Biostimulant Market Size

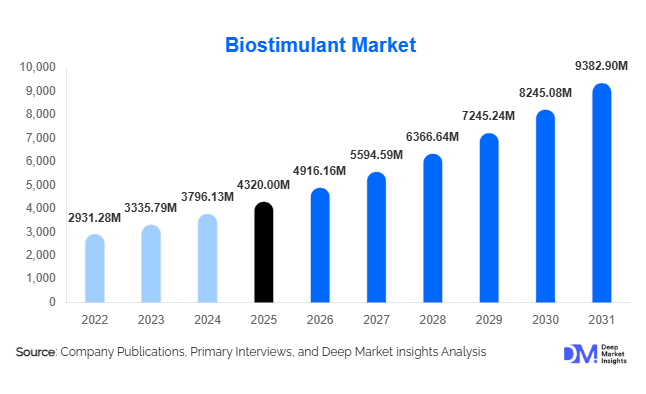

According to Deep Market Insights, the global biostimulant market size was valued at USD 4,320 million in 2025 and is projected to grow from USD 4,916.16 million in 2026 to reach USD 9,382.90 million by 2031, expanding at a CAGR of 13.8% during the forecast period (2026–2031). Market growth is primarily driven by increasing adoption of sustainable agricultural practices, rising concerns regarding soil degradation, and growing demand for residue-free food production worldwide. Farmers are increasingly integrating biostimulants into crop nutrition programs to enhance nutrient uptake efficiency, improve stress tolerance, and stabilize yields under changing climatic conditions.

Key Market Insights

- Biostimulants are transitioning from niche biological inputs to mainstream crop productivity solutions, supported by sustainability regulations and fertilizer optimization strategies.

- Seaweed-based and microbial formulations dominate innovation pipelines, offering improved plant resilience against drought and abiotic stress.

- Europe leads global adoption due to stringent agrochemical regulations and strong organic farming penetration.

- Asia-Pacific is the fastest-growing regional market, driven by agricultural modernization in China and India.

- High-value crops such as fruits and vegetables account for significant consumption due to quality and export requirements.

- Integration with precision agriculture technologies is improving application efficiency and farmer ROI, accelerating commercialization.

What are the latest trends in the biostimulant market?

Shift Toward Regenerative and Climate-Resilient Agriculture

Biostimulants are increasingly positioned as essential inputs within regenerative agriculture systems. Farmers are adopting products that improve soil microbial health, enhance root development, and reduce dependency on synthetic fertilizers. Climate volatility, including drought and salinity stress, is accelerating demand for biological crop enhancement solutions capable of stabilizing productivity. Governments and agricultural organizations are promoting soil restoration initiatives, further supporting adoption. This trend is particularly visible in Europe and Asia, where sustainable farming targets are driving rapid transition toward biological inputs.

Technological Advancements in Microbial Formulations

Advancements in biotechnology and fermentation processes are improving the consistency and efficacy of microbial biostimulants. Companies are developing strain-specific formulations targeting nutrient uptake, stress mitigation, and yield enhancement. Digital agriculture platforms now integrate biostimulant application recommendations based on soil analytics and crop monitoring data. Precision agriculture tools enable optimized dosage and timing, reducing input waste while improving productivity outcomes. These innovations are increasing farmer confidence and enabling premium product positioning across developed agricultural markets.

What are the key drivers in the biostimulant market?

Rising Demand for Sustainable Crop Productivity

Growing pressure to increase agricultural output while reducing environmental impact is a major driver of biostimulant adoption. These products enhance nutrient-use efficiency and plant metabolism, allowing farmers to achieve higher yields with reduced fertilizer inputs. Sustainability certifications and export standards increasingly favor biologically supported crop systems, encouraging widespread adoption across commercial agriculture.

Regulatory Restrictions on Chemical Inputs

Governments worldwide are tightening regulations on agrochemicals to reduce environmental damage and food residue levels. Biostimulants offer a compliant alternative that supports plant growth without contributing to chemical load. European regulatory frameworks and fertilizer reduction strategies have significantly accelerated market expansion, influencing adoption trends globally.

What are the restraints for the global market?

Lack of Regulatory Harmonization

Biostimulants are classified differently across countries, sometimes as fertilizers and sometimes as biological products. This regulatory fragmentation creates approval delays, increases compliance costs, and slows market entry for manufacturers operating internationally.

Performance Variability and Farmer Awareness

Product effectiveness varies depending on soil composition, climate, and crop type, which can lead to inconsistent results. Limited farmer education and agronomic advisory support in developing regions remain barriers to faster adoption, particularly among smallholder farmers unfamiliar with biological inputs.

What are the key opportunities in the biostimulant industry?

Expansion of Organic and Export-Oriented Agriculture

The rapid growth of organic farming and residue-free export markets presents strong opportunities for biostimulant suppliers. Export-focused growers increasingly rely on biological inputs to meet stringent food safety requirements. Countries such as India, Spain, and Brazil are witnessing rising demand as agricultural exports expand, creating opportunities for new entrants offering certified organic-compatible products.

Precision Agriculture Integration

The integration of biostimulants with digital farming platforms is creating a new growth avenue. AI-driven farm analytics enable precise application schedules, improving yield predictability and input efficiency. Partnerships between agri-tech firms and biological input manufacturers are enabling subscription-based crop management models, strengthening long-term farmer engagement and recurring revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4320 Million |

| Market Size in 2026 | USD 4916.16 Million |

| Market Size in 2031 | USD 9382.90 Million |

| CAGR | 13.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global biostimulants market demonstrates strong diversification across product categories, with seaweed extract-based biostimulants maintaining a leading position and accounting for approximately 29% of the global market share in 2025. Their dominance is primarily supported by scientifically validated benefits such as enhanced plant stress tolerance, improved nutrient uptake efficiency, and consistent yield performance across varying climatic conditions. Rising climate variability and increasing occurrences of drought and salinity stress have encouraged farmers to adopt seaweed-derived formulations as preventive crop management solutions. In addition, advancements in extraction technologies and the availability of region-specific seaweed species are enabling manufacturers to develop targeted formulations suited for diverse crop systems.Microbial biostimulants are emerging as one of the fastest-expanding product segments, supported by rapid advancements in biological research, microbial strain optimization, and fermentation technologies. Increasing awareness regarding soil microbiome health and its role in sustainable agriculture is driving adoption among commercial growers seeking long-term soil productivity improvements. These products enhance nutrient solubilization, root development, and resistance to abiotic stress, making them increasingly attractive in precision agriculture systems. Continuous investments in biotechnology and regulatory acceptance of biological inputs are further accelerating commercialization across developed and emerging markets.

Amino acid and protein hydrolysate-based biostimulants continue to witness strong adoption, particularly in intensive horticulture and greenhouse cultivation, where crop quality and productivity optimization are critical. These products stimulate plant metabolism, enhance chlorophyll synthesis, and support rapid recovery from environmental stress. Their compatibility with integrated nutrient management programs and fertigation systems further strengthens their adoption among high-value crop producers.Humic substances remain a vital component of soil-conditioning solutions, especially in regions experiencing declining soil fertility and organic matter depletion. By improving soil structure, nutrient retention capacity, and microbial activity, humic-based biostimulants contribute to long-term soil regeneration. Growing concerns regarding soil degradation and sustainable land management practices are reinforcing demand for these formulations globally. Additionally, ongoing innovation in plant-derived biochemical and hybrid formulations is expanding product development pipelines, enabling manufacturers to deliver multifunctional solutions tailored to crop-specific requirements.

Application Insights

Foliar application represents the leading application segment, accounting for nearly 46% of the global market share, primarily driven by its ability to deliver rapid nutrient absorption and immediate physiological response in plants. The leading segment growth is supported by farmers’ increasing preference for solutions that provide visible crop improvements within shorter timeframes, particularly in high-value horticultural crops. Foliar spraying allows precise dosage control, reduces nutrient losses, and enhances stress mitigation during critical crop growth stages. The expanding adoption of precision agriculture equipment, drone-based spraying technologies, and advanced liquid formulations is further reinforcing the dominance of foliar applications across modern farming systems.Soil application continues to play a critical role in improving long-term soil health and biological activity. As regenerative agriculture practices gain momentum globally, growers are increasingly integrating soil-applied biostimulants to restore soil fertility, enhance microbial diversity, and improve nutrient cycling efficiency. This approach is particularly relevant in large-scale farming regions facing soil degradation and declining organic carbon levels.Seed treatment applications are gaining traction as farmers increasingly focus on early-stage crop establishment and uniform germination. Biostimulant-coated seeds enhance root development, improve nutrient accessibility during early growth phases, and increase resilience against environmental stress. The growing demand for high-performance seeds and integrated crop management strategies is expected to further accelerate adoption in this segment. Additionally, compatibility with drip irrigation and fertigation systems is supporting widespread usage of liquid biostimulants across technologically advanced agricultural operations.

Crop Type Insights

Fruits and vegetables constitute the leading crop segment, accounting for approximately 34% of global demand, driven primarily by the high economic value of these crops and strict quality requirements associated with export-oriented agriculture. The leading segment growth is supported by increasing consumer demand for residue-free produce, improved shelf life, and enhanced visual quality characteristics such as size, color, and uniformity. Biostimulants help growers achieve higher productivity while reducing chemical input dependency, making them particularly attractive for horticultural cultivation systems.Row crops, including cereals and oilseeds, are witnessing growing adoption as farmers increasingly use biostimulants to optimize fertilizer utilization efficiency and maintain yield stability under unpredictable weather conditions. Rising input costs and sustainability pressures are encouraging large-scale farmers to integrate biological solutions into conventional farming programs. Plantation crops such as sugarcane, coffee, cocoa, and tea are emerging as strong growth areas due to the need for productivity enhancement and soil health improvement over long cultivation cycles.Turf and ornamental crops also contribute to steady market demand, supported by expanding urban landscaping projects, sports infrastructure development, and professional turf management practices. Biostimulants are increasingly used in these applications to enhance plant vigor, stress resistance, and aesthetic quality while minimizing chemical fertilizer usage.

Formulation Insights

Liquid formulations dominate the global biostimulants market, accounting for nearly 62% of total market share, largely due to superior ease of application and compatibility with modern irrigation and spraying technologies. The leading segment growth is driven by increasing adoption of precision agriculture practices, fertigation systems, and automated spraying equipment, which favor liquid-based inputs for uniform distribution and rapid absorption. Liquid formulations enable efficient nutrient delivery, improved bioavailability, and flexible application timing, making them highly suitable for intensive farming operations.Dry and granular formulations continue to maintain relevance in large-scale agriculture due to advantages in storage stability, transportation efficiency, and longer shelf life. These formulations are particularly preferred in regions with limited cold-chain infrastructure or where bulk handling is required. Technological advancements in formulation stabilization, encapsulation techniques, and shelf-life enhancement are further improving product performance, thereby strengthening overall adoption across global agricultural markets.

Explore more data points, trends and opportunities Download Free Sample Report

Biostimulant Market Segmentations

By Product Type

- Seaweed Extracts

- Microbial Biostimulants

- Amino Acids Protein Hydrolysates

- Humic Fulvic Substances

- Other Botanical Biochemical Extracts

By Application

- Foliar Treatment

- Soil Treatment

- Seed Treatment

By Crop Type

- Fruits Vegetables

- Cereals Grains

- Oilseeds Pulses

- Turf Ornamentals

- Plantation Crops

By Formulation

- Liquid Biostimulants

- Dry/Granular Biostimulants

By Distribution Channel

- Agricultural Input Dealers Retailers

- Direct Sales (B2B/Farm Contracts)

- Cooperatives Farmer Organizations

- Online Agri-Input Platforms

Regional Insights

North America

North America accounts for nearly 22% of the global biostimulants market, with the United States serving as the primary contributor. Regional growth is driven by increasing adoption of regenerative agriculture practices, strong technological integration in farming operations, and rising awareness regarding soil health management. Large-scale cultivation of corn, soybean, and specialty crops is encouraging growers to adopt biostimulants to enhance nutrient efficiency and reduce dependency on synthetic fertilizers. Supportive research initiatives, advanced agricultural extension services, and strong collaboration between biotechnology companies and farming communities are accelerating product adoption. Additionally, sustainability commitments by food supply chains and retailers are influencing farmers to transition toward biologically derived crop inputs.

Europe

Europe dominates the global market with approximately 36% market share in 2025, supported by stringent environmental regulations and widespread adoption of sustainable agricultural practices. Countries such as Spain, Italy, France, and Germany lead consumption due to strong organic farming penetration and policy-driven reductions in chemical fertilizer usage. Regional growth is further supported by the European Union’s sustainability frameworks promoting environmentally friendly crop inputs and carbon footprint reduction. Intensive greenhouse horticulture, high-value fruit cultivation, and export-focused agriculture continue to drive strong demand. Established regulatory clarity for biostimulants within the region also provides manufacturers with a stable commercialization environment, encouraging innovation and product development.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 15% CAGR, driven by increasing food demand, rapid agricultural modernization, and supportive government initiatives promoting sustainable farming practices. China and India remain key contributors as governments implement fertilizer reduction programs and encourage adoption of biological crop inputs to improve soil health. Rising population pressure, shrinking arable land availability, and climate-related production risks are motivating farmers to adopt productivity-enhancing solutions such as biostimulants. Expansion of horticulture exports, increasing awareness among smallholder farmers, and growing investments by international agrochemical companies in regional distribution networks are further accelerating market growth.

Latin America

Latin America is emerging as a high-potential market, led by Brazil and Argentina, where large-scale commercial agriculture drives strong product demand. Brazil alone accounts for nearly 60% of regional consumption, supported by extensive soybean, corn, and sugarcane cultivation. Regional growth is fueled by the need to improve yield stability under variable climatic conditions and enhance nutrient efficiency in highly intensive farming systems. Export-oriented agricultural production and increasing adoption of sustainable farming practices are encouraging growers to integrate biostimulants into crop nutrition programs. Favorable climatic conditions allowing multiple crop cycles annually further expand usage opportunities across the region.

Middle East & Africa

The Middle East and Africa region is witnessing steadily increasing adoption of biostimulants, primarily driven by water scarcity challenges, desert agriculture expansion, and the need to enhance crop resilience under extreme climatic conditions. Countries such as Israel, South Africa, and the United Arab Emirates are investing heavily in advanced irrigation technologies and biological crop inputs to improve water-use efficiency and agricultural productivity. Government-supported agricultural innovation programs, greenhouse cultivation expansion, and rising food security concerns are contributing to regional market growth. Increasing adoption of precision irrigation systems and controlled-environment agriculture is further creating opportunities for biostimulant manufacturers across the region.

Key Players in the Biostimulant Market

- Valagro (Syngenta Group)

- UPL Ltd.

- BASF SE

- Corteva Agriscience

- FMC Corporation

- Koppert Biological Systems

- Biolchim S.p.A.

- Tradecorp International

- Haifa Group

- Isagro S.p.A.

- Lallemand Plant Care

- Acadian Plant Health

- Italpollina S.p.A.

- BioAtlantis Ltd.

- Rovensa Group