Beer Processing Market Size

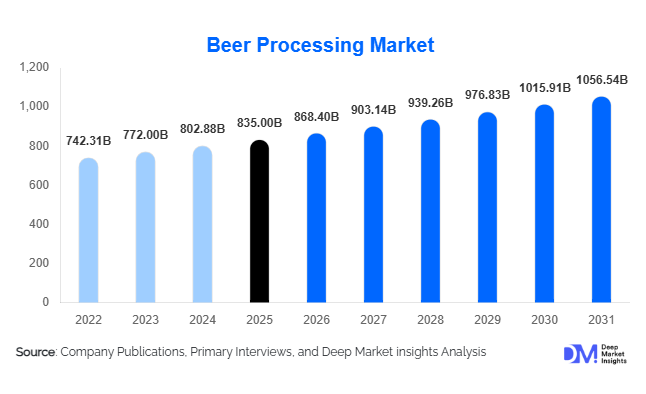

According to Deep Market Insights, the global beer processing market size was valued at USD 835 billion in 2025 and is projected to grow from USD 868.40 billion in 2026 to reach USD 1,056.54 billion by 2031, expanding at a CAGR of 4.0% during the forecast period (2026–2031). The beer processing market growth is primarily driven by rising demand for craft and specialty beers, increased automation adoption across breweries, and expanding beer consumption in emerging markets such as Asia Pacific and Africa. Additionally, non-alcoholic beer trends and premiumization strategies are reshaping process technology investments globally.

Key Market Insights

- Automation and smart brewery solutions are transforming production efficiency, enabling breweries to maintain quality, reduce labor costs, and optimize yield across brewing, fermentation, and packaging stages.

- Craft and specialty beer segments are expanding rapidly, driving investments in modular, flexible processing equipment capable of small-batch, high-variety production.

- Asia Pacific is the fastest-growing region, with China and India leading demand for advanced beer processing capacity due to urbanization, rising disposable incomes, and increasing beer penetration.

- North America and Europe remain mature markets, characterized by high automation adoption, strong craft beer demand, and established export-driven production.

- Health-conscious and non-alcoholic beer trends are creating opportunities for specialized fermentation control and low-alcohol processing techniques.

- Sustainability initiatives, including energy-efficient heat exchangers, water recycling systems, and carbon footprint reduction, are increasingly shaping CapEx decisions across the industry.

What are the latest trends in the beer processing market?

Automation and Digital Integration

Breweries globally are integrating automation and IoT-enabled process control systems to enhance quality, improve efficiency, and reduce downtime. AI-based predictive analytics and real-time monitoring tools optimize fermentation, filtration, and packaging, resulting in consistent beer quality and lower operational costs. Craft breweries are also adopting modular automation to support small-batch variability while maintaining operational efficiency. Advanced sensors and cloud-based monitoring allow remote oversight of brewing processes, enhancing traceability and regulatory compliance.

Premiumization and Specialty Beers

Consumer demand is shifting toward specialty, craft, and premium beer varieties. This trend is driving breweries to invest in flexible processing lines capable of handling diverse ingredients, smaller batch sizes, and experimental recipes. Limited-edition flavors, seasonal variants, and non-alcoholic beer lines are fueling innovation in fermentation and filtration technologies. Packaging flexibility, such as cans for retail convenience and kegs for on-trade consumption, is also increasing to meet evolving consumer preferences.

What are the key drivers in the beer processing market?

Rising Craft Beer Consumption

The global surge in craft and specialty beer consumption is driving breweries to expand production capabilities and invest in flexible processing equipment. Regions like North America, Europe, and Asia Pacific are witnessing strong growth in microbreweries and craft operations. These segments prioritize quality, small-batch customization, and rapid recipe changeovers, pushing investment in modular brewhouse systems, precision fermentation tanks, and advanced filtration technologies.

Technological Advancements and Operational Efficiency

Automation, process digitization, and IoT adoption are key growth enablers. Smart breweries utilize sensors, PLC systems, and data-driven analytics to monitor every stage—from brewing and fermentation to packaging. Predictive maintenance reduces equipment downtime, while energy-efficient heat exchangers and water recycling solutions lower production costs and environmental impact. This technological integration is enhancing competitiveness and scalability in both macro and microbrewery segments.

What are the restraints for the global market?

High Capital Expenditure

Advanced beer processing equipment involves significant upfront investment, often limiting entry for smaller breweries. Capital-intensive brewhouses, automated filtration systems, and digital control platforms require substantial financing, particularly for new entrants and craft operators aiming to scale production without compromising quality.

Raw Material Price Volatility

Beer production relies on key commodities such as barley, malt, hops, and yeast, which are subject to global price fluctuations. Climate variability, crop yields, and trade policies impact input costs, affecting profitability and operational planning for breweries. Price volatility also constrains CapEx decisions and slows expansion in emerging markets.

What are the key opportunities in the beer processing industry?

Emerging Markets Expansion

Asia Pacific, Africa, and Latin America present significant growth potential. Rapid urbanization, rising disposable income, and growing beer culture in countries such as China, India, and Brazil are creating demand for modern processing facilities. Breweries are investing in localized infrastructure, tapping export potential, and adapting equipment to regional beer styles.

Non-Alcoholic and Low-Alcohol Beer Trends

The rising consumer focus on health and wellness has fueled demand for non-alcoholic and low-alcohol beer variants. Breweries are investing in specialized fermentation techniques, filtration, and product differentiation, opening new market segments and revenue streams while complying with regulatory requirements across multiple geographies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 835.00 Billion |

| Market Size in 2026 | USD 868.40 Billion |

| Market Size in 2031 | USD 1056.54 Billion |

| CAGR | 4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The brewing and fermentation segment continues to represent the technological backbone of the global beer processing market, accounting for approximately 38% of the total market share in 2025. Growth in this segment is primarily supported by increasing investments in process optimization, automation integration, and consistency-focused production systems. Breweries across both macro and craft categories are prioritizing advanced brewhouses, modular brewing platforms, precision-controlled fermenters, and high-efficiency filtration systems to improve yield, reduce operational waste, and ensure standardized flavor profiles. The leading driver for this segment is the industry-wide transition toward automated and scalable brewing operations that enable producers to balance high-volume production with product innovation. Modern fermentation systems equipped with temperature monitoring, digital analytics, and predictive maintenance capabilities are increasingly deployed to minimize downtime and improve batch reproducibility.Packaging equipment, particularly canning systems, represents another critical product category, holding nearly 40% share among packaging formats. The strong performance of this segment is driven by shifting consumer preferences toward portable, sustainable, and lightweight packaging solutions. Aluminum cans provide extended shelf life, improved logistics efficiency, and recyclability advantages, encouraging breweries to upgrade processing lines with high-speed filling and sealing technologies. Specialty and craft beer equipment is also witnessing significant expansion as breweries invest in flexible and small-footprint systems capable of supporting limited-edition releases, seasonal variations, and diversified product portfolios. As competition intensifies, equipment capable of quick changeovers and multi-style production is becoming increasingly essential, strengthening demand for adaptable processing infrastructure globally.

Application Insights

The on-trade commercial HORECA segment, encompassing hotels, restaurants, pubs, and bars, remains the dominant application area for processed beer consumption and production planning. The leading growth driver for this segment is the continued recovery and expansion of experiential consumption trends, where consumers increasingly favor freshly served and premium beverages in social environments. Breweries are therefore investing in processing technologies that enhance freshness retention, keg efficiency, and draft quality management. Advanced quality-control systems and hygienic processing standards are becoming central to meeting on-premise service expectations.Off-trade retail channels, including supermarkets, hypermarkets, and rapidly expanding e-commerce platforms, are steadily increasing their share of processed beer demand. Growth in this segment is supported by changing purchasing behaviors, convenience-oriented consumption, and the expansion of organized retail networks in emerging economies. Breweries are adapting production planning toward packaged formats optimized for long-distance distribution and extended shelf stability. Craft and specialty beer applications are expanding at a faster pace than traditional categories, driven by consumer experimentation, premiumization, and localized flavor innovation. These trends require adaptable processing lines capable of handling varied ingredients, fermentation durations, and smaller batch sizes without compromising efficiency.Export-oriented brewing operations represent an increasingly important application area as global trade in premium and craft beers expands. Producers targeting international markets are investing in advanced pasteurization, filtration, and quality assurance technologies to comply with regulatory standards and maintain product consistency across long supply chains. This growing emphasis on export readiness continues to accelerate modernization across brewing facilities worldwide.

Distribution Channel Insights

Distribution channels within the beer processing ecosystem are evolving alongside digital transformation and shifting consumer engagement models. Online and direct-to-consumer sales channels are gaining importance, particularly among craft breweries seeking to establish direct brand relationships and reach niche audiences beyond geographic limitations. The leading driver for this segment is the rapid adoption of digital commerce platforms that enable personalized marketing, subscription-based beer delivery models, and data-driven consumer insights. Breweries are increasingly aligning production planning with online demand forecasting, allowing more efficient inventory management and reduced distribution inefficiencies.Despite the growth of digital channels, traditional distributor networks and retail partnerships continue to dominate volume sales, especially for large-scale breweries. Established logistics infrastructure, cold-chain capabilities, and retail shelf presence remain essential for maintaining market penetration at scale. Hybrid distribution models combining physical retail strength with digital engagement strategies are emerging as the preferred approach, allowing breweries to diversify revenue streams while enhancing brand loyalty. Investments in smart distribution technologies, including demand analytics and automated supply-chain integration, are further supporting market expansion and operational efficiency.

Explore more data points, trends and opportunities Download Free Sample Report

Beer Processing Market Segmentations

By Processing Stage

- Malting & Milling

- Brewing

- Fermentation

- Maturation

- Filtration & Clarification

- Packaging & Filling

- Quality Control & Testing

By Equipment Type

- Brew House Systems

- Fermenters & Bright Beer Tanks

- Filtration & Centrifuge Systems

- Heat Exchangers

- Cooling & Refrigeration Equipment

- Filling & Packaging Lines

- Automation & Control Systems

By Beer Type

- Lager

- Ale

- Stout & Porters

- Specialty & Craft Beers

- Low-Alcohol & Non-Alcoholic Beers

By Packaging Format

- Cans

- Bottles

- Kegs & Draught Systems

By Distribution Channel

- Commercial HORECA

- Retail & Supermarkets

- E-Commerce & Direct to Consumer

- On-Trade vs Off-Trade Channels

Regional Insights

North America

North America accounts for approximately 27% of the global beer processing market, supported by strong demand across the United States and Canada. Regional growth is driven primarily by high craft brewery density, consumer preference for premium and flavored beer varieties, and widespread adoption of automation technologies. Breweries in this region are early adopters of digital brewing systems, AI-enabled monitoring, and sustainability-focused processing solutions aimed at reducing water and energy consumption. Additionally, robust on-trade consumption recovery, strong purchasing power, and continuous product innovation encourage ongoing capital investment in advanced brewing and packaging infrastructure. Regulatory emphasis on quality assurance and traceability further strengthens demand for modern processing equipment.

Europe

Europe represents nearly 30% of the global market, supported by a long-established brewing heritage combined with technological modernization. Countries such as Germany, the United Kingdom, and Spain continue to lead demand for high-efficiency brewing systems designed to maintain traditional beer quality while improving production sustainability. Regional growth is strongly driven by environmental regulations encouraging energy-efficient equipment, water recycling technologies, and carbon-reduction initiatives within breweries. The expansion of craft breweries and microbreweries across Western and Eastern Europe is also stimulating demand for compact and flexible processing solutions. Increasing consumer interest in specialty, organic, and low-alcohol beer varieties further promotes innovation in fermentation and processing technologies.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, accounting for approximately 32% market share. Growth is fueled by rapid urbanization, rising disposable incomes, and expanding middle-class populations across China, India, Japan, and Southeast Asia. Increasing westernization of consumption habits and growing youth demographics are accelerating beer consumption volumes, prompting breweries to expand production capacity. Regional governments’ support for manufacturing modernization and foreign investments in beverage production facilities are also encouraging adoption of advanced processing technologies. The emergence of local craft beer cultures in metropolitan cities, combined with expanding retail infrastructure and e-commerce penetration, is creating sustained demand for flexible brewing systems capable of serving both mass and premium segments.

Latin America

Latin America is experiencing gradual yet consistent growth in beer processing demand, led by Brazil, Mexico, and Argentina. Regional expansion is primarily driven by rising urban populations, increasing social consumption trends, and growing popularity of affordable lager varieties. Breweries are investing in cost-efficient processing systems to enhance production scalability while maintaining competitive pricing. Improvements in retail distribution networks and expanding tourism industries are further contributing to consumption growth. Additionally, multinational brewery investments and modernization initiatives are supporting technology upgrades across local production facilities, strengthening long-term market potential.

Middle East & Africa

The Middle East & Africa region presents emerging opportunities supported by demographic expansion, tourism development, and evolving consumer preferences. Africa hosts several major beer production hubs, including South Africa and Nigeria, where favorable agricultural resources and expanding urban populations drive local manufacturing growth. Investments in modern brewing infrastructure are increasing as producers aim to improve efficiency and product quality. In the Middle East, markets such as the United Arab Emirates and Saudi Arabia are witnessing gradual growth driven by high-income consumer segments, premium hospitality sectors, and luxury tourism activities. Regulatory adaptations and diversification within beverage offerings are encouraging breweries to adopt advanced processing technologies tailored to premium and specialty product categories, supporting steady regional expansion.

Key Players in the Beer Processing Market

- Anheuser-Busch InBev

- Heineken N.V.

- Carlsberg Group

- Molson Coors Beverage Company

- Diageo PLC

- Asahi Group Holdings Ltd.

- Constellation Brands Inc.

- United Breweries Ltd.

- GEA Group AG

- Alfa Laval AB

- Krones AG

- Mahou San Miguel Group

- The Boston Beer Company Inc.

- Sierra Nevada Brewing Co.

- Sapporo Breweries Ltd.