Global Belgian Beer Market Size

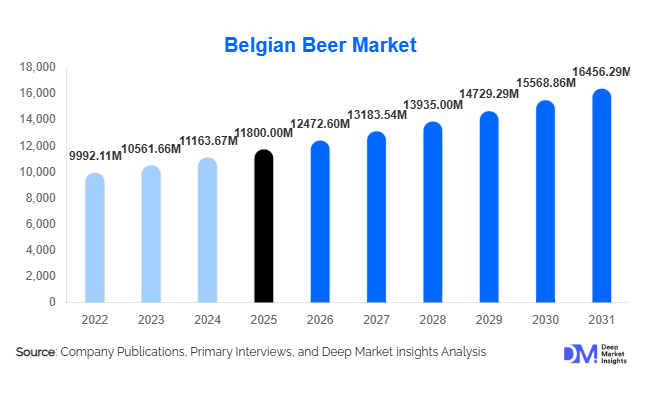

According to Deep Market Insights, the global Belgian beer market size was valued at USD 11,800 million in 2025 and is projected to grow from USD 12,472.60 million in 2026 to reach USD 16,456.29 million by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The Belgian beer market growth is primarily driven by rising global demand for premium and craft beer, increasing consumer preference for heritage-based alcoholic beverages, and expanding international distribution networks supported by hospitality and e-commerce channels.

Key Market Insights

- Premiumization is reshaping global beer consumption, with Belgian beers gaining strong traction in high-income consumer segments seeking authentic and craft-style beverages.

- Trappist and Abbey beers continue to dominate value share, supported by limited production, heritage branding, and strong export demand.

- Europe remains the largest consumption hub, driven by deep-rooted beer culture in Belgium, Germany, France, and the UK.

- Asia-Pacific is emerging as the fastest-growing region, led by rising disposable incomes and increasing demand for imported premium alcoholic beverages.

- E-commerce and direct-to-consumer alcohol platforms are expanding rapidly, enabling broader global access to niche Belgian beer brands.

- Sustainability and low-alcohol innovations are reshaping product portfolios, especially in response to health-conscious consumers in developed markets.

Belgian Beer Market Latest Trends

Premium Craft and Heritage Beer Expansion

Belgian beer brands are increasingly capitalizing on global craft beer culture by emphasizing authenticity, traditional brewing methods, and regional heritage. Consumers are shifting toward complex flavor profiles such as Trappist ales, Lambic beers, and Abbey styles, which are positioned as premium alternatives to mass-market lagers. Breweries are investing in storytelling-driven branding, highlighting centuries-old brewing traditions to differentiate their offerings in highly competitive global beer markets. This trend is particularly strong in North America and Western Europe, where craft beer enthusiasts prioritize uniqueness and origin authenticity over price sensitivity.

Growth of Non-Alcoholic and Low-Alcohol Belgian Beers

Health-conscious consumption patterns are driving strong demand for low-alcohol and alcohol-free Belgian beer variants. Brewers are innovating fermentation techniques to maintain traditional Belgian flavor complexity while reducing alcohol content. This segment is rapidly expanding in Europe and the Middle East, where regulatory and lifestyle shifts are encouraging moderation in alcohol consumption. These products are increasingly positioned as premium wellness-oriented beverages, enabling Belgian breweries to tap into new consumer segments without diluting brand heritage.

Belgian Beer Market Drivers

Rising Global Demand for Premium Alcoholic Beverages

The global shift toward premiumization is one of the strongest drivers of the Belgian beer market. Consumers are increasingly willing to pay higher prices for high-quality, artisanal, and authentic beer experiences. Belgian beers, known for their complexity and heritage, benefit significantly from this trend. Growth in high-net-worth populations across Asia-Pacific and the Middle East is further accelerating demand for premium imported beer brands.

Expansion of Global Distribution and Export Channels

Improved logistics infrastructure, international trade agreements, and the expansion of multinational brewing companies have significantly enhanced global access to Belgian beers. Export markets such as the United States, China, and the United Kingdom are experiencing strong import growth. E-commerce alcohol delivery platforms are also enabling direct access to niche Belgian brands, expanding consumer reach beyond traditional retail networks.

Rising Craft Beer Culture and Flavor Innovation

The global craft beer movement has created strong demand for unique and experimental beer styles, directly benefiting Belgian breweries. Innovations such as fruit-infused beers, barrel-aged variants, and hybrid brewing techniques are attracting younger demographics. This trend is expanding consumption beyond traditional beer drinkers and supporting sustained category diversification.

Global Market Restraints

Strict Alcohol Regulations and Taxation Policies

High taxation on alcoholic beverages and strict regulatory frameworks in several countries act as a significant barrier to market expansion. Compliance costs, advertising restrictions, and import duties reduce pricing flexibility and limit accessibility in price-sensitive markets. These constraints are particularly strong in parts of Asia and the Middle East.

Rising Competition from Local Craft Breweries

The rapid growth of domestic craft breweries across global markets is intensifying competition for Belgian beer producers. Local breweries often offer similar craft-style experiences at lower prices with stronger regional appeal. This is creating pricing pressure and challenging import penetration in emerging economies.

Belgian Beer Industry Key Opportunities

Expansion in Emerging Markets

Emerging economies such as India, China, Vietnam, and Brazil present significant growth opportunities due to rising disposable incomes and increasing demand for premium imported alcoholic beverages. Belgian breweries can leverage partnerships with local distributors and hospitality chains to strengthen market penetration and brand visibility in these high-growth regions.

Alcohol-Free and Wellness-Oriented Product Development

The growing wellness trend presents a major opportunity for Belgian breweries to expand into non-alcoholic and low-alcohol beer categories. These products align with shifting consumer lifestyles focused on health and moderation while maintaining traditional Belgian flavor complexity, enabling broader demographic reach.

E-commerce and Direct-to-Consumer Expansion

The rapid growth of online alcohol delivery platforms offers Belgian beer producers new channels for global expansion. Subscription-based beer clubs, online-exclusive releases, and digital marketing strategies are enabling stronger consumer engagement and brand loyalty, especially among urban and younger consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11800.00 Million |

| Market Size in 2026 | USD 12472.60 Million |

| Market Size in 2031 | USD 16456.29 Million |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Belgian Strong Ales continue to dominate the premium beer category, contributing approximately 22% of the global market. Their leadership is primarily driven by strong export demand, high alcohol content, and deeply rooted heritage branding associated with traditional Belgian brewing craftsmanship. Premiumization trends across developed markets and increasing consumer willingness to pay for complex flavor profiles further reinforce the growth of this segment. Witbier and Pilsner-style beers are witnessing strong adoption in mass-market consumption due to their lighter taste profiles, refreshing character, and broad demographic appeal, making them highly suitable for large-scale commercial distribution and mainstream retail penetration. Abbey and Trappist beers retain a strong premium positioning, supported by limited production capacity, authenticity, and monastery-linked exclusivity, which collectively enhance their perceived value and drive consistent demand among connoisseurs. Fruit beers and Lambic variants are emerging as high-growth niche categories, propelled by experimentation trends, younger consumer preferences for innovative flavor profiles, and increasing craft beer culture globally. Overall, the product landscape reflects a dual structure where heritage-driven premium ales dominate value generation, while lighter beer styles drive volume expansion through accessibility and affordability.

Packaging Insights

Glass bottles remain the dominant packaging format with an estimated 58% market share, primarily driven by their association with premium positioning, superior flavor preservation, and strong alignment with traditional Belgian beer branding. The continued dominance of glass is further supported by consumer perception of authenticity and quality retention in high-end beer categories. Cans are experiencing rapid adoption in the mainstream segment due to their portability, lower transportation cost, recyclability advantages, and suitability for outdoor and on-the-go consumption occasions, making them a key growth driver in urban retail environments. Kegs and draft formats continue to dominate on-trade consumption, particularly in bars, pubs, hotels, and restaurants, where freshness, serving efficiency, and high-volume dispensing are critical. Bulk export barrels remain essential for international distribution networks, enabling efficient cross-border trade and supporting large-scale institutional buyers. Across all packaging formats, sustainability initiatives and lightweight material innovation are becoming central growth enablers, driven by regulatory pressure and increasing consumer demand for environmentally responsible packaging solutions.

Distribution Channel Insights

Off-trade channels, including supermarkets, hypermarkets, and liquor retail stores, account for the largest share of global Belgian beer consumption, primarily driven by retail network expansion, rising household consumption, and increasing product availability across mainstream retail shelves. Growth in this segment is further supported by promotional pricing strategies and wider SKU diversification. On-trade channels remain highly significant, particularly in Europe’s hospitality-driven consumption culture, where experiential drinking, brand engagement, and social consumption in bars and restaurants sustain steady demand for premium and specialty beer variants. Online alcohol platforms represent the fastest-growing distribution channel, fueled by digital convenience, doorstep delivery models, subscription-based beer clubs, and improved access to premium imported products, particularly in urban markets. Duty-free and travel retail channels also contribute meaningfully to high-margin sales, driven by international tourism, airport retail expansion, and strong demand for premium gifting products among global travelers.

End-Use Insights

The hospitality sector remains the largest end-use segment, supported by sustained demand from bars, restaurants, hotels, and tourism-driven establishments where experiential consumption and premium beverage offerings are central to customer engagement strategies. Growth in this segment is strongly influenced by the revival of global tourism, expansion of premium dining experiences, and increasing incorporation of Belgian beers into curated beverage menus. Retail consumption continues to expand steadily, driven by rising household purchasing power, increased availability through organized retail formats, and growing consumer preference for at-home premium drinking experiences. Export-driven wholesale distribution plays a crucial role in global revenue generation, with Belgium maintaining its position as a leading production and export hub, supported by strong international brand recognition and established trade networks. Additionally, the increasing integration of Belgian beer into gourmet dining, food pairing experiences, and fine-dining restaurants is significantly enhancing its premium positioning and reinforcing demand across high-end culinary environments worldwide.

Explore more data points, trends and opportunities Download Free Sample Report

Belgian Beer Market Segmentations

By Product Type

- Trappist Beer

- Abbey Beer

- Witbier

- Saison Beer

- Lambic & Gueuze

- Belgian Strong Ale

- Pilsner-Style Belgian Beer

- Fruit Beer

By Packaging Type

- Glass Bottles

- Cans

- Kegs / Draft Beer

- Bulk Export Barrels

By Alcohol Content

- Low Alcohol

- Medium Alcohol

- High Alcohol

By Distribution Channel

- On-Trade

- Off-Trade

- Online Retail / E-commerce Alcohol Platforms

- Duty-Free & Travel Retail

Regional Insights

Europe

Europe dominates the global Belgian beer market with approximately 41% share in 2025, supported by strong cultural integration of beer consumption, proximity to major production hubs, and high acceptance of premium alcoholic beverages. Demand growth in this region is driven by deep-rooted brewing traditions, strong tourism inflows to Belgium and neighboring countries, and widespread presence of beer-centric hospitality establishments. Increasing consumer preference for craft and specialty beers, along with premiumization of alcoholic beverages, further strengthens regional dominance. Additionally, regulatory support for artisanal brewing and the presence of established distribution networks contribute significantly to sustained market expansion.

North America

North America accounts for approximately 27% of the global market, led primarily by the United States, which remains one of the largest importers of Belgian beer globally. Growth in this region is driven by a strong craft beer culture, rising demand for imported premium beverages, and increasing consumer sophistication in taste preferences. The expansion of specialty liquor stores and premium retail chains has improved product accessibility, while growing interest in Trappist and Abbey beers reflects rising appreciation for authentic and heritage-driven brewing styles. Additionally, strong marketing by import distributors and the integration of Belgian beers into gourmet dining further support regional demand expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by rising disposable incomes, rapid urbanization, and increasing adoption of Western lifestyle and consumption habits. Key markets such as China, India, Japan, and Australia are witnessing strong growth in demand for imported premium alcoholic beverages, particularly in urban centers. Expansion of e-commerce alcohol platforms, digital payment systems, and improved cold-chain logistics has significantly enhanced product accessibility across the region. Furthermore, growing exposure to international food and beverage culture, along with the rising popularity of premium hospitality outlets, is accelerating consumption of Belgian beer varieties across both retail and on-trade channels.

Latin America

Latin America, led by Brazil, Mexico, and Argentina, is emerging as a promising growth region for Belgian beer consumption. Market expansion is primarily driven by rapid urbanization, increasing middle-class income levels, and growing exposure to global beer and premium beverage culture. The expansion of modern retail infrastructure and rising penetration of imported alcoholic beverages are further supporting demand. Additionally, the growing hospitality and tourism sector, particularly in urban and coastal cities, is enhancing consumption opportunities for premium beer offerings. Increasing consumer interest in international brands and experiential drinking culture is expected to sustain long-term regional growth.

Middle East & Africa

Middle East & Africa presents a dual growth structure, where the Middle East, particularly the UAE and other hospitality-driven economies, is witnessing rising demand for premium alcoholic beverages supported by tourism, luxury hospitality, and expatriate populations. Growth in this sub-region is driven by expanding high-end hotels, international restaurants, and duty-free retail environments. In Africa, markets such as South Africa and Kenya are contributing to both production and consumption, supported by expanding urban populations, improving retail infrastructure, and gradual acceptance of premium beer products. Overall, regional growth is further supported by tourism expansion, urban lifestyle shifts, and increasing integration of international beverage brands into hospitality sectors.

Key Players in the Belgian Beer Market

- Anheuser-Busch InBev

- Heineken N.V.

- Duvel Moortgat

- Carlsberg Group

- Molson Coors Beverage Company

- Chimay Brewery

- Rochefort Brewery

- Westmalle Brewery

- Orval Brewery

- Lindemans Brewery

- Brouwerij Boon

- Brasserie Dupont

- La Trappe (Koningshoeven)