Beta Glucan Supplement Market Size

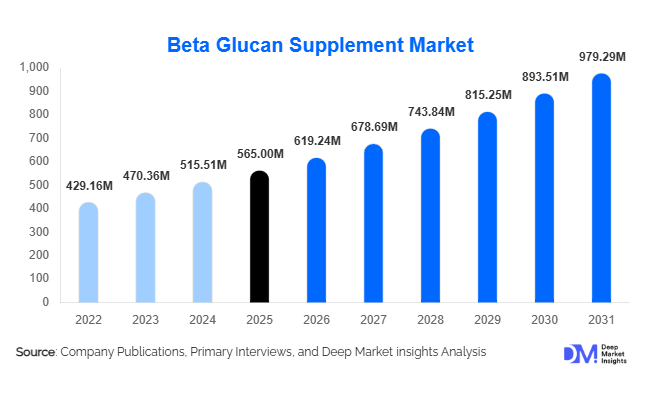

According to Deep Market Insights,the global beta glucan supplement market size was valued at USD 565 million in 2025 and is projected to grow from USD 619.24 million in 2026 to reach USD 979.29 million by 2031, expanding at a CAGR of 9.6% during the forecast period (2026–2031). The market growth is primarily driven by rising global awareness of preventive healthcare, increasing demand for immune-support nutraceuticals, and expanding applications of beta glucan in cardiovascular and metabolic health management. Strong scientific backing for cholesterol reduction and immune modulation, particularly for oat- and yeast-derived beta glucan, continues to strengthen product adoption across developed and emerging markets.

Key Market Insights

- Immune health applications dominate the market, accounting for nearly 45% of total demand in 2025, supported by sustained post-pandemic consumer focus on immunity.

- Yeast-derived beta glucan leads by source, contributing approximately 38% of global revenue due to high purity levels and clinical-grade positioning.

- Capsules and tablets remain the preferred dosage form, holding over 40% market share owing to dosage precision and consumer familiarity.

- North America dominates global revenue, representing around 34% of the 2025 market, driven by high supplement penetration rates.

- Asia-Pacific is the fastest-growing region, projected to expand at over 11% CAGR through 2031 due to rising nutraceutical adoption in China and India.

- Premium, high-purity (>60%) beta glucan formulations are witnessing strong demand, reflecting increasing medical and practitioner-driven applications.

What are the latest trends in the beta glucan supplement market?

Shift Toward High-Purity and Clinical-Grade Formulations

Manufacturers are increasingly focusing on high-concentration beta glucan extracts exceeding 60% purity to cater to clinical nutrition and practitioner channels. This trend is supported by growing scientific studies validating immune modulation and cholesterol reduction properties. Pharmaceutical-grade fermentation and advanced extraction technologies are being adopted to ensure consistency, bioavailability, and regulatory compliance. Clinical trials and substantiated health claims are becoming strategic differentiators, enabling brands to command premium pricing and expand into medical nutrition segments.

Expansion of Multi-Functional Supplement Blends

Beta glucan is increasingly incorporated into combination formulations with vitamin D, zinc, probiotics, collagen, and omega-3 fatty acids. Consumers prefer comprehensive wellness products that address immunity, gut health, cardiovascular health, and metabolic balance simultaneously. Gummies, effervescent powders, and ready-to-drink formats are emerging as convenient delivery systems, especially among younger consumers. Direct-to-consumer subscription models and digital wellness ecosystems are further reinforcing repeat purchase behavior.

What are the key drivers in the beta glucan supplement market?

Rising Preventive Healthcare Awareness

Consumers globally are prioritizing daily supplementation to prevent chronic illnesses rather than relying solely on reactive treatment. Beta glucan’s role in immune support and heart health aligns directly with preventive health trends. Increasing lifestyle diseases and aging populations are strengthening sustained demand, particularly in North America and Europe.

Growing Cardiovascular and Metabolic Health Concerns

Cardiovascular diseases remain a leading global health burden. Regulatory support for cholesterol-lowering claims associated with oat beta glucan has significantly improved product credibility. Rising cases of hyperlipidemia and type-2 diabetes are driving demand for fiber-based nutraceuticals with clinically supported outcomes.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in oat, barley, yeast, and specialty mushroom cultivation impact input costs and margin stability. Climatic variations and agricultural yield constraints contribute to pricing inconsistencies, affecting smaller manufacturers disproportionately.

Regulatory Variability Across Regions

Health claim approvals and supplement regulations differ significantly across North America, Europe, and Asia-Pacific. Compliance costs, labeling requirements, and clinical substantiation demands create barriers for new entrants and smaller companies.

What are the key opportunities in the beta glucan supplement industry?

Expansion in Emerging Asia-Pacific Markets

Countries such as China and India are witnessing rapid nutraceutical adoption supported by expanding middle-class income and digital retail infrastructure. Localization strategies, halal-certified products, and region-specific marketing campaigns offer strong revenue potential for global manufacturers.

Integration into Clinical and Practitioner Channels

Growing acceptance of nutraceuticals within integrative medicine is opening new practitioner-driven distribution avenues. Hospitals, nutritionists, and wellness clinics are increasingly recommending beta glucan supplements for immune-compromised and geriatric populations, strengthening premium market segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 565 Million |

| Market Size in 2026 | USD 619.24 Million |

| Market Size in 2031 | USD 979.29 Million |

| CAGR | 9.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Yeast-derived beta glucan dominates the global market, accounting for nearly 38% of total revenue in 2025. The segment’s leadership is primarily driven by its superior bioactivity, high purity levels, and strong clinical validation supporting immune modulation benefits. Yeast beta glucan demonstrates consistent molecular structure and standardized extraction processes, making it highly suitable for immune-focused formulations, clinical nutrition products, and pharmaceutical-grade applications. Increasing demand for scientifically substantiated ingredients in post-pandemic preventive healthcare has further accelerated its adoption across nutraceutical and functional food manufacturers. Oat-derived beta glucan represents the second-largest source segment, supported by well-established cholesterol-lowering health claims and regulatory approvals in multiple developed markets. Its integration into heart-health functional foods, breakfast cereals, and dietary supplements strengthens its commercial viability. Meanwhile, mushroom-derived beta glucan is witnessing expanding penetration in specialty wellness, beauty-from-within supplements, and premium immune blends, benefiting from consumer preference for plant-based and adaptogenic ingredients.

Form Insights

Capsules and tablets account for approximately 42% of the global market share in 2025, making them the leading form segment. The primary driver of this dominance is dosage precision and consumer trust in standardized supplement formats, particularly within pharmacy and practitioner-recommended channels. These formats offer longer shelf life, convenient storage, and easier regulatory compliance, which enhances manufacturer preference. Powder formulations hold a significant share due to their flexibility in bulk nutraceutical blending, sports nutrition mixes, and functional beverage fortification. Their adaptability for customized dosing and combination formulas supports growth among contract manufacturers and private-label brands. Gummies and liquid formats are expanding at a rapid pace, especially among younger consumers seeking convenience, improved taste profiles, and lifestyle-oriented supplementation. Innovation in flavor masking and sugar-free formulations continues to accelerate growth within these emerging formats.

Application Insights

Immune health applications lead the global beta glucan market, capturing nearly 45% of total revenue in 2025. The leading driver for this segment is sustained consumer focus on immune resilience following global health crises, alongside growing awareness of preventative healthcare strategies. Clinical evidence supporting beta glucan’s ability to activate macrophages and enhance innate immune response reinforces its integration into daily wellness regimens. Cardiovascular and cholesterol management represents the second-largest application area, supported by extensive scientific validation of beta glucan’s role in reducing LDL cholesterol levels. Rising global incidence of cardiovascular diseases, combined with aging populations and increasing lifestyle-related risk factors, continues to strengthen demand within this segment. Additional applications, including metabolic health, gut health, and sports immunity support, are steadily gaining traction as research expands the functional scope of beta glucan.

Distribution Channel Insights

Online retail and direct-to-consumer platforms account for approximately 34% of total global sales in 2025, positioning digital commerce as the fastest-growing distribution channel. The primary growth driver is expanding consumer preference for convenience, subscription-based supplement models, and access to product transparency through digital reviews and ingredient traceability. E-commerce platforms enable global brand reach, targeted marketing strategies, and personalized health recommendations, significantly accelerating product penetration. Pharmacies and specialty health stores remain essential distribution channels, particularly for clinically positioned and practitioner-endorsed formulations. These channels benefit from consumer trust, pharmacist recommendations, and strong offline retail infrastructure in developed markets. Supermarkets and hypermarkets also contribute to volume sales through functional food integration and mass-market supplement offerings.

End-Use Insights

The adult general wellness segment holds nearly 48% of total global demand in 2025, driven primarily by routine daily supplementation and rising preventive health awareness among working-age populations. Increasing disposable income, expanding fitness culture, and broader access to nutraceutical education continue to reinforce demand within this demographic. The geriatric population represents the fastest-growing end-use segment, projected to expand at a CAGR exceeding 10% during the forecast period. Growth in this segment is driven by age-related immune decline, higher cardiovascular risk prevalence, and increasing demand for non-pharmaceutical health management solutions. Pediatric applications are gradually expanding as well, particularly in chewable and syrup formulations designed to support immunity in children.

Explore more data points, trends and opportunities Download Free Sample Report

Beta Glucan Supplement Market Segmentations

By Source

- Oat-Derived Beta Glucan

- Barley-Derived Beta Glucan

- Yeast-Derived Beta Glucan

- Mushroom-Derived Beta Glucan

- Algae & Seaweed-Derived Beta Glucan

By Form

- Capsules & Tablets

- Powder

- Gummies & Chewables

- Liquid & Syrup

- Softgels

By Application

- Immune Health

- Cardiovascular & Cholesterol Management

- Digestive & Gut Health

- Blood Sugar Management

- Sports Nutrition & Recovery

- Skin & Beauty Supplements

By Distribution Channel

- Online Retail & Direct-to-Consumer

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Practitioner & Clinical Channels

By End-Use

- Adult General Wellness

- Geriatric Population

- Pediatric Supplements

- Athletes & Fitness Consumers

- Clinical & Medical Nutrition

Regional Insights

North America

North America accounts for approximately 34% of the global market in 2025, with the United States contributing nearly 78% of regional demand. Regional growth is primarily driven by high dietary supplement penetration rates, advanced retail infrastructure, and strong consumer awareness regarding preventive healthcare. Widespread clinical research, established regulatory frameworks supporting functional claims, and high healthcare expenditure further strengthen market expansion. The integration of beta glucan into functional foods and immune-support beverages enhances product diversification across retail shelves. Canada supports steady growth through increasing functional food adoption and government-supported heart health initiatives promoting cholesterol-lowering dietary fibers.

Europe

Europe holds nearly 29% of the global market share in 2025, led by Germany, the United Kingdom, and France. A key driver of regional growth is regulatory backing for cholesterol reduction claims associated with oat beta glucan, which supports widespread incorporation into cereals, bakery products, and heart-health supplements. Germany represents the largest European consumer and importer, benefiting from strong nutraceutical manufacturing capabilities and high consumer health consciousness. The United Kingdom and Nordic countries contribute significantly due to rising aging populations and established functional food markets. Increasing demand for clean-label, plant-based ingredients further supports beta glucan expansion across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, projected to expand at a CAGR exceeding 11% over the forecast period. Growth is driven by rising disposable incomes, rapid urbanization, and increasing consumer awareness of immune and cardiovascular health. China and Japan lead regional demand through strong functional food traditions and integration of beta glucan into fortified beverages and nutritional products. Japan’s aging population significantly contributes to immune and heart-health supplement consumption. India is emerging as a high-growth nutraceutical market, supported by expanding e-commerce penetration, growing middle-class income, and rising urban wellness awareness. Local manufacturing expansion and government initiatives promoting preventive healthcare further stimulate regional market development.

Latin America

Latin America demonstrates steady growth, with Brazil and Mexico leading regional demand. Market expansion is driven by urban middle-class population growth, improving retail accessibility, and increasing adoption of dietary supplements. Rising healthcare awareness and growing prevalence of lifestyle-related diseases encourage consumers to seek preventive nutritional solutions. Expansion of international supplement brands into the region further strengthens product availability and category awareness.

Middle East & Africa

The Middle East & Africa region is experiencing gradual market expansion, supported by rising health consciousness and increasing disposable income in key economies. Saudi Arabia and the United Arab Emirates represent high-income consumer bases with strong demand for imported premium supplements. Expanding pharmacy chains and modern retail infrastructure enhance accessibility to nutraceutical products. South Africa anchors sub-Saharan African consumption, driven by growing urbanization and increasing awareness of immune-support supplementation. Government healthcare diversification strategies and expanding private healthcare investments further support long-term regional growth potential.

Key Players in the Beta Glucan Supplement Market

- Koninklijke DSM N.V.

- Kerry Group plc

- Tate & Lyle PLC

- Lesaffre Group

- Lallemand Inc.

- Cargill Incorporated

- Archer Daniels Midland Company

- Garuda International Inc.

- Biotec Pharmacon ASA

- Kemin Industries Inc.

- Ceapro Inc.

- Naturex SA

- GlycaNova AS

- Super Beta Glucan Inc.

- Nutraceutical International Corporation