Beverage Market Size

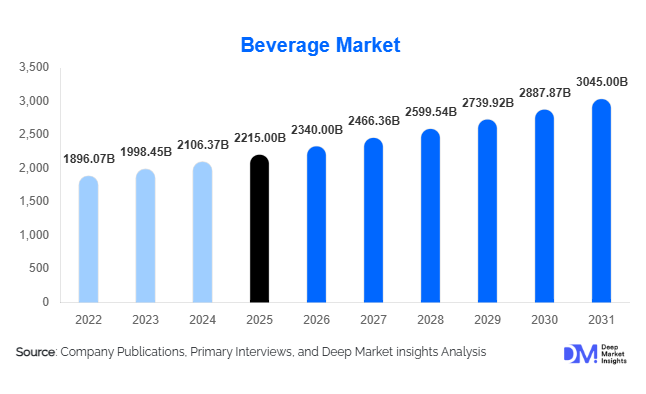

According to Deep Market Insights, the global beverage market size was valued at USD 2,215 billion in 2025 and is projected to grow from USD 2,340 billion in 2026 to reach approximately USD 3,045 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The global beverage market continues to demonstrate steady expansion driven by evolving consumer lifestyles, rising disposable incomes in emerging economies, premiumization trends, and rapid innovation across functional, health-oriented, and convenience beverage categories.

Changing consumption patterns are reshaping the beverage industry worldwide, with consumers increasingly shifting toward healthier, low-sugar, plant-based, and functional drink options. While traditional carbonated soft drinks maintain strong global volumes, faster growth is being observed in ready-to-drink (RTD) coffee, functional beverages, flavored water, dairy alternatives, and premium alcoholic beverages. Urbanization and on-the-go consumption habits are significantly influencing product innovation, packaging formats, and distribution models.

Digital retail expansion, cold-chain infrastructure development, and quick-commerce delivery platforms are enabling beverage brands to reach wider consumer bases. Emerging markets in Asia-Pacific, Latin America, and Africa are contributing substantial volume growth, while mature markets such as North America and Europe are driving value growth through premium and specialty beverages. Sustainability initiatives—including recyclable packaging, water stewardship, and carbon-neutral production—are also becoming central to corporate strategies, shaping long-term competitiveness in the global beverage ecosystem.

Key Market Insights

- Non-alcoholic beverages account for the largest global consumption share, supported by rising demand for hydration, energy, and functional wellness drinks.

- Functional and health-oriented beverages are the fastest-growing category globally, particularly probiotic, protein-enriched, and immunity-support drinks.

- Asia-Pacific dominates volume consumption, driven by population growth and expanding middle-class purchasing power.

- Premiumization trends are accelerating value growth across alcoholic beverages and specialty coffees.

- E-commerce and quick commerce are reshaping beverage distribution through instant delivery models.

- Sustainable packaging adoption is becoming a key competitive differentiator among global beverage manufacturers.

What are the latest trends in the beverage market?

Health and Functional Beverage Transformation

The beverage industry is undergoing a structural transformation toward health-focused consumption. Consumers increasingly prefer drinks that provide functional benefits such as energy enhancement, digestive health, immunity support, hydration optimization, and cognitive performance. Functional waters, kombucha, protein beverages, electrolyte drinks, and botanical-infused beverages are witnessing rapid adoption globally. Reduced sugar formulations and natural ingredient sourcing are becoming baseline expectations rather than niche offerings. Beverage manufacturers are investing heavily in R&D to develop formulations using adaptogens, probiotics, plant proteins, and natural sweeteners to align with wellness-driven purchasing behavior.

Premiumization and Craft Beverage Expansion

Premiumization has emerged as a major revenue driver across both alcoholic and non-alcoholic segments. Consumers increasingly value quality, origin transparency, artisanal production, and unique flavor experiences. Craft beer, specialty coffee, premium tea, single-origin juices, and small-batch spirits are gaining traction across developed markets. This trend allows brands to command higher margins while offsetting slower volume growth in mature categories. Premium packaging designs, limited-edition launches, and experiential branding strategies are strengthening consumer engagement and loyalty.

What are the key drivers in the beverage market?

Urbanization and On-the-Go Consumption

Rapid urbanization and busy lifestyles are driving demand for convenient beverage formats such as ready-to-drink coffees, packaged juices, energy drinks, and bottled water. Single-serve packaging and resealable containers cater to mobile consumers seeking instant refreshment. Growth of convenience stores and quick-service restaurants further supports impulse beverage purchases globally.

Expansion of Emerging Market Consumption

Rising disposable incomes across India, China, Indonesia, Brazil, and African economies are significantly increasing per-capita beverage consumption. Younger populations and expanding retail infrastructure are accelerating adoption of branded beverages, shifting demand away from unorganized local alternatives toward packaged and premium offerings.

Innovation in Product Formulation and Packaging

Technological advancements in processing, flavor science, and packaging materials enable longer shelf life, improved taste retention, and sustainable production. Smart packaging, recyclable bottles, and lightweight cans are improving logistics efficiency while meeting environmental goals.

What are the restraints for the global market?

Regulatory Pressure on Sugar and Alcohol Consumption

Governments worldwide are implementing sugar taxes, labeling regulations, and alcohol consumption controls to address public health concerns. These regulations increase compliance costs and force reformulation investments for manufacturers.

Volatility in Raw Material Prices

Fluctuations in agricultural commodities such as sugar, coffee beans, barley, fruits, and aluminum packaging materials impact production costs and pricing strategies. Climate change-related supply disruptions further increase uncertainty across beverage supply chains.

What are the key opportunities in the beverage industry?

Functional and Personalized Nutrition Beverages

The convergence of nutrition science and beverages presents significant opportunities for innovation. Personalized drinks tailored to hydration, fitness recovery, mental wellness, or metabolic health are gaining commercial viability. AI-driven nutrition insights and wearable integration may enable customized beverage formulations, creating new premium categories.

Expansion into Emerging Regional Markets

Untapped rural and semi-urban markets in Asia, Africa, and Latin America offer substantial growth potential. Improved cold-chain logistics and localized flavor development allow companies to penetrate new demographics. Affordable packaging formats such as sachets and smaller bottles are accelerating adoption.

Sustainable Packaging and Circular Economy Models

Investment in biodegradable materials, refillable systems, and closed-loop recycling provides differentiation and long-term cost benefits. Governments encouraging plastic reduction policies are creating favorable environments for sustainable beverage innovations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2215 Billion |

| Market Size in 2026 | USD 2340 Billion |

| Market Size in 2031 | USD 3045 Billion |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global beverage market continues to be primarily shaped by evolving consumer lifestyle patterns, increasing health awareness, and rapid product innovation across both alcoholic and non-alcoholic categories. Non-alcoholic beverages dominate the global beverage industry, accounting for approximately 68% of total market share in 2025. This dominance is largely attributed to the universal nature of daily hydration needs and the broad consumer base spanning all demographic and income groups. Bottled water remains the leading contributor within this segment, supported by rising concerns regarding water quality, increasing urbanization, and growing preference for convenient hydration solutions. Consumers are increasingly replacing sugary carbonated drinks with healthier alternatives such as mineral water, flavored water, plant-based beverages, and low-calorie ready-to-drink (RTD) products. The shift toward wellness-oriented consumption patterns has significantly strengthened demand across Asia-Pacific and Europe, where regulatory pressure on sugar reduction and consumer education campaigns continue to reshape purchasing behavior.Alcoholic beverages represent approximately 32% of the global beverage market, driven by premiumization trends and changing social consumption habits. Growth within this segment is increasingly value-driven rather than volume-driven. Premium spirits, craft beer, flavored alcoholic beverages, and ready-to-drink cocktails are gaining popularity among younger adult consumers seeking experiential and high-quality drinking options. Emerging markets are witnessing expanding alcohol consumption due to rising disposable incomes and urban social culture, while developed markets are focusing on premium and low-alcohol alternatives. The leading segment driver across product types remains the global consumer transition toward healthier, functional, and premium beverage experiences, encouraging manufacturers to diversify portfolios and invest heavily in innovation.

Category Insights

Among beverage categories, functional beverages represent the fastest-growing segment, accounting for nearly 18% share of the total beverage market in 2025. This growth reflects a structural shift from traditional refreshment-focused beverages toward purpose-driven consumption. Consumers increasingly expect beverages to deliver measurable health benefits such as improved energy levels, digestive health support, enhanced immunity, hydration optimization, and mental focus enhancement. Energy drinks continue to lead category expansion, particularly among young professionals, gamers, and fitness-oriented consumers seeking convenient performance solutions.The leading driver for this category is the convergence of nutrition and convenience. Modern consumers prefer functional beverages that integrate seamlessly into daily routines without requiring dietary supplements or complex preparation. Beverage companies are increasingly positioning products as lifestyle enhancers, combining taste, convenience, and scientifically supported benefits. This shift is further reinforced by digital marketing, influencer-driven wellness trends, and growing consumer access to nutritional information.

Packaging Type Insights

Packaging innovation remains a critical competitive factor within the global beverage market, influencing product preservation, branding, sustainability performance, and consumer convenience. Plastic bottles currently dominate packaging formats, accounting for nearly 44% market share, primarily due to their affordability, lightweight structure, durability, and suitability for mass distribution. PET bottles remain particularly important in bottled water and carbonated drink segments where large-scale production efficiency is essential.However, sustainability concerns and tightening environmental regulations are accelerating the transition toward alternative packaging solutions. Aluminum cans are rapidly gaining adoption globally, supported by their high recyclability rates, reduced environmental footprint, and strong association with premium beverage positioning. Beverage manufacturers are increasingly adopting cans for energy drinks, sparkling water, ready-to-drink coffee, and alcoholic beverages as consumers perceive them as environmentally responsible choices.The leading driver within packaging segmentation is sustainability-driven innovation. Governments, retailers, and consumers are collectively pushing beverage companies toward circular packaging models, recycled materials usage, and reduced plastic dependency, fundamentally reshaping long-term packaging strategies.

Distribution Channel Insights

Distribution dynamics within the beverage market are undergoing significant transformation as retail ecosystems evolve. Supermarkets and hypermarkets continue to dominate beverage distribution, accounting for approximately 39% of global beverage sales. These retail formats provide extensive product assortments, promotional pricing advantages, and bulk purchasing opportunities that attract both household and commercial buyers. Large-format retail stores remain particularly influential in emerging markets where organized retail penetration continues to expand.Online retail represents the fastest-growing distribution channel, expanding at double-digit growth rates globally. E-commerce platforms enable direct-to-consumer engagement, subscription-based beverage delivery models, and personalized product recommendations. The pandemic accelerated digital adoption, permanently altering consumer purchasing behavior. Beverage brands are increasingly investing in digital storefronts, quick-commerce partnerships, and last-mile delivery optimization to capture online demand.The leading driver for distribution channel growth is convenience-oriented consumption combined with digital retail transformation. Consumers increasingly prioritize accessibility, speed of delivery, and product discovery, encouraging omnichannel strategies that integrate physical retail with online platforms.

End-Use Insights

Household consumption dominates global beverage demand, representing nearly 72% of total market share. Beverages form an essential component of daily consumption patterns across all age groups, supporting consistent baseline demand regardless of economic fluctuations. Rising work-from-home culture and increasing at-home dining trends have further strengthened household beverage consumption across both developed and developing markets.The foodservice and hospitality sectors are experiencing strong recovery following pandemic-related disruptions. Restaurants, cafés, bars, and hotels are driving demand for premium beverages, specialty coffees, craft drinks, and alcoholic products. Beverage companies are collaborating with foodservice operators to develop exclusive menu offerings and customized formulations tailored to experiential dining environments.The leading driver in end-use segmentation is lifestyle diversification. Consumers now consume beverages across multiple occasions-hydration, socialization, wellness, convenience meals, and entertainment-expanding usage frequency and encouraging innovation across product categories.

End-Use Analysis

The foodservice industry represents one of the fastest-growing end-use sectors for beverages, expanding at an estimated annual growth rate of nearly 6.8%. The global expansion of café culture, increasing urban dining frequency, and rising penetration of quick-service restaurants significantly influence beverage innovation and consumption patterns. Coffee chains, bubble tea outlets, juice bars, and specialty beverage cafés are introducing new flavors and formats that later transition into retail markets.International trade continues to support global beverage expansion through export-driven demand for coffee, tea, wine, energy drinks, and functional beverages. Cross-border brand expansion enables companies to leverage global consumer trends while adapting formulations to regional taste preferences.Emerging applications are expanding beverage consumption into new environments such as workplace wellness programs, fitness centers, healthcare facilities, and educational institutions. Nutrition-focused beverages designed for recovery, hydration, or cognitive performance are gaining traction, illustrating how beverages are evolving beyond refreshment into functional lifestyle solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Beverage Market Segmentations

By Product Type

- Alcoholic Beverages

- Non-Alcoholic Beverages

- Hot Beverages

- Functional & Wellness Beverages

- Dairy & Plant-Based Beverages

By Packaging Type

- Bottled Packaging

- Canned Beverages

- Carton Packaging

- Fountain & Dispensed Formats

- Bulk Containers & Kegs

By Distribution Channel

- On-Trade

- Off-Trade Retail

- Online & Direct-to-Consumer

- Institutional & Foodservice Supply

By End Use

- Household Consumption

- Hospitality & Foodservice

- Corporate & Institutional Consumption

- Travel & Leisure

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 36% of the global beverage market share in 2025, making it the largest and fastest-evolving regional market. The region’s growth is primarily driven by large population bases, rising disposable incomes, rapid urbanization, and expanding middle-class consumer segments. China and India remain key demand centers, supported by increasing retail penetration and growing awareness of packaged beverage safety and quality standards.Regional growth is further driven by digital commerce expansion, strong local brand competition, and increasing investments by multinational beverage companies in localized product development. Climate conditions, rising temperatures, and expanding modern retail infrastructure also support sustained beverage consumption growth across the region.

North America

North America holds nearly 24% of global beverage market share, led predominantly by the United States. The region is characterized by high product innovation, premium pricing strategies, and strong consumer demand for health-oriented beverages. Functional drinks, plant-based beverages, and specialty coffee categories are key contributors to value growth.Regional growth drivers include premiumization trends, strong brand loyalty, advanced cold-chain logistics, and high consumer willingness to experiment with new beverage concepts. The wellness movement and fitness culture remain particularly influential in shaping long-term market expansion.

Europe

Europe represents a mature yet premium-driven beverage market led by Germany, the United Kingdom, France, and Italy. Although volume growth remains moderate compared to emerging regions, value growth is supported by premium beverages, organic products, and sustainable packaging innovations.Strict environmental regulations and circular economy initiatives are significantly influencing packaging transformation across the region. Consumers increasingly prioritize ethically sourced ingredients, low-carbon production processes, and recyclable packaging formats. Demand for non-alcoholic alternatives and low-alcohol beverages is also rising as lifestyle preferences shift toward moderation.Key regional growth drivers include sustainability-focused policies, strong café and specialty beverage culture, innovation in craft beverages, and increasing demand for natural and organic formulations. Europe’s emphasis on quality and authenticity continues to shape global beverage innovation trends.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential beverage market driven by demographic expansion, urbanization, and climate-related consumption patterns. Rising temperatures and water scarcity concerns significantly increase bottled water demand, making hydration products essential consumer staples.Countries such as the UAE and Saudi Arabia lead premium beverage consumption, supported by tourism growth, expanding hospitality sectors, and high disposable incomes. Meanwhile, African markets present long-term growth opportunities due to rapid population growth, improving retail infrastructure, and increasing penetration of affordable packaged beverages.Regional growth drivers include youthful population demographics, infrastructure development, expanding modern trade channels, and increasing foreign investment in beverage manufacturing facilities. Local flavor innovation and affordability strategies are key to market expansion across diverse income groups.

Latin America

Latin America remains a dynamic beverage market with Brazil and Mexico dominating regional demand. Carbonated soft drinks and beer continue to account for significant consumption volumes, supported by strong cultural integration of beverage consumption within social gatherings and foodservice environments.Functional beverages are emerging as a major growth category among younger consumers seeking healthier alternatives. Economic recovery trends and expanding urban middle-class populations are encouraging premium beverage adoption, particularly in energy drinks, flavored water, and ready-to-drink coffee segments.Key regional growth drivers include urbanization, rising retail modernization, expanding convenience store networks, and increasing consumer exposure to global beverage brands. Manufacturers are also investing in localized flavors and affordable packaging formats to improve accessibility and market penetration.

Key Players in the Beverage Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Nestlé S.A.

- Anheuser-Busch InBev

- Diageo plc

- Heineken N.V.

- Keurig Dr Pepper Inc.

- Red Bull GmbH

- DANONE S.A.

- Monster Beverage Corporation

- Asahi Group Holdings

- Kirin Holdings Company

- Pernod Ricard

- Constellation Brands

- Molson Coors Beverage Company