Global Beverage Flavors Market Size

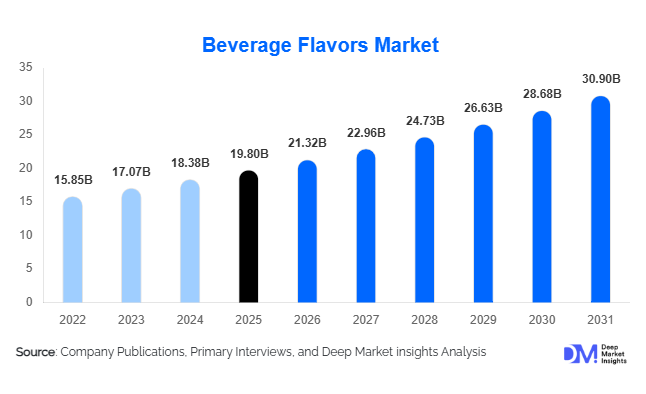

The global beverage flavors market size was valued at USD 19.8 billion in 2025 and is projected to grow from USD 21.32 billion in 2026 to reach USD 30.90 billion by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for functional and health-focused beverages, the rising preference for natural and clean-label flavors, and growing adoption of premium and alcoholic ready-to-drink beverages across the globe.

Key Market Insights

- Consumer preference is shifting toward natural and clean-label flavors, driving growth for flavor manufacturers offering plant-based, botanical, and sugar-reduction solutions.

- Functional and fortified beverages are expanding rapidly, increasing demand for flavors that mask bitter nutrients while delivering desirable taste profiles.

- North America holds a dominant share, led by the U.S. and Canada, due to innovation in RTD alcoholic beverages and flavored water products.

- Asia-Pacific is the fastest-growing region, fueled by rising urbanization, middle-class disposable income, and expanding packaged beverage consumption in China, India, and Southeast Asia.

- Europe continues to focus on premiumization and regulatory-compliant natural flavors, driving innovation in functional beverages, low-sugar formulations, and botanical infusions.

- Technological adoption, including flavor encapsulation, AI-assisted formulation, and shelf-life enhancement, is enabling beverage companies to launch complex flavors and meet regional taste preferences.

What are the latest trends in the beverage flavors market?

Clean-Label and Natural Flavor Innovation

Manufacturers are increasingly developing natural, plant-based, and clean-label flavor systems that meet consumer demand for transparency and health-conscious products. Flavors derived from fruits, herbs, botanicals, and spices are replacing synthetic counterparts, while maintaining shelf stability and sensory appeal. Sugar reduction, plant-based beverage masking, and immunity-boosting flavor blends are key trends, with flavor houses investing in advanced extraction, encapsulation, and stabilization technologies. Regulatory pressures in North America and Europe have accelerated this transition, making natural flavors a critical differentiator for competitive advantage.

Functional & Fortified Beverage Focus

Functional beverages such as energy drinks, vitamin-fortified waters, probiotic drinks, and adaptogenic formulations are driving innovative flavor applications. Consumers expect beverages to offer health benefits without compromising taste, which has increased demand for flavor systems capable of masking bitterness and enhancing palatability. Flavor manufacturers are collaborating closely with beverage brands to develop formulations tailored to regional preferences, nutritional requirements, and sensory expectations, further boosting R&D investments in functional beverage flavoring.

What are the key drivers in the beverage flavors market?

Rising Packaged Beverage Consumption

Urbanization, lifestyle changes, and higher disposable income are increasing global demand for ready-to-drink beverages, soft drinks, and functional beverages. Packaged beverage consumption directly drives demand for flavors, with fruit, botanical, and natural flavors being the most preferred. In 2025, carbonated soft drinks and flavored waters accounted for over 31% of global flavor consumption.

Premiumization and Alcoholic RTD Growth

The rise of premium alcoholic beverages and ready-to-drink cocktails has fueled demand for complex, layered flavors. Alcoholic beverages represent nearly 18% of global flavor demand, driven by consumer willingness to pay for high-quality taste experiences. Innovative flavor combinations, such as botanical and exotic fruit infusions, are increasingly adopted in premium segments.

Technological Advancements in Flavor Formulation

Advances in micro-encapsulation, AI-assisted flavor design, and shelf-life extension are enabling the creation of more stable, intense, and regionally tailored flavor systems. These innovations allow beverage manufacturers to experiment with novel flavor profiles and maintain taste consistency, even in challenging formulations such as sugar-reduced or plant-based beverages.

What are the restraints for the global market?

Raw Material Price Volatility

Natural flavor ingredients such as citrus oils, vanilla, and botanical extracts are subject to agricultural risks, climate variability, and geopolitical disruptions, causing supply volatility and price fluctuations. This impacts profitability and cost predictability for flavor manufacturers.

Regulatory Complexity

Diverse labeling and safety regulations across regions increase compliance costs and may delay product launches. Particularly in Europe and North America, adherence to strict EFSA and FDA standards for natural, artificial, and functional flavors is necessary, posing challenges for global distribution.

What are the key opportunities in the beverage flavors industry?

Functional Beverage Expansion

Functional beverages offer immense growth potential. Immunity-boosting, probiotic, and adaptogenic drinks require innovative flavor systems to mask unpleasant tastes. Companies offering customized solutions for health-oriented beverages are capturing premium contracts, as this segment is growing at over 9% CAGR globally.

Emerging Market Regional Customization

Asia-Pacific, Latin America, and Africa are experiencing rapid growth in packaged beverage consumption. Localized flavor development—incorporating tropical fruits, spices, and indigenous botanicals—is a major opportunity. Regional R&D centers and sourcing partnerships enable companies to capture this demand efficiently.

Natural and Clean-Label Innovation

Consumer preference for natural flavors, sugar-reduced beverages, and botanical infusions is driving research and product innovation. Flavor houses offering cost-effective, stable, and regulatory-compliant natural alternatives are gaining market share and expanding globally, supported by M&A and technology licensing opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 19.8 Billion |

| Market Size in 2026 | USD 21.32 Billion |

| Market Size in 2031 | USD 30.90 Billion |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fruit flavors are expected to dominate the market with a 38% share in 2025 due to their broad consumer appeal, versatility, and adaptability across carbonated beverages, juices, and ready-to-drink (RTD) beverages. Within the nature-based segment, natural flavors lead with a 52% share, driven by increasing consumer preference for clean-label and health-conscious products. Liquid flavors constitute 64% of total demand owing to their ease of formulation and integration into various beverage matrices. In terms of distribution, direct B2B supply accounts for 58% of the market, reflecting the prevalence of long-term contracts and strategic partnerships with beverage manufacturers. The growth of fruit and natural flavors is particularly fueled by innovation in functional and plant-based beverages, where flavor plays a crucial role in consumer acceptance.

Application Insights

Carbonated soft drinks remain the largest application segment, capturing a 31% share in 2025, while functional beverages and flavored waters are the fastest-growing applications due to rising health awareness and demand for functional benefits. Emerging niches such as alcoholic RTDs and plant-based beverages are driving the adoption of premium and botanical flavor systems, supporting innovation in flavor profiles. Additionally, export-oriented beverage manufacturing hubs in Mexico, Vietnam, and Poland are accelerating cross-border flavor trade, boosting demand for versatile and high-quality flavor solutions. The leading driver for applications is the growing consumer preference for functional and wellness-oriented beverages, which increases the demand for fruit, botanical, and natural flavors.

Distribution Channel Insights

The B2B supply channel dominates, primarily through direct contracts between flavor houses and beverage manufacturers. Contract flavor houses and private-label supply remain significant contributors, especially for mid-sized and regional beverage producers. The rise of online platforms and digital integration is enhancing efficiency in order management, particularly in emerging markets, making the procurement process more seamless. Key drivers for distribution include long-term partnerships, digital adoption, and increasing beverage production in high-growth regions.

Explore more data points, trends and opportunities Download Free Sample Report

Beverage Flavors Market Segmentations

By Flavor Type

- Fruit Flavors

- Brown Flavors

- Herbal & Botanical

- Floral Flavors

- Spice & Savory Flavors

By Nature

- Natural Beverage Flavors

- Nature-Identical Beverage Flavors

- Artificial Beverage Flavors

By Beverage Application

- Carbonated Soft Drinks

- Juices & Juice Concentrates

- Functional & Energy Drinks

- Alcoholic Beverages (Beer, Spirits, RTD Cocktails)

- Dairy-Based Beverages

By Form

- Liquid Beverage Flavors

- Powdered Beverage Flavors

- Encapsulated Flavor Systems

Distribution Channel

- Direct B2B Supply to Beverage Manufacturers

- Contract Flavor Houses

- Private Label Supply

Regional Insights

North America

North America represents 29% of the global market, with the U.S. and Canada leading the demand for functional beverages, RTD alcoholic drinks, and premium beverages. Growth is driven by high disposable incomes, early adoption of innovative flavors, and strong demand for natural and clean-label products. Additionally, health-conscious consumer trends and regulatory support for natural ingredients further accelerate the uptake of fruit, botanical, and natural flavors.

Europe

Europe accounts for 22% of the market, led by Germany, France, and the U.K. Consumer preference for clean-label, premium, and functional beverages drives flavor innovation. Regulatory frameworks emphasizing transparency and natural ingredients encourage the adoption of natural and nature-based flavors. Regional growth is further supported by mature retail infrastructure, a high number of beverage manufacturers investing in product differentiation, and increasing cross-border trade within the EU.

Asia-Pacific

Asia-Pacific is the fastest-growing region, capturing 34% of global market share. Rapid urbanization, rising middle-class incomes, and increasing packaged beverage consumption in China, India, and Southeast Asia drive demand. Tropical, spice, and botanical flavors are particularly popular due to cultural preferences and local flavor innovations. Growth drivers include expanding beverage manufacturing infrastructure, increasing youth-oriented consumption, and the proliferation of RTD and functional beverage segments.

Latin America

Latin America accounts for 9% of the market, with Brazil and Mexico being key contributors. Young, urban consumers and rising disposable income are fueling demand for fruit-based and innovative beverage flavors. The growth is also supported by expanding retail channels, increasing beverage exports, and a growing interest in flavored waters, energy drinks, and RTD beverages.

Middle East & Africa

Middle East & Africa represent 6% of the global market. High-income consumers in the UAE, Saudi Arabia, and Qatar drive demand for premium beverage flavors, while Africa continues to serve as a key production hub for natural flavor ingredients. Growth drivers include rising urbanization, increased beverage imports, and the expansion of functional and RTD beverage categories in Gulf countries. The region is also witnessing rising adoption of exotic and botanical flavors, catering to evolving premium and health-conscious consumer preferences.

Key Players in the Beverage Flavors Market

- Givaudan

- Firmenich

- IFF

- Symrise

- Kerry Group

- Takasago

- Sensient Technologies

- Mane

- Robertet

- T. Hasegawa

- Flavorchem

- Keva Flavours

- Huabao International

- Synergy Flavors

- Bell Flavors & Fragrances