Beverage Processing Equipment Market Size

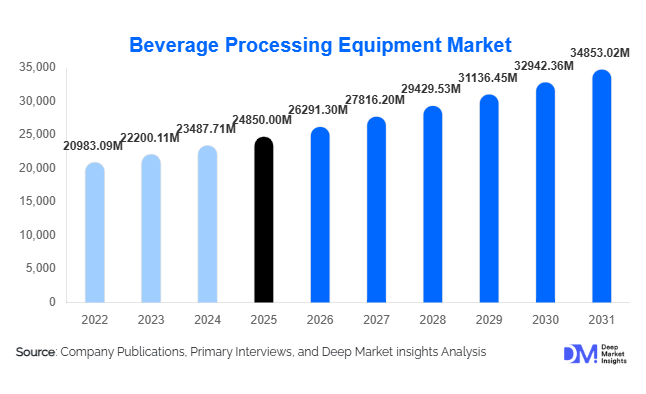

According to Deep Market Insights, the global beverage processing equipment market size was valued at USD 24,850 million in 2025 and is projected to grow from USD 26,291.30 million in 2026 to reach USD 34,853.02 million by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The beverage processing equipment market growth is primarily driven by rising global consumption of alcoholic and non-alcoholic beverages, rapid automation across food processing facilities, and increasing investments in energy-efficient and hygienic production technologies.

Key Market Insights

- Thermal processing equipment dominates the market, accounting for nearly 28% of 2025 revenue, driven by universal pasteurization and sterilization requirements.

- Non-alcoholic beverages represent over 62% of equipment demand, led by bottled water, functional drinks, and plant-based beverages.

- Asia-Pacific leads the global market with 34% share, supported by strong manufacturing expansion in China and India.

- Fully automatic systems account for approximately 54% of installations, reflecting rapid Industry 4.0 adoption.

- Stainless steel equipment holds over 82% share, due to hygiene compliance and corrosion resistance.

- The top five players control nearly 42% of the global market, indicating moderate consolidation with strong technological competition.

What are the latest trends in the beverage processing equipment market?

Smart & Industry 4.0-Integrated Processing Lines

Digital transformation is significantly reshaping beverage manufacturing facilities. Equipment manufacturers are embedding IoT-enabled sensors, AI-driven predictive maintenance tools, and cloud-based performance monitoring systems into processing lines. Smart homogenizers, pasteurizers, and CIP systems now provide real-time diagnostics, reducing downtime and operational inefficiencies. Large beverage corporations are prioritizing fully automated plants to optimize energy usage, water efficiency, and production yield. Digital twins and remote monitoring systems are also gaining traction, particularly in North America and Europe, where manufacturers seek operational transparency and compliance traceability.

Energy-Efficient and Sustainable Processing Technologies

Sustainability pressures are driving the adoption of heat recovery systems, water recycling modules, and energy-efficient evaporation technologies. Beverage manufacturers are investing in advanced thermal systems that reduce steam consumption and carbon emissions. Closed-loop water treatment and membrane filtration technologies are increasingly implemented to comply with tightening environmental regulations. As sustainability reporting becomes mandatory in several regions, equipment suppliers offering low-carbon solutions are gaining a competitive advantage.

What are the key drivers in the beverage processing equipment market?

Rising Global Packaged Beverage Consumption

Urbanization and rising disposable incomes are accelerating demand for bottled water, RTD beverages, and premium alcoholic drinks. The global non-alcoholic beverage industry alone exceeded USD 1.4 trillion in 2025, growing at 5–6% annually. This expansion directly fuels demand for processing upgrades, plant expansions, and new installations across emerging economies.

Stringent Food Safety & Hygiene Regulations

Global food safety standards such as FDA, EFSA, and HACCP compliance are compelling beverage manufacturers to invest in advanced pasteurization, filtration, and sterilization systems. Hygienic design certifications, including 3-A and EHEDG standards, are becoming procurement prerequisites. Regulatory compliance is particularly driving replacement demand in mature markets.

What are the restraints for the global market?

High Capital Investment Requirements

Beverage processing equipment requires substantial upfront capital expenditure, particularly for automated and turnkey processing lines. This limits adoption among small-scale producers in developing regions and lengthens purchasing cycles.

Volatility in Stainless Steel and Raw Material Prices

Stainless steel constitutes a significant portion of production costs. Price fluctuations directly affect equipment pricing and manufacturer margins, creating uncertainty in long-term contracts and procurement planning.

What are the key opportunities in the beverage processing equipment industry?

Expansion of Plant-Based and Functional Beverage Production

Plant-based milk, protein drinks, kombucha, and fortified beverages are expanding at an 8–10% CAGR globally. These categories require specialized homogenization, fermentation, and membrane filtration technologies. Equipment suppliers developing modular and flexible systems tailored to these applications can capture high-growth opportunities.

Emerging Market Manufacturing Expansion

Countries such as India, Vietnam, Indonesia, Nigeria, and Brazil are witnessing strong investments in domestic beverage production facilities. Government initiatives promoting food processing exports are accelerating plant installations. Localized assembly and cost-optimized systems offer significant growth avenues for global manufacturers entering these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 24850 Million |

| Market Size in 2026 | USD 26291.30 Million |

| Market Size in 2031 | USD 34853.02 Million |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Equipment Type Insights

Thermal processing equipment leads the market with approximately 28% share in 2025, driven by universal demand for pasteurizers and UHT systems across dairy, juice, and alcoholic beverages. Filtration and separation systems are growing rapidly due to increased demand for membrane technologies in water purification and plant-based beverage clarification. Fermentation systems are expanding in alcoholic beverages and kombucha production, while carbonation systems maintain steady demand in carbonated soft drink manufacturing.

Beverage Type Insights

Non-alcoholic beverages account for approximately 62% of total beverage processing equipment demand in 2025, making this the leading segment globally. The dominance of this segment is primarily driven by the high-volume production of bottled water, carbonated soft drinks, ready-to-drink (RTD) tea and coffee, juices, dairy beverages, and rapidly expanding functional drinks. Rising health consciousness, urbanization, and demand for convenient packaged hydration products are accelerating investments in advanced filtration, pasteurization, homogenization, and aseptic processing systems. Bottled water production alone continues to expand in Asia-Pacific, the Middle East, and Africa due to concerns over potable water quality, directly driving membrane filtration and water treatment equipment installations.

Alcoholic beverages account for approximately 38% of total equipment demand, led by beer, spirits, and wine production. Growth in this segment is supported by premiumization trends, craft brewery expansion in North America and Europe, and rising spirits consumption in the Asia-Pacific. Microbreweries and craft distilleries are particularly driving demand for small- to medium-scale fermentation systems, filtration equipment, and modular processing lines.

Automation Level Insights

Fully automatic systems dominate the beverage processing equipment market with nearly 54% share in 2025, driven by operational efficiency requirements, labor optimization, and increasing adoption of Industry 4.0 technologies. Large beverage manufacturers are investing heavily in automated processing lines integrated with PLC controls, SCADA systems, IoT sensors, and predictive maintenance platforms. Automation reduces downtime, improves batch consistency, enhances traceability, and ensures regulatory compliance, particularly in regions with stringent food safety requirements such as North America and Europe.

Smart integrated systems, which incorporate AI-enabled optimization and cloud-based performance monitoring, are the fastest-growing category, particularly in technologically advanced markets such as Germany, the United States, Japan, and South Korea. These systems allow remote diagnostics and energy monitoring, supporting sustainability goals. Semi-automatic systems remain relevant for small-scale producers, craft beverage companies, and emerging market installations where capital constraints limit full automation investments.

Capacity Insights

Large-scale high-volume plants contribute approximately 46% of total market revenue, making them the leading capacity segment globally. This dominance is primarily driven by multinational beverage corporations operating mega-production facilities to serve domestic and export markets. High-capacity plants require integrated thermal processing, large-scale blending systems, automated CIP units, and advanced process control technologies.

The key growth driver for this segment is the globalization of beverage brands and expansion into emerging markets. Companies such as global soft drink and bottled water manufacturers are continuously expanding production capacity in Asia-Pacific, Africa, and Latin America to meet rising consumption demand. Medium-scale plants are expanding rapidly in emerging economies such as India, Indonesia, Vietnam, and Brazil. These facilities cater to regional brands and private-label manufacturing. Meanwhile, small-scale systems are supported by growing craft breweries, specialty beverage startups, and local dairy beverage processors, particularly in North America and Europe.

End-Use Insights

Large beverage corporations account for nearly 48% of global equipment procurement, making them the dominant end-use segment. These corporations invest in plant modernization, energy-efficient retrofits, digital transformation initiatives, and capacity expansion projects. Their procurement strategies prioritize long-term service contracts, turnkey installations, and smart automation integration.

The primary driver for this segment’s leadership is continuous global expansion and portfolio diversification, including entry into plant-based, functional, and low-sugar beverage categories. Contract beverage manufacturers are increasingly investing in flexible and modular processing systems capable of handling multiple SKUs and private-label production runs. This flexibility is essential as beverage brands diversify product offerings. Craft breweries and micro-distilleries represent a growing niche segment, particularly in North America and Europe, where consumer preference for artisanal and locally produced beverages continues to rise. These end users drive demand for compact fermentation systems, filtration equipment, and customizable small-batch processing solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Beverage Processing Equipment Market Segmentations

By Equipment Type

- Preparation & Treatment Equipment

- Thermal Processing Equipment

- Filtration & Separation Equipment

- Carbonation Equipment

- Fermentation Equipment

- Homogenizers

- Cleaning Systems (CIP/SIP)

By Beverage Type

- Alcoholic Beverages

- Non-Alcoholic Beverages

- Plant-Based & Functional Beverages

By Automation Level

- Manual & Semi-Automatic Systems

- Fully Automatic Systems

- Smart/Industry 4.0 Integrated Systems

By Capacity

- Small-Scale Plants

- Medium-Scale Plants

- Large-Scale High-Volume Plants

By End-Use

- Large Beverage Corporations

- Contract Beverage Manufacturers

- Craft & Microbreweries

- Dairy & Functional Beverage Processors

Regional Insights

Asia-Pacific

Asia-Pacific leads the global beverage processing equipment market with approximately 34% share in 2025. China alone contributes nearly 18% of global demand, driven by large-scale beverage manufacturing, export-oriented production, and domestic consumption growth. Government support for food processing modernization and strong investments in automated manufacturing infrastructure are key regional drivers. India is the fastest-growing major market, registering a CAGR above 7%, supported by rising middle-class consumption, rapid urbanization, and initiatives promoting domestic food processing under national manufacturing programs. Southeast Asian countries such as Vietnam and Indonesia are also expanding beverage production capacity due to export growth and increasing foreign direct investment.

North America

North America accounts for approximately 27% of the global market share, with the United States contributing nearly 21%. Regional growth is driven by automation upgrades, replacement of aging infrastructure, strong craft brewery presence, and premium beverage innovation. Sustainability-driven retrofits, including water-saving and energy-efficient systems, are significant growth drivers. The U.S. market is characterized by high adoption of smart manufacturing technologies and strong investment in plant-based beverage production. Canada contributes a steady demand, particularly in dairy and alcoholic beverage processing.

Europe

Europe represents approximately 24% of global demand, led by Germany, Italy, and France. The region is a global hub for advanced beverage equipment manufacturing and technological innovation. Growth drivers include stringent environmental regulations, energy efficiency mandates, and strong export-oriented beverage production.v Germany leads in high-tech automated systems, while Italy is known for processing and bottling line engineering. Western European markets are heavily investing in carbon-neutral processing plants, supporting modernization demand.

Middle East & Africa

The Middle East & Africa account for approximately 8% of the global market share. Growth in this region is primarily driven by bottled water production in GCC countries, where limited freshwater resources necessitate advanced water treatment and desalination-linked processing systems. Saudi Arabia and the UAE are investing in domestic beverage manufacturing capacity to reduce import dependence. In Africa, South Africa leads demand in alcoholic beverage processing, while Nigeria and Kenya are witnessing growing installations of mid-scale beverage plants due to rising urban consumption.

Latin America

Latin America holds approximately 7% share of the global market, with Brazil and Mexico leading regional demand. Growth is supported by export-oriented beverage production, rising soft drink consumption, and the expansion of domestic beer and spirits manufacturing. Brazil remains the largest contributor due to its sizable beverage industry and modernization initiatives. Mexico benefits from strong integration with North American beverage supply chains, driving investments in automated and high-capacity processing systems.

Key Players in the Beverage Processing Equipment Market

- GEA Group

- Tetra Pak

- Krones AG

- Alfa Laval

- SPX FLOW

- Pentair

- Bucher Industries

- Sidel

- KHS Group

- JBT Corporation

- Pall Corporation

- Praj Industries

- IDMC Limited

- Feldmeier Equipment

- Tsingtao Brewery Equipment