Beans and Legumes Market Size

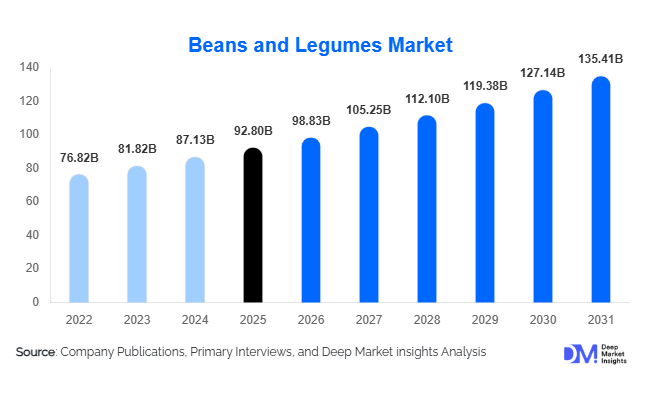

According to Deep Market Insights, the global beans and legumes market size was valued at USD 92.8 billion in 2025 and is projected to grow from USD 98.83 billion in 2026 to reach USD 135.41 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The beans and legumes market growth is primarily driven by rising plant-based protein consumption, increasing demand for sustainable agricultural commodities, and expanding applications across food processing, animal nutrition, and functional food industries. Growing consumer awareness regarding nutritional benefits such as high protein, fiber, and micronutrient content has strengthened global adoption across both developed and emerging economies.

Key Market Insights

- Plant-based diets and flexitarian consumption trends are significantly increasing global demand for pulses and legumes as alternative protein sources.

- Asia-Pacific dominates global production and consumption, supported by dietary dependence and large agricultural output.

- Processed and packaged legumes are growing faster than bulk dry products due to convenience-driven urban consumption.

- Government food security programs are supporting pulse cultivation and trade stability worldwide.

- Export demand from protein-deficit regions such as the Middle East and Europe is accelerating international trade volumes.

- Technological improvements in seed genetics and storage are reducing post-harvest losses and improving yields.

What are the latest trends in the beans and legumes market?

Shift Toward Plant-Based Protein Ingredients

Food manufacturers increasingly use beans and legumes as core ingredients in meat alternatives, dairy substitutes, and protein-enriched snacks. Pea protein, chickpea flour, lentil isolates, and bean concentrates are now widely incorporated into processed foods due to their functional and nutritional properties. The rise of vegan and flexitarian consumers across North America and Europe has accelerated innovation in pulse-based formulations. Manufacturers are investing heavily in protein extraction technologies to produce high-purity isolates for use in ready-to-eat meals, sports nutrition, and fortified foods. This trend has elevated legumes from traditional staples to high-value functional ingredients within global food innovation pipelines.

Growth of Ready-to-Cook and Convenience Formats

Urbanization and changing lifestyles have boosted demand for canned beans, pre-cooked lentils, frozen legumes, and instant pulse mixes. Consumers increasingly seek convenience without compromising nutrition, encouraging retailers and food brands to expand value-added offerings. Packaging innovation, including vacuum sealing and retort processing, has improved shelf life while maintaining nutritional quality. E-commerce platforms are further accelerating sales of packaged legumes, particularly in urban Asia and North America, where consumers prefer easy meal preparation solutions aligned with healthy eating habits.

What are the key drivers in the beans and legumes market?

Rising Global Demand for Affordable Protein

Beans and legumes represent one of the most cost-effective protein sources globally. With rising meat prices and growing awareness of sustainable diets, consumers are shifting toward plant-based protein consumption. Governments and international organizations are promoting pulses as part of nutritional security strategies, particularly in developing economies. Increased inclusion of legumes in institutional food programs and school nutrition schemes has further expanded consumption volumes.

Expansion of Sustainable Agriculture Practices

Legumes play a critical role in regenerative agriculture through nitrogen fixation, soil health improvement, and reduced fertilizer dependency. Farmers are increasingly integrating pulses into crop rotation systems to improve soil productivity and reduce environmental impact. Sustainability certifications and climate-smart farming initiatives are encouraging large-scale cultivation across India, Canada, Australia, and Africa, strengthening long-term supply stability.

Growth in Food Processing and Ingredient Applications

The processed food industry is driving large-scale demand for chickpeas, lentils, and peas used in flour blends, snacks, and protein ingredients. Food manufacturers favor legumes due to clean-label positioning and allergen-friendly characteristics compared to soy or dairy proteins. Investments in pulse fractionation facilities globally have significantly expanded industrial utilization.

What are the restraints for the global market?

Price Volatility and Climate Dependency

Production remains heavily dependent on weather conditions, making supply vulnerable to droughts, floods, and changing climate patterns. Yield fluctuations create pricing instability, affecting procurement planning for processors and exporters.

Supply Chain and Storage Constraints

Post-harvest losses due to inadequate storage infrastructure remain a challenge in developing regions. Limited cold chain systems and inefficient logistics increase spoilage risks and reduce export competitiveness, particularly in Africa and parts of Asia.

What are the key opportunities in the beans and legumes industry?

Plant-Based Food Innovation

The rapid expansion of plant-based meat and dairy alternatives presents a major opportunity for pulse producers and processors. Companies entering protein isolate manufacturing or ingredient processing can capture higher margins compared to commodity trading. Rising investments in alternative protein technologies are expected to expand premium product categories globally.

Export Expansion into Protein-Deficit Markets

Regions such as the Middle East, Europe, and parts of Southeast Asia rely heavily on imports to meet protein demand. Export-oriented producers in Canada, India, and Australia can benefit from increasing trade agreements and growing demand for affordable plant proteins. Improved logistics corridors and trade partnerships are further supporting export growth.

Government Food Security Programs

National initiatives promoting pulse cultivation offer long-term growth opportunities. Programs supporting minimum support prices, seed innovation, and farmer subsidies are encouraging acreage expansion. Public procurement for nutrition schemes also ensures stable demand, reducing market risk for producers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 92.8 Billion |

| Market Size in 2026 | USD 98.83 Billion |

| Market Size in 2031 | USD 135.41 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global beans and legumes market is characterized by a diverse product portfolio, with dry beans and legumes dominating the landscape, accounting for approximately 48% of the global market share in 2025. This dominance is largely attributed to their affordability, nutritional richness, and long shelf life, which make them a staple in households across Asia, Africa, and Latin America. Among dry beans, chickpeas have emerged as the fastest-growing category, propelled by increasing consumer interest in plant-based diets, the rising popularity of hummus, and the expansion of innovative snack offerings that integrate chickpeas as a protein-rich ingredient. Lentils, contributing nearly 18% of the market share, maintain consistent demand due to their essential role in traditional cuisines across South Asia and the Middle East.Processed and canned legumes are witnessing growing traction, particularly in North America and Europe, where convenience-oriented lifestyles drive consumer preference for ready-to-use options. The rise of urban households, dual-income families, and time-sensitive meal preparation needs has accelerated the adoption of these products. Additionally, the fortification of processed legumes with nutrients, the development of gluten-free and organic variants, and the expansion of ready-to-cook meal kits further bolster their market penetration. This combination of affordability, health appeal, and convenience continues to support the steady growth of the dry and processed legumes segment globally.

Application Insights

Human food consumption remains the largest application for beans and legumes, accounting for nearly 72% of global demand in 2025. The traditional use of pulses in daily meals continues to drive volume consumption, especially in regions with strong dietary dependence on plant proteins. The food processing segment is witnessing the fastest growth as manufacturers increasingly incorporate pulse flours, protein isolates, and legume-derived ingredients into packaged foods, bakery products, and plant-based beverages. This trend is particularly notable in North America and Europe, where health-conscious consumers actively seek protein-rich and functional foods.Animal feed applications are steadily expanding, fueled by growing livestock, poultry, and aquaculture sectors in Asia-Pacific and South America. Legumes serve as an economical and nutrient-dense source of protein, improving feed efficiency and supporting sustainable animal husbandry practices. Additionally, emerging applications in the development of plant-based protein ingredients, including protein powders, bars, and meat alternatives, are reshaping market dynamics and opening avenues for product innovation across diverse applications. The convergence of nutrition, sustainability, and consumer awareness continues to underpin demand growth across multiple applications.

Distribution Channel Insights

Distribution channels play a pivotal role in shaping market reach and consumer accessibility. Offline retail, encompassing supermarkets, hypermarkets, traditional grocery stores, and wholesale markets, dominates sales, accounting for approximately 63% of total sales globally. This strong presence is reinforced in developing economies where bulk purchasing, price sensitivity, and familiarity with traditional retail channels encourage continued reliance on physical stores. Supermarkets also serve as platforms for promoting processed and packaged legumes through marketing campaigns, sampling programs, and loyalty initiatives.Conversely, online retail is emerging as the fastest-growing distribution channel, driven by the expansion of digital grocery platforms, e-commerce marketplaces, and direct-to-consumer subscription models. In North America, Europe, and parts of Asia-Pacific, online sales of legumes and pulses are benefiting from the convenience of doorstep delivery, curated product offerings, and the ability to compare prices and nutritional information digitally. Brands are increasingly leveraging digital marketing, social media promotions, and influencer partnerships to reach niche consumer segments, such as health-conscious individuals and urban millennials, thereby accelerating growth through online channels. The synergy between offline trust and online convenience continues to create a multi-channel ecosystem for product accessibility and consumer engagement.

End-Use Insights

Household consumption represents the largest end-use segment, holding nearly 55% market share in 2025, driven by the role of beans and legumes as dietary staples in regions such as Asia, Africa, and Latin America. Cultural food habits, rising population, and increasing awareness of protein-rich diets sustain household demand. Simultaneously, the food manufacturing segment is emerging as the fastest-growing end-use category, fueled by the surge in plant-based product innovation, functional foods, and packaged offerings enriched with legume proteins. Processors are increasingly integrating pulses into snacks, bakery items, protein powders, and dairy alternatives, responding to consumer preferences for high-protein, low-fat, and fiber-rich products.Export-oriented demand is also strengthening, with European and Middle Eastern manufacturers sourcing high-quality pulses from Asia-Pacific and North America. Institutional buyers, including government nutrition programs, schools, and hospitals, are contributing to consistent bulk procurement, supporting both domestic consumption and international trade. The integration of legumes into public nutrition strategies, food aid programs, and fortified food initiatives further diversifies end-use applications and drives market expansion across regions.

Explore more data points, trends and opportunities Download Free Sample Report

Beans and Legumes Market Segmentations

By Product Type

- Dry Beans

- Lentils

- Chickpeas

- Peas

- Processed & Canned Legumes

- Legume Flours & Protein Ingredients

By Application

- Human Food Consumption

- Food Processing & Packaged Foods

- Animal Feed

- Plant-Based Protein Ingredients

- Institutional & Government Nutrition Programs

By Distribution Channel

- Offline Retail

- Online Retail & E-commerce Platforms

- Direct B2B Procurement

- Foodservice & Institutional Supply

- Export & Commodity Trading Channels

By End-Use

- Household Consumption

- Food Manufacturing Industry

- Foodservice Industry

- Animal Nutrition Industry

Regional Insights

Asia-Pacific

Asia-Pacific emerges as the global leader in the beans and legumes market, commanding approximately 46% of the global market share in 2025. India stands as the largest consumer and producer in the region, with pulses forming a fundamental component of daily diets. The government’s initiatives to enhance pulse production, coupled with initiatives such as minimum support prices and distribution through public food programs, continue to underpin strong domestic demand. China, while a significant producer of some legumes, increasingly relies on imports to support its growing food processing and plant-based product industries. The rising popularity of vegetarian and vegan diets, urbanization, and increasing disposable income in Southeast Asian countries are also key drivers, creating new opportunities for premium and processed legumes. Australia plays a strategic role as a global export hub, supplying lentils, chickpeas, and specialty beans to markets in the Middle East, Asia, and Europe. Infrastructure development, advancements in irrigation, and adoption of modern agricultural technologies further strengthen the region’s production capacity and competitive advantage in the global market.

North America

North America accounts for nearly 17% of global demand, with the United States and Canada being central to market dynamics. Canada is recognized as one of the world’s largest exporters of lentils, peas, and chickpeas, benefiting from vast arable land, government support programs, and technological innovations in crop management. The U.S., on the other hand, drives domestic consumption through growing plant-based food innovation and increasing adoption of health-conscious diets. Trends such as veganism, flexitarian eating patterns, and high-protein snack preferences are significantly influencing consumer behavior. Additionally, sustainability initiatives, regenerative agriculture practices, and local sourcing of pulses contribute to regional market growth. North America’s advanced supply chain, processing capabilities, and marketing infrastructure facilitate both domestic consumption and export-led expansion, establishing the region as a key growth contributor to the global market.

Europe

Europe represents approximately 15% of global market share, with strong import dependence due to limited domestic pulse production. Germany, France, Italy, and the United Kingdom lead consumption, driven by increasing awareness of sustainable diets, organic produce, and plant-based protein alternatives. Premium food product development, including organic, non-GMO, and fortified legumes, is shaping regional demand. The rise of functional foods, vegan diets, and the promotion of legumes in national dietary guidelines contribute to steady market expansion. Furthermore, import of high-quality pulses from Canada, Australia, and Asia-Pacific strengthens the food manufacturing sector, particularly in snacks, ready-to-eat meals, and plant-based protein formulations. European consumers’ growing preference for clean-label, ethically sourced, and environmentally sustainable products reinforces the adoption of legumes as both a household staple and an industrial ingredient.

Middle East & Africa

The Middle East and Africa display diverse market dynamics. The Middle East is highly reliant on imports, with Turkey, UAE, and Saudi Arabia serving as major trading hubs. Rising demand is influenced by urbanization, expatriate populations, and growing interest in convenient and nutrient-dense food options. Legumes are increasingly incorporated into processed foods, ready-to-cook meals, and modern snack innovations, reflecting changing lifestyles. In Africa, production potential is growing, particularly in Ethiopia, Nigeria, and Kenya, supported by agricultural development programs, government subsidies, and improved seed quality initiatives. Population growth, urban expansion, and increasing disposable income drive consumption, while export opportunities from African producers are enhancing regional trade. Investments in cold storage, transport logistics, and processing infrastructure are further enabling the region to meet both domestic and international demand efficiently.

Latin America

Latin America demonstrates steady and stable demand, led by Brazil, Mexico, and Argentina, where beans remain a central element of daily diets and traditional cuisine. While household consumption dominates, there is growing interest in specialty legumes and processed products, particularly in urban centers and emerging middle-class segments. Brazil and Argentina serve as significant exporters of beans and chickpeas, benefiting from favorable climatic conditions and large-scale cultivation practices. The development of legume processing facilities, government initiatives supporting crop diversification, and increased investment in food innovation contribute to both domestic market stability and export potential. Furthermore, the rise of packaged, ready-to-cook legume products, coupled with increasing awareness of protein-rich diets, is gradually transforming consumption patterns and offering growth opportunities across the region.

Key Players in the Beans and Legumes Market

- Archer Daniels Midland Company (ADM)

- Cargill Incorporated

- Bunge Limited

- AGT Food and Ingredients

- Olam Group

- Louis Dreyfus Company

- Viterra

- Ingredion Incorporated

- Roquette Frères

- The Scoular Company

- SunOpta Inc.

- Parrish & Heimbecker

- Goya Foods

- BroadGrain Commodities

- Best Cooking Pulses Inc.