Binders Market Size

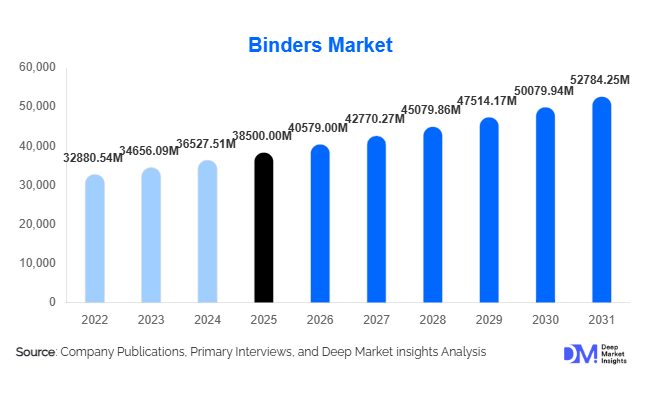

According to Deep Market Insights, the global binders market size was valued at USD 38,500 million in 2025 and is projected to grow from USD 40,579.00 million in 2026 to reach USD 52,784.25 million by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The binders market growth is primarily driven by rising demand from construction and infrastructure development, increasing consumption in paints & coatings applications, and the rapid expansion of energy storage technologies such as lithium-ion batteries, which require advanced binder formulations for electrode stability and performance enhancement.

Key Market Insights

- Polymeric binders dominate the global market, driven by their extensive use in coatings, adhesives, and construction materials due to superior flexibility and performance.

- Water-based binders are witnessing rapid adoption as environmental regulations push industries toward low-VOC and sustainable formulations.

- Asia-Pacific leads global demand, supported by large-scale infrastructure development, manufacturing expansion, and battery production in China and India.

- Construction & infrastructure remains the largest end-use segment, accounting for the majority of binder consumption globally.

- Battery binders are the fastest-growing application area, fueled by electric vehicle adoption and renewable energy storage expansion.

- Technological innovation in bio-based and high-performance binders is reshaping competitive dynamics across industries.

What are the latest trends in the binders market?

Shift Toward Sustainable and Bio-Based Binders

The binders market is experiencing a strong shift toward sustainability, driven by tightening environmental regulations in Europe, North America, and parts of Asia. Manufacturers are increasingly developing bio-based binders derived from starch, lignin, and protein sources to reduce dependence on petrochemicals. These alternatives are gaining traction in packaging, paper, and construction applications due to their lower carbon footprint and improved biodegradability. Water-based acrylic and polyurethane systems are also replacing solvent-based binders, helping industries meet strict VOC emission standards. This transition is further supported by corporate ESG commitments and green procurement policies, which are encouraging end-users to adopt environmentally responsible material solutions across supply chains.

Expansion of High-Performance Battery Binder Technologies

With the rapid rise of electric vehicles and renewable energy storage systems, advanced binder technologies for lithium-ion batteries are becoming a critical innovation area. Manufacturers are developing binders with improved electrochemical stability, silicon compatibility, and enhanced adhesion properties to improve battery lifecycle performance. Water-based PVDF alternatives and conductive polymer binders are gaining attention as they improve safety and reduce environmental impact. This trend is particularly strong in the Asia-Pacific, where large-scale battery manufacturing ecosystems are driving continuous R&D investments. The integration of nanotechnology and functional polymers is also enabling next-generation binder systems tailored for high-energy-density applications.

What are the key drivers in the binders market?

Rising Global Construction and Infrastructure Development

The construction sector is the largest consumer of binders, accounting for a significant share of global demand. Rapid urbanization, smart city projects, and infrastructure modernization programs across emerging economies are driving large-scale consumption of cementitious and polymer-modified binders. Governments in Asia-Pacific, the Middle East, and Africa are heavily investing in residential, commercial, and transportation infrastructure, boosting long-term demand. The increasing use of advanced construction materials with improved durability and strength is further supporting binder adoption in large-scale engineering projects.

Growth of Paints, Coatings, and Adhesives Industry

The paints and coatings industry is another major growth driver, with binders playing a critical role in film formation, adhesion, and durability. Rising demand for decorative coatings, automotive finishes, and industrial protective coatings is fueling consumption of acrylic and styrene-butadiene binders. The shift toward water-based coatings is accelerating the adoption of environmentally friendly binder systems. Additionally, the adhesives segment is growing due to increased demand in packaging, woodworking, and automotive assembly applications, further strengthening market expansion.

What are the restraints for the global market?

Volatility in Raw Material Prices

The binders market is highly dependent on petrochemical-derived raw materials, making it vulnerable to crude oil price fluctuations. This volatility directly impacts production costs and profit margins, especially for polymeric binder manufacturers. Frequent price instability creates challenges in long-term pricing contracts and reduces cost predictability for end-users. Smaller manufacturers are particularly affected due to their limited ability to hedge against raw material cost variations.

Strict Environmental and Regulatory Compliance Requirements

Increasingly stringent environmental regulations regarding VOC emissions and hazardous chemical usage are restraining the growth of solvent-based binders. Manufacturers are required to invest heavily in R&D and process modifications to comply with global sustainability standards. Compliance with regional regulations such as REACH in Europe and EPA guidelines in North America increases operational complexity and cost burdens, particularly for small and mid-sized players.

What are the key opportunities in the binders industry?

Expansion of Electric Vehicle and Energy Storage Applications

The rapid growth of electric vehicles and renewable energy systems presents a major opportunity for binder manufacturers. Lithium-ion battery production requires specialized binders that ensure electrode integrity and improve energy efficiency. As global EV adoption accelerates, demand for advanced binder formulations is increasing significantly. Companies investing in conductive polymers, silicon-compatible binders, and water-based systems are well-positioned to capture high-growth opportunities in this emerging segment.

Growth of Bio-Based and Circular Economy Solutions

Increasing focus on sustainability and circular economy models is driving demand for bio-based binders. Industries such as packaging, construction, and textiles are shifting toward renewable and biodegradable materials. Governments are also promoting green chemistry initiatives and low-carbon manufacturing practices. This creates strong opportunities for innovation in lignin-based, starch-based, and protein-based binder systems that reduce environmental impact while maintaining performance standards.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38500 Million |

| Market Size in 2026 | USD 40579 Million |

| Market Size in 2031 | USD 52784.25 Million |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Polymeric binders dominate the global market, accounting for approximately 48% of total market share in 2025, primarily due to their superior performance characteristics such as flexibility, adhesion strength, and resistance to environmental degradation. Their widespread use across paints & coatings, adhesives, and advanced construction materials continues to drive their leadership. The increasing demand for high-performance coatings in automotive and industrial applications, along with the shift toward water-based polymer systems, is further strengthening this segment. Inorganic binders, including cement-based and silicate systems, remain indispensable in large-scale construction and infrastructure projects, particularly in emerging economies where cost efficiency and structural durability are critical. Meanwhile, bio-based binders are emerging as a high-growth niche segment, supported by stringent environmental regulations and rising demand for sustainable materials. In terms of form, liquid binders hold the largest share at around 60%, driven by ease of handling, uniform application, and compatibility with automated industrial processes. From a technology perspective, water-based binders account for over 55% of total demand, with growth driven by global regulatory pressures to reduce VOC emissions and increasing adoption across coatings, adhesives, and packaging applications.

Application Insights

Paints & coatings represent the largest application segment, contributing approximately 32% of the global market share, driven by strong demand from construction, automotive, and industrial sectors. The segment’s dominance is supported by continuous growth in residential and commercial construction, along with increasing demand for protective and decorative coatings. Construction materials, including cement additives and mortars, form the second-largest segment, benefiting from global infrastructure development and urbanization trends. Adhesives & sealants are witnessing steady growth due to rising applications in packaging, automotive assembly, and electronics manufacturing, where high-performance bonding solutions are essential. The battery electrode segment is the fastest-growing application, fueled by exponential growth in lithium-ion battery production for electric vehicles and renewable energy storage systems. This segment is expected to significantly increase its market share over the forecast period. Additionally, paper and packaging applications are expanding steadily, supported by e-commerce growth and the global shift toward sustainable and recyclable packaging materials, which require advanced binder formulations for improved strength and durability.

Distribution Channel Insights

Direct sales dominate the binders market, accounting for over 65% of total market share, as large-scale industrial buyers prefer long-term supply agreements to ensure product consistency, cost stability, and reliable supply chains. This channel is particularly prevalent in industries such as construction, automotive, and coatings, where bulk procurement is standard practice. Distributors and chemical suppliers play a crucial role in serving small and medium-sized enterprises, especially in fragmented and developing markets where direct manufacturer access is limited. These intermediaries provide logistical support, technical assistance, and localized inventory management. Meanwhile, online industrial platforms are gradually gaining traction, driven by digital transformation in procurement processes. These platforms offer enhanced price transparency, faster order processing, and access to a broader supplier base, making them increasingly attractive for standardized binder products and smaller volume purchases.

End-Use Industry Insights

The construction & infrastructure sector leads global binder demand, accounting for approximately 35% of the market, driven by rapid urbanization, population growth, and large-scale government investments in infrastructure projects such as roads, bridges, and housing. The automotive and transportation sector is another significant consumer, utilizing binders extensively in coatings, adhesives, and composite materials to enhance durability and reduce vehicle weight. Electronics and energy storage represent the fastest-growing end-use segment, expanding at a CAGR of over 8%, driven by increasing demand for lithium-ion batteries in electric vehicles and renewable energy systems. The packaging and paper industries are also witnessing steady growth, supported by the rise of e-commerce and increasing consumer preference for sustainable packaging solutions. Additionally, emerging applications in industrial manufacturing and consumer goods are further diversifying binder demand across global markets.

Explore more data points, trends and opportunities Download Free Sample Report

Binders Market Segmentations

By Product Type

- Polymeric Binders

- Inorganic Binders

- Bio-Based / Natural Binders

By Application

- Paints & Coatings

- Construction Materials

- Adhesives & Sealants

- Battery Electrodes

- Paper & Packaging

- Textiles & Nonwovens

By Distribution Channel

- Direct Sales (B2B Contracts)

- Distributors & Chemical Suppliers

- Online Industrial Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global binders market, accounting for approximately 42% of the total market share in 2025, making it the largest and fastest-growing region. China alone contributes nearly 22% of global demand, driven by its massive construction sector, strong manufacturing base, and leadership in lithium-ion battery production. India is emerging as a high-growth market, supported by government initiatives such as infrastructure development programs, smart city projects, and industrial expansion. Japan and South Korea contribute significantly through advanced electronics, automotive manufacturing, and innovation in high-performance materials. Key growth drivers in the region include rapid urbanization, increasing foreign direct investment, expansion of manufacturing hubs, and strong government support for infrastructure and renewable energy projects. The presence of large-scale production facilities and cost-effective labor further enhances regional competitiveness.

North America

North America holds around 22% of the global market share, with the United States being the dominant contributor. The region’s growth is driven by strong demand for advanced coatings, renovation and refurbishment activities in the construction sector, and increasing investments in electric vehicle and battery manufacturing. The U.S. government’s focus on infrastructure modernization and clean energy initiatives is further boosting binder demand. Additionally, the presence of leading chemical manufacturers and strong R&D capabilities supports innovation in sustainable and high-performance binder technologies. Regulatory emphasis on low-VOC and environmentally friendly products is accelerating the transition toward water-based and bio-based binders across industries.

Europe

Europe accounts for approximately 20% of the global binders market, led by countries such as Germany, France, and the United Kingdom. The region is characterized by strict environmental regulations, which are driving rapid adoption of bio-based and low-VOC binder systems. Europe’s strong focus on sustainability, circular economy practices, and green building standards is a key growth driver. Additionally, the region’s well-established automotive and industrial sectors contribute significantly to binder demand, particularly for high-performance coatings and adhesives. Continuous investment in research and innovation, along with government support for sustainable technologies, is further strengthening Europe’s position as a leader in advanced binder solutions.

Latin America

Latin America is experiencing steady growth in the binders market, with key contributions from Brazil, Mexico, and Argentina. The region’s demand is primarily driven by infrastructure development, urban housing projects, and the expansion of manufacturing industries. Growth drivers include increasing foreign investments, improving economic stability, and rising demand for construction materials and packaging solutions. The automotive sector in Mexico and Brazil is also contributing to binder consumption, particularly in coatings and adhesives applications. However, market growth is somewhat moderated by economic fluctuations and limited technological advancements compared to developed regions.

Middle East & Africa

The Middle East & Africa region is witnessing growing demand for binders, driven by large-scale infrastructure and urban development projects in countries such as the UAE, Saudi Arabia, and South Africa. Government-led initiatives, including smart city developments and diversification of economies away from oil dependence, are key growth drivers. The construction boom across Africa, supported by population growth and urbanization, is significantly contributing to binder consumption. Additionally, increasing investments in industrialization and manufacturing are creating new opportunities for market expansion. While the region presents strong growth potential, challenges such as political instability and limited local production capabilities may impact overall market dynamics.

Key Players in the Binders Market

- BASF SE

- Dow Inc.

- Arkema Group

- Wacker Chemie AG

- Celanese Corporation

- Synthomer plc

- Trinseo PLC

- Ashland Global Holdings

- Evonik Industries AG

- DIC Corporation

- Allnex Group

- H.B. Fuller Company

- Sika AG

- Akzo Nobel N.V.

- Henkel AG