amino acids frequently require masking technologies. Oral care and animal nutrition remain smaller segments but demonstrate steady growth due to increasing focus on palatable therapeutic and preventive formulations.

Distribution Channel Insights

Direct B2B ingredient supply dominates with approximately 62% market share, as multinational pharmaceutical and food manufacturers prefer long-term contracts to ensure formulation consistency, regulatory compliance, and traceability. This channel’s leadership is driven by high customization requirements and strict quality standards, particularly in pharmaceutical-grade applications.

Contract formulation partnerships are growing steadily, especially in nutraceutical and mid-sized pharmaceutical companies that outsource R&D-intensive taste modulation solutions. Customized private blends are gaining traction among beverage brands seeking proprietary flavor profiles and competitive differentiation. The increasing integration of technical service support alongside ingredient supply is further strengthening direct supplier-manufacturer relationships.

End-Use Industry Insights

Pharmaceutical manufacturing remains the largest end-use industry, supported by expanding generic drug exports from India and China and continued innovation in oral dosage forms in the U.S. and Europe. The global push for improved patient compliance in chronic disease treatment further strengthens demand for advanced suppressor systems. Nutraceutical production is accelerating globally, particularly in North America and Europe, where preventive healthcare spending continues to rise.

Export-driven supplement manufacturing in Asia-Pacific is significantly boosting demand for encapsulated flavor carriers, especially in powder and sachet formats. Emerging applications in cannabis-infused beverages, fortified confectionery, and high-protein sports nutrition products are creating niche but high-margin growth avenues. As functional ingredients become more concentrated, the reliance on effective masking and delivery systems will intensify.

| By Product Type | By Application | By Distribution Channel | By Form | By Source |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, with the United States alone contributing nearly 28% of worldwide demand. The primary regional growth driver is the advanced pharmaceutical ecosystem, including high R&D spending, strong generic production, and regulatory emphasis on patient-centric drug formulations. Sugar-reduction regulations and strong demand for functional beverages further stimulate the adoption of natural bitterness suppressors. Canada contributes by expanding nutraceutical manufacturing and increasing clean-label product launches. The region benefits from strong innovation pipelines and established supplier networks.

Europe

Europe captures around 27% of global revenue, led by Germany, France, and the UK. The key driver for regional growth is stringent sugar taxation policies and clean-label regulations encouraging natural ingredient adoption. European consumers show a strong preference for plant-based and functional nutrition products, boosting suppressor demand. Additionally, robust pharmaceutical manufacturing in Germany and Switzerland supports steady uptake of pharmaceutical-grade carriers. Sustainability mandates are also pushing manufacturers toward bio-based encapsulation technologies.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of the market share and is the fastest-growing region at nearly 9.5% CAGR. China and India drive growth through large-scale generic drug manufacturing and expanding export markets. Government initiatives supporting domestic pharmaceutical ingredient production and “Make in India”-type industrial programs accelerate local capacity expansion. Rising middle-class consumption of functional beverages and dietary supplements further boosts demand. Japan contributes through technological leadership in microencapsulation and advanced delivery systems.

Latin America

Latin America holds around 4% share, with Brazil and Mexico leading regional demand. Growth drivers include increasing OTC drug consumption, expanding beverage reformulation, and rising health awareness among urban populations. Regional pharmaceutical manufacturing expansion and improving regulatory frameworks are gradually strengthening local demand for advanced taste modulation technologies.

Middle East & Africa

The Middle East & Africa region represents about 6% of global demand. Growth is primarily driven by increasing pharmaceutical imports, expanding local formulation facilities in Saudi Arabia and South Africa, and government investments aimed at strengthening domestic drug manufacturing capacity. Rising demand for fortified foods and supplements in GCC countries is also contributing to the steady adoption of flavor carriers and suppressors.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Bitterness Suppressor & Flavor Carrier Market

- Givaudan

- International Flavors & Fragrances (IFF)

- Symrise

- Firmenich

- Tate & Lyle

- Sensient Technologies

- Kerry Group

- Ingredion

- Cargill

- BASF

- DSM-Firmenich

- Roquette

- Ashland

- Dow

- DuPont